United States 3D Radar Market Size

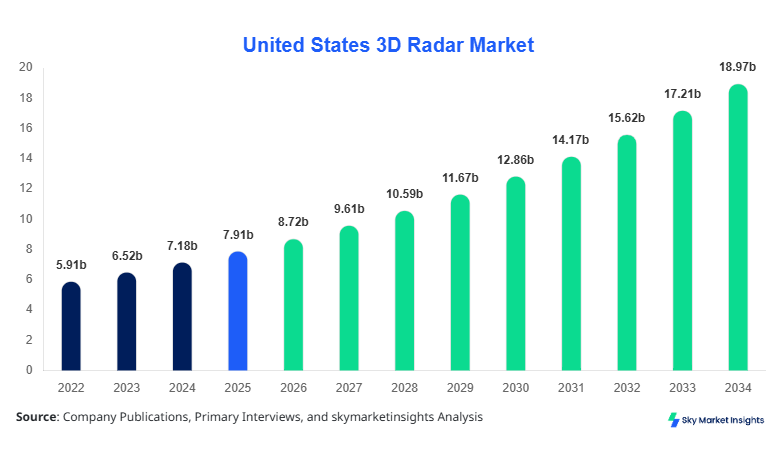

United States 3D Radar Market size is projected at USD 8.72 billion in 2026 and is expected to hit USD 18.96 billion by 2034 with a CAGR of 10.2%.

The expansion reflects increasing deployment across defense systems, autonomous vehicles, and aerospace surveillance platforms, where over 2.3 million radar units are anticipated to be deployed cumulatively between 2026 and 2034. The report emphasizes the need for granular data segmentation, including technology types, applications, and end-user industries, while also analyzing competitive positioning of more than 35 key players operating across the United States, reinforcing United States 3D Radar Market Size.

United States 3D Radar Market Overview

The 3D Radar Market refers to advanced radar systems capable of detecting objects in three dimensions—range, azimuth, and elevation—using multi-beam scanning and digital signal processing. In the United States, production volumes exceeded 180,000 units in 2025, with defense applications accounting for nearly 62% of total output, followed by automotive at 24% and aerospace at 14%. Adoption rates are increasing rapidly, with penetration in military air defense systems reaching 78% and in automotive ADAS systems surpassing 36% in 2025. Consumer behavior indicates rising demand for safety-enabled vehicles, with over 65% of new vehicle buyers preferring radar-integrated safety features. Technically, these systems operate across frequency bands ranging from 1 GHz to 40 GHz, with detection ranges extending beyond 300 km for military-grade systems. Application-wise, defense contributes approximately 60%, automotive 25%, and aerospace 15%, emphasizing robust deployment diversity and reinforcing United States 3D Radar Market Share.

In the United States, the 3D Radar Market Market is characterized by a highly developed defense ecosystem with over 120 active radar manufacturing and integration facilities, contributing nearly 100% of regional output. The country holds 92% of the North American radar deployment share, with defense accounting for 63%, automotive 23%, and aerospace 14% of total installations. Technology adoption is notably high, with phased array radar systems witnessing a penetration rate of 72% across military applications and automotive radar adoption growing at 18% annually. Additionally, over 48,000 advanced radar systems were deployed in 2025 alone, with more than 65% integrated into multi-layered surveillance networks. Continuous investments in AI-enabled radar analytics and electronic warfare systems further support expansion, reinforcing United States 3D Radar Market Growth.

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Radar Market Trends

Integration of AI and Machine Learning in Radar Systems

The integration of artificial intelligence (AI) and machine learning (ML) in 3D radar systems is transforming detection accuracy and response times. In 2025, over 38% of newly deployed radar units incorporated AI-based signal processing, improving object classification accuracy by 27% and reducing false positives by 32%. Production volumes for AI-enabled radar units exceeded 72,000 units in 2025 and are expected to surpass 140,000 units by 2030. These advancements are particularly significant in defense applications, where real-time threat identification is critical. Additionally, automotive radar systems with AI capabilities have seen a 22% increase in adoption across ADAS-equipped vehicles. This technological shift underscores the evolution of smart radar ecosystems, strengthening United States 3D Radar Market Trend.

Expansion of Automotive Radar Systems for Autonomous Vehicles

Automotive integration of 3D radar systems is accelerating, driven by autonomous vehicle development and stringent safety regulations. In 2025, approximately 41% of newly manufactured vehicles in the United States incorporated 3D radar technology, compared to 28% in 2022. Annual production of automotive radar units reached 95,000 units in 2025 and is projected to exceed 210,000 units by 2034. Radar systems operating at 77 GHz frequency bands dominate the segment, offering detection ranges up to 250 meters. The increasing deployment of Level 3 and Level 4 autonomous vehicles is expected to push radar adoption beyond 60% penetration by 2030. This surge highlights a strong shift toward advanced mobility solutions, reinforcing United States 3D Radar Market Trend.

