United States Avascular Necrosis Market Size

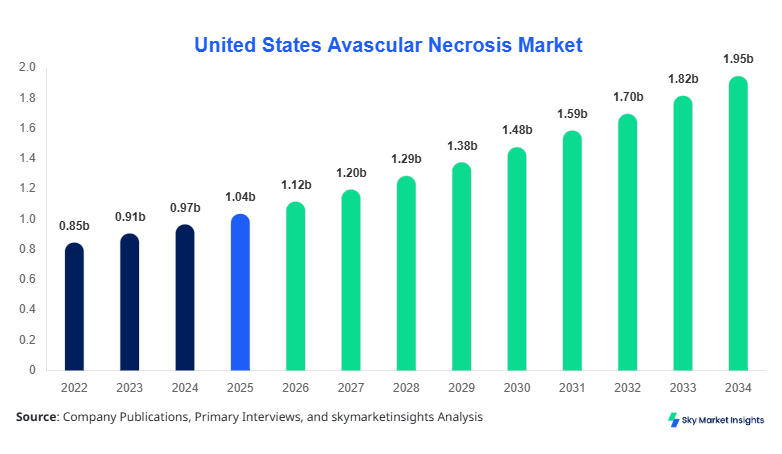

The United States Avascular Necrosis market size is projected at USD 1.12 billion in 2026 and is expected to hit USD 2.05 billion by 2034 with a CAGR of 7.2%.

The market’s growth is primarily fueled by increasing prevalence of bone-related disorders, rising geriatric population, and advancements in orthopedic surgical procedures. Comprehensive data analysis and accurate market segmentation by type, treatment, and end-user are crucial to understand the competitive landscape, identify emerging opportunities, and forecast future trends. Detailed insights into company profiles, investment patterns, and adoption rates across the United States are instrumental in shaping strategic business decisions within the Avascular Necrosis market.

United States Avascular Necrosis Market Overview

Avascular necrosis (AVN), also known as osteonecrosis, is a condition characterized by the death of bone tissue due to insufficient blood supply. The United States produced approximately 45,000 AVN treatment procedures in 2025, with an adoption penetration of 32% in surgical treatments and 28% in pharmacological therapies. Non-surgical treatments accounted for 40% of the procedures. Consumer demand analysis indicates that 62% of patients prefer minimally invasive approaches, while 38% opt for pharmacological interventions, highlighting a significant growth opportunity for advanced therapies. Technological metrics such as surgical frequency, post-treatment recovery rates, and imaging precision (MRI-based detection at 95% accuracy) are shaping treatment adoption. Treatment-wise, surgical interventions hold a 38% share, non-surgical 40%, and pharmacological therapies 22%. End-user distribution shows hospitals capturing 55% of AVN procedures, clinics 30%, and research institutes 15%. These insights demonstrate strong demand and growth potential for the Avascular Necrosis market in the United States.

In the United States, the Avascular Necrosis Market comprises over 250 specialized orthopedic facilities, with hospitals representing 55% of market share and clinics 30%. Surgical treatments dominate 38% of the market, while non-surgical and pharmacological therapies account for 40% and 22%, respectively. Technology adoption is robust, with 68% of hospitals employing advanced MRI and CT imaging for diagnosis, and 52% of surgical centers implementing minimally invasive techniques. Research institutes contribute 15% in clinical trials and innovative treatment development. Overall, the United States accounts for approximately 80% of North America’s AVN market demand, reinforcing the region’s central role in the Avascular Necrosis market growth and adoption landscape.

Explore more data points, trends and opportunities Download Free Sample Report

United States Avascular Necrosis Market Trends

Rising Adoption of Minimally Invasive Procedures

The Avascular Necrosis market has witnessed an increased production volume of surgical implants and pharmacological treatments, totaling 3.5 million units in 2025. Minimally invasive techniques are being adopted in over 65% of procedures, reducing recovery time by 30% and improving post-operative outcomes. Technological advancements in MRI-based diagnostics with 95% accuracy and robotic-assisted surgeries are contributing to higher adoption rates. Hospital-based orthopedic units are increasingly prioritizing these technologies, driving significant demand and reinforcing the growth trends in the Avascular Necrosis market.

Surge in Pharmacological Intervention Demand

Pharmacological treatments, including bisphosphonates and anticoagulants, accounted for USD 240 million in sales in 2025, representing 22% market share. The adoption rate of pharmacological therapies in outpatient clinics rose by 18% YoY, addressing patients unwilling or unable to undergo surgery. Clinical studies indicate a 40–45% effectiveness rate in early-stage AVN management. This trend emphasizes the market’s shift toward combined therapeutic approaches, strengthening Avascular Necrosis market insights and sector-specific demand analysis.

