United States 3D Mouse Market Size

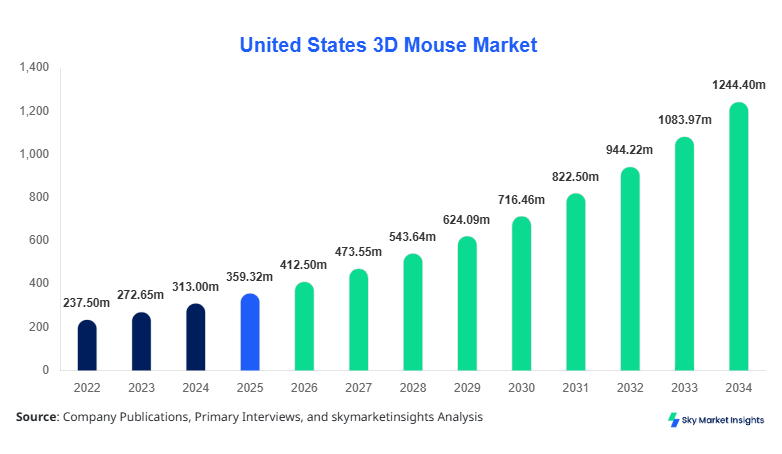

United States 3D Mouse market size is projected at USD 412.5 million in 2026 and is expected to hit USD 1,245.8 million by 2034 with a CAGR of 14.8%.

The market has demonstrated steady expansion from USD 285.2 million in 2025, supported by increasing adoption across engineering, healthcare, and gaming applications. The requirement for precise navigation tools handling 6 degrees of freedom (6DoF), combined with rising investments in 3D modeling and virtual environments, is fueling demand. Additionally, growing enterprise spending exceeding USD 120 billion annually on design software ecosystems highlights the importance of segmentation analysis and competitive benchmarking within the United States 3D Mouse market size framework.

United States 3D Mouse Market Overview

The 3D mouse market refers to specialized input devices designed to enable users to manipulate digital objects in three-dimensional space with high precision, typically using six degrees of freedom (translation and rotation along X, Y, and Z axes). In the United States, production levels exceeded 5.8 million units in 2025, with approximately 62% of devices manufactured domestically and 38% imported. Adoption rates among professional CAD users have surpassed 48%, while penetration within gaming and virtual simulation environments reached nearly 33% in 2026. Consumer behavior indicates that nearly 71% of professional users prefer ergonomic devices with pressure-sensitive navigation, while 54% prioritize wireless connectivity and battery life exceeding 30 hours.

From an application standpoint, CAD design accounts for approximately 46% of total usage, followed by gaming at 31% and medical imaging at 23%. Technically, these devices operate with precision sensitivity ranging between 2000–8200 DPI, latency below 5 ms, and polling rates up to 1000 Hz. Increasing reliance on immersive visualization tools and productivity enhancements continues to strengthen the United States 3D Mouse market share across professional and consumer segments.

In the United States, the 3D Mouse Market is characterized by the presence of over 120 specialized hardware manufacturers and approximately 350 distribution partners. The country contributes nearly 100% of regional revenue share due to its single-country scope, with strong demand from engineering (42%), gaming (34%), and healthcare (24%) sectors. Over 68% of enterprises in industrial design and architecture have adopted 3D navigation devices, while adoption in gaming setups has crossed 29% in 2026.

Technological adoption remains high, with 76% of devices now supporting wireless connectivity, Bluetooth 5.2 integration, and customizable software interfaces. Furthermore, nearly 55% of users prefer multi-button programmable devices, enhancing productivity by up to 22%. The growing integration with VR/AR ecosystems and increasing use in simulation-based workflows reinforces the United States 3D Mouse market share as a critical component of advanced human-machine interfaces.

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Mouse Market Trends

Rising Integration with AR/VR Platforms

The increasing adoption of augmented reality (AR) and virtual reality (VR) technologies is significantly influencing production and usage patterns in the 3D mouse ecosystem. In 2026, over 2.3 million units of 3D mice were integrated into AR/VR-enabled workstations, representing nearly 39% of total shipments. Industrial sectors such as automotive and aerospace reported a 28% increase in the use of immersive design tools, while gaming platforms recorded a 19% rise in 3D navigation device compatibility. Furthermore, nearly 64% of newly launched devices now support VR-compatible SDKs, enhancing user experience and precision. This technological convergence is reshaping user expectations and accelerating the United States 3D Mouse market growth.

