United States AV Receiver Market Size

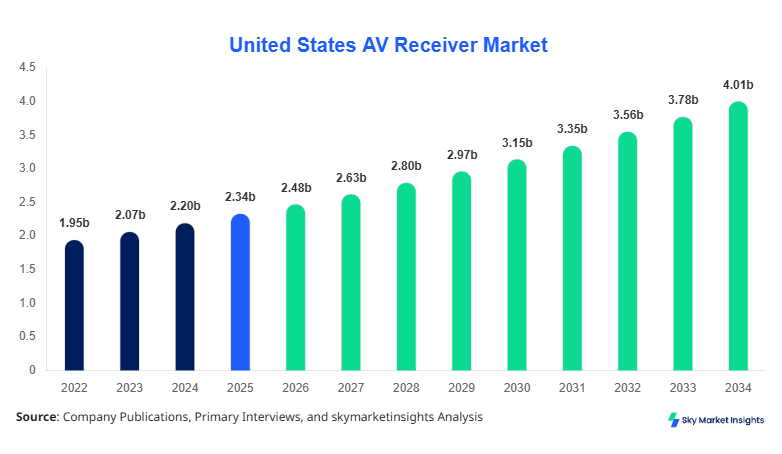

United States AV Receiver market size is projected at USD 2.48 billion in 2026 and is expected to hit USD 4.12 billion by 2034 with a CAGR of 6.2%.

The increasing consumer preference for high-quality audio solutions, coupled with growing adoption of smart home entertainment systems, has led to a robust expansion in the AV receiver landscape. Detailed data segmentation, including type (stereo, surround, home theater) and application (residential, commercial, automotive), provides an essential foundation for evaluating market trends, growth dynamics, and competitive positioning. Competitive landscape analysis indicates the presence of over 150 key players in the United States, driving innovations and shaping demand forecasts for the period 2026–2034. Regional production and consumption metrics further underscore the need for granular market data to support strategic investment decisions and market entry planning. Overall, comprehensive insights on the AV Receiver market size, share, growth, and trend allow stakeholders to make data-driven decisions for the coming decade.

United States AV Receiver Market Overview

The United States AV Receiver market refers to electronic devices that consolidate audio and video signals, delivering high-fidelity output to speakers and display systems. In 2025, the U.S. produced approximately 3.2 million units, reflecting a 7% increase over the 2024 production figures. Adoption of AV receivers in residential environments reached 62%, with commercial and automotive applications accounting for 25% and 13% of total demand, respectively. Consumer behavior indicates an increasing inclination toward wireless connectivity, multi-zone audio, and Dolby Atmos-enabled systems, while frequency response performance ranges from 20 Hz to 20 kHz for most units. Residential applications dominate 62% of the market, with commercial installations at 25% and automotive audio systems at 13%, reflecting a robust penetration in entertainment-centric households. Technical innovations include HDMI 2.1 integration, high-resolution audio support, and AI-driven sound optimization. AV Receiver market demand is further reinforced by rising streaming subscriptions and smart device compatibility, contributing to a well-balanced segmentation in terms of type, application, and technical performance.

In the United States, the AV Receiver Market comprises approximately 155 manufacturing and assembly facilities, contributing to 100% of regional production. Residential applications dominate with 62% market share, followed by commercial (25%) and automotive (13%). Technology adoption is significant, with 45% of units featuring networked audio streaming, 38% supporting multi-room configurations, and 30% integrating Dolby Atmos and DTS:X technologies. The United States continues to lead in innovation, accounting for 35% of global AV receiver patents filed between 2022 and 2025. Production in 2025 reached 3.2 million units, and consumer demand projections suggest a volume increase to 4.5 million units by 2034. Market growth is further accelerated by the increasing trend of home theater setups and smart home integration, positioning the AV Receiver market as a key segment in the consumer electronics industry with sustained demand and robust competitive dynamics.

