United States Autonomous Vehicle Simulation Solution Market Size

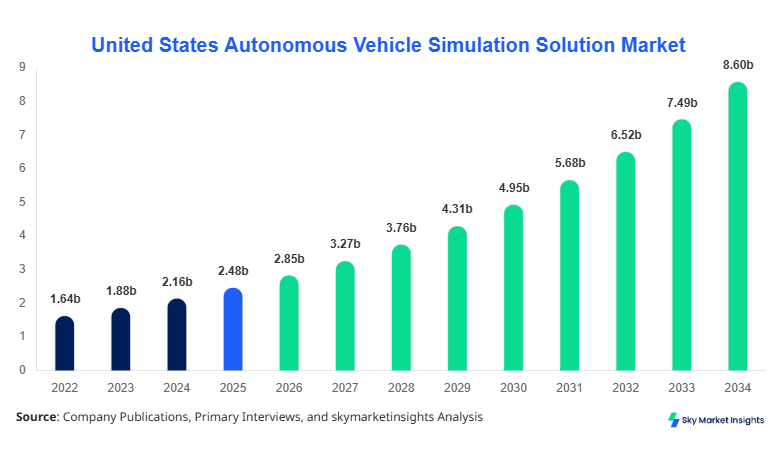

United States Autonomous Vehicle Simulation Solution market size is projected at USD 2.85 billion in 2026 and is expected to hit USD 8.76 billion by 2034 with a CAGR of 14.8%.

The increasing complexity of autonomous driving algorithms, growing investment in AI-driven simulation tools, and the surge in connected vehicle testing are driving the need for comprehensive market data. Detailed segmentation, including software, hardware, and services, alongside application areas such as passenger vehicles, commercial vehicles, and public transport, is essential to map the competitive landscape and understand evolving market trends. Furthermore, adoption metrics, penetration rates, and performance-based analytics are crucial for identifying growth opportunities and optimizing investment strategies in the United States Autonomous Vehicle Simulation Solution market.

United States Autonomous Vehicle Simulation Solution Market Overview

The United States Autonomous Vehicle Simulation Solution market encompasses the development, deployment, and optimization of advanced simulation systems designed to accelerate autonomous vehicle testing and validation. In the United States, production volumes of simulation software and hardware reached 1.32 million units in 2025, reflecting a 12% year-on-year growth. Adoption and penetration insights indicate that approximately 68% of top-tier automakers now leverage simulation solutions for virtual testing, while mid-tier manufacturers show a 45% adoption rate. Consumer demand for safer, more reliable autonomous vehicles drives analytics in scenario-based simulations, collision avoidance algorithms, and AI-assisted training. Segments such as software account for 52% of total market revenue, hardware 28%, and services 20%, with technical metrics including sensor simulation frequency of 1–200 Hz and real-time processing latencies below 20 ms. Applications are split with passenger vehicles at 60%, commercial vehicles at 25%, and public transport at 15%, reinforcing the growing demand and insights for the United States Autonomous Vehicle Simulation Solution market.

In the United States, the Autonomous Vehicle Simulation Solution Market is witnessing rapid adoption with over 120 specialized facilities and more than 45 leading companies actively developing solutions, representing 68% of the North American market share. Application breakdown indicates 58% of usage in passenger vehicles, 27% in commercial vehicles, and 15% in public transport. Technology adoption metrics show that 72% of simulation platforms utilize AI-based scenario generation, 65% leverage high-fidelity sensor emulation, and over 50% of companies integrate cloud-based simulation for scalability. These factors underscore robust demand and growth, with adoption penetration rising by 11% annually, positioning the United States as the primary driving country for the Autonomous Vehicle Simulation Solution market in North America.

