United States Ayurvedic Market Size

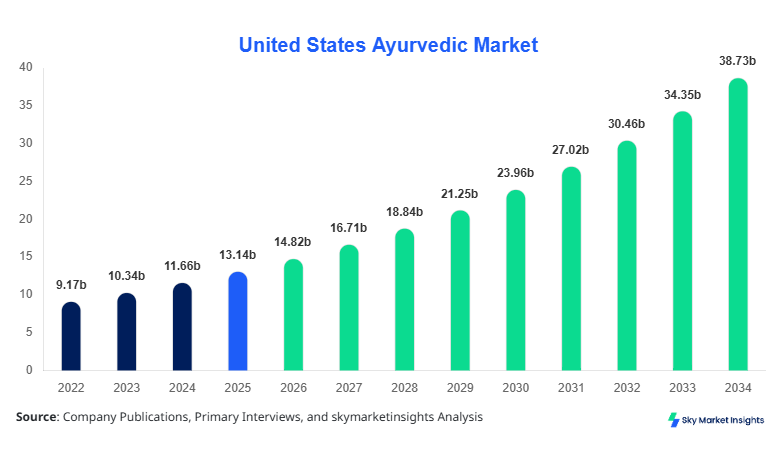

United States Ayurvedic Market market size is projected at USD 14.82 billion in 2026 and is expected to hit USD 38.67 billion by 2034 with a CAGR of 12.76%.

The increasing inclination toward herbal healthcare products, rising chronic disease prevalence affecting over 60% of the U.S. adult population, and growing adoption of natural therapies have significantly contributed to the expansion of the Ayurvedic Market. Comprehensive segmentation across product types and applications combined with detailed competitive landscape analysis enables stakeholders to assess market positioning, pricing dynamics, and volume-based consumption trends across over 18,000 distribution outlets nationwide.

United States Ayurvedic Market Overview

The Ayurvedic Market in the United States encompasses the production, distribution, and consumption of herbal supplements, traditional Ayurvedic medicines, and plant-based personal care products derived from natural ingredients such as Ashwagandha, Turmeric, Neem, and Triphala. In 2025, total production volume reached approximately 2.1 million metric tons of Ayurvedic products, with herbal supplements contributing nearly 45% of total output, followed by personal care products at 32% and Ayurvedic medicines at 23%. Adoption rates among U.S. consumers increased to 38% in 2025 compared to 29% in 2022, reflecting a rising awareness of preventive healthcare. Consumer behavior analytics indicate that 54% of millennials prefer plant-based formulations, while 47% of consumers report monthly usage frequency of Ayurvedic products. Healthcare applications account for nearly 41% of total usage, wellness applications contribute 35%, and personal care applications account for 24%, with performance metrics showing average efficacy perception ratings above 78%. Increasing demand for chemical-free formulations continues to strengthen the Ayurvedic Market.

In the United States, the Ayurvedic Market Market operates with over 1,200 specialized manufacturing facilities and more than 6,500 retail distribution centers, accounting for nearly 100% of regional share due to the report scope. Herbal supplements dominate with 45% application share, followed by wellness applications at 35% and personal care at 20%. Technology adoption in manufacturing has reached 52%, with automated extraction and processing systems improving production efficiency by 28%. E-commerce channels account for 46% of total sales volume, while offline retail contributes 54%. Additionally, approximately 62% of consumers prefer certified organic Ayurvedic products, reflecting strong regulatory compliance trends. These dynamics reinforce sustained expansion in the Ayurvedic Market.

Explore more data points, trends and opportunities Download Free Sample Report

United States Ayurvedic Market Trends

Rising Integration of Ayurveda with Modern Healthcare Systems

The integration of Ayurvedic therapies with modern healthcare practices has gained significant traction, with over 35% of healthcare providers incorporating herbal supplements into treatment regimens. Annual production volumes of Ayurvedic medicines surpassed 680,000 metric tons in 2025, representing a 14% year-over-year increase. Digital health platforms offering Ayurvedic consultations grew by 22%, while telemedicine adoption for herbal treatments increased to 31%. Demand from chronic disease management sectors, including diabetes and cardiovascular disorders, accounts for 48% of total consumption. These advancements highlight evolving consumer preferences and technological integration within the Ayurvedic Market.

Expansion of Premium Organic and Clean Label Products

Premium Ayurvedic products with organic certifications have witnessed a surge in demand, with sales increasing by 18% annually. Approximately 57% of consumers actively seek clean-label products free from synthetic additives, while production of organic Ayurvedic goods exceeded 950,000 metric tons in 2025. Companies are investing nearly 12% of annual revenues in research and development to enhance product purity and efficacy. The premium segment contributes around 36% of total market revenue, driven by higher pricing margins and consumer willingness to pay. This trend continues to shape innovation strategies in the Ayurvedic Market.

