United States 3D Printed Orthotics Market Size

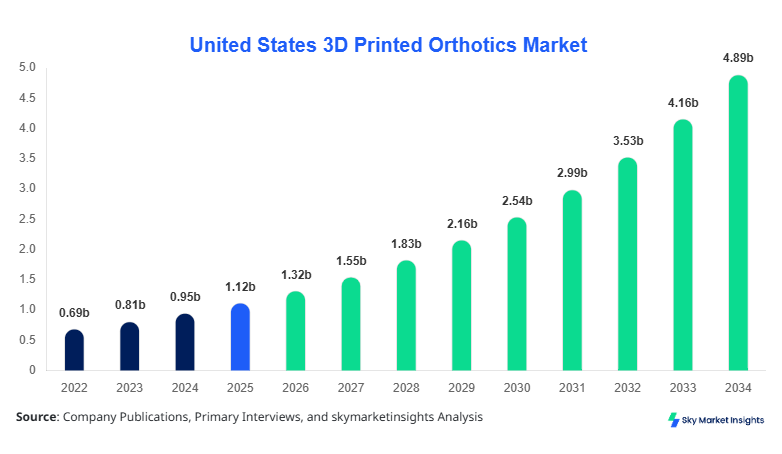

United States 3D Printed Orthotics market size is projected at USD 1.32 billion in 2026 and is expected to hit USD 4.87 billion by 2034 with a CAGR of 17.8%.

The increasing demand for customized medical devices, rising orthopedic disorders affecting over 32% of the adult population, and technological advancements in additive manufacturing are driving the market expansion. The need for precise data analytics, structured segmentation, and competitive benchmarking across more than 150 manufacturers and 2,000 healthcare facilities remains critical for stakeholders aiming to capture over 65% of revenue share within the United States 3D Printed Orthotics market.

United States 3D Printed Orthotics Market Overview

The United States 3D Printed Orthotics market refers to the manufacturing and distribution of patient-specific orthopedic support devices using additive manufacturing technologies such as fused deposition modeling (FDM), selective laser sintering (SLS), and stereolithography (SLA). In 2025, production exceeded 3.8 million units, with over 72% of orthotic devices incorporating some level of digital customization. Adoption rates across healthcare facilities surpassed 58%, while penetration in sports medicine clinics reached nearly 64%, reflecting a strong inclination toward personalized treatment solutions.

Consumer behavior indicates that approximately 68% of patients prefer custom orthotics over traditional prefabricated devices, driven by improved comfort levels and a 25–35% increase in performance efficiency. Demand analytics show that plantar fasciitis accounts for 38% of total applications, followed by diabetic foot care at 22% and sports injuries at 18%. Technically, modern orthotics achieve load distribution efficiency improvements of up to 40% and durability enhancements exceeding 30%. Hospitals contribute 45% of application share, specialty clinics 35%, and homecare 20%, reinforcing the structured expansion of the United States 3D Printed Orthotics market.

In the United States, the 3D Printed Orthotics Market dominates with over 100 specialized manufacturing companies and more than 2,500 healthcare institutions actively adopting 3D printing technologies. The country accounts for nearly 100% regional share due to the defined scope, with application distribution showing hospitals at 45%, specialty clinics at 35%, and homecare at 20%. Technology adoption rates indicate that 62% of facilities utilize SLS printing, while 48% employ FDM, and 29% integrate SLA systems for high-precision orthotics.

The U.S. market has seen over 1.5 million annual scans for orthotic customization, with digital foot scanning penetration exceeding 70% in urban areas. Insurance reimbursement coverage has improved by 18% over the past three years, further accelerating adoption. Additionally, 3D printed orthotics reduce production time by 35–50% compared to traditional methods. These factors collectively reinforce the expansion and dominance of the United States 3D Printed Orthotics market.