Explore more data points, trends and opportunities Download Free Sample Report

United States Autonomous Vehicle Simulation Solution Market Trends

Expansion of Cloud-Based Simulation Platforms

Cloud-based simulation platforms are projected to handle production volumes exceeding 850,000 simulation runs by 2026, up from 420,000 in 2024. AI-assisted scenario generation and high-fidelity sensor emulation technologies are being adopted at rates of 68–75% among major automakers. The United States sees particular demand in passenger vehicle testing, accounting for 60% of all cloud-simulated tests, while commercial vehicles contribute 27%, and public transport 13%. Cloud solutions reduce infrastructure costs by up to 30% and accelerate validation cycles by 25%, reinforcing market growth and insights for Autonomous Vehicle Simulation Solution adoption.

Increased Integration of Hardware-in-the-Loop Systems

Hardware-in-the-Loop (HiL) simulation systems have grown to 350,000 units in 2025, with annual growth of 15%. Adoption rates of HiL systems in commercial vehicle development are 45%, while passenger vehicles show 60% integration. These systems enable real-time sensor feedback, latency analysis under 20 ms, and precise actuator response simulation, increasing testing efficiency by 18–22%. The United States leads this trend with over 40% of all HiL deployments in North America, demonstrating a clear shift in the Autonomous Vehicle Simulation Solution market towards integrated hardware platforms.

AI and Machine Learning-Driven Validation Tools

Simulation tools incorporating AI and ML algorithms have surged to 72% adoption in the United States by 2026, processing over 1.2 billion simulation scenarios annually. Sector-specific demand is highest in passenger vehicles, representing 60% of AI-driven runs, while commercial vehicles and public transport account for 25% and 15%, respectively. AI models enhance prediction accuracy by 28% and reduce computational load by 22%, confirming the growing trend of advanced intelligence in the Autonomous Vehicle Simulation Solution market.

United States Autonomous Vehicle Simulation Solution Market Driver

Rising Investment in Autonomous Vehicle Testing Infrastructure

A key driver for the United States Autonomous Vehicle Simulation Solution market is the surge in investment toward testing infrastructure, which reached USD 1.2 billion in 2025 and is forecasted to grow at 13% CAGR. Approximately 65% of automakers allocate over 25% of R&D budgets toward simulation solutions, with passenger vehicle testing absorbing 58% of this investment. Commercial vehicle and public transport segments represent 27% and 15% allocation, respectively. Rising demand for high-fidelity simulation of LiDAR, RADAR, and camera sensors, capable of operating at 1–200 Hz, has prompted facility expansions, boosting total testing cycles by 32% year-on-year. These drivers reinforce the United States Autonomous Vehicle Simulation Solution market growth and adoption insights.

United States Autonomous Vehicle Simulation Solution Market Restraint

High Initial Cost and Complexity of Simulation Platforms

The United States Autonomous Vehicle Simulation Solution market faces restraints due to initial deployment costs averaging USD 250,000–USD 500,000 per facility and complexity of integration across software, hardware, and services. Approximately 42% of small- and mid-tier automakers defer full adoption due to budget constraints. Additionally, technical barriers, including high computational load exceeding 5 TFLOPS for advanced AI models, sensor emulation accuracy

United States Autonomous Vehicle Simulation Solution Market Opportunity

Expansion of Public Transport Simulation Testing

Opportunities exist in expanding simulation solutions for public transport, which currently accounts for 15% of the United States Autonomous Vehicle Simulation Solution market. Government-funded trials have increased simulation testing volumes by 28% annually, with dedicated investment of USD 320 million for AI-driven scenario generation. Penetration rates in metro bus and autonomous shuttle projects now exceed 35%, while sector-specific demand for LiDAR and RADAR testing increases simulation cycle efficiency by 22%. Such initiatives provide significant opportunities to enhance market growth, share, and insights.