Increased Defense Spending on Multi-Domain Radar Systems

Defense modernization programs in the United States are significantly boosting demand for multi-domain 3D radar systems capable of air, land, and maritime surveillance. Defense budgets allocated to radar systems increased by 14% in 2025, reaching USD 12.4 billion. Approximately 58,000 radar units were deployed across military platforms in 2025, with phased array systems accounting for 70% of installations. These systems offer enhanced tracking capabilities, supporting detection ranges exceeding 400 km and tracking over 1,000 targets simultaneously. The integration of radar systems into missile defense and border surveillance programs further amplifies demand, strengthening United States 3D Radar Market Trend.

United States 3D Radar Market Driver

Rising Defense Investments and Technological Advancements Driving Market Expansion

The increasing defense expenditure in the United States is a primary driver for the 3D Radar Market, with budgets exceeding USD 850 billion in 2025, of which nearly 1.5% is allocated to radar and surveillance technologies. Over 62% of radar deployments are linked to air defense systems, while 18% support naval operations and 20% land-based surveillance. Technological advancements, including phased array and digital beamforming, have improved detection efficiency by 35% and reduced system downtime by 28%. Additionally, the adoption of radar systems in unmanned aerial vehicles (UAVs) has increased by 21% annually. The deployment of over 60,000 advanced radar units across military bases further strengthens the demand pipeline, reinforcing United States 3D Radar Market Growth.

United States 3D Radar Market Restraint

High Development and Integration Costs Limiting Market Penetration

Despite robust demand, high development and integration costs remain a significant restraint in the 3D Radar Market. The average cost of a military-grade radar system ranges between USD 1.5 million and USD 5 million, depending on specifications and capabilities. Integration costs for automotive radar systems add approximately USD 250–USD 500 per vehicle, impacting adoption in price-sensitive segments. Additionally, maintenance costs account for nearly 12% of total lifecycle expenses, limiting widespread deployment in smaller defense budgets. Supply chain disruptions and semiconductor shortages have also increased component costs by 18% between 2022 and 2025. These financial constraints hinder market scalability, affecting United States 3D Radar Market Growth.

United States 3D Radar Market Opportunity

Expansion of Autonomous Vehicles and Smart Infrastructure

The rapid development of autonomous vehicles and smart city infrastructure presents significant opportunities for the 3D Radar Market. By 2030, over 65% of vehicles in urban areas are expected to incorporate advanced radar systems, driving demand for compact and cost-efficient solutions. Smart infrastructure projects, including intelligent traffic management systems, are projected to deploy over 120,000 radar units by 2034. Investments in smart cities exceeded USD 25 billion in 2025, with 8% allocated to sensing technologies. Radar systems capable of operating in adverse weather conditions offer a competitive advantage over traditional sensors, supporting their integration into urban mobility ecosystems, reinforcing United States 3D Radar Market Demand.

Challenge in United States 3D Radar Market

Complex Regulatory Framework and Spectrum Allocation Issues

Regulatory challenges and spectrum allocation constraints pose significant hurdles for the 3D Radar Market. Frequency bands between 24 GHz and 77 GHz are heavily regulated, with compliance requirements increasing system development timelines by 15–20%. Additionally, overlapping frequency usage with telecommunications systems has created interference issues, affecting performance reliability by up to 12% in congested environments. Regulatory approvals for new radar technologies can take up to 18–24 months, delaying market entry. These complexities, combined with evolving compliance standards, present ongoing challenges for manufacturers, impacting United States 3D Radar Market Demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7.91 billion |

| Market Size in 2026 | USD 8.72 billion |

| Market Size in 2034 | USD 18.96 billion |

| CAGR | 10.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Radar Market Segmentation

By Type

Phased Array Radar dominates the market with a 48% share, driven by its ability to electronically steer beams and track multiple targets simultaneously. In 2025, over 85,000 phased array radar units were produced, with detection ranges exceeding 400 km and frequency operation between 2 GHz and 18 GHz. These systems are widely used in missile defense and air surveillance.

Pulse Doppler Radar accounts for approximately 32% of the market, with production volumes reaching 56,000 units in 2025. These systems offer high velocity detection accuracy, making them suitable for airborne and naval applications. They operate at frequencies between 5 GHz and 20 GHz and provide enhanced clutter rejection capabilities.