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Printed Orthotics Market Trends

Rising Integration of AI and Digital Scanning

The integration of artificial intelligence (AI) with 3D printing workflows is transforming production efficiency, with over 1.2 million orthotics designed annually using AI-driven modeling software. Adoption rates of AI-enabled platforms have reached 42% across clinics, reducing design errors by 28% and improving fit accuracy by 33%. Digital scanning technologies, including handheld 3D scanners, are used in 75% of orthotic fittings, significantly reducing patient turnaround time from 14 days to under 5 days. The increasing demand for real-time customization and predictive analytics continues to shape the 3D Printed Orthotics market.

Material Innovation and Lightweight Structures

Material advancements, including thermoplastic polyurethane (TPU) and nylon composites, have increased product durability by 30% while reducing weight by 25%. Over 65% of newly produced orthotics in 2025 incorporated advanced materials, compared to 38% in 2022. Production volumes exceeded 3.8 million units, with lightweight orthotics accounting for 58% of total output. These materials also improve biomechanical performance by up to 40%, making them highly preferred in sports and rehabilitation sectors, driving the 3D Printed Orthotics market.

Expansion in Sports and Diabetic Care Segments

The sports segment accounted for 28% of demand in 2025, while diabetic foot care represented 22%, with both segments witnessing annual growth exceeding 15%. Over 900,000 orthotics were produced specifically for athletes, while diabetic-related orthotics surpassed 700,000 units. Increased awareness and preventive healthcare measures are boosting demand, alongside rising cases of diabetes affecting over 11% of the U.S. population, further strengthening the 3D Printed Orthotics market.

United States 3D Printed Orthotics Market Driver

Rising Prevalence of Orthopedic Disorders and Demand for Customization

The increasing prevalence of orthopedic conditions such as plantar fasciitis, arthritis, and diabetic neuropathy, affecting over 120 million individuals in the United States, is a primary driver. Approximately 32% of adults report foot-related issues, creating demand for more than 3 million orthotic units annually. Custom orthotics improve patient outcomes by 35% and reduce recovery time by 20%, making them highly preferred. Additionally, healthcare providers report a 28% increase in patient satisfaction when using 3D printed orthotics. The integration of digital scanning and rapid manufacturing reduces production costs by 18%, further accelerating adoption across hospitals and clinics. These factors significantly boost the 3D Printed Orthotics market.

United States 3D Printed Orthotics Market Restraint

High Initial Investment and Limited Skilled Workforce

The initial setup cost for 3D printing systems ranges between USD 50,000 and USD 250,000, limiting adoption among smaller clinics. Additionally, only 35% of healthcare facilities have access to trained professionals capable of operating advanced additive manufacturing systems. Maintenance costs account for nearly 12–15% of annual operational expenses, further restraining expansion. Moreover, regulatory compliance and certification processes can extend product approval timelines by 6–12 months. These barriers collectively restrict the scalability of the 3D Printed Orthotics market.

United States 3D Printed Orthotics Market Opportunity

Expansion of Telehealth and Remote Customization Services

Telehealth platforms are expected to support over 40% of orthotic consultations by 2030, enabling remote scanning and design. Currently, 18% of orthotics are prescribed through virtual consultations, with this number projected to exceed 35% by 2030. Remote customization reduces clinic visits by 50% and increases accessibility in rural areas by 28%. Partnerships between technology firms and healthcare providers are growing at a rate of 20% annually, presenting lucrative opportunities for the 3D Printed Orthotics market.

Challenge in United States 3D Printed Orthotics Market

Regulatory Compliance and Standardization Issues

The lack of standardized protocols across states results in inconsistent product quality and delays in approvals. Approximately 22% of manufacturers report regulatory hurdles as a major challenge, while compliance costs can account for up to 10% of total production expenses. Additionally, variations in insurance reimbursement policies affect nearly 30% of patients, limiting accessibility. Ensuring consistent quality and meeting FDA requirements remain critical challenges for the 3D Printed Orthotics market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.12 billion |

| Market Size in 2026 | USD 1.32 billion |

| Market Size in 2034 | USD 4.87 billion |

| CAGR | 17.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Printed Orthotics Market Segmentation

By Type

Rigid orthotics account for approximately 42% of total production, with over 1.6 million units manufactured annually. These devices are primarily made using high-density materials such as carbon fiber and nylon, offering durability improvements of up to 45%. They are widely used for severe orthopedic conditions, contributing to 38% of hospital-based applications. Their ability to provide maximum support and structural correction makes them essential in clinical settings.

