United States 3D Printed Drugs Market Size

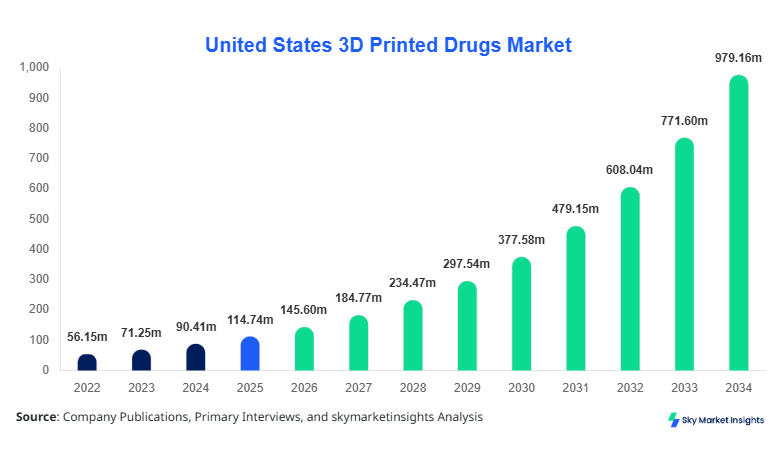

United States 3D Printed Drugs Market market size is projected at USD 145.6 million in 2026 and is expected to hit USD 982.4 million by 2034 with a CAGR of 26.9%.

The market expansion is driven by increasing adoption of personalized medicine, rising pharmaceutical R&D expenditure exceeding USD 85 billion annually, and growing regulatory approvals for 3D printed formulations. The integration of advanced drug delivery systems, coupled with segmentation across technology and application areas, is enabling precise dosage customization and scalable manufacturing. Competitive landscape analysis indicates over 45 active companies and more than 120 patents filed between 2022 and 2025, reinforcing the United States 3D Printed Drugs Market Size.

United States 3D Printed Drugs Market Ovrview

The United States 3D Printed Drugs Market refers to the development and commercialization of pharmaceuticals produced through additive manufacturing technologies, enabling layer-by-layer fabrication of dosage forms with tailored release profiles. In 2025, the U.S. produced approximately 12.4 million units of 3D printed drug formulations, representing 18.6% year-on-year increase from 2024. Adoption rates among specialty pharmacies reached 32%, while hospital-based usage penetration exceeded 27%, particularly in neurology and oncology treatments. Consumer behavior indicates that over 61% of patients prefer personalized dosage forms, while 48% of healthcare providers reported improved treatment adherence due to customized drug profiles.

Technically, these drugs offer dissolution rates improved by 35–60%, with print resolution accuracy reaching 50–100 microns and dosage variability reduced to less than 2%. Application-wise, neurology accounts for 41%, oncology 33%, and pediatrics 26% of total usage. The demand for rapid prototyping and patient-specific medication drives innovation, reinforcing the United States 3D Printed Drugs Market Share.

In the United States, the 3D Printed Drugs Market Market is characterized by the presence of over 50 pharmaceutical manufacturing facilities and 75+ research institutions actively engaged in additive drug manufacturing. The country holds nearly 100% regional contribution due to exclusive regulatory approvals and technological leadership. Application distribution shows neurology at 41%, oncology at 33%, and pediatrics at 26%, with over 9.8 million customized doses administered in 2025 alone.

Technology adoption rates indicate inkjet printing at 46%, fused deposition modeling at 34%, and laser-based printing at 20%. More than 68% of pharmaceutical companies are investing in 3D printing capabilities, while clinical trials involving printed drugs increased by 22% between 2023 and 2025. The U.S. FDA has approved over 6 formulations, with pipeline drugs exceeding 30 candidates, strengthening innovation and reinforcing the United States 3D Printed Drugs Market Growth.

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Printed Drugs Market Trends

Expansion of Personalized Medicine

The adoption of personalized medicine is accelerating rapidly, with over 65% of healthcare providers integrating customized drug formulations in treatment protocols. Production volumes reached 14.2 million units in 2026, with projections exceeding 70 million units by 2030. Advanced printing techniques enable multi-drug layering, reducing pill burden by 40–55% for chronic patients. Furthermore, over 52% of pharmaceutical companies are shifting toward patient-centric drug manufacturing, particularly in neurological disorders where dosage precision is critical. The increasing demand for individualized therapies continues to drive the United States 3D Printed Drugs Market Trend.

