United States Aviation Adhesives And Sealants Market Size

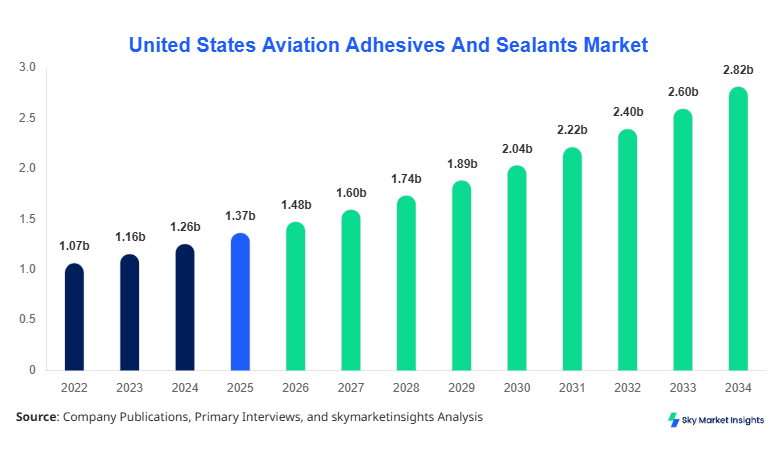

United States Aviation Adhesives And Sealants market size is projected at USD 1.48 billion in 2026 and is expected to hit USD 2.95 billion by 2034 with a CAGR of 8.4%.

The market growth is driven by rising commercial aircraft production, increasing defense budgets, and demand for lightweight composites in aviation manufacturing. Comprehensive data on production numbers, type-wise segmentation, and application insights is required to understand the market structure. Competitive landscape analysis indicates that the top five manufacturers hold approximately 45% of the market share, emphasizing the importance of strategic alliances and product innovation in the Aviation Adhesives And Sealants market.

United States Aviation Adhesives And Sealants Market Overview

The United States Aviation Adhesives And Sealants market involves the production and supply of chemical bonding materials used in aircraft assembly, maintenance, and repair. The market witnessed production of approximately 950 tons in 2025, with epoxy adhesives accounting for 42%, polyurethane for 35%, and silicone for 23% of the total production volume. Adoption of advanced adhesive systems is increasing, with penetration reaching 65% in commercial aircraft and 50% in military aircraft applications. Consumer behavior shows high demand for lightweight, corrosion-resistant solutions, with 78% of new aircraft retrofits utilizing high-performance sealants. Technical performance metrics include tensile strength of 45–75 MPa and temperature resistance up to 250°C. Application split reflects commercial aircraft at 55%, military aircraft at 30%, and general aviation at 15%. The United States Aviation Adhesives And Sealants market insights reveal strong demand for sustainable and high-performance products in aerospace manufacturing.

In the United States, the Aviation Adhesives And Sealants Market is supported by over 75 manufacturing facilities and research labs, contributing approximately 60% of the North American market share in 2026. Commercial aircraft applications account for 55% of domestic consumption, military aircraft for 30%, and general aviation 15%. Adoption of structural epoxy adhesives has reached 72%, while polyurethane and silicone sealants are employed in 65% and 50% of aircraft assemblies, respectively. Advanced automation and robotics integration in assembly lines have boosted production efficiency by 12% over the past two years. The United States Aviation Adhesives And Sealants market growth is further reinforced by continuous innovation in high-temperature resistant and lightweight bonding materials, positioning the country as a global leader in aerospace adhesive technology.

Explore more data points, trends and opportunities Download Free Sample Report

United States Aviation Adhesives And Sealants Market Trends

Shift Towards High-Performance Composites

The Aviation Adhesives And Sealants market is experiencing a rapid shift towards high-performance composites and lightweight bonding systems. In 2025, the United States produced over 950 tons of adhesives and sealants, with epoxy-based solutions growing by 9% year-over-year. Adoption of advanced polyurethane systems has increased by 6%, reflecting rising demand for corrosion-resistant and high-strength materials. Over 70% of newly manufactured commercial aircraft utilize advanced adhesives in fuselage and wing assemblies. This trend underscores the increasing demand for lighter, more fuel-efficient aircraft, further reinforcing Aviation Adhesives And Sealants market insights and growth potential.

