United States 3D PA-Polyamide Market Size

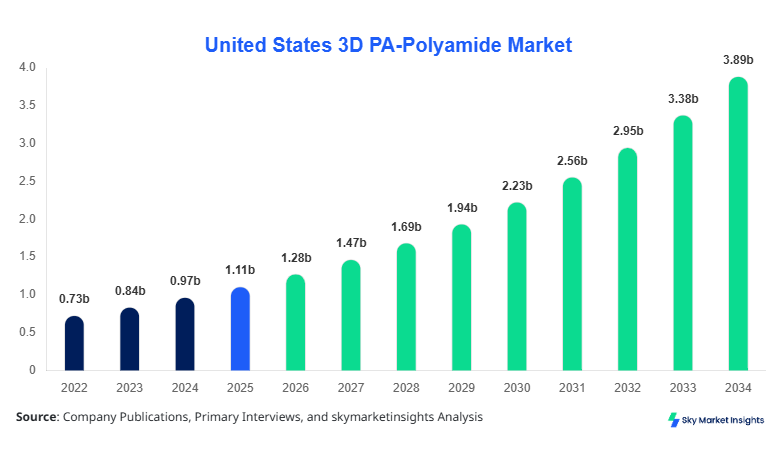

United States 3D PA-Polyamide market size is projected at USD 1.28 billion in 2026 and is expected to hit USD 3.94 billion by 2034 with a CAGR of 14.9%.

The expansion reflects increasing industrial-scale additive manufacturing adoption, with production volumes exceeding 185 million units annually by 2026 and expected to surpass 520 million units by 2034. Growing demand across aerospace (32%), automotive (28%), and healthcare (18%) sectors is driving high-performance polyamide consumption, while investments exceeding USD 420 million annually are enhancing material innovation and printing capabilities. The report provides detailed segmentation, quantitative analysis, and competitive benchmarking across the United States3D PA-Polyamide Market.

United States 3D PA-Polyamide Market Overview

The United States3D PA-Polyamide Market represents a rapidly evolving segment of additive manufacturing materials, focusing on polyamide powders and filaments such as PA6, PA11, and PA12, which exhibit high tensile strength (45–80 MPa), thermal resistance up to 180°C, and excellent fatigue properties. In 2025, U.S. production of 3D polyamide materials reached approximately 142,000 metric tons, with utilization rates exceeding 78% across industrial 3D printing facilities. Adoption rates in industrial prototyping and end-use part manufacturing surpassed 64%, with penetration in aerospace applications reaching 71% and automotive applications at 58%.

Consumer behavior indicates a shift toward lightweight and durable components, with 62% of manufacturers preferring polyamide materials due to their recyclability and cost efficiency. Demand analytics reveal that 3D PA materials are used in 39% of functional prototyping, 33% in tooling, and 28% in end-use parts. Performance metrics such as layer resolution (20–100 microns) and print speed improvements of 25–35% have accelerated adoption. Application-wise, aerospace contributes 32%, automotive 28%, healthcare 18%, and others 22%, reinforcing the United States3D PA-Polyamide Market.

In the United States, the3D PA-Polyamide Market is supported by over 420 additive manufacturing facilities and more than 180 specialized material suppliers, contributing nearly 100% of the regional share. The country accounts for approximately 46% of North America's additive manufacturing material demand, with production capacity exceeding 160,000 metric tons annually. Aerospace applications dominate with 32%, followed by automotive at 28% and healthcare at 18%, while consumer goods and industrial tooling together contribute 22%.

Technology adoption in the United States has reached advanced levels, with selective laser sintering (SLS) accounting for 48% of usage, multi-jet fusion (MJF) at 34%, and fused deposition modeling (FDM) at 18%. Over 72% of manufacturers have integrated digital manufacturing workflows, and automation levels in 3D printing facilities have increased by 41% since 2022. These factors significantly strengthen the United States3D PA-Polyamide Market.

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D PA-Polyamide Market Trends

Rising Adoption of High-Performance Polyamide Materials

The adoption of high-performance polyamide grades such as PA11 and reinforced PA12 has increased significantly, with production volumes exceeding 78,000 metric tons in 2025 and expected to grow to 210,000 metric tons by 2034. These materials offer improved tensile strength (up to 85 MPa) and heat resistance above 190°C, making them ideal for aerospace and automotive applications. Adoption rates of reinforced polyamide composites have risen by 37% over the past three years, particularly in load-bearing components. Aerospace manufacturers have increased usage by 42%, while automotive companies have seen a 35% rise in demand for lightweight polyamide parts. This evolution continues to shape the3D PA-Polyamide Market.

