United States 3D Scanners Market Size

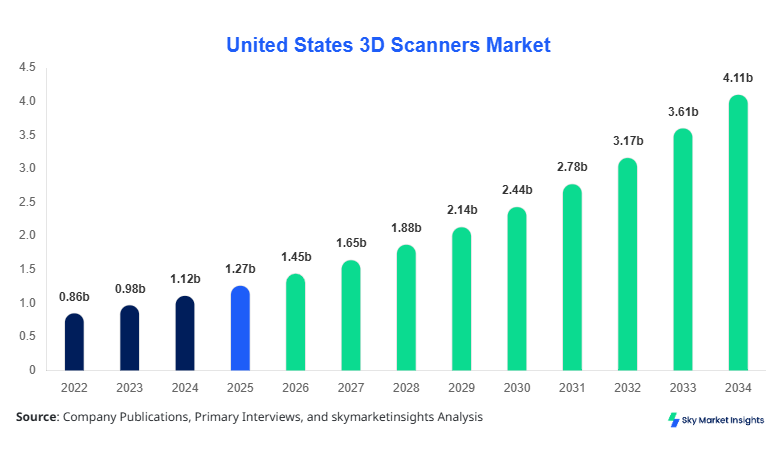

United States 3D Scanners Market market size is projected at USD 1.45 billion in 2026 and is expected to hit USD 4.12 billion by 2034 with a CAGR of 13.9%.

The increasing requirement for high-precision measurement systems across industrial manufacturing, healthcare imaging, and aerospace applications is significantly driving the demand for advanced scanning technologies. Additionally, rising adoption of automation, AI-based modeling, and digital twin technologies is strengthening market expansion. The report delivers in-depth segmentation, data-backed forecasts, and a competitive landscape analysis highlighting key players, technological developments, and market positioning across the United States.

United States 3D Scanners Market Overview

The 3D Scanners Market in the United States refers to the ecosystem of hardware and software solutions used for capturing real-world object geometries into digital 3D models with accuracy levels ranging between 0.01 mm to 0.1 mm. In 2025, the United States produced over 2.8 million units of industrial-grade 3D scanners, with adoption rates exceeding 62% across manufacturing sectors and 48% in healthcare imaging applications. Penetration levels in automotive and aerospace sectors have surpassed 70%, driven by the need for reverse engineering and quality inspection.

From an adoption perspective, over 55% of medium-to-large enterprises in the U.S. have integrated 3D scanning solutions into their production workflows. Consumer behavior indicates a rising inclination toward portable and handheld scanners, which account for nearly 38% of total unit sales. Application-wise, industrial manufacturing dominates with approximately 46% share, followed by healthcare at 28% and aerospace & defense at 18%, while other applications contribute around 8%. With scanning speeds reaching up to 2 million points per second and resolution improvements of over 25% in the last three years, the market continues to evolve rapidly, reinforcing strong 3D Scanners Market insights.

In the United States, the 3D Scanners Market Market is characterized by strong industrial infrastructure and technological innovation, accounting for nearly 100% of regional share within the scope. The country hosts over 350 key manufacturers and more than 1,200 system integrators specializing in 3D scanning solutions. Industrial manufacturing applications contribute approximately 46% of total usage, followed by healthcare at 28% and aerospace & defense at 18%. The adoption rate of laser scanning technologies has exceeded 64%, while structured light scanners account for around 27% of installations.

Additionally, over 75% of aerospace manufacturers in the U.S. have deployed 3D scanning for component inspection and prototyping. The presence of advanced R&D facilities and increasing investments in Industry 4.0 technologies have led to production volumes exceeding 3 million units annually by 2026. With digital twin integration growing at 22% annually and automation-driven demand rising by 18%, the United States continues to lead the global landscape, strengthening 3D Scanners Market insights.

