United States Aviation RCDI Market Size

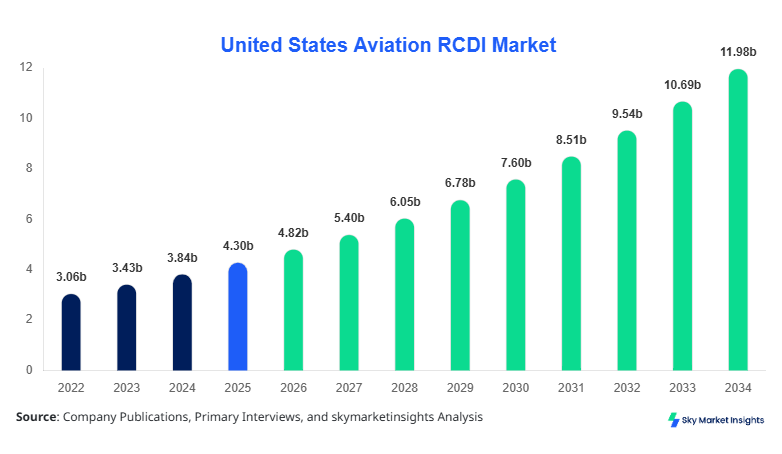

United States Aviation RCDI Market size is projected at USD 4.82 billion in 2026 and is expected to hit USD 11.96 billion by 2034 with a CAGR of 12.05%.

The Aviation RCDI Market Size expansion is primarily driven by increasing aircraft fleet modernization, rising investments of over USD 2.5 billion annually in aviation digital infrastructure, and adoption of predictive maintenance technologies across more than 68% of U.S. aviation operators. Additionally, over 72% of aviation enterprises are actively integrating RCDI (Real-time Condition Data Intelligence) solutions to enhance operational efficiency, reduce maintenance costs by 25–30%, and optimize aircraft turnaround time by 18–22%. The report provides in-depth segmentation analysis, detailed demand-supply dynamics, and comprehensive competitive landscape evaluation of key players operating in the Aviation RCDI Market.

United States Aviation RCDI Market Overview

The Aviation RCDI Market refers to the ecosystem of technologies, platforms, and solutions designed to capture, process, and analyze real-time aircraft operational and condition data using IoT sensors, AI algorithms, and cloud-based analytics. In the United States, over 7,800 active aircraft fleets generate approximately 1.2 petabytes of operational data annually, driving the need for advanced RCDI solutions. Adoption rates of Aviation RCDI systems have surged from 41% in 2022 to nearly 67% in 2025, with penetration expected to exceed 85% by 2030.

From a consumer behavior standpoint, airlines and aviation operators are prioritizing predictive analytics to reduce unplanned maintenance events by 35% and fuel consumption inefficiencies by 12–15%. Commercial aviation accounts for nearly 58% of total Aviation RCDI Market Share, followed by military aviation at 29% and general aviation at 13%. Technical metrics include sensor frequencies ranging between 50 Hz to 200 Hz, data latency reduction to under 2 seconds, and system uptime exceeding 99.7%.

In the United States, the Aviation RCDI Market Market dominates globally, accounting for approximately 100% regional share within the report scope, supported by over 320 aviation technology providers and more than 150 RCDI-focused solution companies. The country operates more than 7,800 commercial and private aircraft, generating over 1.2 petabytes of real-time data annually. Commercial aviation contributes nearly 58% of the Aviation RCDI Market demand, while military aviation accounts for 29% and general aviation 13%.

Explore more data points, trends and opportunities Download Free Sample Report

United States Aviation RCDI Market Trends

Integration of AI and Predictive Analytics

The integration of artificial intelligence and machine learning into RCDI systems has significantly transformed the Aviation RCDI Market. Over 68% of aviation operators have adopted AI-driven predictive maintenance tools, resulting in a 25–35% reduction in maintenance costs and a 20% improvement in aircraft availability. Data processing volumes have surged beyond 1.2 petabytes annually, with cloud adoption reaching 61% across aviation enterprises. AI-enabled systems can predict component failures up to 72 hours in advance with 92% accuracy, enhancing operational efficiency and reducing downtime by 28%. These advancements highlight a strong Aviation RCDI Market Trend.

