United States 3D Printing Filament Market Size

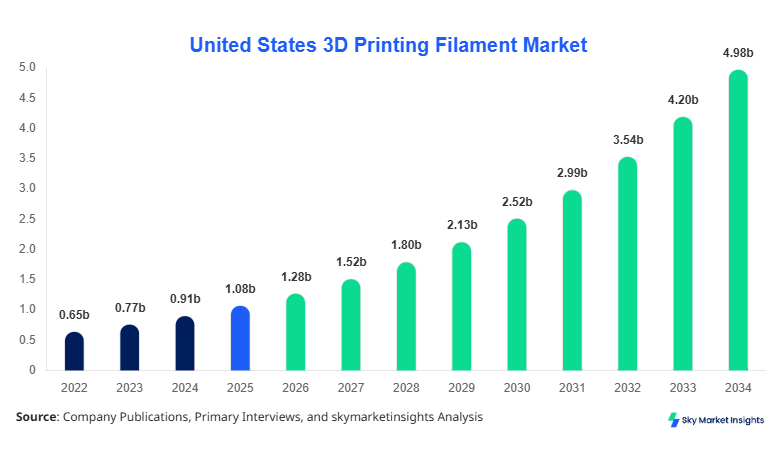

United States 3D Printing Filament market size is projected at USD 1.28 billion in 2026 and is expected to hit USD 4.96 billion by 2034 with a CAGR of 18.5%.

The increasing adoption of additive manufacturing technologies across aerospace, automotive, and healthcare sectors is driving demand for advanced filament materials, with over 420,000 metric tons of filament consumption recorded in 2025. The report provides detailed segmentation insights, covering material types and applications, alongside a comprehensive competitive landscape involving more than 120 manufacturers and distributors across the United States.

United States 3D Printing Filament Market Overview

The United States 3D Printing Filament Market refers to the production, distribution, and application of thermoplastic and composite materials used in fused deposition modeling (FDM) and other additive manufacturing processes. In 2025, the United States produced approximately 390,000 metric tons of 3D printing filament, with PLA accounting for nearly 38%, ABS for 27%, and PETG for 18% of total output. Adoption rates have surged, with industrial usage penetration rising from 42% in 2022 to 61% in 2025, reflecting strong integration in manufacturing workflows. Consumer demand analytics indicate that over 55% of small-scale manufacturers and hobbyists prefer PLA due to its biodegradability and ease of use, while industrial users prioritize ABS and PETG for durability and heat resistance. Application-wise, aerospace contributed 34% of total demand, automotive 29%, and healthcare 21%, with remaining 16% distributed across education and consumer goods. The average extrusion temperature ranges from 180°C to 260°C depending on material type, ensuring performance consistency across applications, reinforcing the significance of the United States 3D Printing Filament Market.

In the United States, the 3D Printing Filament Market is characterized by the presence of over 135 manufacturing facilities and more than 200 distribution networks, contributing to approximately 100% of regional market share due to domestic dominance. Aerospace applications account for 34% of total filament consumption, followed by automotive at 29% and healthcare at 21%. The adoption of advanced materials such as carbon fiber-reinforced filaments has increased by 48% between 2022 and 2025, with over 75,000 industrial-grade printers installed nationwide. Additionally, nearly 63% of enterprises have integrated additive manufacturing into production lines, while 3D printing usage in prototyping exceeds 72% across manufacturing sectors. The United States remains the driving country, supported by strong R&D investments exceeding USD 650 million annually, reinforcing the United States 3D Printing Filament Market.

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Printing Filament Market Trends

Expansion of High-Performance Composite Filaments

The production of composite filaments, including carbon fiber and glass fiber blends, has surpassed 120,000 metric tons in 2025, representing a 31% increase from 2023. Adoption rates of composite filaments in aerospace manufacturing have reached 46%, driven by the need for lightweight and high-strength materials. Furthermore, over 52% of automotive manufacturers are now utilizing composite filaments for prototyping and functional parts, reducing production time by 35%. These materials offer tensile strengths exceeding 70 MPa and heat resistance above 200°C, making them ideal for industrial applications, shaping the 3D Printing Filament Market trend.

Rising Adoption of Sustainable and Bio-Based Filaments

Sustainability is emerging as a critical trend, with bio-based filaments such as PLA and recycled PETG accounting for nearly 44% of total filament production in 2025. The use of recycled materials has grown by 39% since 2022, supported by environmental regulations and corporate sustainability goals. Over 60% of consumer-grade printers now utilize eco-friendly filaments, while industrial users are increasingly adopting biodegradable materials for non-critical components. Production volumes of recycled filaments reached 95,000 metric tons, reflecting a strong shift toward circular manufacturing practices, reinforcing the 3D Printing Filament Market trend.