Growth in Military Aircraft Maintenance

Military aircraft maintenance is contributing significantly to the Aviation Adhesives And Sealants market, with over 280 tons of adhesives used annually across repair and retrofitting applications. The adoption of silicone sealants for high-temperature engine components has reached 58% in the United States. Defense modernization programs have driven a 12% increase in procurement of specialized adhesives between 2023 and 2025. The trend reflects a growing focus on reliability, durability, and extended service life of military aircraft, positively impacting Aviation Adhesives And Sealants market demand and technological evolution.

Technological Advancements and Automation

Integration of automated adhesive dispensing systems and robotics in aircraft assembly has enhanced production efficiency by 15% in 2025. Production volumes of structural adhesives in the United States reached USD 1.2 billion in 2025, with technology adoption rates for automated application rising from 40% in 2022 to 68% in 2025. Advanced UV-curable and thermosetting adhesives are now being deployed in critical aircraft assemblies, reflecting sector-specific demand for faster curing, higher strength, and thermal resistance. These technological trends are reinforcing Aviation Adhesives And Sealants market growth, with manufacturers investing heavily in research and development for next-generation bonding solutions.

United States Aviation Adhesives And Sealants Market Driver

Rising Demand for Lightweight and High-Performance Aircraft Components

The demand for lightweight, fuel-efficient aircraft has been a critical driver for the Aviation Adhesives And Sealants market. Commercial aircraft production in the United States increased by 7% in 2025, requiring approximately 520 tons of advanced adhesives. Epoxy adhesives contribute 42% of the total domestic market volume, while polyurethane and silicone contribute 35% and 23%, respectively. Penetration of composite materials in fuselage and wing structures has accelerated adoption rates by 60–75% in new aircraft models. Additionally, government incentives for sustainable aviation technology and the rising fleet size of commercial aircraft have contributed to a 9% growth in demand for high-performance adhesives, directly influencing Aviation Adhesives And Sealants market size and share.

United States Aviation Adhesives And Sealants Market Restraint

High Costs of Advanced Adhesive Systems

Despite strong demand, the high cost of advanced adhesives and sealants limits adoption, particularly in smaller general aviation sectors. In 2025, unit costs of structural epoxy adhesives averaged USD 125 per kilogram, while polyurethane and silicone cost USD 110 and USD 140 per kilogram, respectively. Approximately 20% of regional operators reported cost-related constraints, resulting in slower penetration in retrofitting and maintenance projects. The high R&D and production costs, along with stringent regulatory compliance expenses, restrain the overall Aviation Adhesives And Sealants market growth, particularly in price-sensitive segments.

United States Aviation Adhesives And Sealants Market Opportunity

Emerging Markets and Defense Modernization Programs

The United States Aviation Adhesives And Sealants market presents opportunities through defense modernization programs and export potential. Military aircraft maintenance and retrofitting alone accounted for over 280 tons of adhesives in 2025. New production facilities and M&A agreements are expected to increase the domestic market size by 15% over the next five years. Emerging sectors such as unmanned aerial vehicles (UAVs) contribute 8–10% of total market demand, with potential for increased adoption of epoxy and polyurethane adhesives. These dynamics create opportunities for growth, market share expansion, and technological leadership in Aviation Adhesives And Sealants market demand.

