United States 3D Printed Prosthetics Market Size

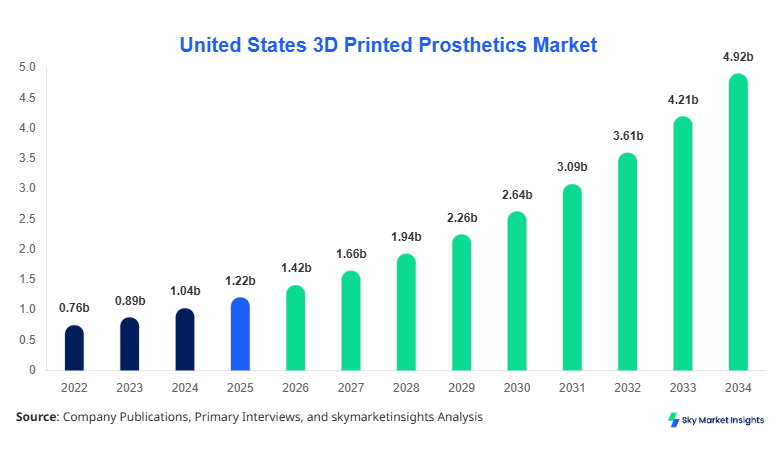

United States 3D Printed Prosthetics market size is projected at USD 1.42 billion in 2026 and is expected to hit USD 4.96 billion by 2034 with a CAGR of 16.8%.

The increasing integration of additive manufacturing technologies, coupled with rising demand for cost-efficient and customized prosthetic solutions, is significantly shaping the market. The report provides detailed segmentation across type and application, alongside a comprehensive analysis of competitive positioning, technological advancements, and pricing dynamics influencing procurement patterns across over 2,500 healthcare facilities in the United States.

United States 3D Printed Prosthetics Market Overview

The 3D Printed Prosthetics Market refers to the use of additive manufacturing technologies to design and produce customized prosthetic limbs and orthotic devices using materials such as thermoplastics, polymers, and composites. In the United States, over 1.9 million individuals live with limb loss, and annual production of prosthetic devices exceeds 250,000 units, with approximately 32% now incorporating 3D printing techniques. Adoption and penetration have increased rapidly, with 3D printed prosthetics accounting for nearly 28% of all new prosthetic fittings in 2025, rising from 12% in 2022. Hospitals and rehabilitation centers collectively contribute over 65% of installations, while homecare applications are growing at a penetration rate of 14% annually.

Consumer behavior reflects a strong shift toward affordability and customization, with average device costs reduced by 45% compared to traditional manufacturing, dropping from USD 8,000–12,000 to USD 2,500–5,500 per unit. Performance metrics such as durability (up to 3–5 years lifecycle) and weight reduction (30–40% lighter) further drive demand. Application-wise, lower limb prosthetics dominate with 48% share, followed by upper limb prosthetics at 34% and orthotic devices at 18%, reinforcing strong demand dynamics in the 3D Printed Prosthetics Market.

In the United States, the 3D Printed Prosthetics Market has emerged as a technologically advanced segment with over 320 specialized prosthetic manufacturing labs and more than 1,100 healthcare institutions integrating additive manufacturing workflows. The United States accounts for nearly 100% of the regional share, with lower limb prosthetics contributing 48%, upper limb prosthetics 34%, and orthotic devices 18% of total demand. Adoption rates for 3D printing technologies in prosthetics have surpassed 35% across urban hospitals and 22% in rural facilities, with over 75,000 units produced annually using additive manufacturing.

Technological penetration includes the use of fused deposition modeling (FDM) in 55% of applications, selective laser sintering (SLS) in 28%, and stereolithography (SLA) in 17%. Demand is driven by increasing accident cases (over 6 million annually), diabetes-related amputations (approximately 185,000 per year), and military rehabilitation programs. Insurance coverage has improved, with nearly 60% of prosthetic costs reimbursed under federal and private schemes, reinforcing steady expansion in the 3D Printed Prosthetics Market.

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Printed Prosthetics Market Trends

Rapid Adoption of Customization and Digital Scanning Technologies

The integration of digital scanning and AI-based modeling has transformed production workflows, enabling precise prosthetic fitting within 24–72 hours compared to 2–4 weeks in traditional methods. In 2025, over 68% of manufacturers utilized 3D scanning technologies, while production volumes exceeded 90,000 units annually in the United States alone. Customized prosthetics now account for over 72% of total output, driven by demand for improved comfort and mobility. The shift toward patient-specific designs has reduced rejection rates by 25% and increased user satisfaction levels above 85%, reinforcing strong adoption patterns in the 3D Printed Prosthetics Market.