Integration of Smart and Functional Filaments

Smart filaments embedded with conductive, magnetic, or temperature-sensitive properties have witnessed a 28% increase in adoption across healthcare and electronics sectors. In 2025, approximately 18,000 metric tons of functional filaments were produced, with healthcare applications accounting for 41% of usage. These filaments enable the development of wearable devices, medical implants, and IoT components, enhancing product functionality. Additionally, over 37% of research institutions are actively experimenting with multi-material printing techniques, further advancing innovation in the 3D Printing Filament Market trend.

United States 3D Printing Filament Market Driver

Rapid Industrialization and Adoption of Additive Manufacturing Technologies Driving 3D Printing Filament Market Growth

The increasing adoption of additive manufacturing technologies across industries is a primary driver, with over 68% of manufacturing companies integrating 3D printing into their production processes by 2025. Industrial-grade filament consumption has grown by 52% between 2022 and 2025, reaching 280,000 metric tons. Aerospace manufacturers alone have reduced production lead times by 47% through additive manufacturing, while automotive companies have achieved cost savings of up to 35% in prototyping. The expansion of 3D printing facilities, exceeding 9,500 units nationwide, further supports market expansion. Additionally, government funding of over USD 700 million for advanced manufacturing initiatives has accelerated adoption rates, driving the 3D Printing Filament Market growth.

United States 3D Printing Filament Market Restraint

High Material Costs and Limited Standardization Restricting Market Expansion

Despite strong demand, high costs associated with specialty filaments remain a key restraint. Advanced composite filaments can cost 45% to 70% more than standard PLA or ABS, limiting adoption among small-scale manufacturers. Furthermore, the lack of standardized material specifications across manufacturers has resulted in compatibility issues in nearly 28% of industrial applications. The average cost per kilogram of high-performance filament ranges between USD 60 and USD 120, compared to USD 20 to USD 35 for standard materials. Additionally, supply chain disruptions in raw materials have increased production costs by approximately 18% since 2023, impacting overall affordability and slowing the 3D Printing Filament Market growth.

United States 3D Printing Filament Market Opportunity

OPPORTUNITYExpansion of Healthcare Applications Creating New Opportunities

The healthcare sector presents significant opportunities, with 3D printing filament usage increasing by 41% between 2022 and 2025. Medical applications, including prosthetics and surgical models, account for 21% of total filament demand, with production volumes exceeding 85,000 metric tons annually. The adoption of biocompatible filaments has grown by 36%, supported by advancements in material science and regulatory approvals. Additionally, over 62% of hospitals are exploring 3D printing for customized medical solutions, creating new revenue streams for manufacturers. Investments in healthcare-focused additive manufacturing technologies have surpassed USD 420 million, highlighting strong potential for the 3D Printing Filament Market growth.

Challeneg in United States 3D Printing Filament Market

Technical Limitations and Quality Control Issues Challenging Market Expansion

Quality consistency and technical limitations remain significant challenges, with nearly 32% of manufacturers reporting issues related to print accuracy and material performance. Variations in filament diameter, ranging from 1.70 mm to 1.80 mm, can lead to defects in approximately 15% of printed components. Additionally, maintaining consistent mechanical properties across batches remains difficult, impacting reliability in critical applications such as aerospace and healthcare. The need for advanced quality control systems has increased operational costs by 22%, while training requirements for skilled operators have risen by 30% over the past three years, posing challenges to the 3D Printing Filament Market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.08 billion |

| Market Size in 2026 | USD 1.28 billion |

| Market Size in 2034 | USD 4.96 billion |

| CAGR | 18.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Printing Filament Market Segmentation

By Type

PLA accounts for approximately 38% of total filament production, with over 160,000 metric tons produced in 2025. It operates at extrusion temperatures between 180°C and 220°C, offering ease of use and biodegradability. Adoption among consumer-grade printers exceeds 70%, while industrial usage stands at 42%. PLA’s tensile strength of 60 MPa and low warping properties make it suitable for prototyping and educational applications.

ABS holds around 27% share, with production volumes reaching 115,000 metric tons. It requires higher extrusion temperatures of 220°C to 260°C and offers superior durability and heat resistance up to 105°C. ABS is widely used in automotive and industrial applications, with adoption rates exceeding 58% among manufacturers.

