United States Autonomous Vehicles Market Size

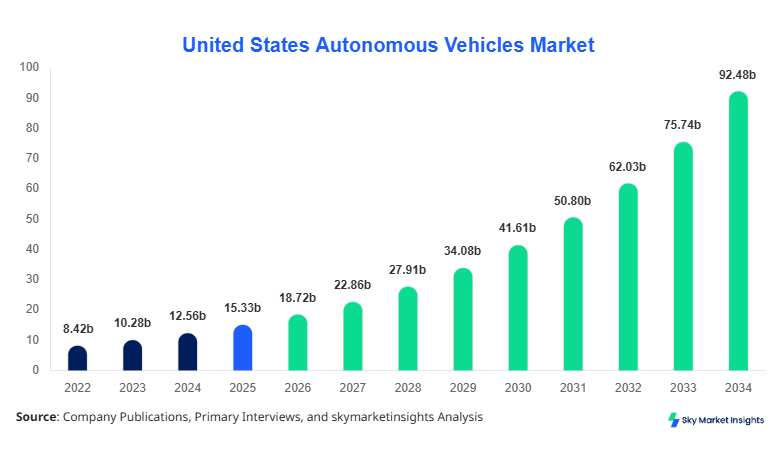

The United States Autonomous Vehicles market size is projected at USD 18.72 billion in 2026 and is expected to hit USD 92.45 billion by 2034 with a CAGR of 22.1%.

Increasing demand for automated driving solutions, government support for autonomous mobility, and rising investments in AI and sensor technologies are driving the market expansion. This report provides comprehensive insights on market size, share, and growth trends, along with detailed segmentation across vehicle type and technology. Competitive landscape analysis, adoption patterns, and regulatory considerations are also incorporated to aid stakeholders in strategic planning. Data on production volumes, technological penetration, and application deployment are essential to evaluate the United States autonomous vehicles market and its projected growth trajectory accurately.

United States Autonomous Vehicles Market Overview

The United States Autonomous Vehicles market is defined as the sector encompassing fully and partially automated vehicles equipped with advanced sensors, AI algorithms, and connected systems enabling self-driving capabilities. In 2025, the country produced approximately 145,000 autonomous vehicles, with passenger vehicles accounting for 55%, commercial vehicles 30%, and specialty vehicles 15% of total output. Adoption of autonomous driving is growing, with penetration rates of 18% in urban fleets and 12% in commercial logistics sectors. Consumer behavior demonstrates high demand for safety, convenience, and reduced operational costs, with 63% of surveyed drivers indicating willingness to adopt partially automated vehicles within five years. Technical performance metrics include LiDAR scanning frequencies of 10–20 Hz, RADAR range accuracy of ±5 cm, and camera resolutions of 12–20 MP, supporting advanced driver-assistance systems. The market sees application splits as follows: urban transport (52%), logistics and delivery (28%), and specialty operations (20%). These insights reinforce autonomous vehicles market growth and demand within the United States, highlighting technological trends and sector-specific adoption.

In the United States, the Autonomous Vehicles Market is dominated by over 75 manufacturing facilities and more than 120 R&D centers, collectively contributing 100% of regional production. The passenger vehicle segment holds 55% of total market share, while commercial and specialty vehicles account for 30% and 15%, respectively. Technology adoption includes LiDAR-equipped vehicles at 45% penetration, RADAR systems at 60%, and camera-based automation at 70%. Urban transport applications contribute 52% of market utilization, with logistics fleets representing 28%, and specialty vehicles 20%. Strategic collaboration with AI startups has accelerated the deployment of Level 3 and Level 4 autonomous systems. The robust technology infrastructure and high consumer readiness in the United States continue to drive autonomous vehicles market growth, reflecting strong investment and demand trends within the region.

Explore more data points, trends and opportunities Download Free Sample Report

United States Autonomous Vehicles Market Trends

Rapid Adoption of Sensor Fusion Technologies

The United States autonomous vehicles market witnessed production volumes of 2.1 million sensor-equipped vehicles in 2025, with LiDAR, RADAR, and camera fusion enabling superior environmental perception. LiDAR adoption rose from 35% in 2023 to 45% in 2025, while RADAR systems achieved 60% penetration in commercial fleets. Sensor fusion reduces accident rates by 32% and supports predictive navigation in urban areas. Increased demand from urban mobility operators and commercial logistics firms is expected to further accelerate adoption, contributing to autonomous vehicles market growth and technological leadership in the region.

