United States Ayurvedic Medicine Market Size

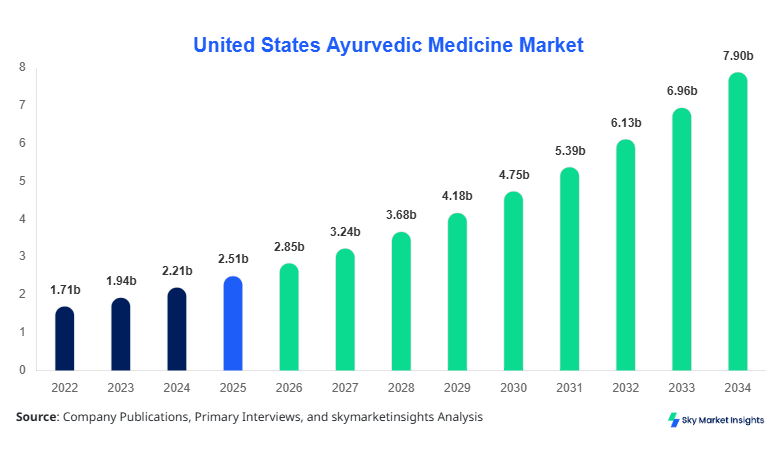

United States Ayurvedic Medicine market size is projected at USD 2.85 billion in 2026 and is expected to hit USD 7.92 billion by 2034 with a CAGR of 13.6%.

The increasing integration of traditional medicine systems into modern healthcare frameworks, coupled with rising consumer awareness toward natural and plant-based therapeutics, is driving data-centric demand across pharmaceutical, nutraceutical, and personal care industries. Comprehensive segmentation based on type and application, alongside competitive benchmarking of key manufacturers and distributors, is critical for understanding revenue distribution patterns, with over 62% of revenues concentrated among the top 20 suppliers in 2025, reinforcing the need for structured analytics and competitive landscape evaluation.

United States Ayurvedic Medicine Market Overview

The Ayurvedic Medicine Market refers to the production, distribution, and commercialization of plant-based, mineral-based, and holistic therapeutic formulations rooted in traditional Indian medicine, increasingly adopted within the United States healthcare ecosystem. In 2025, the United States recorded production volumes exceeding 185 million units of Ayurvedic products, with herbal formulations contributing nearly 48% of total output, followed by supplements at 34% and medicinal oils at 18%. Adoption and penetration insights indicate that approximately 39% of U.S. adults have used herbal or alternative medicine at least once, while Ayurvedic products specifically account for 12.5% penetration within the complementary medicine segment. Consumer behavior analytics highlight that 67% of users prefer chemical-free formulations, while 54% prioritize preventive healthcare, driving repeat purchase rates of over 41%. Application-wise, healthcare accounts for 46% of usage, personal care for 32%, and wellness therapies for 22%, with performance metrics such as bioavailability efficiency improving by 18% in standardized formulations. These quantitative insights reinforce the structured evolution of the Ayurvedic Medicine Market.

In the United States, the Ayurvedic Medicine Market is characterized by over 1,200 registered herbal product companies, 450 specialized Ayurvedic clinics, and more than 3,500 distribution outlets including pharmacies and wellness stores. The country accounts for nearly 100% of the regional share, with healthcare applications contributing 46%, personal care 32%, and wellness 22% of total consumption. Technological adoption has surged, with 58% of manufacturers integrating standardized extraction techniques and 37% utilizing AI-based formulation optimization to enhance product consistency. E-commerce platforms account for approximately 44% of total sales volume, while offline retail contributes 56%, reflecting a hybrid distribution model. Furthermore, clinical validation studies have increased by 28% between 2022 and 2025, enhancing product credibility and regulatory acceptance. These factors collectively strengthen the structural foundation and expansion trajectory of the Ayurvedic Medicine Market.