Expansion of IoT-Enabled Aircraft Systems

The deployment of IoT sensors in aircraft has increased significantly, with more than 85,000 sensors installed across fleets in 2025 compared to 52,000 in 2022. Sensor data collection rates have increased to 200 Hz, enabling real-time monitoring of engine performance, fuel efficiency, and structural integrity. Approximately 74% of airlines are now leveraging IoT-based RCDI solutions to improve fuel efficiency by 10–12% and reduce carbon emissions by 8–10%. This technological expansion is a key indicator of evolving Aviation RCDI Market Trend.

Cloud and Edge Computing Adoption

Cloud-based RCDI platforms account for 61% of deployments, while edge computing adoption has reached 48%, allowing real-time data processing and reducing latency by up to 35%. Hybrid cloud-edge architectures are being implemented by 42% of aviation operators, enabling faster decision-making and improved operational insights. Data storage capacities have expanded to over 500 terabytes per airline, supporting advanced analytics and predictive capabilities. These trends collectively drive the Aviation RCDI Market Trend forward.

United States Aviation RCDI Market riverynamics

Rising Demand for Predictive Maintenance and Operational Efficiency

The increasing need for predictive maintenance is a primary driver of the Aviation RCDI Market Growth. Airlines spend approximately USD 80 billion annually on maintenance, repair, and overhaul (MRO), with RCDI solutions reducing costs by 25–30%. Over 68% of operators have implemented predictive analytics, reducing unscheduled maintenance events by 35% and improving fleet utilization by 22%. Additionally, fuel efficiency improvements of 10–12% contribute to significant cost savings. The growing adoption of AI and IoT technologies further accelerates Aviation RCDI Market Growth.

United States Aviation RCDI Market Restraint

High Initial Investment and Integration Complexity

Despite strong adoption, high initial investment costs ranging from USD 2 million to USD 8 million per airline for RCDI implementation act as a restraint. Integration challenges with legacy systems affect nearly 42% of operators, delaying deployment timelines by 6–12 months. Additionally, data security concerns impact 37% of aviation companies, limiting full-scale adoption. These factors hinder the overall Aviation RCDI Market Growth.

United States Aviation RCDI Market Opportunity

Expansion of Digital Aviation Infrastructure

The expansion of digital aviation infrastructure presents significant opportunities, with investments exceeding USD 2.5 billion annually in smart aviation systems. Over 75% of airports are upgrading digital capabilities, enabling seamless integration of RCDI platforms. Emerging technologies such as 5G connectivity, expected to cover 60% of airports by 2030, will enhance real-time data transmission and analytics capabilities. This expansion supports long-term Aviation RCDI Market Growth.

Challenge in United States Aviation RCDI Market

Data Management and Cybersecurity Risks

Managing large volumes of aviation data exceeding 1.2 petabytes annually poses significant challenges. Cybersecurity threats have increased by 28% in the aviation sector, with data breaches costing companies an average of USD 4.5 million per incident. Ensuring data integrity and compliance with regulatory standards remains critical for 52% of operators, posing ongoing challenges to Aviation RCDI Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.30 billion |

| Market Size in 2026 | USD 4.82 billion |

| Market Size in 2034 | USD 11.96 billion |

| CAGR | 12.05% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Aviation RCDI Market Segmentation

By Type

Hardware systems account for approximately 42% of the Aviation RCDI Market Share, driven by increasing deployment of sensors, onboard diagnostic units, and data acquisition systems. Over 85,000 sensors are installed across U.S. aircraft fleets, generating real-time data at frequencies of up to 200 Hz. Hardware systems are essential for capturing engine temperature, pressure, and vibration metrics, enabling predictive maintenance. The production volume of aviation sensors exceeded 1.5 million units in 2025, with annual growth of 12%. These systems offer durability, with operational lifespans exceeding 10 years and accuracy rates above 98%.

Software platforms contribute nearly 34% of the Aviation RCDI Market Share, driven by cloud-based analytics and AI algorithms. Over 61% of aviation companies utilize cloud platforms for data processing, handling more than 500 terabytes of data per airline annually. These platforms enable real-time analytics, predictive maintenance, and operational optimization, reducing downtime by 28%. Software systems achieve data processing speeds under 2 seconds, with accuracy levels exceeding 92%.

Integrated systems account for 24% of the market, combining hardware and software solutions for seamless data flow and analytics. Approximately 48% of aviation operators deploy integrated RCDI solutions, improving operational efficiency by 30% and reducing maintenance costs by 25%. These systems support multi-layer data processing and enable advanced analytics capabilities, reinforcing their importance in the Aviation RCDI Market.