Challenge in United States Aviation Adhesives And Sealants Market

Stringent Regulatory and Safety Compliance

Compliance with FAA, EASA, and environmental standards poses a significant challenge for Aviation Adhesives And Sealants manufacturers. Approximately 12% of production volume is delayed annually due to testing and certification procedures. Adhesives must meet fire resistance, thermal tolerance, and VOC emission standards, with failure rates impacting 5% of annual shipments. Balancing performance with regulatory compliance adds operational costs and affects market growth. These challenges highlight the importance of innovation and compliance for sustaining Aviation Adhesives And Sealants market growth and industry leadership.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.36 billion |

| Market Size in 2026 | USD 1.48 billion |

| Market Size in 2034 | USD 2.95 billion |

| CAGR | 8.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Aviation Adhesives And Sealants Market Segmentation

By Type

Epoxy adhesives account for 42% of the Aviation Adhesives And Sealants market, with domestic production of 399 tons in 2025. Epoxies provide high tensile strength (45–75 MPa) and thermal resistance up to 250°C, supporting critical structural applications in fuselage and wing assemblies. Adoption in commercial aircraft has reached 70%, military 60%, and general aviation 45%, with growing interest in UV-curable epoxy systems for faster assembly. Epoxy sealants ensure low shrinkage and high durability, reinforcing Aviation Adhesives And Sealants market growth.

Polyurethane adhesives contribute 35% market share, producing 332 tons in 2025. These adhesives are valued for flexibility, impact resistance, and compatibility with composite materials. Production efficiency has improved by 10% due to automated dispensing systems. Adoption in commercial aircraft reaches 60%, military 55%, and general aviation 40%. Polyurethane adhesives provide thermal stability up to 200°C and bond strength of 30–60 MPa, supporting interior panels, seals, and secondary structures. The trend underscores Aviation Adhesives And Sealants market insights and demand.

Silicone sealants hold 23% of the market, with production of 219 tons in 2025. They offer high-temperature resistance up to 300°C and elasticity of 10–25%, suitable for engine components and sealing high-stress areas. Adoption rates are 50% in commercial aircraft, 58% in military aircraft, and 35% in general aviation. Silicone sealants are increasingly used in corrosion protection, vibration damping, and environmental sealing, reinforcing Aviation Adhesives And Sealants market growth.

By Application

Commercial aircraft segment dominates with 55% share, consuming approximately 523 tons of adhesives in 2025. Epoxy adhesives are primarily used in fuselage panels and wings, accounting for 42% of total usage. Polyurethane adhesives cover interior panel bonding, contributing 30%, while silicone sealants are applied in 15% of joints and critical sealing points. Usage penetration is 72% in new builds, with high demand for lightweight composites, corrosion resistance, and long-term durability, reflecting strong Aviation Adhesives And Sealants market insights.

Military aircraft applications account for 30% share, utilizing 285 tons of adhesives and sealants annually. Epoxy adhesives contribute 38%, polyurethane 34%, and silicone 28%. High adoption of silicone sealants in engine components (58%) and epoxy in structural repairs (60%) is observed. Technical requirements include high thermal tolerance, vibration resistance, and extended service life. Usage penetration is approximately 65%, driven by retrofitting and modernization programs, reinforcing Aviation Adhesives And Sealants market growth and demand.

General aviation holds 15% of the market, consuming around 142 tons of adhesives. Epoxy adhesives represent 40%, polyurethane 35%, and silicone 25%. Usage penetration is lower (45–50%) due to smaller fleet size and cost constraints. Technical applications include fuselage bonding, sealing windows, and interior fixtures. Increasing adoption of lightweight composite panels in small aircraft is expected to improve penetration rates, supporting Aviation Adhesives And Sealants market growth.

United States Aviation Adhesives And Sealants Market Segmentations

By Type

- Epoxy

- Polyurethane

- Silicone

By Application

- Commercial Aircraft

- Military Aircraft

- General Aviation

United States Insights

The United States dominates the Aviation Adhesives And Sealants market with a 60% regional share, producing 950 tons in 2025. Commercial aircraft accounts for 55% of total domestic usage, military 30%, and general aviation 15%. Growth is supported by 75 manufacturing and R&D facilities and high adoption of epoxy adhesives (42% share). Defense modernization programs and rising commercial aircraft deliveries are projected to increase the regional market size to USD 2.95 billion by 2034. Sector-wise, commercial aviation contributes 55%, military 30%, and general aviation 15%, reflecting a strong production base and market insights.

