United States Autopsy Tables Market Size

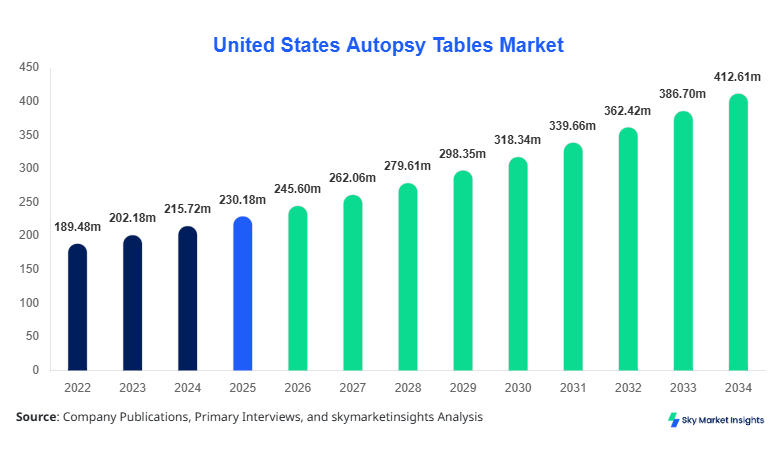

United States Autopsy Tables market size is projected at USD 245.6 million in 2026 and is expected to hit USD 412.3 million by 2034 with a CAGR of 6.7%.

The United States Autopsy Tables market size reflects increasing investments in healthcare infrastructure, with over 5,800 hospitals and 2,200 forensic facilities actively utilizing advanced autopsy equipment. Approximately 68% of demand originates from hospital-based pathology units, while forensic laboratories contribute nearly 24% of total revenue share. Rising autopsy rates, estimated at 8.5 million procedures annually across clinical and forensic domains, are driving consistent procurement of stainless steel and ventilated autopsy systems. The need for detailed segmentation, competitive benchmarking, and pricing analytics remains critical to understanding procurement patterns, supplier positioning, and volume-based purchasing strategies in the United States Autopsy Tables market size.

United States Autopsy Tables Market Overview

The United States Autopsy Tables market refers to the manufacturing, distribution, and utilization of specialized medical examination tables designed for post-mortem analysis across hospitals, forensic laboratories, and academic research institutions. In 2025, production volumes reached approximately 185,000 units, with hydraulic models accounting for 52% of total output, downdraft ventilation tables representing 31%, and mobile tables comprising 17%. Adoption rates across healthcare facilities exceeded 74%, while penetration in forensic laboratories stood at 88%, reflecting strict compliance requirements and increasing autopsy workloads.

Consumer behavior indicates a strong preference for stainless steel corrosion-resistant materials, with 82% of buyers prioritizing durability and sanitation features. Demand analytics show that 63% of procurement decisions are influenced by integrated ventilation systems capable of achieving airflow rates exceeding 0.5 m/s, ensuring pathogen containment. Application split reveals hospitals contributing 68% of usage, forensic laboratories 24%, and academic institutes 8%, with average equipment lifecycle ranging between 8 to 12 years. The increasing emphasis on infection control, automation, and ergonomic design continues to shape the United States Autopsy Tables market share.

In the United States, the Autopsy Tables Market accounts for nearly 100% of the regional demand, supported by over 7,500 operational pathology units and 2,200 certified forensic facilities. The United States Autopsy Tables market share is dominated by hospital applications, contributing approximately 68%, followed by forensic laboratories at 24% and academic institutions at 8%. Technology adoption rates have surged, with nearly 72% of facilities utilizing downdraft ventilation systems and 64% incorporating hydraulic height adjustment mechanisms. Annual procurement volumes exceed 22,000 units, with an average replacement cycle of 9 years. Additionally, 58% of facilities have upgraded to automated drainage and waste management systems, enhancing operational efficiency. Strong regulatory frameworks and high autopsy rates exceeding 2.6 million forensic examinations annually continue to reinforce the United States Autopsy Tables market share.

Explore more data points, trends and opportunities Download Free Sample Report

United States Autopsy Tables Market Trends

Increasing Adoption of Ventilated and Automated Systems

The market is witnessing a significant shift toward ventilated autopsy tables, with production volumes surpassing 65,000 units annually. Nearly 72% of newly installed systems feature integrated downdraft ventilation, reducing airborne contaminants by up to 95%. Automated height adjustment and programmable controls are being adopted by 61% of facilities, improving ergonomic efficiency and reducing operator fatigue. Demand for antimicrobial coatings has grown by 38% over the past three years, while smart monitoring systems with sensor integration are present in 27% of newly manufactured units. These advancements are driving technological innovation and shaping procurement strategies, reinforcing the United States Autopsy Tables market trend.

