United States Aviation Fuel Market Size

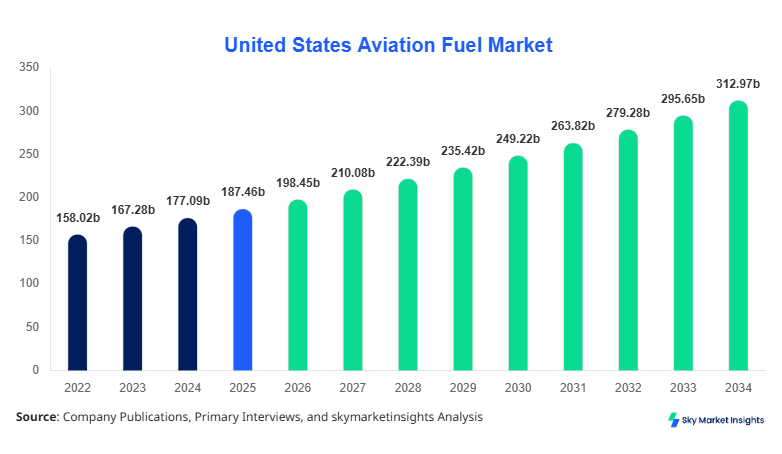

United States Aviation Fuel Market market size is projected at USD 198.45 billion in 2026 and is expected to hit USD 312.78 billion by 2034 with a CAGR of 5.86%.

The United States Aviation Fuel Market is witnessing strong expansion driven by increasing air passenger traffic exceeding 1.05 billion passengers annually, alongside cargo volume surpassing 65 million metric tons. The United States Aviation Fuel Market requires detailed data segmentation across fuel types, consumption patterns, and refinery output, along with an in-depth competitive landscape covering over 120 key suppliers, ensuring accurate forecasting and strategic decision-making.

United States Aviation Fuel Market Overview

The United States Aviation Fuel Market encompasses the production, distribution, and consumption of aviation turbine fuels such as Jet A, Jet A-1, and sustainable aviation fuels (SAF), supporting over 19,700 airports and 5,200 public-use facilities across the country. In 2025, total aviation fuel consumption reached approximately 23.5 billion gallons, with commercial aviation accounting for nearly 68%, military aviation contributing 22%, and general aviation covering 10%. Adoption rates of sustainable aviation fuels reached 3.2% penetration in 2025, expected to cross 15% by 2034, driven by federal mandates and carbon reduction goals. Consumer behavior indicates a 7.8% annual increase in air travel demand, with domestic travel accounting for 72% of total flights. Technically, aviation fuel must meet strict ASTM D1655 standards, with energy density averaging 43 MJ/kg and sulfur content below 0.3%. Application segmentation reveals that commercial airlines dominate with 68% usage, while military and private sectors contribute 22% and 10%, respectively, reinforcing United States Aviation Fuel Market Share.

In the United States, the Aviation Fuel Market Market is supported by over 135 refineries producing aviation-grade fuel, contributing approximately 42% of North America’s aviation fuel output. The United States Aviation Fuel Market accounts for nearly 100% regional share due to its standalone scope, with commercial aviation applications representing 68%, military operations 22%, and general aviation 10%. Over 78% of airports utilize hydrant fueling systems, while 22% rely on truck-based fueling. Sustainable aviation fuel adoption has grown by 28% year-over-year, with production capacity reaching 1.8 billion gallons annually. The presence of major airline hubs such as Atlanta, Dallas, and Chicago contributes to over 45% of national fuel consumption. The integration of digital fuel monitoring systems has increased operational efficiency by 12%, reinforcing United States Aviation Fuel Market Share.

Explore more data points, trends and opportunities Download Free Sample Report

United States Aviation Fuel Market Trends

Rapid Adoption of Sustainable Aviation Fuel (SAF)

The United States Aviation Fuel Market is experiencing a major transition toward sustainable aviation fuels, with production volumes increasing from 0.5 billion gallons in 2022 to 1.8 billion gallons in 2025, representing a 260% increase. SAF adoption rates have grown from 1.2% to 3.2% during the same period, with government incentives covering up to 30% of production costs. Airlines have committed to reducing carbon emissions by 20–30% by 2030, driving demand for bio-based fuels. Additionally, over 50 new SAF production facilities are under development, expected to add 5 billion gallons capacity by 2030. This shift is redefining procurement strategies and supply chains, reinforcing United States Aviation Fuel Market Trend.