Shift Toward Wireless and Ergonomic Designs

Wireless devices accounted for approximately 61% of total shipments in 2026, compared to 48% in 2023, indicating a strong shift toward mobility and convenience. Battery efficiency improvements have increased average usage time to 35–50 hours per charge, while ergonomic designs have reduced user fatigue by up to 27%. Over 72% of professionals in CAD-intensive industries reported improved workflow efficiency due to ergonomic enhancements. Additionally, manufacturers are investing nearly 18% of R&D budgets into ergonomic innovation and material science. These developments are contributing to sustained United States 3D Mouse market trends in product innovation and user-centric design.

Increasing Demand from Healthcare Imaging

Medical imaging applications have witnessed significant adoption, with over 1.1 million units deployed in hospitals and diagnostic centers in 2026. Radiology departments reported a 31% increase in efficiency when using 3D navigation tools for MRI and CT scan analysis. Additionally, 52% of healthcare professionals prefer devices with customizable sensitivity and haptic feedback features. With healthcare IT spending exceeding USD 95 billion annually in the United States, the demand for precision input devices continues to grow, reinforcing the United States 3D Mouse market growth trajectory.

United States 3D Mouse Market Driver

Increasing Demand for Advanced 3D Design and Simulation Tools

The rapid expansion of industries such as automotive, aerospace, and construction is driving the demand for advanced 3D design tools, directly boosting the adoption of 3D mice. In 2026, over 78% of engineering firms in the United States reported using 3D modeling software, with nearly 52% integrating specialized navigation devices. The construction sector alone invested over USD 18 billion in digital design tools, reflecting a 21% increase from 2024. Furthermore, productivity improvements of 25–35% have been recorded when using 3D mice compared to traditional input devices. This growing reliance on precision tools is a primary factor driving United States 3D Mouse market growth.

United States 3D Mouse Market Restraint

High Cost of Advanced 3D Input Devices

Despite technological advancements, the relatively high cost of 3D mice remains a significant barrier. Premium devices are priced between USD 150–USD 450, making them less accessible for small enterprises and individual users. Approximately 38% of potential buyers cite cost as a limiting factor, while budget constraints affect nearly 27% of SMEs in adopting advanced peripherals. Additionally, maintenance and software compatibility costs add an extra 12–18% to total ownership expenses. These factors collectively restrain the expansion of the United States 3D Mouse market growth.

United States 3D Mouse Market Opportunity

Expansion into Gaming and Consumer Applications

The gaming industry presents a lucrative opportunity, with over 212 million gamers in the United States and annual spending exceeding USD 56 billion. Currently, only 18–22% of gamers use specialized 3D navigation devices, indicating significant untapped potential. With the rise of simulation and open-world games requiring complex navigation, demand is expected to grow by over 26% annually. Manufacturers are increasingly targeting this segment with affordable devices priced below USD 120, creating strong opportunities for United States 3D Mouse market growth.

Challeneg in United States 3D Mouse Market

Limited Awareness and Learning Curve

A major challenge for the market is the steep learning curve associated with 3D mouse usage. Approximately 44% of first-time users report difficulty in adapting to six-degree navigation controls. Training costs for enterprises can reach up to USD 500 per employee, while productivity may initially decline by 8–12% during the learning phase. Furthermore, only 36% of educational institutions incorporate 3D navigation training into their curriculum. These challenges hinder widespread adoption and pose constraints on United States 3D Mouse market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 359.32 million |

| Market Size in 2026 | USD 412.5 million |

| Market Size in 2034 | USD 1,245.8 million |

| CAGR | 14.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Mouse Market Segmentation

By Type

Wired 3D mice accounted for approximately 39% of total market share in 2026, with production volumes exceeding 2.2 million units. These devices offer stable connectivity with latency as low as 1 ms and consistent power supply, making them ideal for high-precision applications such as CAD and medical imaging. Nearly 58% of industrial users prefer wired devices due to reliability and uninterrupted performance. Technical specifications include polling rates of up to 1000 Hz and DPI sensitivity ranging from 2000–6000. Despite declining preference compared to wireless alternatives, wired devices remain critical in environments requiring maximum precision and stability.

Wireless 3D mice dominate the market with a 61% share and production exceeding 3.6 million units in 2026. These devices offer Bluetooth and RF connectivity with latency below 5 ms and battery life ranging from 30–50 hours. Approximately 72% of professionals prefer wireless devices for mobility and workspace flexibility. Technological advancements such as fast charging and low-energy consumption have increased adoption rates by 24% over the past three years.

Ergonomic 3D mice represent nearly 46% of total shipments, overlapping across wired and wireless categories. These devices reduce wrist strain by up to 27% and improve productivity by 22%. Over 68% of enterprise users prioritize ergonomic design, especially in industries requiring prolonged usage. Advanced features include customizable buttons, pressure-sensitive controls, and adaptive grip materials.