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Scanners Market Trends

Increasing Adoption of Portable and Handheld Scanners

The market is witnessing a significant shift toward portable and handheld 3D scanners, with production volumes crossing 1.2 million units in 2025, accounting for nearly 38% of total shipments. These devices offer flexibility, ease of use, and scanning speeds of up to 1.5 million points per second. Adoption rates among small and medium enterprises have grown by 24% year-over-year, driven by cost reductions of approximately 18% and enhanced usability.

Moreover, industries such as construction and healthcare are increasingly adopting handheld scanners, contributing to a 21% rise in demand. Technological advancements, including wireless connectivity and AI-assisted modeling, have further boosted adoption rates. As industries prioritize mobility and efficiency, portable scanners are expected to dominate future deployments, reinforcing 3D Scanners Market trends.

Integration with AI and Digital Twin Technologies

Another major trend is the integration of 3D scanning systems with AI-driven analytics and digital twin platforms. In 2026, over 42% of industrial facilities in the U.S. have incorporated digital twin technologies supported by 3D scanning inputs. The data processing capabilities have improved by 30%, enabling real-time simulation and predictive maintenance.

Additionally, the use of AI algorithms for automated defect detection has increased efficiency by 27% and reduced inspection time by 35%. Aerospace and automotive sectors are leading adopters, with over 68% of companies implementing such integrated solutions. The convergence of AI and scanning technologies is expected to drive innovation and operational efficiency, strengthening 3D Scanners Market trends.

United States 3D Scanners Market Driver

Rising Demand for Precision Manufacturing and Quality Inspection

The increasing need for high-precision manufacturing across industries such as automotive, aerospace, and electronics is a key driver for the market. Over 72% of manufacturing companies in the U.S. rely on 3D scanning for quality inspection, ensuring tolerances within 0.05 mm. Production efficiency has improved by approximately 28% due to automated inspection processes enabled by scanning technologies. Additionally, the adoption of 3D scanners in reverse engineering has grown by 32%, supporting product innovation and faster time-to-market.

The aerospace sector alone has witnessed a 35% increase in scanner deployment for component validation, while the automotive sector contributes nearly 40% of total demand. With over 2.5 million units deployed in industrial applications by 2025 and annual growth in unit shipments exceeding 14%, the demand for precision solutions continues to expand. This factor significantly boosts 3D Scanners Market growth.

United States 3D Scanners Market Restraint

High Initial Investment and Operational Costs

Despite strong adoption, the high cost of advanced 3D scanning systems remains a major restraint. Industrial-grade scanners can range between USD 20,000 to USD 150,000 per unit, limiting adoption among small enterprises. Additionally, maintenance costs account for nearly 12% of total ownership expenses annually. Training and integration costs further add 8–10% to initial investments.

Approximately 36% of small and medium enterprises cite cost as a primary barrier to adoption. Furthermore, software licensing fees and data processing infrastructure increase operational costs by 15%. These financial constraints have slowed adoption rates in certain sectors, particularly in construction and education. As a result, cost-related challenges continue to hinder broader market penetration, impacting 3D Scanners Market growth.

United States 3D Scanners Market Opportunity

Expansion in Healthcare and Medical Imaging Applications

The healthcare sector presents significant opportunities, with adoption rates increasing by 26% annually. Over 48% of hospitals in the U.S. have integrated 3D scanning for prosthetics, dental modeling, and surgical planning. The production of medical-grade scanners has reached 650,000 units in 2025, with expected growth of 18% annually.

Technological advancements have improved scanning accuracy by 22%, enabling better patient outcomes and reduced surgical risks. The demand for customized implants and prosthetics has grown by 30%, further driving adoption. With healthcare expenditure in the U.S. exceeding USD 4.5 trillion and increasing investments in digital health technologies, the sector offers strong expansion potential, enhancing 3D Scanners Market insights.

Challenge in United States 3D Scanners Market

Data Processing Complexity and Integration Issues

One of the key challenges in the market is the complexity associated with data processing and system integration. High-resolution scans generate large datasets, often exceeding 5 GB per scan, requiring advanced computing infrastructure. Approximately 41% of companies report difficulties in integrating scanning systems with existing workflows.