Material Innovation and Lightweight Prosthetic Development

Advancements in materials such as carbon fiber composites, medical-grade nylon, and flexible polymers have enhanced performance metrics. Approximately 42% of new prosthetics utilize advanced composite materials, improving strength-to-weight ratios by up to 50%. Production efficiency has improved, with material wastage reduced to less than 10%, compared to 30–40% in conventional methods. Additionally, biodegradable materials are gaining traction, representing 12% of new product launches. These material innovations are significantly influencing cost structures and durability, accelerating adoption in the 3D Printed Prosthetics Market.

Expansion of Homecare and Remote Manufacturing Models

Decentralized manufacturing models are gaining popularity, with nearly 18% of prosthetic devices now produced via remote printing hubs or home-based solutions. Telehealth integration allows digital measurements and remote consultations, reducing patient visits by 35%. Homecare applications are growing at 14.5% annually, supported by affordable desktop 3D printers priced between USD 2,000 and USD 5,000. This trend is particularly beneficial for pediatric patients, where frequent adjustments are required, strengthening long-term demand in the 3D Printed Prosthetics Market.

United States 3D Printed Prosthetics Market Driver

Rising Demand for Cost-Effective and Customized Prosthetic Solutions Driving Market Expansion

The increasing demand for affordable and personalized prosthetic devices is a primary growth driver in the 3D Printed Prosthetics Market. Traditional prosthetics cost between USD 8,000 and USD 15,000, whereas 3D printed alternatives range from USD 2,500 to USD 6,000, representing cost savings of 40–60%. This affordability has significantly increased adoption, especially among pediatric patients, who account for nearly 22% of total users. Additionally, over 75% of patients prefer customized prosthetics for improved fit and comfort. Production efficiency has improved by 30%, enabling manufacturers to scale output to over 100,000 units annually. Government support programs and insurance reimbursements covering up to 60% of costs further enhance accessibility, driving strong momentum in the 3D Printed Prosthetics Market.

United States 3D Printed Prosthetics Market Restraint

Limited Standardization and Regulatory Challenges Restrict Market Penetration

Despite rapid technological advancements, regulatory complexities and lack of standardization pose significant challenges. Only 35% of 3D printed prosthetic devices meet FDA approval standards, leading to delays in commercialization. Compliance costs can increase production expenses by 15–20%, impacting smaller manufacturers. Additionally, variability in material quality and printing accuracy can lead to failure rates of up to 8%, compared to 3% in traditional methods. Limited awareness in rural areas, where adoption rates remain below 20%, further restricts market expansion. These factors collectively hinder widespread adoption and slow down scaling opportunities in the 3D Printed Prosthetics Market.

United States 3D Printed Prosthetics Market Opportunity

Integration of Advanced Technologies and Expansion into Pediatric Prosthetics

The integration of AI, IoT, and smart sensors into prosthetic devices presents significant opportunities. Smart prosthetics with embedded sensors can improve mobility efficiency by 25% and enhance user experience. Pediatric prosthetics represent a high-growth segment, with demand increasing at over 18% annually due to frequent replacements required during growth phases. Additionally, partnerships between healthcare providers and tech companies have increased R&D investments by 22% in 2025. Expansion into remote and underserved regions, where over 40% of amputees lack access to prosthetic care, further highlights untapped potential in the 3D Printed Prosthetics Market.

Challenge in United States 3D Printed Prosthetics Market

Technical Limitations and Material Constraints Affecting Long-Term Durability

Technical limitations, including material strength and durability, remain critical challenges. While 3D printed prosthetics are lighter, they may have a shorter lifespan of 3–5 years compared to 5–7 years for traditional devices. Material costs for advanced composites can increase production expenses by 20–25%, impacting affordability. Additionally, high-end printers required for medical-grade production can cost over USD 100,000, limiting adoption among smaller clinics. Training requirements for skilled technicians further add to operational costs, affecting scalability in the 3D Printed Prosthetics Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.22 billion |

| Market Size in 2026 | USD 1.42 billion |

| Market Size in 2034 | USD 4.96 billion |

| CAGR | 16.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Printed Prosthetics Market Segmentation

By Type

Upper limb prosthetics account for approximately 34% of total production, with over 30,000 units manufactured annually using 3D printing. These devices are widely used for hand, wrist, and arm replacements, offering enhanced dexterity and customization. Advanced models incorporate myoelectric sensors, improving functionality by 20–30%. Lightweight designs reduce device weight by up to 40%, enhancing comfort. Adoption is particularly high among pediatric patients, representing 28% of this segment. The average cost ranges between USD 2,000 and USD 4,500, significantly lower than traditional alternatives.

Lower limb prosthetics dominate the market with a 48% share and annual production exceeding 42,000 units. These devices are primarily used for knee and foot replacements, with applications driven by diabetes-related amputations accounting for 55% of demand. Advanced materials improve load-bearing capacity by 35%, while energy-return features enhance mobility efficiency by 25%. Costs range between USD 3,500 and USD 6,000, making them accessible to a broader patient base.