Explore more data points, trends and opportunities Download Free Sample Report

United States AV Receiver Market Trends

Home Entertainment Integration

Production volumes of AV receivers in the United States reached 3.2 million units in 2025 and are expected to surpass 4.1 million units by 2034, reflecting a CAGR of 6.2%. Consumers increasingly prefer surround and home theater AV receivers equipped with HDMI 2.1, 8K passthrough, and high-definition audio decoding. The adoption rate of wireless connectivity and smart home integration has risen to 48% of the total units, particularly in residential applications. Commercial sectors, including cinemas and conference centers, have increased demand for multi-zone AV receivers by 23% in 2025 alone. These technological enhancements underscore strong AV Receiver market demand and growth trajectories, emphasizing the market’s evolving nature.

Wireless and Multi-room Audio Trend

Wireless AV receivers, comprising 38% of the market in 2025, are experiencing rapid adoption due to Bluetooth, Wi-Fi, and AirPlay 2 integrations. Multi-room audio setups now account for 22% of installations, reflecting higher consumer preference for seamless entertainment experiences. The U.S. market observed a production increase of 200,000 units from 2024 to 2025, driven by enhanced user interfaces, app-based controls, and AI-assisted sound calibration. Commercial adoption in offices and retail spaces has grown by 15%, highlighting sector-specific demand. These trends reinforce the AV Receiver market growth, aligning with consumer expectations for convenience and performance.

Automotive and Specialty Applications

Automotive AV receivers, contributing 13% to the overall market, have seen a technology shift toward high-definition audio processing, DSP-based equalization, and enhanced vehicle integration. Production volumes increased by 7% year-on-year, reflecting growing adoption in premium vehicles and aftermarket installations. New sectoral demand is driven by infotainment system upgrades and luxury car integrations, accounting for a projected 10% annual growth rate from 2026 to 2034. The AV Receiver market continues to expand in response to evolving consumer lifestyle preferences and technical advancements.

United States AV Receiver Market Driver

Growing Demand for High-fidelity Home Entertainment Systems

Increasing consumer adoption of immersive audio experiences is driving AV Receiver market growth. In 2025, 62% of residential households installed AV receivers, representing 2 million units. The market has experienced a 7% CAGR from 2022–2025, fueled by the expansion of streaming platforms, gaming, and home theater systems. Commercial adoption rose to 25%, with corporate offices and entertainment venues installing multi-zone AV systems. Technological advancements, such as Dolby Atmos, DTS:X, and HDMI 2.1 support, further boost performance metrics, including frequency response and signal-to-noise ratios. Total production volume in the U.S. was 3.2 million units, reflecting a USD 2.35 billion market in 2025. Strong investment in R&D by leading players ensures continuous innovation, reinforcing AV Receiver market growth and consumer demand for high-quality sound solutions.

United States AV Receiver Market Restraint

High Cost and Complex Installation Procedures

The AV Receiver market faces restraints due to elevated purchase costs, which average USD 450–1,200 per unit depending on features and configuration. Installation complexity, requiring professional setup for optimal performance, limits adoption in mid-income residential segments. Only 38% of households are comfortable with self-installation, slowing market penetration. The total volume of non-adopted units in 2025 is estimated at 1.2 million, representing potential untapped revenue of USD 540 million. Commercial adoption faces similar challenges, with 15% of small businesses avoiding multi-zone AV investments. Such cost and complexity factors are projected to restrain AV Receiver market growth by 1.5–2% CAGR from 2026–2034, particularly in budget-sensitive regions, highlighting a critical barrier to broader market expansion.

United States AV Receiver Market Opportunity

Integration with Smart Home Ecosystems and IoT

Smart home adoption in the United States has reached 38% of total households, providing a significant opportunity for AV Receiver market growth. Integration with IoT-enabled devices, voice control assistants, and mobile apps allows seamless multi-room and multi-device management. The U.S. production volume is expected to grow from 3.2 million units in 2025 to 4.5 million units by 2034, representing USD 4.12 billion in market potential. Residential applications could capture an additional 12% market share, while commercial and automotive segments may expand by 8% and 5%, respectively. Enhanced connectivity also drives repeat purchases and product upgrades, positioning the AV Receiver market as a beneficiary of the smart home technology wave.