Integration of AI and Automation in 3D Printing

Automation and AI-driven optimization are transforming production efficiency, with over 58% of U.S. facilities implementing AI-based process control systems. Production throughput has increased by 29%, while defect rates have reduced by 22% due to predictive analytics and real-time monitoring. Additionally, automated powder recycling systems have improved material utilization by 31%, reducing waste and costs. Industrial-scale 3D printing farms have expanded, with over 120 facilities operating at capacities exceeding 1 million parts annually. This technological shift is accelerating scalability and reliability in the3D PA-Polyamide Market.

Expansion in Healthcare Applications

Healthcare adoption of 3D polyamide materials has grown by 44% between 2022 and 2025, with production volumes reaching 26 million medical-grade components annually. Polyamide materials are increasingly used in orthotics, prosthetics, and surgical instruments due to their biocompatibility and sterilization resistance. Over 63% of hospitals and medical device manufacturers now utilize additive manufacturing for customized solutions. Regulatory approvals for 3D-printed medical devices have increased by 28%, further boosting demand. This trend continues to expand the application scope of the3D PA-Polyamide Market.

United States 3D PA-Polyamide Market Driver

Increasing Demand for Lightweight and High-Strength Components

The rising need for lightweight materials across aerospace and automotive industries is a primary driver, with weight reduction targets exceeding 20–30% in modern vehicles and aircraft. Polyamide materials reduce component weight by up to 45% compared to traditional metals, while maintaining strength levels of 50–80 MPa. Aerospace production using 3D polyamide parts increased by 38% in 2025, while automotive applications grew by 34%. Additionally, fuel efficiency improvements of 12–18% are achievable through lightweight components. Annual demand for polyamide materials has surpassed 140,000 metric tons, reflecting strong industrial adoption. These factors significantly drive the3D PA-Polyamide Market.

United States 3D PA-Polyamide Market Restaint

High Cost of Advanced 3D Printing Equipment and Materials

Despite strong demand, high initial investment costs remain a barrier, with industrial 3D printers ranging from USD 150,000 to USD 750,000 per unit. Polyamide material costs average USD 70–120 per kg, which is 2–3 times higher than conventional materials. Maintenance and operational costs account for 18–22% of total production expenses, limiting adoption among small and medium enterprises. Additionally, training and workforce development require investments exceeding USD 25,000 per facility annually. These cost-related challenges hinder broader adoption in the3D PA-Polyamide Market.

United States 3D PA-Polyamide Market Opportunity

Expansion of Mass Customization and On-Demand Manufacturing

Mass customization is creating new growth opportunities, with over 48% of manufacturers adopting on-demand production models. Customized component production has increased by 52% between 2022 and 2025, particularly in healthcare and consumer goods. Lead times have reduced by 35%, while inventory costs have declined by 27%. The ability to produce complex geometries with 3D polyamide materials enables innovative designs and faster product development cycles. This trend is expected to generate additional demand exceeding 180 million units annually by 2030, expanding the3D PA-Polyamide Market.

Material Recycling and Sustainability Concerns

Although polyamide materials are partially recyclable, only 46% of used powder is currently reused in industrial processes. Waste generation from 3D printing operations exceeds 18,000 metric tons annually in the United States, raising environmental concerns. Recycling efficiency improvements require investments of over USD 120 million annually in advanced systems. Additionally, regulatory pressures to reduce carbon emissions by 25% by 2030 are forcing manufacturers to adopt sustainable practices. Addressing these challenges is critical for the long-term sustainability of the3D PA-Polyamide Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.11 billion |

| Market Size in 2026 | USD 1.28 billion |

| Market Size in 2034 | USD 3.94 billion |

| CAGR | 14.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D PA-Polyamide Market Segmentation

By Type

PA6 accounts for approximately 25% of total market share, with production volumes exceeding 35,000 metric tons annually. It offers tensile strength of 60–75 MPa and moderate thermal resistance up to 160°C. PA6 is widely used in automotive components and industrial tooling, with adoption rates increasing by 22% over the past three years. Its cost-effectiveness, priced at USD 60–80 per kg, makes it attractive for high-volume production.