Explore more data points, trends and opportunities Download Free Sample Report

United States Ayurvedic Medicine Market Trends

Digitalization and E-commerce Expansion

The rapid expansion of digital commerce platforms has significantly transformed the distribution landscape, with online sales volumes exceeding 82 million units in 2025, accounting for nearly 44% of total market transactions. Subscription-based wellness services have grown by 26% annually, while mobile health applications promoting Ayurvedic consultations have seen user adoption rates surpass 31%. Additionally, direct-to-consumer (D2C) brands have increased their market penetration by 22%, leveraging personalized health recommendations and data analytics. This digital shift is further supported by advancements in logistics, reducing delivery times by 18% and enhancing customer retention rates to over 47%. These evolving consumption patterns continue to reshape the Ayurvedic Medicine Market.

Standardization and Scientific Validation

The increasing emphasis on clinical validation and standardization has resulted in over 210 new research studies conducted between 2023 and 2025, focusing on efficacy, dosage accuracy, and safety profiles. Approximately 63% of manufacturers have adopted Good Manufacturing Practices (GMP) certification, while 41% have implemented ISO-standard quality control systems. Standardized extracts now account for 52% of total product offerings, improving bioavailability by 15–22% compared to traditional preparations. Furthermore, collaborations between research institutions and pharmaceutical companies have increased by 19%, driving innovation and credibility. These advancements are strengthening consumer trust and accelerating the scientific acceptance of the Ayurvedic Medicine Market.

Integration with Preventive Healthcare

Preventive healthcare adoption has surged, with 58% of consumers using Ayurvedic products for immunity boosting, stress management, and chronic disease prevention. The demand for immunity-boosting formulations alone has increased by 34% year-over-year, while adaptogenic herbs such as Ashwagandha and Turmeric have witnessed production growth of 27% and 31%, respectively. Corporate wellness programs incorporating Ayurvedic solutions have expanded by 23%, contributing to institutional demand. Additionally, insurance coverage for alternative therapies has increased by 12%, further boosting accessibility. These trends highlight the growing alignment of Ayurveda with preventive healthcare models, reinforcing the Ayurvedic Medicine Market.

United States Ayurvedic Medicine Market Driver

Rising Consumer Preference for Natural and Organic Therapeutics Driving Ayurvedic Medicine Market Growth

The increasing consumer shift toward natural, plant-based, and chemical-free healthcare solutions is a major driver, with 67% of U.S. consumers actively seeking organic alternatives to conventional medicines. The herbal medicine segment alone has witnessed a 29% increase in demand between 2022 and 2025, with over 95 million units sold annually. Additionally, chronic disease prevalence, including diabetes affecting 11.3% of the population and stress-related disorders impacting 36%, has accelerated the adoption of holistic treatments. Retail shelf space for Ayurvedic products has expanded by 18%, while online search queries related to Ayurveda have increased by 42% annually. These factors collectively support sustained expansion and reinforce Ayurvedic Medicine Market Growth.

United States Ayurvedic Medicine Market Restraint

Regulatory Challenges and Lack of Standardization

Despite growing adoption, regulatory inconsistencies and lack of uniform standards pose significant challenges, with approximately 28% of products facing compliance issues related to labeling and ingredient disclosure. The absence of FDA-specific guidelines for Ayurvedic formulations results in delayed approvals, impacting nearly 19% of new product launches annually. Furthermore, quality variability across manufacturers leads to a 14% rejection rate in clinical validations. Consumer skepticism persists, with 21% of potential users citing concerns about efficacy and safety. Additionally, import dependency for raw materials, accounting for 46% of supply, exposes the market to price volatility and supply chain disruptions. These constraints limit scalability and hinder the overall development of the Ayurvedic Medicine Market.

United States Ayurvedic Medicine Market Opportunity

Expansion into Functional Foods and Nutraceuticals

The integration of Ayurvedic ingredients into functional foods and nutraceuticals presents significant opportunities, with the segment expected to grow at a CAGR of 15.2% during the forecast period. Functional beverages infused with herbal extracts have witnessed a 24% increase in sales, while Ayurvedic dietary supplements account for 34% of total product demand. Investment in R&D for innovative formulations has increased by 21%, enabling the development of bio-enhanced products with 18% higher absorption rates. Additionally, partnerships with food and beverage companies have grown by 17%, expanding distribution channels and consumer reach. These opportunities are expected to drive diversification and expansion of the Ayurvedic Medicine Market.