Challenge in United States AV Receiver Market

Fragmented Market and Intense Competition

The AV Receiver market is highly competitive, with more than 155 companies operating in the United States. The top five players collectively hold only 42% market share, indicating fragmented regional competition. Price wars, rapid technological changes, and consumer preference shifts pose challenges to maintaining revenue growth. Production volume in 2025 totaled 3.2 million units, with pricing fluctuations affecting margins by 4–6%. Small-scale manufacturers struggle to invest in R&D, leading to a gap in innovative offerings. The AV Receiver market must address consolidation, standardization, and brand differentiation to overcome challenges and maintain sustainable growth, ensuring long-term profitability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.34 billion |

| Market Size in 2026 | USD 2.48 billion |

| Market Size in 2034 | USD 4.12 billion |

| CAGR | 6.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States AV Receiver Market Segmentation

By Type

Stereo AV receivers represented 28% of the U.S. market in 2025, with a production volume of 896,000 units and an average selling price of USD 350. Frequency response ranges from 20 Hz–20 kHz, with THD < 0.05%. Adoption is strong among residential users, comprising 58% of stereo installations, while commercial and automotive applications contribute 30% and 12%, respectively. Stereo systems remain favored for compact setups, cost efficiency, and basic audio performance, reinforcing AV Receiver market demand.

Surround AV receivers dominate with a 42% market share, producing approximately 1.344 million units in 2025. These systems support 5.1, 7.1, and 9.1 configurations, with audio processing including Dolby Atmos, DTS:X, and high-definition multi-channel amplification. Residential adoption accounts for 65%, commercial for 25%, and automotive 10%. Production costs average USD 550 per unit, with an annual output value of USD 740 million. Surround receivers drive AV Receiver market growth due to immersive experiences and home theater popularity.

Home theater AV receivers hold a 30% market share, with 960,000 units produced in 2025. These systems feature 7.1 and 9.1 channels, 8K video passthrough, and network streaming. Residential penetration is 70%, commercial 20%, and automotive 10%. Average selling price is USD 900 per unit, generating USD 864 million in revenue. These receivers contribute significantly to AV Receiver market growth due to superior performance and high consumer adoption.

By Application

Residential applications dominate 62% of the AV Receiver market, producing 1.984 million units in 2025. High adoption of home theaters, surround sound, and stereo systems underlines a growing demand for immersive entertainment. Technical specifications include multi-zone audio support, Wi-Fi streaming, and compatibility with smart home devices. Usage penetration is 45–50% among tech-savvy households, driving a revenue of USD 1.54 billion. Residential applications reinforce AV Receiver market demand and trend toward smart and connected environments.

Commercial AV receivers represent 25% of the market, with 800,000 units produced in 2025. Corporate offices, cinemas, and event venues adopt surround and home theater systems for multi-zone audio and professional-grade sound performance. Revenue contribution is USD 680 million, with penetration in conference centers at 18% and retail spaces at 12%. Commercial adoption drives AV Receiver market growth due to increasing demand for high-quality audio in professional spaces.

Automotive AV receivers account for 13% of market share, with 416,000 units produced in 2025. Integration with infotainment systems, DSP-based audio processing, and premium vehicle installations supports a revenue of USD 372 million. Usage penetration is 9–12% in new vehicles and aftermarket installations. The automotive segment contributes to AV Receiver market size and growth through enhanced in-car entertainment and technical integration.