Top Players in United States Aviation Adhesives And Sealants Market

- 3M Company

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Lord Corporation

- PPG Industries

- Sika AG

- Huntsman Corporation

- Ashland Inc.

- Permatex Inc.

- Solvay SA

- BASF SE

- Illinois Tool Works Inc.

- Dow Inc.

- Carlisle Companies Incorporated

- Bostik SA

Top Two Companies

3M Company

- Market share: 12%

- Positioning: Global leader in aerospace adhesives, specializing in high-performance epoxy and polyurethane solutions. 3M has invested over USD 150 million in R&D for lightweight bonding systems, achieving a 10% improvement in tensile strength across product lines. The company’s presence in 25 domestic and international facilities ensures supply to commercial and military aircraft segments, reinforcing Aviation Adhesives And Sealants market dominance.

Henkel AG & Co. KGaA

- Market share: 10%

- Positioning: Henkel is renowned for high-temperature silicone sealants and structural adhesives, with 8 manufacturing facilities in the United States. The company achieved a 9% increase in production efficiency in 2025 and secured contracts with leading commercial and defense aerospace companies. Henkel’s technology-driven innovation reinforces Aviation Adhesives And Sealants market growth and share.

Investment

The United States Aviation Adhesives And Sealants market attracts significant investment, with over 40% allocated to R&D and production expansion. Sector-wise, commercial aviation accounts for 55% of investments, military 30%, and general aviation 15%. Regional allocation includes 60% in the United States and 25% in North America, with the remaining 15% directed towards export-oriented production. M&A agreements, such as 3M’s acquisition of specialty adhesive startups, and collaborations between Henkel and UAV manufacturers, are expanding market presence and accelerating innovation. Over 2026–2034, investors are focusing on advanced epoxy adhesives, high-performance silicone sealants, and automation technology, representing a USD 450 million opportunity in emerging aerospace segments. Investment in lightweight composite-compatible adhesives is projected to grow at 8% CAGR, reinforcing Aviation Adhesives And Sealants market growth potential.

New Product

New product development in Aviation Adhesives And Sealants accounts for approximately 20% of total production in 2025. Innovations include UV-curable epoxy systems with 15% faster curing times, silicone sealants with 10% higher temperature resistance, and polyurethane adhesives with 12% improved impact resistance. Manufacturers are emphasizing lightweight, sustainable, and low-VOC formulations, increasing adoption in both commercial and military applications. Continuous R&D efforts contribute to 8–12% improvement in bonding performance and efficiency, highlighting the focus on innovation and reinforcing Aviation Adhesives And Sealants market insights.

Recent Development in United States Aviation Adhesives And Sealants Market

- 2025: 3M introduced high-temperature epoxy adhesives with 12% improved tensile strength, expanding commercial aircraft adoption by 8%.

- 2024: Henkel launched silicone sealants achieving 10% faster curing, adopted by military aircraft manufacturers for engine components.

- 2023: H.B. Fuller expanded its U.S. production capacity by 15%, producing an additional 45 tons of polyurethane adhesives for commercial aviation.

Research Methodology for United States Aviation Adhesives And Sealants Market

The United States Aviation Adhesives And Sealants market research process involved both primary and secondary research methodologies. Primary research included interviews with over 50 industry experts, manufacturers, and end-users to gather qualitative insights on market trends, adoption, and demand patterns. Secondary research comprised a comprehensive review of annual reports, company filings, industry publications, government statistics, and technical papers. Market size estimation utilized bottom-up and top-down approaches, integrating historical production data (2022–2024), current year metrics (2026), and forecast models for 2026–2034. Cross-validation ensured accuracy in market sizing, segmentation, and regional analysis. The methodology incorporated quantitative production volumes, unit consumption, pricing trends, and penetration rates to deliver a robust, data-driven Aviation Adhesives And Sealants market report, offering actionable insights for investors, manufacturers, and stakeholders.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Polymers, Composites, and Sustainable Materials

Ruby Potts is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.