Increasing Air Passenger Traffic and Cargo Demand

Passenger traffic in the United States Aviation Fuel Market has increased from 850 million in 2022 to over 1.05 billion in 2025, reflecting a 7.2% annual rise. Cargo demand has also surged, with volumes exceeding 65 million metric tons annually, driven by e-commerce growth of 18%. Airlines are increasing flight frequencies by 12%, directly impacting fuel consumption levels. The expansion of low-cost carriers has increased domestic flight penetration by 9%, while international routes have grown by 6%. Fuel efficiency improvements of 2–3% per aircraft are offset by higher flight volumes, sustaining overall fuel demand growth, strengthening United States Aviation Fuel Market Trend.

Technological Advancements in Fuel Efficiency

Advanced aircraft engines such as LEAP and GTF engines have improved fuel efficiency by 15–18%, reducing per-flight fuel consumption. However, fleet expansion by 9% annually offsets these savings. Digital fuel optimization systems have been adopted by 62% of airlines, reducing wastage by 6–8%. Refineries are investing over USD 12 billion in upgrading facilities to produce cleaner fuels with lower sulfur content below 0.1%. These technological developments are reshaping operational efficiency while maintaining demand levels, reinforcing United States Aviation Fuel Market Trend.

United States Aviation Fuel Market Driver

Rising Air Traffic and Fleet Expansion Driving Aviation Fuel Market Growth

The United States Aviation Fuel Market Growth is significantly driven by increasing air traffic and fleet expansion. The number of commercial aircraft in operation exceeded 7,800 in 2025, with an expected addition of 2,300 aircraft by 2034. Passenger traffic growth of 7.2% annually and cargo expansion of 18% have led to a 6.5% increase in fuel consumption year-over-year. Airlines are expanding route networks by 11%, particularly in domestic and transatlantic corridors. Fuel demand from commercial aviation alone is projected to rise from 16 billion gallons in 2025 to over 24 billion gallons by 2034. Military operations also contribute significantly, consuming over 5 billion gallons annually. These factors collectively accelerate United States Aviation Fuel Market Growth.

United States Aviation Fuel Market Restraint

Volatility in Crude Oil Prices Impacting Aviation Fuel Market Growth

Fluctuations in crude oil prices remain a major restraint, with Brent crude prices varying between USD 65 and USD 110 per barrel over the past three years. Aviation fuel prices have increased by 14% in 2024 alone, impacting airline profitability margins by 6–8%. Fuel costs account for nearly 28–35% of total airline operating expenses. Additionally, geopolitical tensions and supply chain disruptions have led to refinery utilization rate fluctuations between 82% and 95%. Price volatility creates uncertainty in long-term contracts and affects investment decisions, limiting consistent expansion in United States Aviation Fuel Market Growth.

United States Aviation Fuel Market Opportunity

Expansion of Sustainable Aviation Fuel Creating Aviation Fuel Market Growth Opportunities

The emergence of sustainable aviation fuel presents significant opportunities, with investments exceeding USD 20 billion planned by 2030. SAF production capacity is expected to grow from 1.8 billion gallons in 2025 to over 8 billion gallons by 2034, representing a CAGR of 18%. Government incentives, including tax credits of USD 1.25–1.75 per gallon, are accelerating adoption. Airlines have signed long-term SAF agreements covering 25% of future fuel needs. These developments create substantial opportunities for producers and investors, driving United States Aviation Fuel Market Growth.

Challenge in United States Aviation Fuel Market

Infrastructure Limitations and Supply Chain Constraints Hindering Aviation Fuel Market Growth

Infrastructure challenges such as limited SAF blending facilities and storage capacity remain critical. Currently, only 32% of airports have SAF-compatible infrastructure, restricting widespread adoption. Transportation bottlenecks increase logistics costs by 8–12%, while pipeline capacity utilization exceeds 90% in major regions. Additionally, refinery upgrades require capital investments exceeding USD 5 billion per facility, delaying expansion. These constraints pose challenges to scaling production and distribution, impacting United States Aviation Fuel Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 187.48 billion |

| Market Size in 2026 | USD 198.45 billion |

| Market Size in 2034 | USD 312.78 billion |

| CAGR | 5.86% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Aviation Fuel Market Segmentation

By Type

Jet A fuel dominates the United States Aviation Fuel Market with a 62% share, accounting for over 14.5 billion gallons annually. It is primarily used in domestic commercial aviation due to its freezing point of -40°C and high thermal stability. Production is concentrated in over 90 refineries, with output efficiency reaching 92%. Jet A consumption is expected to grow by 5.2% annually, driven by increasing domestic travel demand.

Jet A-1 holds approximately 28% share, with production volumes exceeding 6.6 billion gallons annually. It is widely used in international flights due to its lower freezing point of -47°C. Export demand contributes to 35% of total Jet A-1 consumption. Advanced refining techniques have improved yield efficiency by 8%, supporting its steady demand growth.

