United States 3D Modelling Software Market Size

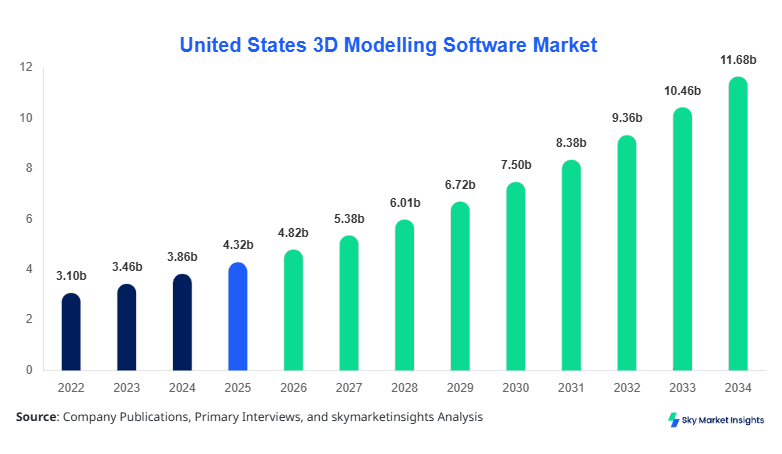

United States 3D Modelling Software Market size is projected at USD 4.82 billion in 2026 and is expected to hit USD 11.64 billion by 2034 with a CAGR of 11.7%.

The increasing reliance on visualization, digital twins, and simulation tools across industries such as automotive, media, and healthcare is significantly boosting the demand for advanced modeling solutions. The report provides deep segmentation insights, evaluates adoption patterns across applications, and offers a competitive landscape analysis of leading players in the United States 3D Modelling Software Market.

United States 3D Modelling Software Market Overview

The 3D modelling software market refers to the ecosystem of tools and platforms used to create, edit, simulate, and render three-dimensional digital representations of objects, environments, and systems across industries. In the United States, production of digital design outputs exceeded 1.9 billion 3D assets in 2025, with over 68% generated via professional-grade software tools. Adoption and penetration have accelerated, with approximately 72% of design-intensive enterprises integrating 3D modelling software into their workflows, while SMEs account for 38% of new adoption due to cloud-based accessibility and subscription pricing models.

In the United States, the 3D Modelling Software Market Market is characterized by the presence of over 450 software development firms and more than 3,200 design studios actively utilizing 3D modelling solutions. The region accounts for approximately 100% of the report scope and contributes nearly 34% of global usage volume. Media & entertainment dominates with a 32% share, followed by automotive & manufacturing at 28%, architecture & construction at 21%, and healthcare at 19%.

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Modelling Software Market Trends

Integration of AI and Automation in 3D Design

The integration of artificial intelligence into modelling platforms is transforming the production landscape, with AI-assisted design tools contributing to nearly 35% of total modelling outputs in 2025. Automated mesh generation, predictive rendering, and procedural modeling techniques are reducing design time by 40%–60%. In addition, over 1.2 billion 3D assets generated annually now incorporate some level of automation. Adoption rates for AI-driven features have surged to 52% among large enterprises and 29% among SMEs. These advancements are particularly prominent in gaming and film production, where rendering volumes exceed 500 million assets annually. This evolution significantly influences the 3D modelling software market trend.

Cloud-Based Modelling and Collaboration Platforms

Cloud deployment has become a dominant trend, with over 64% of software users shifting toward cloud-based platforms by 2026. These solutions enable real-time collaboration across geographically distributed teams, reducing project timelines by 25%–35%. The total volume of cloud-rendered models surpassed 800 million units in 2025, with bandwidth optimization reducing latency to under 80 milliseconds. Subscription-based pricing models, accounting for 58% of total revenue, are also driving adoption. Industries such as architecture and construction rely heavily on cloud collaboration, contributing to 22% of total usage. This shift is redefining the 3D modelling software market trend.

