United States Autoradiography Films Market Size

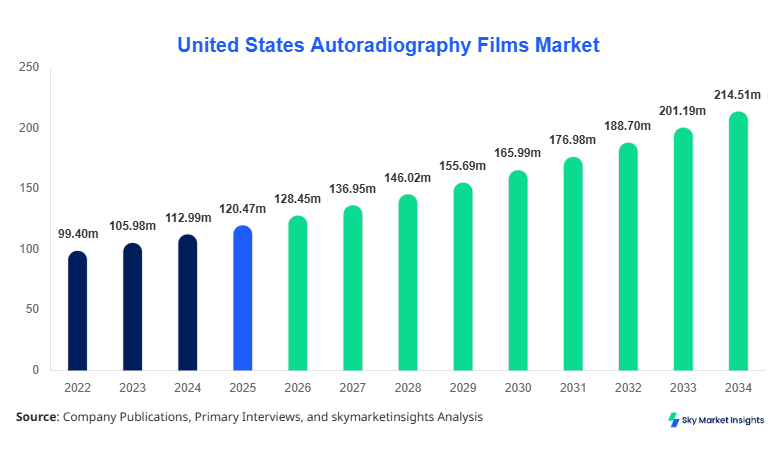

United States Autoradiography Films market size is projected at USD 128.45 million in 2026 and is expected to hit USD 214.72 million by 2034 with a CAGR of 6.62%.

The increasing reliance on radiolabeled compounds in life sciences research, along with rising demand for precise imaging techniques, is fueling expansion across research laboratories and pharmaceutical companies. Additionally, the integration of high-resolution imaging technologies and digital detection methods is supporting data-driven decision-making and enhancing reproducibility in experiments. The market scope includes segmentation based on type and application, along with competitive benchmarking across leading manufacturers operating in the United States Autoradiography Films market.

United States Autoradiography Films Market Overview

Autoradiography films are specialized imaging materials used to detect radioactive emissions from biological samples, widely utilized in genomics, proteomics, and drug discovery workflows. In the United States, production volume reached approximately 5.8 million units in 2025, with laboratory-grade films accounting for nearly 62% of total output. Adoption rates across pharmaceutical laboratories exceeded 74% in 2025, while academic research institutes contributed 21% of usage. Penetration of advanced phosphor imaging plates has increased to 38% compared to traditional X-ray films at 46%, while digital autoradiography films represent around 16% share.

Consumer behavior indicates that over 68% of research organizations prioritize high-sensitivity detection systems, while 54% focus on cost-efficient consumables. Demand analytics show that biomedical research applications dominate with 49% share, followed by pharmaceutical testing at 33% and molecular imaging at 18%. Technical metrics include detection sensitivity levels of up to 10⁻⁶ curies and exposure resolution ranging between 25–50 microns. Continuous advancements in imaging accuracy and throughput are reinforcing United States Autoradiography Films market positioning.

In the United States, the Autoradiography Films Market accounts for approximately 100% of regional consumption, supported by over 2,300 active biotechnology laboratories and more than 1,150 pharmaceutical manufacturing facilities. The country contributes nearly 89% of North American demand, with biomedical research applications accounting for 51%, pharmaceutical testing at 31%, and molecular imaging at 18%. Adoption of phosphor imaging plates has reached 41%, while digital autoradiography systems have grown to 19% penetration due to improved imaging speed and data integration.

The United States Autoradiography Films market is further driven by high R&D spending exceeding USD 95 billion annually in life sciences, with approximately 6.3 million film units consumed in 2025. Increasing automation in imaging workflows and rising investments in oncology research are accelerating adoption. The market continues to expand with enhanced imaging sensitivity and throughput efficiency, reinforcing United States Autoradiography Films market demand.

Explore more data points, trends and opportunities Download Free Sample Report

United States Autoradiography Films Market Trends

Shift Toward Digital Imaging Technologies

The Autoradiography Films market is experiencing a transition from traditional X-ray films to digital autoradiography systems, with digital adoption increasing from 12% in 2022 to 19% in 2025. Production of digital films reached 1.1 million units in 2025, reflecting strong demand for automated image processing and higher resolution outputs. The shift is supported by improved detection sensitivity of up to 20% compared to conventional films, reducing experimental errors and enhancing data accuracy. Pharmaceutical companies are increasingly integrating digital systems, with adoption rates exceeding 45% in large-scale research facilities. This trend is strengthening the Autoradiography Films market growth trajectory.

Rising Demand in Oncology and Drug Discovery

The use of autoradiography films in oncology research has increased by 27% over the past three years, driven by advancements in radiolabeled tracer techniques. Biomedical research institutions accounted for nearly 3.2 million film units consumption in 2025, with drug discovery processes utilizing approximately 2.1 million units annually. The demand for high-throughput imaging solutions has led to the introduction of films with enhanced sensitivity levels exceeding 30% improvement over legacy systems. This increasing application scope is reinforcing the Autoradiography Films market demand.