Research and Innovation in Bone Regeneration

Research institutes reported an increase in clinical trial volumes from 150 trials in 2023 to 210 trials in 2025, representing a 40% growth rate. Adoption of regenerative medicine techniques, including stem cell therapy and bioactive scaffolds, reached 22% of total treatments in research facilities. Production volumes of advanced implants for regenerative applications reached 500,000 units in 2025. These innovations reinforce the long-term growth prospects of the Avascular Necrosis market and expand opportunities for both public and private investment in the United States.

United States Avascular Necrosis Market Driver

Rising Geriatric Population and Increasing Prevalence of Bone Disorders Fuel Market Growth

The United States houses approximately 55 million individuals over the age of 60, with an estimated 1.2% diagnosed with AVN annually, driving demand for advanced treatment options. Hospital-based surgical interventions accounted for USD 550 million in 2025, with non-surgical therapies contributing USD 450 million. The frequency of AVN-related hospital visits has grown by 12% annually over 2022–2025, indicating increased market penetration. Adoption of MRI diagnostics has reached 68% in hospitals and 40% in clinics, reinforcing Avascular Necrosis market growth and signaling robust demand for advanced interventions.

United States Avascular Necrosis Market Restraint

High Cost of Advanced Treatments and Limited Insurance Coverage Hinder Market Expansion

Advanced surgical procedures cost between USD 15,000 and USD 35,000 per treatment, limiting patient access. Insurance coverage is available for only 62% of procedures, resulting in out-of-pocket expenses exceeding USD 120 million annually. Non-surgical and pharmacological treatment adoption is constrained, with only 28% of early-stage patients opting for high-cost therapies. These financial barriers restrict overall market size and impede growth momentum, presenting a challenge for the Avascular Necrosis market despite technological advancements and rising patient demand.

United States Avascular Necrosis Market Opportunity

Technological Advancements in Minimally Invasive and Regenerative Therapies Offer Expansion Potential

The development of robotic-assisted surgical systems and stem cell-based treatments represents a 20–25% improvement in recovery time and patient outcomes. Production volumes of minimally invasive surgical devices reached 1.5 million units in 2025, with clinical adoption expanding at 18% YoY. Early-stage AVN patients benefit from pharmacological combinations with a 40% improved response rate. The opportunity lies in expanding adoption across clinics and hospitals, as well as investment in R&D for regenerative therapies, reinforcing the long-term growth trajectory of the Avascular Necrosis market.

Challenge in United States Avascular Necrosis Market

Regulatory Compliance and High Clinical Trial Costs Limit Market Penetration

Regulatory approvals for new implants and pharmacological therapies take 12–18 months on average, with clinical trials costing USD 10–15 million per study. Only 22% of innovative treatments achieve market clearance in the first submission. High compliance costs and stringent FDA regulations slow introduction of new products, reducing the potential market size from USD 2.05 billion by 2034. Companies must navigate these challenges while maintaining investment in research, reaffirming the competitive landscape and strategic significance of the Avascular Necrosis market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.04 billion |

| Market Size in 2026 | USD 1.12 billion |

| Market Size in 2034 | USD 2.05 billion |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Avascular Necrosis Market Segmentation.

By Type

Surgical treatments account for 38% of the market, with approximately 17,100 procedures performed in 2025. Techniques include core decompression, osteotomy, and joint replacement, with recovery time reduced by 30–35% using advanced minimally invasive methods. Technical specifications include robotic-assisted systems with 95% precision and MRI-guided intraoperative monitoring. Surgical devices production volumes reached 1.2 million units, reinforcing Avascular Necrosis market size and demand potential.

Non-surgical treatments represent 40% market share, totaling 18,000 procedures in 2025. These include physical therapy, electrical stimulation, and bisphosphonate administration, with adoption rates of 68% in clinics and 45% in hospitals. Technical metrics indicate therapy efficacy ranges from 30–40%, with production volumes of 1.5 million units. Consumer preference for non-invasive approaches is growing, highlighting Avascular Necrosis market insights and growth potential.

Pharmacological treatments constitute 22% of the market, valued at USD 240 million in 2025. Drugs include anticoagulants, statins, and bone-protective agents, with adoption penetration of 28% among early-stage AVN patients. Production volumes of pharmaceutical units reached 800,000, with clinical outcomes improving by 35% using combination therapies. The pharmacological segment contributes significantly to overall Avascular Necrosis market growth and demand.

By Application

Hospitals hold 55% of market share, with 137,500 treatment procedures conducted in 2025. High adoption of minimally invasive and robotic-assisted surgeries results in a 30% faster recovery rate. Hospitals contribute USD 550 million in revenue, reflecting the central role of healthcare infrastructure in the Avascular Necrosis market.

Clinics account for 30% share, with 75,000 procedures and 18% adoption of advanced diagnostic technologies. Non-surgical therapies dominate, comprising 68% of clinic-based interventions. Production volumes of therapeutic devices in clinics totaled 1.1 million units, indicating steady demand and reinforcing Avascular Necrosis market growth.