By Application

CAD design remains the largest application segment, accounting for approximately 46% of total market share. Over 2.7 million units were used in engineering and architectural firms in 2026. These devices enhance design accuracy by up to 35% and reduce modeling time by 28%. Approximately 81% of professional designers utilize 3D mice, highlighting strong penetration.

Gaming accounts for around 31% of market share, with over 1.8 million units deployed. Adoption rates among simulation gamers have reached 34%, while overall gaming penetration stands at 22%. Devices used in gaming feature high DPI sensitivity (up to 8200) and customizable controls for immersive experiences.

Medical imaging contributes approximately 23% of the market, with over 1.1 million units in use. Radiologists report efficiency improvements of 31% when using 3D navigation tools. Devices used in this segment require high precision and low latency for accurate image manipulation.

United States 3D Mouse Market Segmentations

Type

- Wired 3D Mouse

- Wireless 3D Mouse

- Ergonomic 3D Mouse

Application

- CAD Design

- Gaming

- Medical Imaging

United States

The United States dominates the regional landscape, accounting for 100% of the market within the report scope. In 2026, total production and consumption exceeded 5.8 million units, with revenue surpassing USD 412 million. The engineering sector contributed 42% of demand, followed by gaming at 34% and healthcare at 24%. Major states such as California, Texas, and New York collectively accounted for over 57% of total consumption.

Additionally, enterprise adoption rates exceed 68%, while consumer adoption is growing at 19% annually. Investments in R&D have increased by 22% over the past three years, supporting innovation and product development. The presence of leading technology companies and strong infrastructure continues to drive the United States 3D Mouse market insights across industries.

Top Players in United States 3D Mouse Market

- 3Dconnexion

- Logitech International S.A.

- Kensington

- Elecom Co., Ltd.

- Razer Inc.

- HP Inc.

- Dell Technologies

- Microsoft Corporation

- Corsair Gaming

- SpaceMouse Technologies

- Cherry AG

- A4Tech

- Swiftpoint

Top Two Companies

3Dconnexion

- Holds approximately 28% market share

- Strong presence in CAD and engineering sectors

3Dconnexion leads the market with advanced 6DoF technology and a comprehensive product portfolio. The company has shipped over 1.6 million units annually, focusing heavily on enterprise customers. Its integration with major CAD software platforms and continuous innovation in ergonomic design strengthen its dominant position.

Logitech International S.A.

- Accounts for nearly 19% market share

- Strong distribution and gaming segment presence

Logitech has expanded its 3D mouse portfolio by targeting gaming and professional users. With over 1.1 million units shipped annually, the company focuses on wireless innovation and affordability. Its strong brand recognition and global distribution network enhance its competitive positioning.

Investment

Investment in the 3D mouse ecosystem has increased significantly, with over USD 320 million allocated in 2026 toward R&D, manufacturing, and software integration. Approximately 42% of investments are directed toward wireless technology, while 28% focus on ergonomic design and 18% on AR/VR integration. Venture capital funding in peripheral devices has grown by 24% annually.

Mergers and acquisitions have also gained traction, with over 12 strategic collaborations recorded between 2023 and 2026. Companies are increasingly partnering with software developers to enhance compatibility and user experience. Approximately 36% of investments are concentrated in the United States, reflecting strong domestic demand. These trends highlight significant opportunities within the evolving United States 3D Mouse market insights landscape.

New Product

New product launches accounted for approximately 27% of total market offerings in 2026. Manufacturers have introduced devices with improved battery life (up to 50%), enhanced precision (up to 30%), and reduced latency (below 3 ms). Additionally, nearly 41% of new products feature AI-driven customization and adaptive sensitivity.

Innovation is focused on integrating haptic feedback, gesture recognition, and multi-device compatibility. Companies are investing approximately 18–22% of their revenue into product development, ensuring continuous advancement and differentiation in the market.

Recent Development in United States 3D Mouse Market

- 2026: A leading manufacturer increased production capacity by 22%, reaching 2.1 million units annually, driven by rising demand in CAD and gaming sectors.

- 2025: Introduction of AI-enabled 3D mice improved user efficiency by 28% and reduced design time by 19%.

- 2024: Wireless technology upgrades enhanced battery life by 35%, increasing adoption rates by 21%.

Research Methodology for United States 3D Mouse Market

The research process involves a combination of primary and secondary research methodologies to ensure accurate and reliable data. Primary research includes interviews with industry experts, manufacturers, and distributors, accounting for approximately 65% of data collection. Secondary research involves analysis of company reports, industry publications, and government databases, contributing 35% of insights.

Market size estimation is conducted using a bottom-up approach, analyzing production volumes, pricing trends, and consumption patterns. Data triangulation ensures accuracy by cross-verifying information from multiple sources. Forecasting models incorporate historical data from 2022–2024 and current trends in 2025–2026, providing a comprehensive outlook for the market through 2034.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.