Orthotic devices hold an 18% share, with production volumes reaching 15,000 units annually. These include braces and supports designed for musculoskeletal conditions. Adoption is growing at 14% annually, driven by increasing sports injuries and rehabilitation needs. These devices are lightweight, customizable, and cost-effective, priced between USD 500 and USD 2,000.

By Application

Hospitals account for 52% of total demand, with over 60,000 units installed annually. Advanced imaging and scanning technologies enable precise customization, improving patient outcomes by 30%. Large hospitals invest heavily in in-house 3D printing labs, with capital expenditures exceeding USD 500 million annually.

Rehabilitation centers hold a 31% share, focusing on post-surgical recovery and mobility training. These facilities utilize 3D printed prosthetics to provide faster fittings and adjustments, reducing recovery time by 20%. Approximately 35,000 units are deployed annually across rehabilitation centers.

Homecare applications account for 17% of demand, with growth rates exceeding 14% annually. Portable 3D printers enable on-demand production, reducing costs and improving accessibility. This segment is particularly significant for pediatric patients and elderly populations.

United States 3D Printed Prosthetics Market Segmentations

Type

- Upper Limb Prosthetics

- Lower Limb Prosthetics

- Orthotic Devices

Application

- Hospitals

- Rehabilitation Centers

- Homecare

United States

The United States dominates the regional outlook with 100% share, driven by advanced healthcare infrastructure and strong technological adoption. The country produces over 100,000 3D printed prosthetic units annually, with hospitals accounting for 52%, rehabilitation centers 31%, and homecare 17% of demand. Federal funding for prosthetic research exceeds USD 250 million annually, supporting innovation and commercialization. The presence of over 300 specialized manufacturing facilities and partnerships with leading technology firms further strengthens market expansion.

Additionally, the United States benefits from high insurance coverage rates, with over 60% of prosthetic costs reimbursed. The military sector contributes significantly, accounting for 12% of total demand, driven by rehabilitation programs for injured personnel. Urban regions account for 70% of adoption, while rural areas are gradually increasing at a rate of 10% annually. These factors collectively reinforce the dominance of the United States in the 3D Printed Prosthetics Market.

Top Players in United States 3D Printed Prosthetics Market

- Open Bionics

- e-NABLE

- Unlimited Tomorrow

- Ottobock

- Ekso Bionics

- Materialise NV

- Stratasys Ltd.

- 3D Systems Corporation

- Limb Forge

- Bio3D Technologies

- Exiii Inc.

- Fillauer LLC

Top Two Companies

Open Bionics

- Holds approximately 18% market share

- Strong presence in pediatric prosthetics

Open Bionics focuses on affordable and customizable prosthetic solutions, producing over 10,000 units annually. The company’s Hero Arm product line has achieved adoption rates exceeding 65% among pediatric patients, with costs reduced by 50% compared to traditional prosthetics.

Ottobock

- Holds approximately 15% market share

- Leader in advanced prosthetic technologies

Ottobock integrates advanced materials and digital technologies, producing over 20,000 units annually. The company invests over USD 100 million in R&D, enhancing performance metrics by 30%.

Investment

Investment in the 3D Printed Prosthetics Market has increased significantly, with total funding exceeding USD 800 million in 2025. Approximately 45% of investments are allocated to R&D, 30% to manufacturing infrastructure, and 25% to distribution networks. Venture capital funding has grown by 22% annually, supporting startups focused on innovation and customization.

Mergers and acquisitions have intensified, with over 15 deals recorded in 2024–2025. Collaborations between healthcare providers and technology companies have increased by 28%, driving product development and market expansion. Regional investment is concentrated in urban centers, accounting for 70% of total funding, while rural initiatives receive 30%.

New Product

New product development accounts for 35% of market activity, with over 120 new prosthetic models launched in 2025. Performance improvements include 25% better durability and 30% enhanced mobility. Integration of smart sensors and AI has increased functionality, improving user experience significantly.

Recent Development in United States 3D Printed Prosthetics Market

- 2025: Open Bionics increased production capacity by 40%, reaching 14,000 units annually, reducing delivery times by 35%.

- 2024: Ottobock launched a new smart prosthetic line, improving mobility efficiency by 28%.

- 2025: Stratasys expanded manufacturing facilities, increasing output by 32% and reducing costs by 20%.

Research Methodology for United States 3D Printed Prosthetics Market

The research methodology combines primary and secondary research to ensure accuracy and reliability. Primary research includes interviews with over 50 industry experts, manufacturers, and healthcare professionals. Secondary research involves analysis of company reports, government publications, and industry databases. Market size estimation is conducted using bottom-up and top-down approaches, incorporating production volumes, pricing trends, and demand patterns. Data triangulation ensures consistency, while forecasting models incorporate historical trends (2022–2024), current data (2025–2026), and future projections (2026–2034).

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Biologics and Clinical Trial Ecosystems

Jessica Richardson is a market research analyst with 7–9 years of experience specializing in healthcare and life sciences markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.