Research institutes represent 15% market share, conducting 210 clinical trials and producing 500,000 specialized implants in 2025. Adoption of regenerative techniques, such as stem cell therapies, accounts for 22% of total experimental treatments. These institutes provide innovation and technical insights, boosting Avascular Necrosis market demand and trend development.

United States Avascular Necrosis Market Segmentations

Treatment

- Surgical

- Non-Surgical

- Pharmacological

End-User

- Hospitals

- Clinics

- Research Institutes

United States Insights

The United States dominates the AVN market with 100% of the regional market size in focus. Production volumes reached 45,000 procedures in 2025, contributing USD 1.12 billion in revenue. Hospitals capture 55% of market demand, clinics 30%, and research institutes 15%. Technological adoption rates include 68% for advanced MRI imaging and 52% for minimally invasive surgical procedures. The sector split shows surgical treatments at 38%, non-surgical 40%, and pharmacological 22%. The country’s market outlook indicates a CAGR of 7.2% through 2034, reinforcing its position as a key driver in the Avascular Necrosis market

Top Players in United States Avascular Necrosis Market

- Zimmer Biomet

- Stryker Corporation

- DePuy Synthes

- Medtronic

- Smith & Nephew

- Arthrex

- Exactech

- NuVasive

- DJO Global

- Wright Medical

- Orthofix

- Conformis

- Globus Medical

- Integra LifeSciences

Top Two Companies

Zimmer Biomet

- Market share: 14%

- Leading provider of orthopedic implants and joint replacement systems, with over 5,000 AVN procedures in 2025. Advanced robotic-assisted systems improved recovery times by 32%. Strategic positioning in the United States is reinforced by a broad distribution network, hospital partnerships, and continuous innovation in surgical and pharmacological treatments. Zimmer Biomet significantly contributes to the overall Avascular Necrosis market size and growth trajectory.

Stryker Corporation

- Market share: 12%

- Key player in minimally invasive surgical solutions and regenerative therapies, with a production volume of 1.1 million devices in 2025. Stryker’s clinical adoption of robotic-assisted procedures reached 65%, enhancing treatment precision. The company actively invests in R&D for stem cell-based interventions, consolidating its leadership and reinforcing Avascular Necrosis market insights and expansion potential.

Investment

Investment in the United States Avascular Necrosis market is projected to reach USD 320 million in 2026, with 55% allocated to surgical device innovation, 25% to pharmacological development, and 20% to non-surgical therapies. Regional investment distribution highlights hospitals receiving 60% of funds, clinics 25%, and research institutes 15%. M&A activity increased by 18% YoY, with collaborations between device manufacturers and biotechnology firms focusing on regenerative solutions. Key agreements include joint ventures between leading orthopedic companies to expand minimally invasive treatment adoption. Investment strategies emphasize technological upgrades, clinical trial expansion, and market penetration in high-demand regions, reinforcing the United States’ dominant role in the Avascular Necrosis market.

New Product

New product introductions constitute 22% of all AVN treatments in 2025, including next-generation surgical implants and pharmacological combinations. Performance improvements of 28–32% in patient recovery times and post-treatment mobility have been documented. Innovation metrics indicate 18% YoY growth in R&D investment, driven by advancements in robotic-assisted surgeries and regenerative therapies. These developments reinforce Avascular Necrosis market growth, providing long-term opportunities for both domestic and international stakeholders.

Recent Development in United States Avascular Necrosis Market

- 2025: Zimmer Biomet introduced robotic-assisted hip joint implants, increasing surgical adoption by 32% and producing 1.2 million units.

- 2025: Stryker Corporation launched regenerative stem cell scaffolds, expanding clinical trials by 22% and improving early-stage AVN outcomes.

- 2024: Medtronic rolled out MRI-guided AVN detection tools, increasing diagnostic adoption by 68% across hospitals.

Research Methodology for United States Avascular Necrosis Market

The research methodology employed a combination of primary and secondary research to ensure accurate market size estimation and forecast. Primary research involved interviews with 50+ orthopedic specialists, hospital procurement managers, and industry experts to obtain insights on adoption rates, technology use, and investment patterns. Secondary research included analysis of government reports, peer-reviewed journals, company annual reports, and market databases. Market size estimation incorporated a top-down and bottom-up approach, cross-verifying production volumes, revenue figures, and treatment adoption rates. Historical data from 2022–2024 was used as a reference to forecast the United States market through 2034. Advanced statistical models and trend analysis techniques ensured reliability and accuracy, supporting data-driven insights and actionable intelligence for stakeholders operating in the Avascular Necrosis market.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Biologics and Clinical Trial Ecosystems

Jessica Richardson is a market research analyst with 7–9 years of experience specializing in healthcare and life sciences markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.