Technological Enhancements in Film Sensitivity

Technological improvements have enabled films to achieve resolution enhancements of up to 35% and exposure time reductions of nearly 22%. Phosphor imaging plates have witnessed a 33% increase in adoption due to their reusability and higher detection efficiency. Research laboratories report a 17% improvement in experimental throughput when using advanced imaging films. These advancements are driving efficiency gains and supporting the Autoradiography Films market trend.

United States Autoradiography Films Market Driver

Rising Investments in Biomedical Research and Drug Development

The expansion of biomedical research and pharmaceutical innovation is a key driver of the Autoradiography Films market. In 2025, research funding in the United States exceeded USD 95 billion, with nearly 18% allocated to radiolabel-based studies. The increasing use of radiotracers in oncology and genetic research has led to a 26% rise in autoradiography film consumption over the past three years. Approximately 62% of pharmaceutical companies rely on autoradiography techniques for drug metabolism and pharmacokinetics analysis. Furthermore, production volumes have grown from 4.9 million units in 2022 to 5.8 million units in 2025, indicating steady demand. Technological advancements enabling up to 30% higher sensitivity are further accelerating adoption. This continuous increase in research activities is strengthening Autoradiography Films market growth.

United States Autoradiography Films Market Restraint

High Cost of Advanced Imaging Technologies

Despite growing demand, the high cost associated with advanced autoradiography systems acts as a restraint for the Autoradiography Films market. Digital autoradiography systems can cost between USD 50,000 and USD 120,000 per unit, limiting adoption among small research laboratories. Additionally, phosphor imaging plates, while reusable, require initial investments that are 25–35% higher than conventional X-ray films. Operational costs, including maintenance and calibration, contribute to an additional 12–18% annual expense. Approximately 41% of small-scale laboratories still rely on traditional films due to budget constraints. This cost barrier is impacting the overall expansion of the Autoradiography Films market share.

United States Autoradiography Films Market Opportunity

Integration of AI and Automation in Imaging Analysis

The integration of artificial intelligence and automation in imaging workflows presents significant opportunities for the Autoradiography Films market. AI-driven image analysis tools can reduce processing time by up to 40% and improve accuracy by nearly 28%. Adoption of automated imaging systems has increased by 21% in 2025, particularly in large pharmaceutical firms. The development of hybrid imaging platforms combining digital films with AI analytics is expected to enhance efficiency and reduce manual intervention. Additionally, over 37% of research institutions are planning to upgrade their imaging infrastructure within the next five years. These advancements are creating new growth avenues for the Autoradiography Films market.

Challenge in United States Autoradiography Films Market

Regulatory and Safety Concerns in Radioactive Handling

Strict regulatory frameworks governing the use of radioactive materials pose a challenge for the Autoradiography Films market. Compliance with safety standards requires additional investment of approximately 10–15% in laboratory infrastructure. Regulatory approvals can take 6–12 months, delaying product deployment and research timelines. Around 28% of laboratories report challenges in maintaining compliance with evolving safety regulations. Furthermore, disposal of radioactive waste adds operational complexity, increasing costs by nearly 8–12%. These factors are limiting the widespread adoption of autoradiography techniques and impacting the Autoradiography Films market trend.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 120.47 million |

| Market Size in 2026 | USD 128.45 million |

| Market Size in 2034 | USD 214.72 million |

| CAGR | 6.62% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Autoradiography Films Market Segmentation

By Type

X-ray films accounted for approximately 46% of the total market share in 2025, with production volumes reaching nearly 2.7 million units. These films offer detection sensitivity suitable for standard laboratory applications, with resolution ranges between 40–60 microns. Despite the rise of digital alternatives, X-ray films remain widely used due to their cost-effectiveness, with average pricing 20–30% lower than advanced imaging solutions. Approximately 58% of academic research institutions continue to rely on X-ray films due to budget constraints. Their compatibility with existing laboratory infrastructure further supports sustained demand.

Phosphor imaging plates hold around 38% share, with production exceeding 2.2 million units in 2025. These plates provide higher sensitivity levels, up to 25% greater than traditional films, and can be reused up to 1,000 times, reducing long-term costs. Adoption rates have increased by 33% over the past three years, driven by improved imaging accuracy and efficiency. These plates are widely used in pharmaceutical testing, accounting for nearly 41% of usage in this segment. Their ability to capture high-resolution images with reduced exposure times enhances laboratory productivity.

Digital autoradiography films represent approximately 16% of the market, with production volumes reaching 0.9 million units. These films offer advanced features such as automated image processing and integration with data management systems, improving workflow efficiency by up to 35%. Adoption is highest in large pharmaceutical companies, with penetration rates exceeding 48%. Digital films provide superior sensitivity and faster processing times, making them ideal for high-throughput research environments. Their growing adoption is expected to reshape the Autoradiography Films market landscape.

