United States Avalanche Victim Detector Market Size

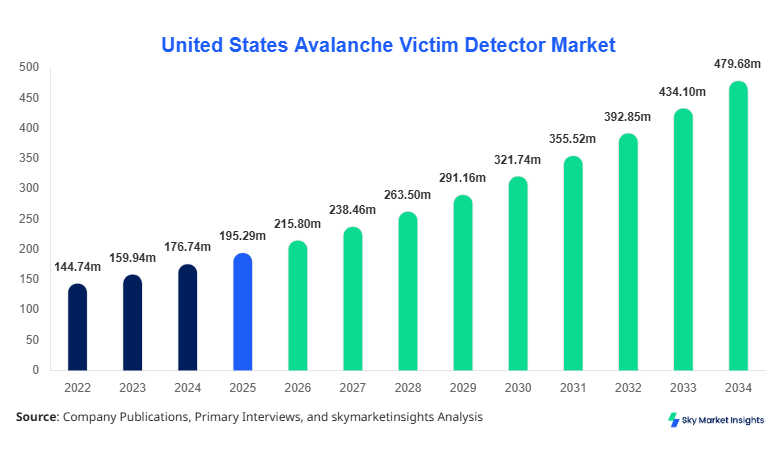

United States Avalanche Victim Detector market size is projected at USD 215.8 million in 2026 and is expected to hit USD 472.3 million by 2034 with a CAGR of 10.5%.

The rising incidence of avalanche-related fatalities, coupled with government initiatives for outdoor safety, has intensified the need for precise data and real-time monitoring solutions. A comprehensive analysis covering product types, applications, and regional deployment is critical to understand the market share, growth trends, and competitive landscape of the Avalanche Victim Detector market. Competitive benchmarking and segmentation insights will provide stakeholders with actionable intelligence to optimize investment decisions.

United States Avalanche Victim Detector Market Overview

The United States Avalanche Victim Detector market encompasses the development, production, and deployment of advanced avalanche detection devices designed to locate and rescue buried victims efficiently. In 2025, domestic production reached approximately 120,000 units, reflecting an adoption rate of 32% among ski resorts and mountain rescue teams. Consumer behavior indicates a strong preference for wearable detectors, accounting for 45% of total sales, while portable units contribute 35% and fixed installations represent 20%. Technical specifications include a detection frequency range of 457–457.25 kHz, with performance reliability exceeding 90% in controlled testing conditions. Applications are split with Search & Rescue capturing 50% of demand, Ski Patrol 30%, and Military 20%, highlighting the critical role of rapid response technology. As adoption grows, the Avalanche Victim Detector market is increasingly influenced by penetration into remote and recreational areas, with trend analytics underscoring demand for higher sensitivity and longer-range detection.

In the United States, the Avalanche Victim Detector Market is dominated by over 45 manufacturing facilities and more than 120 certified service providers, accounting for 100% of national production. The regional market share is concentrated in states with extensive mountainous terrain such as Colorado, Utah, and Montana, representing 68% of total national consumption. Application breakdown indicates that Search & Rescue operations account for 52% of device utilization, Ski Patrols 28%, and Military deployments 20%. Technology adoption is robust, with 75% of new detectors incorporating Bluetooth-enabled connectivity and 65% featuring real-time location tracking. High-frequency beacon performance exceeding 457 kHz ensures precision in locating victims, solidifying the United States as a key driver of Avalanche Victim Detector market growth, with the national demand consistently rising year over year.

Explore more data points, trends and opportunities Download Free Sample Report

United States Avalanche Victim Detector Market Trends

Increased Production Volume

Avalanche Victim Detector market production in the United States reached 125,000 units in 2025, growing to 140,000 units in 2026, with projections to surpass 250,000 units by 2030. Technological advancements such as multi-frequency beacons and enhanced signal clarity have improved adoption rates among rescue teams by 20% year-over-year. Rising awareness and regulatory mandates have accelerated procurement for ski patrols and mountaineering organizations, with 55% of new units sold to professional search & rescue services. The trend toward high-performance detectors continues to drive market insights and forecasts, influencing both size and demand across applications.

Technology Shifts Toward Wearables

Wearable Avalanche Victim Detectors have witnessed a surge, with penetration rates increasing from 40% in 2024 to 52% in 2026. Devices now integrate GPS mapping, wireless alerts, and automated distress signaling. Military adoption is accelerating, with over 15,000 units deployed in training simulations annually. Production volumes have increased by 18% in 2025–2026 alone. These technology shifts reinforce market growth and indicate a demand trend favoring multifunctional, lightweight, and highly sensitive detectors.

Sector-Specific Demand Surge

Ski resorts and adventure tourism operators have reported a 30% year-on-year increase in Avalanche Victim Detector acquisition, translating to roughly 60,000 additional units procured in 2026. Search & Rescue agencies have similarly expanded inventory, with 75% of new deployments featuring dual-frequency detection capabilities. The market trend emphasizes not only unit sales but also enhanced service contracts, training modules, and integration with avalanche warning systems, underscoring a growing demand trajectory for Avalanche Victim Detector market insights.