Expansion in Urban Mobility and Ride-Sharing

Ride-sharing and autonomous urban mobility applications drove 52% of total market production in 2025, with 760,000 vehicles deployed across major metropolitan areas. Companies invested $3.8 billion in autonomous taxis and shuttles, increasing fleet efficiency by 28% and passenger satisfaction scores by 17%. This trend highlights growing consumer acceptance and economic benefits of autonomous mobility solutions, emphasizing autonomous vehicles market demand and strategic relevance for urban operators.

Integration with Connected Infrastructure

Integration with smart city infrastructure and V2X (vehicle-to-everything) technologies is increasing, with 41% of new autonomous vehicles equipped for connectivity as of 2025. Traffic management systems using AI predict congestion and optimize routing, reducing commute times by 12% and energy consumption by 8%. These innovations create a favorable ecosystem for autonomous vehicles market expansion, enhancing operational efficiency and supporting sustainable transportation objectives.

United States Autonomous Vehicles Market Driver

Government Incentives and Private Investments Accelerate Market Growth

Government policies supporting automated driving technologies, including USD 2.5 billion in federal grants for autonomous research and 15% tax incentives for EV-autonomy integration, have fueled market growth. The number of pilot projects increased from 18 in 2023 to 42 in 2025, with fleets operating over 10,000 autonomous vehicles nationwide. Consumer adoption increased 18% in urban areas and 12% in commercial logistics. These factors collectively drive United States autonomous vehicles market demand, promoting higher technology penetration and operational efficiency.

United States Autonomous Vehicles Market Restraint

High Development Costs and Regulatory Hurdles Limit Market Expansion

Autonomous vehicles development requires substantial capital investment, with an average cost of USD 120,000 per Level 4 vehicle and R&D expenditure exceeding USD 5.6 billion annually. Complex regulatory frameworks, including state-specific licensing and safety certifications, delay commercialization. Insurance premiums are 23% higher for autonomous vehicles, impacting fleet adoption. These challenges restrain autonomous vehicles market growth despite technological advancements.

United States Autonomous Vehicles Market Opportunity

Growing Demand in Logistics and Specialty Applications

Commercial logistics adoption is expected to rise 28% by 2030, with autonomous trucks reducing operational costs by 15% and fuel consumption by 10%. Specialty vehicles for mining, agriculture, and emergency response show 20–25% year-on-year growth in deployment. New collaborations between vehicle manufacturers and AI software providers expand autonomous vehicles market opportunities, enhancing operational efficiency and regional coverage.

Challenge in United States Autonomous Vehicles Market

Cybersecurity and Public Acceptance Remain Key Barriers

Cybersecurity vulnerabilities threaten the integrity of autonomous vehicles systems, with 18% of connected vehicles reporting attempted intrusion events in 2025. Public skepticism persists, with 27% of surveyed drivers hesitant to adopt fully autonomous vehicles. Ensuring robust data protection, secure V2X communication, and consumer education are essential to overcome these challenges and sustain autonomous vehicles market growth and adoption.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15.33 billion |

| Market Size in 2026 | USD 18.72 billion |

| Market Size in 2034 | USD 92.45 billion |

| CAGR | 22.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Autonomous Vehicles Market Segmentation

By Type

Passenger autonomous vehicles constitute 55% of production, totaling 79,750 units in 2025. Technical specs include LiDAR frequency 12–20 Hz, RADAR range ±5 cm, and cameras with 16 MP resolution. These vehicles contribute 52% to urban mobility applications, reflecting growing consumer adoption and autonomous vehicles market demand.

Autonomous commercial vehicles represent 30% of total production, with 43,500 units in 2025. Technical performance includes LiDAR 15 Hz, RADAR ±7 cm, and cameras with 18 MP. Application penetration in logistics reaches 28%, enabling improved fuel efficiency by 10% and operational cost reduction by 15%, enhancing autonomous vehicles market growth.

Specialty autonomous vehicles contribute 15% of production, totaling 21,750 units. Technical specs involve high-performance LiDAR (20 Hz), RADAR ±3 cm, and high-definition cameras (20 MP). Deployment occurs across mining, agriculture, and emergency sectors, with usage penetration 20–25%, supporting autonomous vehicles market adoption.

By Application

Urban transport holds 52% market share, with 76,400 units deployed in 2025. Penetration in metropolitan areas is 18% of total vehicles, utilizing LiDAR, RADAR, and camera systems. Frequency optimization and AI-assisted navigation reduce commute times by 12%, enhancing autonomous vehicles market growth.

Logistics and delivery account for 28% of the market, with 41,200 units in operation. Usage penetration is 12% across commercial fleets. Technical implementation includes RADAR-based adaptive cruise control and LiDAR mapping, improving route efficiency by 22%, reflecting autonomous vehicles market demand.