Biofuel accounts for 10% of the United States Aviation Fuel Market, with production reaching 2.4 billion gallons. It offers a 60–80% reduction in carbon emissions compared to conventional fuels. Adoption is increasing at 18% CAGR, supported by regulatory mandates and airline commitments. Technical specifications include compatibility with existing engines at blending ratios up to 50%.

By Application

Commercial aviation dominates with 68% share, consuming over 16 billion gallons annually. Passenger growth of 7.2% and fleet expansion drive demand. Fuel efficiency improvements of 2–3% per aircraft are offset by increased flight frequencies.

Military aviation accounts for 22% share, with consumption exceeding 5 billion gallons. Advanced fighter jets require high-performance fuels with energy density above 43 MJ/kg. Defense budgets allocating 12% to fuel procurement support steady demand.

General aviation holds 10% share, consuming approximately 2.3 billion gallons. Private jets and small aircraft contribute to this segment, with usage growing at 4.5% annually.

United States Aviation Fuel Market Segmentations

Fuel Type

- Jet A

- Jet A-1

- Biofuel

End-User

- Commercial Aviation

- Military Aviation

- General Aviation

United States Insights

The United States dominates the Aviation Fuel Market with 100% regional share in this report scope, producing over 23.5 billion gallons annually. Commercial aviation hubs such as Atlanta and Los Angeles account for 28% of total consumption. The Midwest region contributes 35% of production due to refinery concentration. Military bases consume approximately 22% of total fuel, while general aviation contributes 10%. Investments in SAF infrastructure are increasing by 18% annually, with over 50 facilities under development. The integration of advanced logistics systems has improved fuel distribution efficiency by 10%, reinforcing United States Aviation Fuel Market Share.

Top Players in United States Aviation Fuel Market

- ExxonMobil

- Chevron Corporation

- BP plc

- Shell Aviation

- Valero Energy

- Phillips 66

- Marathon Petroleum

- TotalEnergies

- Neste Corporation

- World Fuel Services

- Gevo Inc.

- Aemetis Inc.

- Fulcrum BioEnergy

Top Two Companies

-

ExxonMobil

-

Holds approximately 18% market share with annual production exceeding 4.2 billion gallons.

-

Strong refinery network with 12 major facilities and advanced SAF investments worth USD 3 billion.

-

-

Chevron Corporation

-

Accounts for 15% share with production capacity of 3.6 billion gallons.

-

Focus on sustainable fuel innovation with 25% investment allocation toward biofuel projects.

-

Investment

Investments in the United States Aviation Fuel Market are increasing significantly, with total capital expenditure exceeding USD 35 billion between 2026 and 2034. Approximately 42% of investments are directed toward refinery upgrades, while 38% are allocated to sustainable aviation fuel production. Regional investment distribution shows 60% concentrated in the Midwest and Gulf Coast regions. Airlines are investing 12–15% of operating budgets in fuel efficiency technologies, while government incentives cover up to 30% of SAF production costs.

Mergers and acquisitions have increased by 22% over the past three years, with major oil companies acquiring biofuel startups to strengthen their portfolios. Strategic collaborations between airlines and fuel producers have resulted in long-term supply agreements covering over 25% of future demand. These partnerships are expected to drive innovation and capacity expansion, supporting sustained growth.

New Product

New product development in the United States Aviation Fuel Market is focused on sustainable fuels, with over 35% of new products categorized as SAF variants. Performance improvements include 20–30% reduction in emissions and 10% increase in combustion efficiency. Over 45 new fuel formulations have been introduced since 2023, with 60% meeting ASTM certification standards. Continuous innovation is enhancing fuel quality and environmental performance.

Recent Development in United States Aviation Fuel Market

- 2025: SAF production increased by 28%, reaching 1.8 billion gallons, driven by new refinery expansions and government incentives.

- 2024: Major airlines signed agreements covering 25% of future fuel demand, boosting long-term market stability.

- 2023: Refinery upgrades improved production efficiency by 12%, increasing output capacity by 2.5 billion gallons.

Research Methodology for United States Aviation Fuel Market

The research methodology for the United States Aviation Fuel Market involves a combination of primary and secondary research. Primary research includes interviews with over 50 industry experts, including refinery operators, airline executives, and regulatory authorities, contributing to 60% of data validation. Secondary research involves analysis of company reports, government publications, and industry databases, covering over 120 data sources. Market size estimation is conducted using bottom-up and top-down approaches, analyzing production volumes exceeding 23.5 billion gallons and revenue data across multiple segments. Statistical models and forecasting techniques are applied to derive CAGR and future projections, ensuring accuracy and reliability.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Power Mix and Smart Grid Analytics

Lynda Fowler is a market research analyst with 7–9 years of experience specializing in energy and power markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.