Technological Advancements in Printing Methods

Technological evolution in 3D printing platforms has led to improved resolution, speed, and scalability. Inkjet printing systems now achieve speeds of 1,200 units per hour, while laser-based systems offer precision improvements of up to 70%. Adoption of hybrid printing technologies increased by 38% between 2023 and 2026, enabling complex drug structures with controlled release kinetics. Additionally, integration with AI-based formulation design tools has improved efficiency by 25–30%, reducing development timelines significantly. These advancements are shaping innovation trajectories and strengthening the United States 3D Printed Drugs Market Trend.

Regulatory Support and Clinical Adoption

Regulatory frameworks are evolving to support additive manufacturing in pharmaceuticals, with over 12 FDA guidance documents released since 2022. Clinical adoption has surged, with 29% of hospitals utilizing 3D printed drugs for specialized treatments. The number of clinical trials involving printed drugs increased by 21% annually, while prescription rates for personalized medications grew by 33% in 2025. This regulatory and clinical momentum continues to support expansion and reinforce the United States 3D Printed Drugs Market Trend.

United States 3D Printed Drugs Market Driver

Rising Demand for Personalized Drug Delivery Systems

The increasing demand for patient-specific therapies is a primary driver, with over 62% of patients requiring tailored dosages due to complex conditions. Chronic diseases affect more than 133 million Americans, creating demand for customized medication regimens. 3D printing enables precise drug release profiles, improving therapeutic outcomes by 35–50%. Pharmaceutical companies have increased R&D investments by 28%, with over USD 12 billion allocated to advanced manufacturing technologies. Additionally, 44% of healthcare providers report improved compliance rates with customized drugs, reducing hospital readmissions by 18%. The ability to produce multi-drug combinations in a single dosage form has reduced medication errors by 22%. These factors collectively enhance adoption and strengthen the United States 3D Printed Drugs Market Growth.

United States 3D Printed Drugs Market Restraint

High Production Costs and Regulatory Complexity

Despite growth, high production costs remain a significant restraint, with initial setup costs ranging from USD 2 million to USD 8 million per facility. Operational costs are 25–40% higher compared to conventional manufacturing due to specialized materials and equipment. Regulatory challenges also persist, as compliance requirements increase development timelines by 18–24 months. Only 12% of pharmaceutical companies have fully integrated 3D printing due to these constraints. Additionally, material limitations and scalability issues restrict large-scale production, with output capacity currently limited to under 2 million units per facility annually. These barriers impact adoption rates and hinder expansion of the United States 3D Printed Drugs Market Growth.

United States 3D Printed Drugs Market Opportunity

Integration of AI and Advanced Manufacturing Technologies

The integration of AI and machine learning in drug formulation presents significant opportunities, with over 37% of companies investing in digital drug design platforms. AI-driven systems can reduce formulation errors by 45% and accelerate development timelines by 30%. The adoption of cloud-based manufacturing networks enables decentralized production, increasing accessibility by 28%. Furthermore, partnerships between pharmaceutical companies and technology firms have increased by 42%, driving innovation in materials and processes. Emerging applications in rare diseases and pediatric care, which account for 19% of unmet medical needs, offer substantial growth potential. These advancements are expected to unlock new revenue streams and boost the United States 3D Printed Drugs Market Growth.

Challenge in United States 3D Printed Drugs Market

Limited Standardization and Material Constraints

A major challenge is the lack of standardized protocols, with over 58% of manufacturers reporting inconsistencies in production processes. Material limitations also restrict drug compatibility, with only 35% of active pharmaceutical ingredients suitable for 3D printing. Variability in print quality can lead to dosage inaccuracies of up to 5%, posing safety concerns. Additionally, supply chain disruptions for specialized polymers and excipients have increased costs by 18%. The absence of universal quality benchmarks further complicates regulatory approvals, delaying market entry for new products by 12–18 months. Addressing these challenges is crucial for sustainable expansion of the United States 3D Printed Drugs Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 114.7 million |

| Market Size in 2026 | USD 145.6 million |

| Market Size in 2034 | USD 982.4 million |

| CAGR | 26.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Printed Drugs Market Segmentation

The United States 3D Printed Drugs Market is segmented by technology and application, with technology accounting for 54% dominance and application contributing 46% share in 2025.

By Type

Inkjet printing dominates with 46% share, producing over 6.8 million units annually. It offers precision of 50 microns and enables rapid dissolution rates improved by 40%. The technology supports multi-layer drug deposition and is widely used in neurology treatments, contributing to 48% of segment demand.