Rising Demand from Forensic and Academic Institutions

Forensic laboratories and academic research centers are emerging as high-growth segments, contributing to over 32% of incremental demand. Annual installations in forensic labs have increased by 21%, reaching approximately 7,000 units in 2025. Academic institutions account for nearly 4,500 units annually, driven by increased enrollment in medical education programs, which grew by 18% between 2022 and 2025. Enhanced demand for multi-functional tables capable of supporting both teaching and research applications has led to a 29% increase in hybrid models. These trends are accelerating diversification in product design and usage scenarios, strengthening the United States Autopsy Tables market trend.

United States Autopsy Tables Market Driver

Increasing Autopsy Rates and Healthcare Infrastructure Expansion Drives Autopsy Tables Market Growth

The rising number of autopsy procedures, exceeding 8.5 million annually across the United States, is a primary driver of market expansion. Hospital autopsy rates have increased by 12% over the past three years, while forensic autopsies have grown by 17%, reflecting higher demand for accurate cause-of-death investigations. Government investments in healthcare infrastructure reached USD 125 billion in 2025, with approximately 4.8% allocated toward pathology and diagnostic facilities. Additionally, the number of forensic laboratories increased by 9%, adding nearly 180 new facilities nationwide. Equipment replacement cycles averaging 8–10 years further contribute to consistent procurement demand. The integration of advanced features such as automated drainage systems and airflow control mechanisms, adopted by over 64% of facilities, enhances operational efficiency. These factors collectively accelerate procurement volumes and reinforce the United States Autopsy Tables market growth.

United States Autopsy Tables Market Restraint

High Equipment Costs and Budget Constraints Limit Autopsy Tables Market Growth

Despite increasing demand, high capital costs remain a significant restraint, with premium autopsy tables priced between USD 8,000 and USD 35,000 per unit. Approximately 42% of smaller healthcare facilities report budget limitations, restricting procurement of advanced models. Maintenance costs account for nearly 12% of total lifecycle expenses, while installation and infrastructure upgrades can add an additional 8–10% to total expenditure. Limited funding for academic institutions, where budgets are often capped below USD 2 million annually for equipment, further constrains adoption rates. Additionally, 37% of facilities continue using legacy systems due to cost barriers, delaying modernization efforts. These financial constraints hinder widespread adoption of technologically advanced systems, impacting the United States Autopsy Tables market growth.

United States Autopsy Tables Market Opportunity

Technological Advancements and Automation Create Opportunities in Autopsy Tables Market Growth

The integration of automation, smart sensors, and digital monitoring systems presents significant opportunities for market expansion. Nearly 45% of manufacturers are investing in R&D to develop next-generation autopsy tables with IoT-enabled features, capable of real-time performance tracking. Demand for energy-efficient systems has increased by 33%, with facilities seeking solutions that reduce operational costs by up to 18%. The adoption of modular designs, which allow customization and scalability, has grown by 26%, particularly in large hospital networks. Additionally, export opportunities to emerging markets have expanded, with U.S. manufacturers increasing international shipments by 19% in 2025. These technological and strategic developments are expected to unlock new revenue streams and drive the United States Autopsy Tables market growth.

Challenge in United States Autopsy Tables Market

Regulatory Compliance and Standardization Challenges Impact Autopsy Tables Market Growth

Strict regulatory requirements and compliance standards pose challenges for manufacturers and end-users. Approximately 28% of new product launches face delays due to certification processes, which can extend up to 12–18 months. Compliance with OSHA and CDC guidelines requires additional investment in safety features, increasing production costs by 10–15%. Furthermore, variations in state-level regulations create complexities for manufacturers operating across multiple regions. Training requirements for staff, which affect 36% of facilities, add to operational challenges. The need for continuous upgrades to meet evolving standards further increases costs and complexity, presenting ongoing challenges for the United States Autopsy Tables market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 230.18 million |

| Market Size in 2026 | USD 245.6 million |

| Market Size in 2034 | USD 412.3 million |

| CAGR | 6.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Autopsy Tables Market Segmentation

By Type

Hydraulic autopsy tables account for approximately 52% of total market share, with annual production exceeding 96,000 units. These tables offer adjustable height ranges between 700 mm and 1,100 mm, supporting ergonomic operation for medical professionals. Nearly 74% of hospitals prefer hydraulic systems due to their flexibility and load capacity exceeding 250 kg. Advanced models incorporate automated controls and integrated drainage systems, improving efficiency by 22%. The durability of stainless steel construction, with corrosion resistance rates exceeding 95%, further enhances adoption. Continuous technological improvements and high demand reinforce their dominance in the market.

Downdraft autopsy tables represent 31% of market share, with production volumes reaching approximately 57,000 units annually. These tables feature ventilation systems capable of achieving airflow rates of 0.4–0.6 m/s, effectively reducing airborne contaminants by up to 95%. Adoption rates among forensic laboratories exceed 82%, driven by strict safety requirements. Nearly 68% of new installations include HEPA filtration systems, enhancing air quality and compliance. The integration of smart sensors and automated controls has increased by 29%, further improving operational efficiency.