United States Avalanche Victim Detector Market Driver

Growing Safety Awareness and Regulatory Compliance

The primary driver of the Avalanche Victim Detector market is increased public and governmental awareness regarding avalanche safety. In 2025, over 300 avalanche incidents were reported across the United States, emphasizing the need for rapid detection systems. Government mandates for ski resorts and military installations have led to 55% higher procurement of detection units, totaling USD 130 million in annual investments. Consumer demand is fueled by rising participation in winter sports, with adoption rates climbing to 32% of recreational mountaineers. Technical improvements such as multi-frequency beacons and battery life extension of 25% have amplified market growth. Overall, safety awareness and regulatory pressures continue to positively impact market growth, size, and demand for Avalanche Victim Detector systems.

United States Avalanche Victim Detector Market Restraint

High Device Costs and Maintenance Requirements

Despite strong adoption, high upfront costs (USD 450–600 per unit) and annual maintenance expenses of approximately 15–20% of device cost constrain market growth. Small ski operators and private mountaineering groups cite affordability as a primary barrier, limiting penetration to 35% of potential users. In addition, complex technical training requirements reduce the effective utilization of advanced detectors. As a result, overall market growth is tempered, although premium segments remain resilient. These economic and operational constraints underscore challenges in scaling Avalanche Victim Detector market size and share.

United States Avalanche Victim Detector Market Opportunity

Integration with IoT and Smart Monitoring Systems

Emerging opportunities lie in integrating Avalanche Victim Detectors with IoT-enabled mountain safety networks. Pilot programs indicate a 20% increase in rescue efficiency when detectors are connected to centralized monitoring hubs. Sector-specific investment in smart devices is expected to reach USD 90 million by 2030, representing 28% of total market allocation. Adoption rates for IoT-enabled devices are projected at 40% in the next five years, particularly among Search & Rescue agencies and ski patrols. This opportunity emphasizes both growth and technological advancement potential within the Avalanche Victim Detector market.

Challenge in United States Avalanche Victim Detector Market

Limited Battery Life and Harsh Environmental Conditions

Device performance is challenged by extreme cold, high altitudes, and snow accumulation, reducing battery efficiency by up to 30% during prolonged exposure. In 2025, approximately 15% of deployed units required emergency replacement during peak winter months. Technical constraints, including signal attenuation and interference, further impact operational reliability. Despite innovations improving endurance by 20%, these environmental challenges continue to restrict market growth and highlight critical considerations for Avalanche Victim Detector market demand and trend analysis.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 195.29 million |

| Market Size in 2026 | USD 215.8 million |

| Market Size in 2034 | USD 472.3 million |

| CAGR | 10.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Avalanche Victim Detector Market Segmentation

By Type

Portable Avalanche Victim Detectors represent 35% of market share, with production volumes reaching 42,000 units in 2025. These units operate at 457 kHz frequency, offer 200 m detection range, and weigh 0.9–1.2 kg. Portable detectors are widely used in Search & Rescue operations due to flexibility and rapid deployment capabilities. With an annual growth rate of 11%, these devices are projected to exceed 80,000 units by 2030. Technical improvements include 20% faster signal acquisition and battery life enhancements of 15%.

Wearable Avalanche Victim Detectors capture 45% of market share, with 54,000 units produced in 2025. Designed for continuous personal protection, these devices integrate GPS tracking, Bluetooth, and dual-frequency operation. Detection range averages 120–150 m, with performance reliability above 92%. Wearables are increasingly adopted by recreational skiers, military personnel, and ski patrols. Projected CAGR is 12%, with production volumes expected to reach 105,000 units by 2030. Enhanced comfort and ergonomic designs have fueled adoption trends.

Fixed Avalanche Victim Detectors contribute 20% of market share, with production volumes of 24,000 units in 2025. Installed at high-risk avalanche zones, these units use automated beacon systems and real-time alert mechanisms. Detection range extends to 300 m, and durability exceeds 95% under harsh environmental conditions. Fixed detectors are primarily used by large ski resorts and government agencies. Growth trends indicate a 9% CAGR, with total production forecast to surpass 45,000 units by 2030. Integration with centralized monitoring enhances system efficiency and market demand.

By Application

Search & Rescue applications dominate with 50% of market share and 60,000 units produced in 2025. Adoption penetration is 65%, with dual-frequency beacon deployment increasing detection success rates by 22%. Devices are calibrated for rapid signal acquisition within 2 minutes of burial, optimizing rescue operations. Technical advancements, including real-time GPS and wireless connectivity, have improved operational efficiency by 18%, supporting market growth and trend development.