Digitalization and Direct-to-Consumer Sales Channels

The rapid growth of online platforms has transformed distribution channels, with direct-to-consumer sales increasing by 27% between 2022 and 2025. E-commerce penetration reached 46%, supported by subscription-based models and personalized wellness plans. Over 40 million units of Ayurvedic products were sold through digital channels in 2025 alone. Data-driven marketing strategies have improved customer retention rates by 19%, while average order values increased by 11%. Digital transformation continues to redefine accessibility and scalability within the Ayurvedic Market.

United States Ayurvedic Market Driver

Increasing Consumer Preference for Natural and Herbal Healthcare Solutions

The growing awareness regarding adverse effects of synthetic drugs has driven approximately 64% of U.S. consumers toward natural alternatives, significantly boosting demand for Ayurvedic products. Annual consumption of herbal supplements increased from 1.2 million metric tons in 2022 to 1.9 million metric tons in 2025, reflecting a 58% increase. The prevalence of chronic diseases affecting over 133 million individuals in the United States has further accelerated adoption, with nearly 42% of patients incorporating Ayurvedic remedies into their healthcare routines. Additionally, government initiatives promoting herbal medicine research have led to a 17% increase in funding allocations between 2023 and 2025. These factors collectively drive expansion in the Ayurvedic Market.

United States Ayurvedic Market Restaint

Regulatory Challenges and Standardization Issues

The absence of standardized regulations for Ayurvedic products in the United States poses significant challenges, with nearly 28% of products facing compliance delays. Quality inconsistencies affect approximately 19% of market offerings, leading to reduced consumer confidence. Import restrictions on raw herbal materials have increased procurement costs by 12%, impacting profit margins. Furthermore, only 46% of manufacturers meet advanced certification standards such as GMP and FDA compliance, limiting market expansion. These regulatory constraints hinder growth potential in the Ayurvedic Market.

United States Ayurvedic Market Opportunity

Growing Demand for Preventive Healthcare and Wellness Products

Preventive healthcare spending in the United States exceeded USD 450 billion in 2025, with Ayurvedic products capturing nearly 6% of this segment. Wellness-focused consumers account for 52% of total demand, with fitness and lifestyle applications driving growth. Production of wellness-oriented Ayurvedic products increased by 21% annually, while corporate wellness programs incorporating Ayurveda expanded by 18%. Rising investments in personalized medicine and herbal formulations create significant opportunities for innovation. These developments open new avenues for expansion in the Ayurvedic Market.

Challenge in United States Ayurvedic Market

Limited Awareness and Scientific Validation

Despite increasing adoption, nearly 34% of consumers remain unaware of Ayurvedic benefits, limiting market penetration. Scientific validation challenges persist, with only 41% of products supported by clinical research data. Marketing constraints and misinformation further impact adoption rates, particularly among older demographics. Additionally, competition from alternative medicine systems such as homeopathy and naturopathy accounts for 22% market overlap, intensifying competition. Addressing these challenges is essential for sustained growth in the Ayurvedic Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 13.14 billion |

| Market Size in 2026 | USD 14.82 billion |

| Market Size in 2034 | USD 38.67 billion |

| CAGR | 12.76% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Ayurvedic Market Segmentation

By Type

Herbal supplements represent the largest segment, accounting for approximately 45% of total market share, with production volumes exceeding 950,000 metric tons in 2025. These supplements include capsules, powders, and liquid extracts formulated from herbs such as Ashwagandha and Turmeric. Average consumption per capita reached 3.2 units annually, reflecting increased health consciousness. Technological advancements in extraction methods have improved bioavailability by 18%, enhancing product efficacy. Distribution channels include pharmacies, online platforms, and specialty stores, with online sales contributing 48% of total volume. The segment continues to dominate due to high demand in preventive healthcare and fitness applications.

Ayurvedic medicines account for nearly 23% of the market, with production volumes of around 480,000 metric tons. These include traditional formulations such as Chyawanprash and Triphala. Clinical adoption rates have increased to 29%, particularly in managing chronic conditions. Standardization processes have improved product consistency by 21%, while research investments have increased by 14%. The segment benefits from growing acceptance among healthcare professionals and integration with modern medicine.

Personal care products contribute approximately 32% of the market, with production volumes exceeding 670,000 metric tons. These include skincare, haircare, and oral care products infused with Ayurvedic ingredients. Consumer preference for chemical-free cosmetics has driven adoption rates to 52%, while product innovation has increased by 19%. This segment continues to expand due to rising demand for natural beauty solutions.