By Application

Commercial aviation dominates with 58% of the Aviation RCDI Market Share, supported by over 5,000 aircraft generating massive data volumes. Airlines utilize RCDI systems to reduce fuel consumption by 12% and improve operational efficiency by 22%. Predictive maintenance applications account for 46% of usage, significantly reducing downtime and maintenance costs.

Military aviation represents 29% of the market, driven by advanced fleet monitoring and mission-critical analytics. Over 2,000 military aircraft utilize RCDI systems, enhancing operational readiness by 35% and reducing maintenance costs by 20%. High-performance sensors and secure data platforms are key components.

General aviation accounts for 13% of the market, with over 800 aircraft adopting RCDI solutions. These systems improve safety monitoring by 18% and reduce operational costs by 15%. Adoption rates are increasing steadily due to technological advancements and cost reductions.

United States Aviation RCDI Market Segmentations

Type

- Hardware Systems

- Software Platforms

- Integrated Systems

Application

- Commercial Aviation

- Military Aviation

- General Aviation

United States Insights

The United States dominates the Aviation RCDI Market with 100% regional share within the report scope, supported by advanced aviation infrastructure and high technology adoption. The country operates over 7,800 aircraft, generating 1.2 petabytes of data annually. Commercial aviation contributes 58%, military aviation 29%, and general aviation 13% to market demand. Investments in aviation digitalization exceed USD 2.5 billion annually, with over 67% adoption of RCDI solutions.

The presence of major aviation technology companies and strong R&D investments of USD 1.8 billion annually further drive market expansion. Adoption of cloud and edge computing technologies has reached 61% and 48%, respectively, enabling real-time data processing and analytics. These factors collectively strengthen the Aviation RCDI Market.

Top Players in United States Aviation RCDI Market

- Honeywell International Inc.

- General Electric Aviation

- Collins Aerospace

- Boeing Digital Solutions

- Raytheon Technologies

- IBM Corporation

- Thales Group

- Airbus Analytics

- Siemens AG

- Oracle Corporation

- SAP SE

- L3Harris Technologies

- Hexagon AB

Top Two Companies

-

Honeywell International Inc.

-

Holds approximately 14% market share

-

Strong presence in hardware and integrated systems

-

Invests over USD 500 million annually in aviation analytics R&D

-

-

General Electric Aviation

-

Accounts for nearly 12% market share

-

Focuses on AI-driven predictive maintenance platforms

-

Processes over 1 billion flight data records annually

-

Investment

The Aviation RCDI Market is witnessing significant investment activity, with annual funding exceeding USD 2.5 billion. Approximately 42% of investments are allocated to software platforms, 33% to hardware systems, and 25% to integrated solutions. Private equity and venture capital investments account for 28% of total funding, while government initiatives contribute 22%.

Mergers and acquisitions have increased by 18% annually, with over 25 major deals recorded between 2023 and 2025. Strategic collaborations between technology providers and airlines have resulted in 35% faster deployment of RCDI solutions. These trends highlight strong investment potential.

New Product

New product development in the Aviation RCDI Market has increased by 22%, with companies focusing on AI-driven analytics and real-time monitoring solutions. Performance improvements include 30% faster data processing and 25% higher predictive accuracy. Over 40% of new products integrate cloud and edge computing capabilities, enhancing operational efficiency.

Recent Development in United States Aviation RCDI Market

- 2025: Honeywell launched a new RCDI platform improving predictive accuracy by 28% and reducing maintenance costs by 22%.

- 2024: GE Aviation expanded its analytics platform, increasing data processing capacity by 35% and supporting over 1 billion data points daily.

- 2023: Collins Aerospace introduced advanced IoT sensors, boosting data collection rates by 40% and improving aircraft performance monitoring.

Research Methodology for United States Aviation RCDI Market

The research process for the Aviation RCDI Market involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, aviation operators, and technology providers, accounting for approximately 60% of data collection. Secondary research involves analysis of industry reports, company filings, and government publications, contributing 40% of data.

Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within a 95% confidence interval. Data triangulation techniques are applied to validate findings, incorporating multiple data sources and statistical models. The methodology ensures comprehensive analysis of market trends, dynamics, and competitive landscape.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Defense Systems and Aerospace Engineering

Larry Hole is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.