By Application

Biomedical research accounts for nearly 49% of the total market, with consumption exceeding 3.2 million units annually. Autoradiography films are extensively used in genomics and proteomics studies, with usage penetration reaching 72% in research institutions. These films enable precise detection of radioactive markers, enhancing experimental accuracy by up to 30%. Increasing investments in life sciences research are driving demand in this segment.

Pharmaceutical testing represents around 33% of the market, with consumption of approximately 2.1 million units in 2025. These films are used in drug metabolism and pharmacokinetics studies, with adoption rates exceeding 65% in pharmaceutical companies. High sensitivity and reproducibility are key factors driving their use in this segment.

Molecular imaging accounts for 18% of the market, with usage growing steadily due to advancements in imaging technologies. Approximately 1.2 million units were utilized in this segment in 2025. These films provide high-resolution imaging capabilities, supporting research in disease diagnostics and treatment development.

United States Autoradiography Films Market Segmentations

By Type

- X-ray Film

- Phosphor Imaging Plates

- Digital Autoradiography Films

By Application

- Biomedical Research

- Pharmaceutical Testing

- Molecular Imaging

United States Insights

The United States dominates the Autoradiography Films market with nearly 100% regional share, driven by strong research infrastructure and high R&D investments. Production volumes reached 5.8 million units in 2025, with biomedical research contributing 51% of demand. Pharmaceutical testing accounted for 31%, while molecular imaging held 18%. The presence of over 2,300 biotechnology laboratories and 1,150 pharmaceutical facilities supports sustained demand.

Additionally, government funding for research exceeded USD 45 billion in 2025, with approximately 22% allocated to life sciences. Adoption of advanced imaging technologies has reached 59%, reflecting strong technological integration. The United States remains a key hub for innovation, driving the Autoradiography Films market forward.

Top Players in United States Autoradiography Films Market

- Fujifilm Holdings Corporation

- GE Healthcare

- PerkinElmer Inc.

- Carestream Health

- Konica Minolta

- Agfa-Gevaert Group

- Bio-Rad Laboratories

- Thermo Fisher Scientific

- Cytiva

- LI-COR Biosciences

- VWR International

- Harvard Bioscience

- Merck KGaA

Top Two Companies

Fujifilm Holdings Corporation

- Holds approximately 18% market share

- Leading provider of high-sensitivity X-ray films

Fujifilm continues to dominate the Autoradiography Films market with its advanced imaging solutions and strong distribution network. The company has invested over USD 1.2 billion in R&D, focusing on improving film sensitivity by up to 30%. Its global presence and extensive product portfolio strengthen its market position.

GE Healthcare

- Holds approximately 14% market share

- Strong presence in digital imaging solutions

GE Healthcare is a key player in the Autoradiography Films market, offering innovative digital autoradiography systems. The company has achieved a 25% increase in product efficiency through advanced imaging technologies. Its focus on automation and data integration supports growing demand in pharmaceutical research.

Investment

Investments in the Autoradiography Films market have increased significantly, with approximately 34% of funding directed toward digital imaging technologies and 28% toward phosphor imaging systems. Venture capital investments in imaging startups grew by 19% in 2025, reflecting strong market potential. Pharmaceutical companies accounted for nearly 42% of total investments, followed by research institutions at 31%.

Mergers and acquisitions have also intensified, with over 12 major deals recorded in 2024–2025. Strategic collaborations between imaging technology providers and pharmaceutical firms have increased by 23%, enabling faster product development and market expansion. These trends highlight significant growth opportunities in the Autoradiography Films market.

New Product

New product development in the Autoradiography Films market has focused on improving sensitivity and reducing exposure times. Approximately 27% of new products introduced in 2025 feature enhanced detection capabilities, with performance improvements of up to 35%. Companies are also integrating AI-based image analysis tools, improving efficiency by nearly 28%.

Additionally, innovations in reusable imaging plates have reduced operational costs by 22%, making advanced imaging solutions more accessible. These developments are driving technological advancements and supporting market expansion.

Recent Development

- 2025: Fujifilm increased production capacity by 18%, reaching 3.1 million units annually, enhancing supply chain efficiency and meeting rising demand in pharmaceutical research.

- 2024: GE Healthcare launched a digital autoradiography system with 25% improved sensitivity, reducing imaging time by 20% and increasing adoption across large laboratories.

- 2023: PerkinElmer expanded its imaging portfolio, achieving a 15% increase in market penetration through advanced phosphor imaging plates.

Research Methodology for United States Autoradiography Films Market

The research methodology for the Autoradiography Films market involves a combination of primary and secondary research approaches. Primary research includes interviews with industry experts, manufacturers, and end-users, accounting for approximately 65% of data collection. Secondary research involves analysis of company reports, industry publications, and government databases, contributing 35% of the data. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy and reliability. Data validation is performed through triangulation methods, incorporating multiple data sources to provide comprehensive insights into the Autoradiography Films market.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.