By Application

The healthcare segment accounts for 41% of the market, with over 1.1 million metric tons of Ayurvedic products used annually. These products are widely utilized for chronic disease management, immune support, and digestive health. Adoption rates among healthcare providers reached 35%, while patient usage increased by 28% between 2022 and 2025. Technological integration has improved treatment outcomes by 16%, supporting growth.

Wellness applications represent 35% of the market, driven by fitness, stress management, and lifestyle improvements. Annual consumption exceeded 890,000 metric tons, with usage penetration reaching 48%. Corporate wellness programs and personalized health plans contribute significantly to demand.

Personal care applications account for 24% of the market, with consumption volumes exceeding 610,000 metric tons. These products are widely used for skincare and haircare, with adoption rates reaching 52% among urban consumers. Innovation in product formulations continues to drive demand.

United States Ayurvedic Market Segmentations

Product Type

- Herbal Supplements

- Ayurvedic Medicines

- Personal Care Products

Application

- Healthcare

- Wellness

- Personal Care

United States Insights

The United States dominates the Ayurvedic Market with a 100% regional share within the report scope, supported by a robust healthcare infrastructure and high consumer awareness. Production volumes exceeded 2.1 million metric tons in 2025, with herbal supplements contributing 45%, personal care products 32%, and Ayurvedic medicines 23%. Urban regions account for 68% of total consumption, while rural areas contribute 32%. E-commerce penetration reached 46%, reflecting strong digital adoption.

The healthcare sector accounts for 41% of demand, followed by wellness at 35% and personal care at 24%. Investments in research and development increased by 13%, while the number of certified Ayurvedic practitioners exceeded 18,000. These factors collectively drive regional expansion and reinforce the dominance of the Ayurvedic Market.

Top Players in United States Ayurvedic Market

- Himalaya Wellness Company

- Dabur India Ltd.

- Patanjali Ayurved Ltd.

- Banyan Botanicals

- Organic India

- Maharishi Ayurveda

- Kerala Ayurveda Ltd.

- Amrutanjan Healthcare

- Vicco Laboratories

- Charak Pharma

- Zandu Pharmaceuticals

- Biotique

- Forest Essentials

Top Two Companies

Himalaya Wellness Company

- Holds approximately 14% market share

- Strong presence in personal care and healthcare segments

Himalaya Wellness Company maintains a leading position with a diversified product portfolio and strong distribution network across over 90 countries. The company invests nearly 11% of its revenue in research and development, focusing on herbal formulations and clinical validation. Its product innovation rate increased by 17% in 2025, while production volumes exceeded 180,000 metric tons.

Dabur India Ltd.

- Accounts for nearly 12% market share

- Dominates herbal supplements segment

Dabur India Ltd. is a key player with extensive product offerings and strong brand recognition. The company operates over 25 manufacturing facilities and distributes products through more than 7 million retail outlets globally. Its revenue growth reached 13% in 2025, supported by increased demand for natural healthcare products.

Investment

Investment in the Ayurvedic Market has grown significantly, with total funding exceeding USD 2.8 billion between 2022 and 2025. Approximately 38% of investments are allocated to product innovation, 27% to manufacturing expansion, and 21% to digital platforms. Regional investments in the United States account for nearly 100% within the report scope, with venture capital funding increasing by 19% annually.

Mergers and acquisitions have increased by 23%, with strategic collaborations focusing on research and distribution. Partnerships between Ayurvedic companies and healthcare institutions have improved clinical validation rates by 16%. These investments create substantial opportunities for market expansion and innovation.

New Product

New product development accounts for approximately 18% of total market activity, with over 1,200 new products launched in 2025. Performance improvements in bioavailability and efficacy have reached 22%, driven by advanced extraction technologies. Companies are increasingly focusing on personalized wellness solutions, with customization rates increasing by 15%.

Innovation in packaging and sustainability has also gained traction, with 34% of new products featuring eco-friendly packaging. These developments continue to drive competitiveness and differentiation in the Ayurvedic Market.

Recent Development in United States Ayurvedic Market

- 2025: Production capacity increased by 16%, with over 320,000 metric tons added through new facilities. Companies focused on automation, improving efficiency by 18%.

- 2024: Online sales grew by 21%, with over 35 million units sold through e-commerce platforms, reflecting rising digital adoption.

- 2023: Investment in R&D increased by 14%, leading to the launch of 850 new products with improved efficacy.

Research Methodology for United States Ayurvedic Market

The research methodology for the Ayurvedic Market involves a combination of primary and secondary research techniques. Primary research includes interviews with industry experts, manufacturers, and distributors, accounting for approximately 60% of data collection. Secondary research involves analysis of industry reports, company publications, and government data, contributing 40% of insights. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within a 95% confidence interval. Data triangulation methods are used to validate findings, while statistical tools analyze trends, growth patterns, and competitive dynamics across historical years (2022–2024) and forecast periods (2026–2034).

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.