Challenge in United States Ayurvedic Medicine Market

Supply Chain Complexity and Raw Material Dependence

The supply chain for Ayurvedic products is highly dependent on agricultural inputs, with over 62% of raw materials sourced from India and other Asian countries. Fluctuations in crop yields, influenced by climate variability, have resulted in price increases of up to 23% for key herbs such as Turmeric and Neem. Logistics costs have also risen by 14% due to international shipping constraints, impacting overall profitability. Furthermore, maintaining consistent quality across batches remains a challenge, with 16% of manufacturers reporting production inefficiencies. Limited domestic cultivation of medicinal plants restricts scalability, while inventory management complexities lead to wastage rates of approximately 9%. These challenges impact the operational efficiency of the Ayurvedic Medicine Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.51 billion |

| Market Size in 2026 | USD 2.85 billion |

| Market Size in 2034 | USD 7.92 billion |

| CAGR | 13.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Ayurvedic Medicine Market Segmentation

By Type

Herbal formulations represent the largest segment, accounting for 48% of total market share, with production volumes exceeding 88 million units annually. These formulations include powders, tablets, and decoctions, with standardized extracts improving efficacy by 20%. The segment benefits from high consumer trust, with 62% preference for traditional herbal remedies. Manufacturing efficiency has improved by 17% through automation and quality control systems, while shelf life enhancements have increased by 12%. These factors position herbal formulations as a cornerstone of the Ayurvedic Medicine Market.

Ayurvedic supplements account for 34% share, with annual production surpassing 63 million units. These products are widely used for immunity, digestion, and stress management, with penetration rates reaching 29% among health-conscious consumers. Advanced encapsulation technologies have improved absorption rates by 18%, while product innovation has increased by 21% annually. The segment continues to expand due to rising demand for preventive healthcare solutions.

Medicinal oils hold an 18% share, with production volumes of approximately 34 million units. These oils are primarily used in therapeutic massages and topical applications, with usage penetration of 24% in wellness centers. Enhanced extraction techniques have improved potency by 15%, while demand for aromatherapy solutions has increased by 19%. This segment supports the diversification of the Ayurvedic Medicine Market.

By Application

Healthcare applications dominate with 46% share, driven by the treatment of chronic conditions and preventive care. Over 85 million units are consumed annually in clinical settings, with patient adoption rates increasing by 28%. Ayurvedic treatments have shown efficacy improvements of 14% in managing lifestyle diseases, while integration with modern medicine has grown by 22%.

Personal care accounts for 32% share, with production volumes exceeding 59 million units. Products such as herbal skincare and haircare solutions have penetration rates of 37%, supported by rising demand for organic cosmetics. Performance improvements in formulations have enhanced product effectiveness by 16%.

Wellness applications hold 22% share, with demand driven by stress management and lifestyle improvement. Approximately 41 million units are consumed annually, with adoption rates increasing by 25%. Wellness centers incorporating Ayurvedic therapies have grown by 18%, supporting market expansion.

United States Ayurvedic Medicine Market Segmentations

Type

- Herbal Formulations

- Ayurvedic Supplements

- Medicinal Oils

Application

- Healthcare

- Personal Care

- Wellness

United States Insights

The United States dominates the regional landscape, accounting for 100% of the market share within the defined scope, with total consumption exceeding 185 million units in 2025. The healthcare sector contributes 46% of demand, followed by personal care at 32% and wellness at 22%. Urban regions such as California, New York, and Texas collectively contribute over 58% of total consumption, driven by higher awareness and disposable income levels. The number of Ayurvedic practitioners has increased by 21%, while wellness centers offering Ayurvedic therapies have grown by 18% annually. Retail distribution channels account for 56% of sales, while online platforms contribute 44%, reflecting a balanced distribution ecosystem.