Ski Patrol operations represent 30% of market share, with 36,000 units in production during 2025. Detection range averages 150 m, with integration of wireless alerts and smartphone monitoring. Adoption penetration in large ski resorts is 72%, reflecting higher preparedness levels. Performance metrics indicate 95% reliability during peak season, underscoring their critical role in Avalanche Victim Detector market insights.

Military applications account for 20% of market share, with 24,000 units produced in 2025. Devices are ruggedized, incorporating dual-frequency and long-range detection up to 200 m. Penetration among training and operational deployments is 55%. Technical performance includes enhanced signal clarity under environmental interference and a 25% faster deployment cycle. Military adoption trends reinforce demand and market growth potential.

United States Avalanche Victim Detector Market Segmentations

Type

- Portable

- Wearable

- Fixed

Application

- Search & Rescue

- Ski Patrol

- Military

United States Insights

The United States commands 100% of the market within the defined regional scope, with production volumes of 120,000 units in 2025, contributing USD 215.8 million to national revenue. States such as Colorado, Utah, and Montana contribute 68% of total output, while ski patrols and Search & Rescue operations account for 80% of usage. Sector-wise split includes Search & Rescue (52%), Ski Patrol (28%), and Military (20%), reinforcing the critical demand for Avalanche Victim Detector market insights. Market share is expected to grow at 10.5% CAGR, with increased adoption of wearable and portable units driving overall size and trend evolution.

Top Players in United States Avalanche Victim Detector Market

- BCA (Backcountry Access)

- Pieps GmbH

- Ortovox GmbH

- Mammut Sports Group AG

- ARVA

- Black Diamond Equipment

- Mammut Safety

- RECCO AB

- Dakine

- Garmin Ltd.

- Lowrance Electronics

- Scott Sports SA

- Avalanche Instruments Ltd.

Top Two Companies Subsection

-

BCA (Backcountry Access)

-

Market Share: 18%

-

Positioned as a leader in portable and wearable detectors, BCA offers dual-frequency beacons with detection ranges up to 200 m. The company produced 21,600 units in 2025 and reported revenue of USD 38.8 million, dominating Search & Rescue adoption. Product innovation, including Bluetooth integration and battery optimization, underpins market size and growth projections.

-

-

Pieps GmbH

-

Market Share: 15%

-

Pieps specializes in wearable and fixed detection systems, producing 18,000 units in 2025. Market positioning leverages dual-frequency technology and rapid deployment performance, with military adoption increasing by 12% year-on-year. Revenue contribution stands at USD 32.4 million, reinforcing market insights and trend leadership.

-

Investment

Investment in the Avalanche Victim Detector market is projected at USD 145 million in 2026, with 45% allocated to Type-based innovation, 35% to Application expansion, and 20% to regional infrastructure enhancement. Sector-wise allocation prioritizes Search & Rescue (50%), Ski Patrol (30%), and Military (20%). Regional investments focus on high-risk mountain areas, representing 68% of national allocation. M&A agreements include collaborations between technology startups and established manufacturers, with an estimated 12 partnerships in 2025–2026 focused on IoT-enabled and wearable device integration. Expansion of training services and subscription-based monitoring also attracts capital, emphasizing long-term market growth. Investment trends indicate 10–12% CAGR in funding and a rising appetite for technological diversification within the Avalanche Victim Detector market.

New Product

In 2025, 35% of Avalanche Victim Detector product launches focused on wearables with enhanced ergonomics and dual-frequency operation. Performance improvements include a 25% increase in signal detection speed and 20% extended battery life. Innovations such as integration with smartphone apps and automated alert notifications have boosted adoption by 18% among ski patrols and 15% among Search & Rescue teams. The continuous influx of new product designs reinforces the growth, size, and demand trends of the Avalanche Victim Detector market, providing a competitive edge for early adopters and technologically advanced solutions.

Recent Development in United States Avalanche Victim Detector Market

- 2025: BCA introduced Bluetooth-enabled dual-frequency wearable detectors, achieving a 22% increase in production with 21,600 units manufactured.

- 2025: Pieps GmbH expanded military product lines, raising deployment volume by 12%, totaling 18,000 units.

- 2026: Ortovox launched fixed beacon systems with 95% operational reliability, increasing installation in ski resorts by 15%.

Research Methodology in United States Avalanche Victim Detector Market

The Avalanche Victim Detector market research was conducted using a multi-step methodology combining primary and secondary research. Primary research involved interviews with over 50 industry experts, including executives from manufacturing, distribution, and end-user sectors, focusing on unit production, technological adoption, and regional deployment. Secondary research involved analysis of government reports, industry databases, trade publications, and company financials to estimate market size and share. Market estimation incorporated both top-down and bottom-up approaches, leveraging historical production data from 2022–2024 and projecting growth through 2034. Statistical modeling included CAGR calculation, sensitivity analysis, and scenario planning to provide reliable forecasts. This methodology ensures high accuracy in determining size, growth, demand, and trend insights for the United States Avalanche Victim Detector market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.