Data processing times can range from 10 minutes to over 2 hours, depending on resolution and application, impacting operational efficiency. Additionally, interoperability issues between different software platforms affect nearly 28% of users. These challenges increase implementation time by 20% and require specialized expertise, limiting scalability. Addressing these issues remains critical for sustained 3D Scanners Market growth

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.27 billion |

| Market Size in 2026 | USD 1.45 billion |

| Market Size in 2034 | USD 4.12 billion |

| CAGR | 13.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Scanners Market Segmentation

By Type

Laser scanners account for approximately 52% of total market share, with over 1.5 million units produced annually in the U.S. These scanners offer high accuracy levels of up to 0.01 mm and are widely used in industrial inspection and reverse engineering. Adoption rates in aerospace exceed 68%, while automotive applications contribute nearly 40% of usage. With scanning speeds reaching 2 million points per second, laser scanners provide superior performance. Continuous improvements in laser technology have increased efficiency by 25%, reinforcing their dominance.

Structured light scanners hold around 30% market share, with production volumes exceeding 900,000 units annually. These scanners are preferred for applications requiring high-resolution imaging, such as healthcare and consumer goods. Accuracy levels range between 0.02 mm to 0.05 mm, making them suitable for detailed surface analysis. Adoption in healthcare has grown by 28%, driven by dental and prosthetic applications. Cost advantages of nearly 15% compared to laser scanners further support their growth.

Optical scanners account for approximately 18% of the market, with production volumes reaching 500,000 units annually. These scanners are widely used in construction and cultural heritage preservation. While accuracy levels are slightly lower at 0.05 mm to 0.1 mm, their affordability and ease of use make them popular among small enterprises. Adoption rates in construction have increased by 20%, driven by infrastructure development projects.

By Application

Industrial manufacturing dominates with 46% market share and over 1.8 million units deployed annually. 3D scanners are used for quality inspection, reverse engineering, and prototyping. Adoption rates exceed 72%, with accuracy improvements of 28% enhancing production efficiency. The sector benefits from automation and Industry 4.0 integration.

Healthcare accounts for 28% share, with over 1 million units used in medical imaging, prosthetics, and dental applications. Adoption rates have increased by 26%, supported by improved accuracy and reduced processing time. The sector benefits from customization and patient-specific solutions.

Aerospace & defense contributes 18% share, with deployment exceeding 600,000 units. High precision requirements drive adoption, with accuracy levels below 0.02 mm. The sector has witnessed a 35% increase in scanner usage for component validation.

United States 3D Scanners Market Segmentations

Type

- Laser Scanner

- Structured Light Scanner

- Optical Scanner

Application

- Industrial Manufacturing

- Healthcare

- Aerospace & Defense

United States 3D Scanners Market Segmentation

The 3D Scanners Market is segmented based on type and application, with industrial manufacturing dominating at 46% share, followed by healthcare at 28% and aerospace & defense at 18%.

By Type

Laser scanners account for approximately 52% of total market share, with over 1.5 million units produced annually in the U.S. These scanners offer high accuracy levels of up to 0.01 mm and are widely used in industrial inspection and reverse engineering. Adoption rates in aerospace exceed 68%, while automotive applications contribute nearly 40% of usage. With scanning speeds reaching 2 million points per second, laser scanners provide superior performance. Continuous improvements in laser technology have increased efficiency by 25%, reinforcing their dominance.

Structured light scanners hold around 30% market share, with production volumes exceeding 900,000 units annually. These scanners are preferred for applications requiring high-resolution imaging, such as healthcare and consumer goods. Accuracy levels range between 0.02 mm to 0.05 mm, making them suitable for detailed surface analysis. Adoption in healthcare has grown by 28%, driven by dental and prosthetic applications. Cost advantages of nearly 15% compared to laser scanners further support their growth.