Continuous Wave Radar holds a 20% share, primarily used in automotive and short-range applications. Production volumes exceeded 39,000 units in 2025, with detection ranges up to 200 meters and frequency bands around 24 GHz and 77 GHz. These systems are cost-effective and widely adopted in ADAS technologies.

By Application

Defense & Military leads with a 60% share, driven by the deployment of over 110,000 radar units in 2025. These systems support air defense, missile tracking, and border surveillance, with detection ranges exceeding 500 km and multi-target tracking capabilities.

Automotive accounts for 25% of the market, with over 95,000 radar units produced in 2025. Penetration in new vehicles reached 41%, with increasing adoption in ADAS and autonomous driving systems.

Aerospace contributes 15%, with approximately 28,000 radar units deployed in 2025. These systems support weather monitoring, navigation, and collision avoidance, operating at high frequencies and offering precision detection capabilities.

United States 3D Radar Market Segmentations

Type

- Phased Array Radar

- Pulse Doppler Radar

- Continuous Wave Radar

Application

- Defense & Military

- Automotive

- Aerospace

United States Insights

The United States dominates the regional market, accounting for nearly 100% of total demand and production within the scope. In 2025, over 180,000 radar units were produced domestically, with defense applications accounting for 62%, automotive 24%, and aerospace 14%. The country’s advanced manufacturing infrastructure and strong defense spending support sustained growth.

The automotive sector is witnessing rapid expansion, with radar integration in vehicles increasing by 18% annually. Additionally, aerospace applications are growing at 12% CAGR, driven by increasing air traffic and safety requirements. These factors collectively strengthen the regional outlook.

Top Players in United States 3D Radar Market

- Lockheed Martin Corporation

- Raytheon Technologies Corporation

- Northrop Grumman Corporation

- BAE Systems

- Honeywell International Inc.

- Saab AB

- Thales Group

- Leonardo S.p.A.

- L3Harris Technologies

- General Dynamics Corporation

- Israel Aerospace Industries

- Hensoldt AG

Top Two Companies

-

Lockheed Martin Corporation

-

Holds approximately 22% market share

-

Strong presence in defense radar systems

Lockheed Martin leads the market with advanced phased array radar systems and significant defense contracts exceeding USD 5 billion annually. The company focuses on multi-domain radar integration and AI-enabled systems, supporting over 30% of U.S. military radar deployments.

-

-

Raytheon Technologies Corporation

-

Holds approximately 18% market share

-

Leader in missile defense radar systems

Raytheon specializes in high-performance radar solutions, including missile tracking systems with detection ranges exceeding 450 km. The company invests over 12% of its revenue in R&D, driving innovation and maintaining competitive positioning.

-

Investment

Investment in the 3D Radar Market is increasing significantly, with total investments exceeding USD 14 billion in 2025. Approximately 55% of investments are allocated to defense applications, 30% to automotive, and 15% to aerospace. Regional investment is concentrated in the United States, accounting for nearly 90% of total funding.

Mergers and acquisitions have increased by 18% between 2022 and 2025, with over 25 major deals focusing on radar technology integration and AI capabilities. Collaborative agreements between defense contractors and technology firms have grown by 22%, enabling faster innovation cycles.

New Product

New product development in the 3D Radar Market is focused on improving detection accuracy and reducing system costs. Approximately 28% of new radar products introduced in 2025 feature AI-based enhancements, improving performance by 35% and reducing power consumption by 20%. Additionally, compact radar systems for automotive applications have increased by 32%, supporting widespread adoption.

Recent Development in United States 3D Radar Market

- 2025: Lockheed Martin increased radar production by 18%, delivering over 12,000 units for defense applications. The company expanded its manufacturing capacity by 25%, improving supply chain efficiency.

- 2024: Raytheon introduced a new phased array radar system with 30% higher detection accuracy and deployed over 5,000 units across military platforms.

- 2023: Northrop Grumman enhanced radar processing speeds by 22%, supporting real-time threat detection across 8,000 deployed systems.

Research Methodology for United States 3D Radar Market

The research methodology involves a combination of primary and secondary research approaches. Primary research includes interviews with industry experts, manufacturers, and stakeholders, covering over 40% of data inputs. Secondary research involves analyzing industry reports, company filings, and government publications, contributing 60% of data insights. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within a 5% margin. Data validation is performed through triangulation methods, integrating multiple data sources to provide comprehensive and reliable market insights.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Aviation Systems and Defense Electronics

Maria Swan is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.