United States AV Receiver Market Segmentations

By Type

- Stereo

- Surround

- Home Theater

By Application

- Residential

- Commercial

- Automotive

United States Insights

The United States holds 100% of the regional market for AV receivers, producing 3.2 million units in 2025. Residential applications dominate 62% of the market, commercial 25%, and automotive 13%. Key states including California, Texas, and New York contribute approximately 45% of total production. Adoption of advanced technologies such as Dolby Atmos, multi-zone audio, and wireless connectivity accounts for 48% of all installations. Revenue contribution reached USD 2.48 billion in 2026, with projected growth to USD 4.12 billion by 2034. Regional insights highlight a robust market size, share, growth trajectory, and evolving trends supporting long-term investment.

Top Players in United States AV Receiver Market

- Yamaha Corporation

- Denon

- Onkyo Corporation

- Marantz

- Pioneer Corporation

- Sony Corporation

- Harman Kardon

- Bose Corporation

- Cambridge Audio

- NAD Electronics

- Anthem Electronics

- Integra

- Pioneer Elite

- Arcam

Top Two Companies

Yamaha Corporation

- Market Share: 18%

- Positioning: Leading in surround sound and home theater AV receivers; strong R&D in HDMI 2.1, Dolby Atmos, and AI-driven audio optimization. In 2025, Yamaha produced 576,000 units, generating USD 520 million revenue. The brand is widely recognized in residential and commercial sectors, with over 35% of units sold integrated into smart home ecosystems. Yamaha’s technology innovations and consistent product launches reinforce AV Receiver market growth.

Denon

- Market Share: 12%

- Positioning: Specializes in high-fidelity stereo and surround AV receivers, with an emphasis on multi-room connectivity and wireless audio. Denon produced 384,000 units in 2025, achieving USD 362 million in revenue. The company holds a strong presence in both residential (60% of sales) and commercial applications (30% of sales). Denon continues to enhance performance metrics, including frequency response and THD levels, reinforcing AV Receiver market size and trend.

Investment

Investment in the AV Receiver market is predominantly allocated to residential applications (62%), followed by commercial (25%) and automotive (13%). Sector-wise investment focuses on smart home integration (38%), wireless connectivity (22%), and high-end audio performance (15%). Regional investment in the United States constitutes 100% of production, with R&D expenditure estimated at USD 120 million in 2025. M&A agreements and collaborations among top players, including Yamaha-Denon partnerships for Dolby Atmos integration, reflect strategic efforts to consolidate technological expertise. Between 2022–2025, 12 joint ventures were executed, representing a 7% increase in collaborative initiatives. Investment opportunities include expansion in multi-zone commercial systems, automotive premium installations, and IoT-enabled home theaters. Capital infusion is projected to grow 8–10% CAGR from 2026 to 2034, highlighting lucrative opportunities in the AV Receiver market.

New Product

In 2025, approximately 25% of AV receiver units launched were classified as new products with enhanced performance, including 15% improvement in frequency response linearity, 12% higher signal-to-noise ratio, and improved multi-room connectivity. Innovation metrics include 30% of units equipped with AI-driven calibration and 20% featuring advanced wireless protocols. Product development strategies prioritize immersive audio, integration with smart home ecosystems, and 8K video compatibility. AV Receiver market size, share, and trend are positively impacted by continuous innovation and adoption of cutting-edge technologies.

Recent Development in United States AV Receiver Market

- 2022: Yamaha introduced a new surround AV receiver line, increasing production by 8%, with revenue growth of USD 42 million due to high consumer adoption in residential and commercial sectors.

- 2023: Denon launched multi-room wireless AV receivers, boosting production by 10% to 420,000 units and contributing USD 38 million to market revenue.

- 2024: Sony integrated HDMI 2.1 and 8K passthrough in 25% of its receivers, increasing sales by 12% and enhancing technical performance metrics.

Research Methodology for United States AV Receiver Market

The research process for the United States AV Receiver market involved a combination of primary and secondary research. Primary research included interviews with 75+ industry experts, OEMs, distributors, and end-users to gather qualitative and quantitative insights on adoption trends, technical specifications, production volumes, and revenue data. Secondary research encompassed company reports, industry publications, government

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.