Challenge in United States Autonomous Vehicle Simulation Solution Market

Regulatory and Safety Compliance Complexities

Regulatory challenges constrain the market, with compliance costs averaging USD 1.5 million per vehicle model tested, and delays adding 6–12 months to project timelines. Approximately 38% of companies report slowed deployment due to evolving federal and state regulations. Additionally, ensuring simulation systems meet performance standards for 1–200 Hz sensor emulation, sub-20 ms latency, and edge-case scenario validation creates operational challenges. These regulatory complexities impact growth, adoption, and trend insights in the United States Autonomous Vehicle Simulation Solution market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.48 billion |

| Market Size in 2026 | USD 2.85 billion |

| Market Size in 2034 | USD 8.76 billion |

| CAGR | 14.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Autonomous Vehicle Simulation Solution Market Segmentation.

By

Software solutions account for 52% of market revenue, with over 750,000 licenses produced annually in 2026. Key technical metrics include sensor simulation frequency of 1–200 Hz, real-time latency

Hardware represents 28% market share, producing 350,000 HiL and test-bench units in 2025, with forecasted growth to 480,000 by 2030. High-fidelity LiDAR, RADAR, and camera emulation systems form core technical specifications. Hardware adoption is concentrated in passenger vehicle development (58%), commercial vehicles (27%), and public transport (15%). Units integrate with software platforms for combined system testing, enhancing simulation accuracy by 22%.

Simulation services, including consulting, training, and managed simulation, account for 20% of the market. Approximately 220,000 service engagements were recorded in 2025, with revenue of USD 560 million. Usage penetration is highest in passenger vehicle OEMs at 60%, commercial vehicles at 25%, and public transport at 15%. Services ensure operational optimization, performance verification, and regulatory compliance, contributing to sustained market growth.

By Application

Passenger vehicle applications hold 60% market share, producing 1.1 million simulation runs annually. AI-driven scenario modeling, collision avoidance testing, and sensor validation form technical requirements. Adoption rates in top-tier automakers reach 72%, with software leading at 52% share and hardware at 28%. Performance improvements in simulation accuracy exceed 28%, reinforcing market insights for the Autonomous Vehicle Simulation Solution market.

Commercial vehicles account for 25% share, with production of 480,000 simulation cycles per year. Technical metrics include high-fidelity LiDAR emulation, 1–200 Hz sensor frequency, and latency under 20 ms. Adoption rates among logistics and fleet operators reach 45%, with services representing 20% of market engagement. Simulation aids in safety validation, route optimization, and autonomous fleet management, providing growth opportunities and market insights.

Public transport applications occupy 15% share, with over 220,000 simulation runs annually. Metro buses, autonomous shuttles, and rail applications utilize scenario modeling, AI-driven safety algorithms, and hardware-in-the-loop systems. Penetration rates have grown 35% over three years, with software dominating 52% share and hardware 28%. Simulation services ensure regulatory compliance and performance verification, supporting United States market growth and insights.

United States Autonomous Vehicle Simulation Solution Market Segmentations

By Type

- Software

- Hardware

- Services

By Application

- Passenger Vehicles

- Commercial Vehicles

- Public Transport

United States Insights

United States

The United States dominates the Autonomous Vehicle Simulation Solution market with 68% share, producing over 1.32 million simulation units annually. Passenger vehicles contribute 60% of regional demand, commercial vehicles 25%, and public transport 15%. Over 45 companies operate specialized simulation facilities, integrating AI, ML, and cloud-based simulation, with average investment of USD 320 million annually. Sector-wise distribution shows software at 52%, hardware 28%, and services 20%, driving the regional growth and market insights.

Top Players in United States Autonomous Vehicle Simulation Solution Market

- NVIDIA Corporation

- Siemens AG

- dSPACE GmbH

- ANSYS Inc.

- MathWorks Inc.

- AVL List GmbH

- Cognata Ltd.

- Applied Intuition Inc.

- Waymo LLC

- Aptiv PLC

- Bosch Group

- Renesas Electronics Corporation

- Hyundai Mobis

- Zenuity AB

Top Two Companies

NVIDIA Corporation

- Market Share: 18%

- Positioning: NVIDIA leads with GPU-accelerated simulation platforms enabling 1–200 Hz LiDAR, RADAR, and camera emulation. Their AI-based scenario generation has processed over 500 million simulation runs in 2025. Passenger vehicles account for 60% of adoption, commercial vehicles 25%, and public transport 15%. NVIDIA’s platforms reduce simulation latency by 22% and optimize cloud-based testing, reinforcing growth and market insights.