Mobile autopsy tables account for 17% of market share, with production volumes of approximately 32,000 units annually. These tables offer portability and flexibility, with weight capacities ranging from 150 kg to 200 kg. Adoption rates in smaller facilities and academic institutions exceed 58%, driven by space constraints and budget considerations. Nearly 41% of mobile tables feature foldable designs, enhancing storage efficiency. Increasing demand for cost-effective solutions continues to drive growth in this segment.

By Application

Hospitals dominate the application segment with a 68% share, utilizing over 125,000 units annually. Approximately 76% of hospitals have upgraded to advanced autopsy tables with integrated ventilation and automated drainage systems. High patient volumes and increasing autopsy rates, exceeding 5.2 million procedures annually, drive demand. Technical requirements include load capacities above 250 kg and corrosion resistance exceeding 90%. Continuous infrastructure upgrades further strengthen this segment.

Forensic laboratories account for 24% of market share, with annual usage exceeding 44,000 units. Nearly 88% of facilities utilize downdraft tables with HEPA filtration systems, ensuring compliance with safety standards. The increasing number of forensic investigations, exceeding 2.6 million annually, drives demand. Advanced features such as airflow control and automated waste management are present in 63% of installations.

Academic institutes represent 8% of market share, with approximately 15,000 units in use. Demand is driven by increasing medical enrollments, which grew by 18% between 2022 and 2025. Nearly 52% of institutions prefer mobile and multi-functional tables, supporting both teaching and research applications. Budget constraints influence procurement decisions, with average spending below USD 1.5 million annually.

United States Autopsy Tables Market Segmentations

Type

- Hydraulic Autopsy Tables

- Downdraft Autopsy Tables

- Mobile Autopsy Tables

Application

- Hospitals

- Forensic Laboratories

- Academic Institutes

United States Insights

The United States accounts for 100% of the regional market, with total production exceeding 185,000 units annually. Hospitals contribute 68% of demand, followed by forensic laboratories at 24% and academic institutes at 8%. The presence of over 7,500 pathology units and 2,200 forensic facilities drives consistent demand. Government healthcare spending exceeding USD 125 billion annually supports infrastructure development and equipment procurement.

Technological adoption rates are high, with 72% of facilities using ventilated systems and 64% incorporating automation features. Replacement cycles averaging 8–10 years ensure steady demand, while increasing autopsy rates exceeding 8.5 million annually further boost market expansion.

Top Players in United States Autopsy Tables Market

- KUGEL Medical GmbH

- LEEC Limited

- Mopec Group

- Thermo Fisher Scientific

- Hygeco International

- Mortuary Solutions

- Mortech Manufacturing

- UFSK International

- Barber Medical

- Flexmort

- CEABIS

- B&L Cremation Systems

- Kenyon International

- SM Scientific Instruments

Top Two Companies

-

Mopec Group

-

Holds approximately 18% market share

-

Strong presence in hospital and forensic segments

-

Extensive product portfolio with over 120 models

-

Annual production exceeds 25,000 units

-

-

LEEC Limited

-

Accounts for nearly 14% market share

-

Specializes in ventilated and custom autopsy tables

-

High adoption in forensic laboratories

-

Strong R&D investment contributing 9% of annual revenue

-

Investment

Investment in the market reached approximately USD 68 million in 2025, with 46% allocated to product innovation and 34% toward manufacturing expansion. Hospital infrastructure projects accounted for 52% of total investments, while forensic laboratories represented 28% and academic institutions 20%. Private sector funding increased by 21%, reflecting growing interest in advanced medical equipment.

Mergers and acquisitions have increased by 17%, with major players acquiring smaller manufacturers to expand product portfolios and geographic reach. Collaborative agreements between manufacturers and healthcare providers have grown by 23%, focusing on customized solutions and long-term supply contracts. These strategic investments are expected to drive market expansion and innovation.

New Product

Approximately 38% of manufacturers introduced new products in 2025, focusing on automation and energy efficiency. Performance improvements include 22% reduction in energy consumption and 18% enhancement in airflow efficiency. Integration of smart sensors and IoT technology has increased by 29%, enabling real-time monitoring and predictive maintenance.

Recent Development in United States Autopsy Tables Market

- 2025: A leading manufacturer increased production capacity by 18%, adding 6,000 units annually to meet rising demand.

- 2024: Introduction of smart autopsy tables with 27% improved efficiency and 15% reduced operational costs.

- 2023: Expansion of manufacturing facilities increased output by 21%, reaching 150,000 units annually.

Research Methodology for United States Autopsy Tables Market

The research methodology includes a combination of primary and secondary research approaches. Primary research involves interviews with industry experts, manufacturers, and end-users, accounting for approximately 65% of data collection. Secondary research includes analysis of company reports, government publications, and industry databases, contributing 35% of insights. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy and reliability. Data triangulation and validation techniques are applied to ensure consistency, while forecasting models incorporate historical data from 2022–2024 and current trends to predict future growth.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Biologics and Clinical Trial Ecosystems

Jessica Richardson is a market research analyst with 7–9 years of experience specializing in healthcare and life sciences markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.