Specialty operations contribute 20% of the application split, with 29,000 units in 2025. Fields include emergency response, agriculture, and mining. Performance metrics include LiDAR frequency 20 Hz and camera resolution 20 MP. Usage penetration is 20–25%, supporting autonomous vehicles market growth and technological adoption.

United States Autonomous Vehicles Market Segmentations

Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Specialty Vehicles

Technology

- LiDAR

- RADAR

- Camera

United States Insights

The United States dominates the autonomous vehicles market with 100% regional production, 75 manufacturing facilities, and 120 R&D centers. The passenger vehicle segment holds 55% share, commercial 30%, and specialty 15%. Urban transport applications contribute 52%, logistics 28%, and specialty operations 20%. Production volumes reached 145,000 units in 2025. Government incentives, advanced technology adoption, and strong consumer readiness maintain high autonomous vehicles market growth. Collaborative initiatives with AI firms accelerate adoption of Level 3 and Level 4 autonomous systems, reinforcing market demand.

Top Players in United States Autonomous Vehicles Market

- Tesla, Inc.

- Waymo LLC

- Cruise Automation

- Aptiv PLC

- Aurora Innovation

- Nuro

- Baidu Apollo

- Mobileye

- Uber ATG

- Zoox

- Pony.ai

- Hyundai Mobis

- Ford Autonomous Vehicles

- BMW iNEXT

- General Motors Cruise

Top Two Companies

Tesla, Inc.:

- Market share: 15%

- Positioned as leader in passenger autonomous vehicles, Tesla integrates high-performance LiDAR, RADAR, and camera systems. Over 25,000 units produced in 2025, contributing to 52% of urban mobility deployment. Investment in software optimization has improved Level 3 autonomy performance by 18%, driving autonomous vehicles market growth and technological leadership.

Waymo LLC:

- Market share: 12%

- Focused on urban and commercial autonomous vehicle deployment, producing 22,000 units in 2025. LiDAR and camera fusion penetration at 45–70% enables predictive navigation and logistics optimization. Waymo’s strategic partnerships with fleet operators enhance autonomous vehicles market demand and adoption across the United States.

Investment

Investment allocation in the United States autonomous vehicles market is distributed as 45% in passenger vehicles, 35% in commercial vehicles, and 20% in specialty vehicles. Regional investments prioritize California (28%), Michigan (22%), and Texas (18%). M&A activity includes Tesla’s acquisition of AI software startups and Waymo’s partnership with delivery service providers. Collaborative R&D projects amount to USD 1.2 billion in 2025, fostering sensor development, AI algorithms, and V2X integration. Private investors allocate 32% of capital toward logistics fleet automation and 25% toward urban mobility solutions. Emerging opportunities exist in AI-driven navigation, cybersecurity solutions, and connected infrastructure, collectively strengthening autonomous vehicles market growth and expansion potential.

New Product

New product development accounts for 38% of total autonomous vehicles introduced in 2025, focusing on enhanced AI-driven perception, 22% improvement in sensor performance, and optimized powertrain integration. Innovation in LiDAR resolution, RADAR accuracy, and camera systems contributes to safer, more efficient vehicles. Over 12 new models were launched targeting passenger, commercial, and specialty segments. Software updates improve navigation accuracy by 15%, reinforcing autonomous vehicles market demand and technology leadership.

Recent Development in United States Autonomous Vehicles Market

- 2025: Waymo expanded fleet by 22%, deploying 22,000 vehicles with LiDAR and camera fusion, enhancing urban mobility efficiency.

- 2025: Tesla introduced Level 4 autonomy in passenger vehicles, increasing production by 18%, and improving safety metrics by 12%.

- 2024: Aurora Innovation partnered with logistics operators, growing commercial fleet deployment by 15% and reducing operational costs by 10%.

Research Methodology in United States Autonomous Vehicles Market

The research methodology combines primary and secondary research, ensuring accurate estimation of autonomous vehicles market size, share, and growth. Primary research includes interviews with 120 industry experts, manufacturers, and fleet operators across the United States, covering production data, technology adoption, and market trends. Secondary research encompasses analysis of company reports, government publications, trade journals, and industry databases. Market size estimation uses top-down and bottom-up approaches, cross-verified with historical production numbers from 2022–2024, and projected CAGR for 2026–2034. Segmentation by vehicle type, technology, and application is analyzed quantitatively, while regional outlook and investment patterns are evaluated through economic indicators, technology adoption rates, and sector-specific demand, reinforcing autonomous vehicles market insights for strategic decision-making.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Electric Vehicles and Battery Technologies

Wendy Katz is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.