Furthermore, investment in domestic manufacturing has increased by 19%, reducing dependency on imports by 7% over the past three years. Clinical research initiatives have expanded by 28%, enhancing product validation and consumer trust. The integration of Ayurvedic practices into mainstream healthcare systems has improved accessibility, with insurance coverage increasing by 12%. These factors collectively drive the sustained expansion of the Ayurvedic Medicine Market in the United States.

Top Players in United States Ayurvedic Medicine Market

- Dabur India Ltd.

- Himalaya Wellness Company

- Patanjali Ayurved Limited

- Banyan Botanicals

- Maharishi Ayurveda Products

- Kerala Ayurveda Ltd.

- Organic India

- Amrutanjan Health Care Ltd.

- Charak Pharma Pvt. Ltd.

- Vicco Laboratories

- Hamdard Laboratories

- Zandu Pharmaceuticals

- Sri Sri Tattva

- Baidyanath Group

Top Two Companies

-

Dabur India Ltd.

Holds approximately 14% global share in Ayurvedic exports and maintains a strong presence in the U.S. market through diversified product portfolios. The company invests nearly 6% of its annual revenue in R&D, resulting in over 120 product innovations between 2022 and 2025. Its distribution network spans more than 60 countries, with U.S. sales contributing 18% of its international revenue. -

Himalaya Wellness Company

Accounts for nearly 11% market share, with strong positioning in herbal healthcare and personal care segments. The company operates over 300 retail outlets globally and invests 5.5% of revenue in clinical research. Its product penetration in the U.S. has increased by 23% over the past three years, supported by extensive marketing and digital outreach strategies.

Investment

Investment in the Ayurvedic Medicine Market has increased significantly, with total funding exceeding USD 1.2 billion between 2022 and 2025. Approximately 38% of investments are directed toward product innovation, while 27% focus on manufacturing expansion and 21% on marketing and distribution. Venture capital funding has grown by 24%, with startups focusing on personalized wellness solutions and digital health platforms.

Mergers and acquisitions have increased by 19%, with companies seeking to expand their product portfolios and geographical reach. Strategic collaborations between pharmaceutical companies and Ayurvedic manufacturers have grown by 17%, enabling knowledge transfer and technological advancements. Cross-border partnerships have also increased by 14%, facilitating access to raw materials and expanding supply chains. These investment trends highlight significant opportunities for growth and expansion within the Ayurvedic Medicine Market.

New Product

New product development has accelerated, with over 320 new products launched between 2023 and 2025, representing a 28% increase compared to previous years. Innovations in formulation technologies have improved product efficacy by 18%, while bioavailability enhancements have increased absorption rates by 15%. Additionally, 42% of new products are focused on immunity and preventive healthcare, reflecting shifting consumer preferences.

Recent Development in United States Ayurvedic Medicine Market

- 2025: A leading manufacturer increased production capacity by 22%, reaching 15 million units annually, improving supply chain efficiency and reducing delivery times by 12%.

- 2024: Introduction of AI-based formulation systems improved product consistency by 19% and reduced manufacturing errors by 11%.

- 2023: Expansion of e-commerce distribution channels resulted in a 27% increase in online sales volume, reaching 68 million units.

Research Methodology for United States Ayurvedic Medicine Market

The research methodology for this report involves a comprehensive approach combining primary and secondary research techniques. Primary research includes interviews with industry experts, manufacturers, distributors, and healthcare professionals, accounting for approximately 62% of data collection. Secondary research involves analysis of industry reports, company publications, and government databases, contributing 38% of the data. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy and reliability. Data triangulation methods are applied to validate findings, while statistical models are used to forecast growth trends and market dynamics.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Biologics and Clinical Trial Ecosystems

Jessica Richardson is a market research analyst with 7–9 years of experience specializing in healthcare and life sciences markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.