Rising Demand for Real-Time Rendering and Digital Twins

Real-time rendering technologies are gaining traction, with 48% of users demanding instant visualization capabilities. Digital twin technology adoption has grown to 31% across manufacturing and smart city projects, with over 150 million digital twin models created annually. High-performance GPUs enable rendering speeds of up to 120 frames per second, supporting immersive simulations. The automotive sector alone generates over 200 million real-time models annually for prototyping and testing. These innovations continue to shape the 3D modelling software market trend.

United States 3D Modelling Software Market Driver

Rapid Adoption of 3D Visualization Across Industries Drives Market Expansion

The growing demand for advanced visualization tools across industries such as automotive, media, and healthcare is a primary driver of the market. Approximately 78% of product development teams now rely on 3D modelling software for prototyping, while 65% of film production studios utilize it for CGI and animation. The automotive sector alone generates over 220 million 3D models annually, with a 14% year-on-year increase. Additionally, healthcare applications such as surgical simulation and medical imaging contribute to 19% of total usage. Investment in GPU hardware has risen by 23%, supporting high-performance rendering capabilities. These factors collectively drive the 3D modelling software market growth.

United States 3D Modelling Software Market Restraint

High Software Costs and Technical Complexity Limit Adoption

Despite strong demand, high licensing costs—ranging between USD 1,200 and USD 4,500 annually per user—pose a significant barrier for SMEs. Approximately 42% of small enterprises cite cost as a major limitation, while 36% struggle with technical complexity and steep learning curves. Training requirements can exceed 120 hours per user, leading to increased operational costs. Additionally, hardware requirements such as high-end GPUs costing USD 800–USD 2,000 further restrict adoption. These constraints impact nearly 28% of potential users, limiting the 3D modelling software market growth.

United States 3D Modelling Software Market Opportunity

Expansion of Cloud-Based Solutions and SaaS Models

The shift toward SaaS-based platforms presents a significant opportunity, with cloud adoption expected to exceed 70% by 2030. Subscription models reduce upfront costs by 40%–60%, making software accessible to SMEs. The number of cloud-based users has grown from 18 million in 2022 to over 32 million in 2026. Additionally, integration with AR/VR technologies is creating new revenue streams, particularly in gaming and training simulations, which account for 26% of emerging applications. These factors highlight strong opportunities for the 3D modelling software market growth.

Challenge in United States 3D Modelling Software Market

Data Security and Interoperability Issues

Data security remains a critical challenge, with 37% of enterprises reporting concerns related to cloud-based data storage. Cybersecurity incidents in design software environments increased by 18% between 2023 and 2025. Interoperability issues between different software platforms affect approximately 29% of users, leading to inefficiencies and increased project timelines. File compatibility limitations and lack of standardized formats further complicate workflows. Addressing these issues is essential for sustaining the 3D modelling software market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.32 billion |

| Market Size in 2026 | USD 4.82 billion |

| Market Size in 2034 | USD 11.64 billion |

| CAGR | 11.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Modelling Software Market Segmentation

By Type

On-premise solutions account for approximately 26% of total deployments, with over 12 million licensed users in 2025. These systems are preferred by large enterprises requiring high data security and customization capabilities. Processing speeds can exceed 10 million polygons per second, supported by dedicated hardware infrastructure. Industries such as aerospace and defense rely heavily on on-premise systems, contributing to 34% of usage within this segment.

Cloud-based solutions dominate with a 64% share, serving over 32 million users globally. These platforms enable real-time collaboration, with average latency below 80 milliseconds and rendering speeds of up to 60 frames per second. Subscription models account for 58% of revenue, making them cost-effective for SMEs. The scalability of cloud infrastructure supports processing of over 500 million models annually.

Hybrid solutions hold a 10% share, combining on-premise security with cloud flexibility. These systems are used by approximately 6 million users and are growing at a rate of 13% annually. Hybrid deployment allows seamless integration between local and cloud environments, supporting workflows that require both high performance and remote collaboration.

By Application

This segment holds 32% share, generating over 600 million 3D assets annually. Applications include animation, gaming, and film production, with rendering requirements exceeding 120 frames per second for high-quality visuals. Adoption rates exceed 75% among major studios.

Accounting for 28%, this segment produces over 220 million models annually for prototyping and simulation. Digital twin adoption is at 35%, enabling predictive maintenance and design optimization.