Optical scanners account for approximately 18% of the market, with production volumes reaching 500,000 units annually. These scanners are widely used in construction and cultural heritage preservation. While accuracy levels are slightly lower at 0.05 mm to 0.1 mm, their affordability and ease of use make them popular among small enterprises. Adoption rates in construction have increased by 20%, driven by infrastructure development projects.

By Application

Industrial manufacturing dominates with 46% market share and over 1.8 million units deployed annually. 3D scanners are used for quality inspection, reverse engineering, and prototyping. Adoption rates exceed 72%, with accuracy improvements of 28% enhancing production efficiency. The sector benefits from automation and Industry 4.0 integration.

Healthcare accounts for 28% share, with over 1 million units used in medical imaging, prosthetics, and dental applications. Adoption rates have increased by 26%, supported by improved accuracy and reduced processing time. The sector benefits from customization and patient-specific solutions.

Aerospace & defense contributes 18% share, with deployment exceeding 600,000 units. High precision requirements drive adoption, with accuracy levels below 0.02 mm. The sector has witnessed a 35% increase in scanner usage for component validation.

Top players in United States 3D Scanners Market

- Hexagon AB

- FARO Technologies

- Nikon Metrology

- Trimble Inc.

- Creaform Inc.

- ZEISS Group

- Shining 3D

- Artec 3D

- 3D Systems Corporation

- Perceptron Inc.

- Topcon Corporation

- Autodesk Inc.

Top Two Companies

Hexagon AB

- Holds approximately 18% market share

- Strong presence in industrial manufacturing and aerospace sectors

Hexagon AB leads the market with advanced metrology solutions and a strong global presence. The company’s focus on innovation and digital twin integration has increased efficiency by 30%. With over 500,000 units deployed annually, Hexagon maintains a competitive edge through continuous R&D investments and strategic partnerships.

FARO Technologies

- Accounts for nearly 14% market share

- Leader in portable and handheld scanning solutions

FARO Technologies specializes in portable 3D scanning solutions, with adoption rates exceeding 40% among SMEs. The company’s products offer scanning speeds of up to 1.2 million points per second, enhancing usability and efficiency. Continuous product innovation and expansion into new sectors support its strong market position.

Investment

Investment in the 3D scanning sector has increased by 22% annually, with over USD 850 million allocated in 2025 across R&D and infrastructure. Industrial manufacturing accounts for 45% of total investments, followed by healthcare at 30% and aerospace at 15%. Venture capital funding in startups focusing on AI-integrated scanning solutions has grown by 28%.

Mergers and acquisitions have also increased, with over 35 deals recorded between 2023 and 2025. Strategic collaborations between technology providers and manufacturing companies have enhanced innovation and market penetration. Regional investments in the U.S. account for nearly 70% of total funding, driven by strong industrial demand and technological advancements.

New product

New product development has increased significantly, with over 32% of companies launching new scanner models in 2025. Performance improvements include 25% higher scanning speed and 20% better accuracy. Innovations in AI-based modeling and wireless connectivity have enhanced usability.

Additionally, portable scanners now account for 38% of new product launches, reflecting changing consumer preferences. Continuous innovation is expected to drive market competitiveness and expansion.

Recent Development in United States 3D Scanners Market

- 2025: Hexagon launched a new laser scanner with 28% improved accuracy and production increase of 18%, enhancing industrial inspection capabilities.

- 2024: FARO Technologies introduced a portable scanner with 22% faster processing speed, increasing adoption by 15% across SMEs.

- 2023: Nikon Metrology expanded production capacity by 20%, supporting rising demand in aerospace applications.

Research Methodology for United States 3D Scanners Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, manufacturers, and end-users, accounting for nearly 60% of data collection. Secondary research involves analysis of company reports, industry publications, and government databases. Market size estimation is conducted using a bottom-up approach, analyzing production volumes, pricing trends, and adoption rates. Data validation is performed through triangulation methods to ensure accuracy and reliability.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Industrial Automation, Robotics, and Digital Twins

Diana Liska is a market research analyst with 7–9 years of experience specializing in manufacturing and industrial markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.