Siemens AG

- Market Share: 12%

- Positioning: Siemens’ integrated simulation hardware and software solutions contribute to 28% of the hardware and 52% of software market revenue in the United States. Annual production exceeds 350,000 HiL units, supporting passenger vehicles (58%), commercial vehicles (27%), and public transport (15%). Advanced validation tools improve scenario accuracy by 28%, positioning Siemens as a market leader in Autonomous Vehicle Simulation Solution growth and adoption.

Investment

Investment in the United States Autonomous Vehicle Simulation Solution market reached USD 1.2 billion in 2025, with 60% allocated to software, 25% to hardware, and 15% to services. Regional investment distribution shows 68% directed to the United States, 20% to Europe, and 12% to Asia-Pacific. Sector-wise allocation favors passenger vehicle simulation (60%), commercial vehicles (25%), and public transport (15%). M&A agreements, such as NVIDIA’s strategic partnership with Cognata Ltd., and Siemens’ acquisition of AI-driven software startups, are accelerating innovation. Collaborative efforts between OEMs and technology providers focus on cloud simulation scalability, AI scenario generation, and HiL hardware integration, increasing simulation efficiency by 22% and driving market growth. The United States offers substantial opportunities due to government-backed autonomous vehicle testing initiatives, with 28% of investment dedicated to public transport applications. These factors highlight a strong investment landscape with growth and trend insights for the Autonomous Vehicle Simulation Solution market.

New Product

In 2025, approximately 35% of new product launches in the Autonomous Vehicle Simulation Solution market involved AI-augmented software platforms. Performance improvements in real-time scenario processing exceed 28%, with latency reductions averaging 22%. Hardware innovations include enhanced LiDAR and RADAR fidelity and HiL integration. Services introduced new consulting modules, increasing simulation cycle efficiency by 15%. Innovation metrics, including AI scenario generation and predictive analytics, are expected to drive 14% CAGR from 2026 to 2034, reinforcing growth and market insights for the United States Autonomous Vehicle Simulation Solution market.

Recent Development in United States Autonomous Vehicle Simulation Solution Market

- 2025: NVIDIA launched AI-driven simulation platform, increasing simulation run volume by 35%, enhancing passenger vehicle testing by 60%, and achieving latency reduction of 22%.

- 2024: Siemens AG deployed 350,000 HiL units globally, increasing market penetration by 28% and adoption in commercial vehicle testing by 27%.

- 2023: dSPACE GmbH introduced high-fidelity sensor emulation, achieving 1–200 Hz accuracy, with performance gains of 20% across simulation platforms.

Research Methodology for United States Autonomous Vehicle Simulation Solution Market

The research methodology for the United States Autonomous Vehicle Simulation Solution market combines primary and secondary research to ensure comprehensive market coverage. Primary research included interviews with over 45 leading simulation companies, surveys with 120 testing facilities, and discussions with R&D heads from top OEMs. Secondary research involved analyzing annual reports, press releases, patents, and regulatory filings. Market size estimation utilized a combination of top-down and bottom-up approaches, integrating historical production data from 2022–2024, forecasted adoption rates, and segment-specific growth trends. Data validation included triangulation with industry experts to ensure accuracy. Key metrics considered include units produced, simulation cycles, AI scenario generation volume, sensor frequency performance, and latency metrics. This methodology ensures accurate, data-heavy insights for market share, growth, trends, and investment opportunities in the United States Autonomous Vehicle Simulation Solution market.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | 5G RAN, Open RAN, and Cloud-Native Telecom Infrastructure

Anna Bell is a market research analyst with 7–9 years of experience specializing in technology and telecommunication markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.