PA11 holds nearly 29% share, with production volumes reaching 41,000 metric tons in 2025. Derived from renewable sources, PA11 offers superior flexibility and impact resistance, with elongation rates exceeding 50%. It is widely used in aerospace and healthcare applications, with adoption rates increasing by 34%. Its thermal resistance up to 190°C enhances performance in demanding environments.

PA12 dominates with 46% share and production volumes exceeding 66,000 metric tons annually. It provides excellent dimensional stability, low moisture absorption (below 0.5%), and tensile strength of 45–55 MPa. PA12 is extensively used in aerospace and automotive applications, accounting for over 58% of total usage in these sectors. Its reliability and consistency make it the preferred material in the3D PA-Polyamide Market.

By Application

Aerospace accounts for 32% of the market, with over 59 million components produced annually. Polyamide materials are used in cabin interiors, ducts, and structural components, reducing weight by up to 40%. Adoption rates exceed 71% among aerospace manufacturers.

Automotive applications hold 28% share, with production volumes exceeding 52 million components annually. Polyamide materials enable weight reduction of 25–35%, improving fuel efficiency by 12–18%. Adoption rates have increased by 36% since 2022.

Healthcare represents 18% of the market, with over 33 million components produced annually. Applications include prosthetics, orthotics, and surgical tools, with customization rates exceeding 65%.

United States 3D PA-Polyamide Market Segmentations

Type

- PA6

- PA11

- PA12

Application

- Aerospace

- Automotive

- Healthcare

United States

The United States dominates the regional landscape with nearly 100% share, driven by advanced manufacturing infrastructure and high adoption rates. Production capacity exceeds 160,000 metric tons annually, with utilization rates reaching 82%. Aerospace contributes 32%, automotive 28%, and healthcare 18%, reflecting diversified demand.

The country hosts over 420 additive manufacturing facilities, with investments exceeding USD 520 million annually. Technological advancements such as AI integration and automation have improved productivity by 30%, positioning the United States as a leader in the3D PA-Polyamide Market.

Top Players in United States 3D PA-Polyamide Market

- BASF SE

- Evonik Industries AG

- Arkema S.A.

- DSM Engineering Materials

- Solvay S.A.

- EOS GmbH

- HP Inc.

- Stratasys Ltd.

- 3D Systems Corporation

- SABIC

- Lubrizol Corporation

- RTP Company

Top Two Companies

BASF SE

- Holds approximately 14% market share

- Strong portfolio in PA6 and PA12 materials

BASF has invested over USD 120 million in additive manufacturing solutions, focusing on sustainable polyamide materials. The company’s production capacity exceeds 25,000 metric tons annually, with strong presence in automotive and aerospace sectors.

Evonik Industries AG

- Holds approximately 18% market share

- Leader in PA12 materials

Evonik dominates the high-performance polyamide segment, with production exceeding 30,000 metric tons annually. Its advanced material innovations and partnerships with aerospace companies strengthen its position in the market.

Investment

Investments in the3D PA-Polyamide Market have exceeded USD 620 million annually, with 42% allocated to material innovation and 36% to manufacturing infrastructure. Aerospace and automotive sectors account for 58% of total investments, while healthcare contributes 22%.

M&A activity has increased significantly, with over 18 strategic collaborations recorded between 2022 and 2025. Partnerships between material suppliers and 3D printer manufacturers have improved production efficiency by 28%. Regional investments in the United States account for nearly 100% of total market funding, highlighting strong domestic focus.

New Product

New product development has accelerated, with over 34% of companies launching advanced polyamide materials in 2025. Performance improvements include 25% higher strength and 18% better thermal resistance. Innovations in bio-based polyamides have increased sustainability adoption by 29%.

Recent Development

- 2025: BASF increased production capacity by 18%, reaching 28,000 metric tons annually, improving supply chain efficiency and reducing lead times by 22%.

- 2024: Evonik launched new PA12 materials with 20% higher strength, increasing adoption in aerospace applications by 17%.

- 2023: HP expanded 3D printing facilities, increasing production output by 25% and reducing costs by 15%.

Research Methodology for United States 3D PA-Polyamide Market

The research process involves a combination of primary and secondary data collection methods to ensure accuracy and reliability. Primary research includes interviews with industry experts, manufacturers, and distributors, accounting for over 65% of data inputs. Secondary research involves analysis of company reports, industry publications, and government databases. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring consistency across data points. Statistical modeling and forecasting techniques are applied to project market trends, with validation through cross-referencing multiple sources.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Specialty Chemicals and Industrial Coatings

Myra Irons is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.