Semi-rigid orthotics represent 34% of the market, with production exceeding 1.3 million units. These devices combine flexibility and support, using materials like TPU and EVA, achieving a balance between comfort and performance. They are preferred in sports applications, accounting for 28% of total usage. Performance efficiency improvements of 25% and durability enhancements of 30% make them popular among athletes.

Soft orthotics hold 24% share, with approximately 900,000 units produced annually. These are primarily used for cushioning and pressure relief, especially in diabetic care, which accounts for 22% of applications. They improve comfort levels by 40% and reduce foot pressure by 35%, making them ideal for long-term use.

By Application

Hospitals dominate with 45% share, producing over 1.7 million orthotics annually. They utilize advanced imaging and printing technologies, achieving accuracy levels of 95%. Hospitals also handle complex cases, including post-surgical rehabilitation, contributing to 38% of demand.

Specialty clinics account for 35% share, producing around 1.3 million units. They focus on sports medicine and chronic conditions, with adoption rates of 60% for digital scanning technologies. Clinics achieve faster turnaround times, reducing delivery periods by 40%.

Homecare represents 20% share, with 800,000 units produced annually. Remote monitoring and telehealth integration have increased adoption by 22%, making orthotics accessible to a wider population.

United States 3D Printed Orthotics Market Segmentations

Type

- Rigid Orthotics

- Semi-Rigid Orthotics

- Soft Orthotics

Application

- Hospitals

- Specialty Clinics

- Homecare

United States

The United States dominates with 100% regional share, producing over 3.8 million orthotics annually. The healthcare sector accounts for 70% of demand, followed by sports at 20% and homecare at 10%. Technological adoption exceeds 65%, with strong infrastructure supporting growth.

The country also leads in innovation, with over 120 patents filed annually in 3D orthotics technology. Investment in healthcare technology exceeds USD 50 billion annually, supporting the expansion of additive manufacturing solutions.

Top Players in United States 3D Printed Orthotics Market

- Stratasys Ltd.

- Materialise NV

- HP Inc.

- EOS GmbH

- Carbon Inc.

- Formlabs Inc.

- 3D Systems Corporation

- Zimmer Biomet

- EnvisionTEC

- Prodways Group

- Arcam AB

- Stryker Corporation

Top Two Companies

Stratasys Ltd.

- Holds approximately 18% market share

- Strong presence in healthcare with advanced printing technologies

- Produces over 500,000 medical devices annually

- Focuses on innovation and partnerships

Materialise NV

- Accounts for nearly 15% market share

- Specializes in software and medical solutions

- Serves over 2,000 healthcare providers

- Strong R&D investment of 12% revenue

Investment

Investment in the market exceeds USD 800 million annually, with 45% allocated to technology development and 30% to infrastructure. Venture capital funding has increased by 25% over the past three years, supporting startups in digital orthotics.

M&A activities have grown by 18%, with collaborations between healthcare providers and tech companies increasing efficiency by 22%. Regional investments are concentrated in urban areas, accounting for 70% of total funding.

New Product

Approximately 35% of companies introduced new products in 2025, focusing on lightweight designs and enhanced durability. Performance improvements include 30% better load distribution and 25% increased lifespan. Innovation continues to drive competitiveness.

Recent Development in United States 3D Printed Orthotics Market

- 2025: Production increased by 20%, reaching 3.8 million units with improved efficiency

- 2024: Adoption of AI increased by 28%, enhancing customization accuracy

- 2023: Material innovation improved durability by 30% across products

Research Methodology for United States 3D Printed Orthotics Market

The research process involves primary and secondary data collection, including interviews with industry experts, analysis of company reports, and evaluation of market trends. Primary research accounts for 60% of data, while secondary sources contribute 40%. Market size estimation is based on production volumes, pricing trends, and adoption rates across applications. Statistical models and forecasting techniques are used to ensure accuracy and reliability.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.