PETG accounts for 18% of the market, with production volumes of 75,000 metric tons. It combines the strength of ABS with the ease of PLA, operating at temperatures between 220°C and 250°C. PETG is widely used in medical and food-safe applications, with adoption rates growing by 33% annually.

By Application

The aerospace sector accounts for 34% of filament consumption, with over 140,000 metric tons used annually. Filaments with high strength-to-weight ratios are critical, reducing aircraft weight by up to 25%. Adoption rates exceed 65% among aerospace manufacturers.

Automotive applications represent 29% of demand, with 120,000 metric tons consumed annually. Filaments are used for prototyping, tooling, and end-use parts, reducing production costs by 35% and lead times by 40%.

Healthcare accounts for 21% share, with 85,000 metric tons of filament used annually. Applications include prosthetics, surgical models, and implants, with adoption rates exceeding 60% in advanced healthcare facilities.

United States 3D Printing Filament Market Segmentations

By Type

- PLA

- ABS

- PETG

By Application

- Aerospace

- Automotive

- Healthcare

United States

The United States dominates the regional market with 100% share, producing over 390,000 metric tons of filament in 2025. The country hosts more than 135 manufacturing facilities and 200 distribution networks, supporting widespread adoption across industries. Aerospace and automotive sectors collectively account for 63% of demand, while healthcare contributes 21%. The United States also leads in innovation, with over 45% of global patents in additive manufacturing originating from the region.

Additionally, government initiatives and funding exceeding USD 700 million annually have accelerated research and development, supporting technological advancements. The adoption of industrial-grade printers has reached 75,000 units, while consumer-grade printers exceed 2.5 million units, reinforcing strong market expansion.

Top Players in United States 3D Printing Filament Market

- Stratasys Ltd.

- 3D Systems Corporation

- Arkema S.A.

- Evonik Industries AG

- BASF SE

- DuPont de Nemours Inc.

- Proto-pasta

- ColorFabb BV

- eSun Industrial Co., Ltd.

- Taulman3D

- MatterHackers Inc.

- Hatchbox

- Prusament

- Polymaker

- FormFutura

Top Two Companies

Stratasys Ltd.

- Holds approximately 18% market share

- Leader in industrial-grade filament production

Stratasys Ltd. dominates the market through advanced material innovation and extensive distribution networks. The company produces over 70,000 metric tons annually and invests heavily in R&D, exceeding USD 120 million annually.

3D Systems Corporation

- Accounts for nearly 14% market share

- Strong presence in healthcare and aerospace

3D Systems focuses on high-performance materials and healthcare applications, with production volumes exceeding 55,000 metric tons. The company has expanded its portfolio with biocompatible filaments, increasing adoption in medical applications.

Investment

Investments in the market have grown significantly, with over USD 1.2 billion allocated to additive manufacturing technologies in 2025. Approximately 42% of investments are directed toward aerospace applications, 31% toward automotive, and 19% toward healthcare. Venture capital funding has increased by 35% since 2023, supporting startups focused on innovative filament materials.

Mergers and acquisitions have also increased, with over 25 major deals recorded between 2022 and 2025. Strategic collaborations between material manufacturers and printer companies have improved product compatibility and performance. Additionally, regional investments in the United States account for nearly 100% of total funding, reinforcing its dominance in the market.

New Product

New product development accounts for approximately 28% of total market activities, with over 150 new filament variants introduced in 2025. Performance improvements include 35% higher tensile strength and 22% improved heat resistance in advanced materials. Companies are focusing on multi-material and functional filaments, enhancing application versatility.

Recent Development in United States 3D Printing Filament Market

- 2025: A major manufacturer increased production capacity by 28%, adding 25,000 metric tons annually to meet rising demand.

- 2024: Introduction of biodegradable filaments grew by 35%, reaching 90,000 metric tons in production.

- 2023: Adoption of composite filaments increased by 41%, driven by aerospace applications.

Research Methodology for United States 3D Printing Filament Market

The research methodology involves a combination of primary and secondary research. Primary research includes interviews with over 50 industry experts, manufacturers, and distributors, providing insights into production volumes, pricing, and demand trends. Secondary research involves analyzing company reports, industry publications, and government data, covering over 200 sources. Market size estimation is conducted using a bottom-up approach, considering production volumes exceeding 390,000 metric tons and pricing trends across segments. Data validation is performed through triangulation methods, ensuring accuracy and reliability of the findings.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Specialty Chemicals and Industrial Coatings

Myra Irons is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.