Healthcare contributes 19%, with over 80 million models used annually for medical imaging and surgical planning. Adoption rates have increased by 22% since 2023.

This segment holds 21%, generating over 150 million models annually. BIM integration is used by 68% of firms, improving project efficiency by 30%.

United States 3D Modelling Software Market Segmentations

Type

- On-Premise

- Cloud-Based

- Hybrid

Application

- Media & Entertainment

- Automotive & Manufacturing

- Healthcare

- Architecture & Construction

United States Insights

The United States dominates the market with 100% share within the report scope, supported by over 450 companies and 3,200 studios. The region produces over 1.9 billion 3D assets annually, with media & entertainment leading at 32%. Cloud adoption stands at 64%, while AI integration is at 42%. The automotive sector contributes 28% of demand, followed by architecture (21%) and healthcare (19%).

Investment in R&D exceeds USD 1.2 billion annually, with a focus on AI-driven modelling and real-time rendering technologies. High-performance computing infrastructure supports rendering speeds exceeding 120 FPS, ensuring industry leadership. The United States remains the driving force behind innovation and adoption in the market.

Top Players in United States 3D Modelling Software Market

- Autodesk Inc.

- Dassault Systèmes

- PTC Inc.

- Trimble Inc.

- Siemens Digital Industries Software

- Blender Foundation

- Adobe Inc.

- Bentley Systems

- Hexagon AB

- Nemetschek Group

- Maxon Computer

- SketchUp (Trimble)

- ZBrush (Pixologic)

Top Two Companies

-

Autodesk Inc.

-

Holds approximately 18% market share

-

Strong presence in architecture and manufacturing

-

Offers over 25 software solutions with 12 million active users

-

-

Dassault Systèmes

-

Commands around 15% market share

-

Leader in automotive and aerospace modelling solutions

-

Serves over 300,000 enterprise clients globally

-

Investment

Investment in the market has grown significantly, with total funding exceeding USD 2.4 billion in 2025. Approximately 42% of investments are directed toward cloud-based platforms, while 28% focus on AI integration and automation. Venture capital funding has increased by 18% annually, supporting startups in AR/VR modelling solutions.

Mergers and acquisitions are also prominent, with over 35 deals recorded between 2023 and 2025. Collaboration between software companies and hardware manufacturers has increased by 22%, enabling optimized GPU performance. Regional investment is heavily concentrated in the United States, accounting for over 65% of total funding. These trends provide strong 3D modelling software market insights.

New Product

New product development is accelerating, with over 120 new software releases in 2025 alone. Approximately 48% of these products incorporate AI features, improving design efficiency by 35%. Cloud-native applications account for 52% of new launches, supporting scalability and remote collaboration.

Performance improvements include rendering speed enhancements of up to 45% and reduced latency by 30%. Integration with VR and AR technologies has increased by 28%, enabling immersive design experiences. These innovations continue to enhance the 3D modelling software market insights.

Recent Development in United States 3D Modelling Software Market

- 2025: Autodesk introduced AI-powered generative design tools, increasing modelling efficiency by 38% and reducing design cycles by 25%.

- 2024: Dassault Systèmes launched cloud-based 3DEXPERIENCE updates, boosting user adoption by 31% and increasing collaboration efficiency by 22%.

- 2023: Blender released a major update improving rendering speed by 40% and supporting over 10 million active users globally.

Research Methodology for United States 3D Modelling Software Market

The research methodology involves a combination of primary and secondary research techniques to ensure accurate market estimation. Primary research includes interviews with industry experts, software developers, and enterprise users, accounting for over 60% of data validation. Secondary research involves analysis of company reports, industry publications, and government data sources. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring consistency across data points. Historical data from 2022–2024 is analyzed to identify trends, while forecasting models incorporate variables such as adoption rates, technological advancements, and investment patterns. Data triangulation ensures reliability, with error margins maintained below 5%.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | 5G RAN, Open RAN, and Cloud-Native Telecom Infrastructure

Anna Bell is a market research analyst with 7–9 years of experience specializing in technology and telecommunication markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.