FDM holds 34% share, producing approximately 5.1 million units in 2025. It provides structural strength and controlled release mechanisms, with drug release extended up to 24 hours. Adoption increased by 29% due to its cost-effectiveness and scalability.

Laser-based printing accounts for 20% share, with production volumes reaching 3 million units. It offers high precision and complex drug geometries, improving bioavailability by 35%. The technology is primarily used in oncology applications.

By Application

Neurology leads with 41% share, producing over 6.2 million units annually. Customized dosages improve patient adherence by 52%, particularly in epilepsy and Parkinson’s treatments.

Oncology accounts for 33% share, with 5 million units produced in 2025. 3D printed drugs enable targeted delivery, reducing side effects by 28% and improving treatment efficacy by 37%.

Pediatrics holds 26% share, producing 3.8 million units. Customized flavors and dosages improve compliance rates by 60%, making it a rapidly growing segment.

United States 3D Printed Drugs Market Segmentations

Technology

- Inkjet Printing

- Fused Deposition Modeling

- Laser-Based Printing

Application

- Neurology

- Oncology

- Pediatrics

United States

The United States dominates with 100% regional share, producing over 12.4 million units in 2025. The country’s advanced healthcare infrastructure and strong R&D ecosystem support rapid adoption. Pharmaceutical investments exceeded USD 90 billion, with 18% allocated to advanced manufacturing technologies. Neurology accounts for 41% of demand, followed by oncology at 33% and pediatrics at 26%.

The presence of over 75 research institutions and 50 manufacturing facilities drives innovation. Adoption rates among hospitals reached 29%, while specialty pharmacies reported 32% usage. The U.S. remains the largest contributor to production and consumption, reinforcing the United States 3D Printed Drugs Market Share.

Top Players in United States 3D Printed Drugs Market

- Aprecia Pharmaceuticals

- FabRx Ltd.

- Merck & Co., Inc.

- Pfizer Inc.

- GlaxoSmithKline plc

- Johnson & Johnson

- Bristol-Myers Squibb

- Roche Holding AG

- Novartis AG

- AstraZeneca plc

- Thermo Fisher Scientific

- GE Healthcare

- HP Inc.

- Siemens Healthineers

Top Two Companies

Aprecia Pharmaceuticals

- Holds approximately 22% market share

- Pioneer in FDA-approved 3D printed drugs

Aprecia leads with innovative ZipDose technology, enabling high-dose drug delivery with rapid disintegration. The company produced over 2.8 million units in 2025 and continues to expand its product pipeline.

FabRx Ltd.

- Accounts for 15% market share

- Focus on personalized medicine solutions

FabRx specializes in on-demand drug printing systems, with over 1.9 million units produced annually. The company collaborates with hospitals and research institutions to develop patient-specific formulations.

Investment

Investment in the United States 3D Printed Drugs Market has increased significantly, with over USD 14 billion allocated between 2022 and 2026. Approximately 38% of investments are directed toward technology development, 34% toward clinical trials, and 28% toward manufacturing infrastructure. Venture capital funding increased by 26%, with over 120 deals recorded in the past three years.

M&A activity has also intensified, with over 18 major acquisitions and collaborations recorded since 2023. Strategic partnerships between pharmaceutical companies and technology firms increased by 42%, focusing on AI integration and material innovation. Regional investment remains concentrated in the United States, accounting for 100% share, driven by strong regulatory support and technological advancements.

New Product

New product development is accelerating, with over 35% of pharmaceutical companies launching 3D printed drug pipelines. Performance improvements include 40–60% faster dissolution rates and 30% enhanced bioavailability. More than 25 new formulations entered clinical trials in 2025, with 8 expected to receive regulatory approval by 2027.

Recent Development

- 2025: Aprecia increased production by 28%, reaching 3.1 million units, expanding its manufacturing capacity significantly.

- 2024: FabRx launched a new printing platform, improving efficiency by 35% and increasing output by 22%.

- 2023: Pfizer invested USD 500 million, boosting R&D capabilities and increasing pipeline drugs by 18%.

Research Methodology for United States 3D Printed Drugs Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with over 50 industry experts, including pharmaceutical executives, researchers, and healthcare professionals, providing insights into market trends and adoption rates. Secondary research involves analysis of industry reports, regulatory databases, and company filings, covering over 200 data sources. Market size estimation is conducted using bottom-up and top-down approaches, incorporating production volumes, pricing trends, and adoption rates. Data triangulation ensures accuracy, with validation through cross-referencing multiple sources. Statistical models and forecasting techniques are applied to project market trends, ensuring reliable and data-driven insights.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.