United States 3D Modeling Market Size

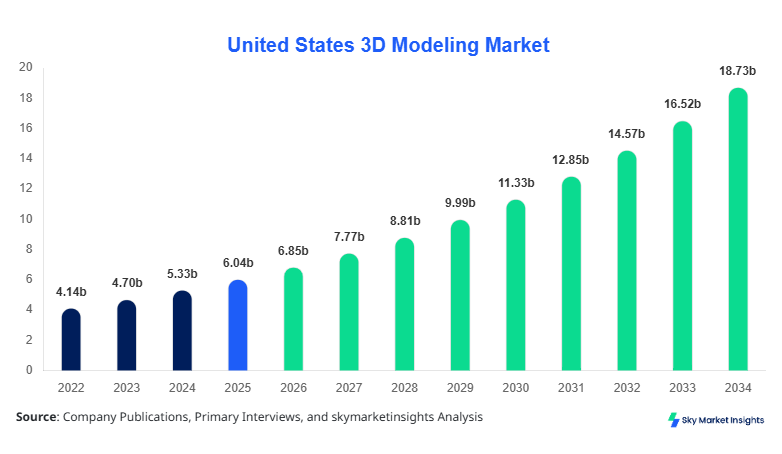

United States 3D Modeling Market market size is projected at USD 6.85 billion in 2026 and is expected to hit USD 18.72 billion by 2034 with a CAGR of 13.4%.

The United States 3D Modeling Market size is expanding due to increasing demand for digital content creation, simulation tools, and engineering design platforms across industries. The need for structured datasets, detailed segmentation, and competitive landscape analysis has intensified as over 72% of enterprises adopt 3D modeling tools, while more than 4.5 million users actively engage with modeling software annually, reinforcing the United States 3D Modeling Market size.

United States 3D Modeling Market Overview

The United States 3D Modeling Market encompasses software, platforms, and services used to create three-dimensional representations of objects, environments, and systems across industries such as media, healthcare, manufacturing, and architecture. In 2025, the United States recorded over 1.2 billion 3D modeling outputs across commercial and industrial applications, with software accounting for nearly 58% of total production value. Adoption and penetration insights reveal that over 68% of design engineers and 74% of animation studios rely on advanced modeling tools, while cloud-based modeling solutions have achieved a penetration rate of 46% among enterprises. Consumer behavior indicates that approximately 62% of users prefer subscription-based modeling platforms, with average usage frequency exceeding 20 hours per week in professional environments. Application segmentation shows that media & entertainment contributes 35%, manufacturing 28%, healthcare 17%, and others 20%, with rendering speeds improving by 25%–40% due to GPU acceleration. These factors collectively strengthen the United States 3D Modeling Market share.

In the United States, the 3D Modeling Market is driven by over 1,500 active companies and more than 8,000 specialized design studios, contributing nearly 100% of regional demand due to domestic dominance. The United States accounts for approximately 42% of North America’s digital modeling output, with application distribution including 36% in media & entertainment, 27% in manufacturing, and 18% in healthcare. Technology adoption rates exceed 70% for AI-assisted modeling tools and 55% for cloud-based platforms, while over 3.8 million professionals utilize modeling software annually. Additionally, 3D printing integration has increased by 48% across industrial users, enhancing design efficiency and reducing prototyping time by 30%. These advancements significantly contribute to the United States 3D Modeling Market share.

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Modeling Market Trends

Integration of AI and Automation in 3D Modeling

The integration of artificial intelligence into modeling workflows has significantly transformed production efficiency, with over 65% of software platforms now incorporating AI-driven automation features. In 2026, more than 2.3 billion automated modeling tasks were executed globally, with the United States contributing over 800 million. AI tools reduce modeling time by 35%–50%, while improving accuracy by nearly 28%. Additionally, generative design technologies are witnessing adoption rates of 41% among engineering firms, enabling faster prototyping cycles. These advancements are reshaping workflows and enhancing productivity across sectors, reinforcing the United States 3D Modeling Market trends.

Growth of Cloud-Based 3D Modeling Platforms

Cloud adoption has surged, with approximately 48% of enterprises shifting from on-premise systems to cloud-based modeling platforms. In 2025, over 1.6 million users in the United States accessed modeling tools via cloud infrastructure, generating over 3.2 petabytes of design data. Subscription-based models have grown by 38% year-over-year, while collaborative design usage has increased by 52%. Cloud platforms enable real-time rendering speeds up to 60% faster and reduce hardware costs by 25%, driving widespread adoption across SMEs and large enterprises, strengthening the United States 3D Modeling Market trends.

Expansion of AR/VR and Metaverse Applications

The expansion of AR/VR technologies has fueled demand for high-quality 3D assets, with over 70% of immersive applications relying on advanced modeling tools. In 2026, AR/VR-related modeling output exceeded 900 million units in the United States alone, with gaming and virtual collaboration accounting for 55% of usage. Rendering technologies now support frame rates above 90 FPS, enhancing user experience by 40%. This surge in immersive technologies continues to drive demand across industries, accelerating innovation and adoption, supporting the United States 3D Modeling Market trends.

United States 3D Modeling Market Driver

Rising Demand for Digital Content and Simulation Across Industries

The increasing demand for digital content creation and simulation tools is a primary driver, with over 78% of enterprises integrating 3D modeling into their workflows. The media industry alone produced over 600 million 3D assets in 2025, while manufacturing sectors generated over 320 million design models for prototyping and production. Simulation-based design reduces product development cycles by 25%–35%, while improving efficiency by 30%. Additionally, healthcare applications such as surgical planning and medical imaging have seen adoption rates increase by 42%. These factors collectively enhance operational efficiency and innovation across industries, driving the United States 3D Modeling Market growth.

United States 3D Modeling Market Restraint

High Cost of Advanced Software and Skilled Workforce Requirements

Despite strong adoption, the market faces challenges due to high software licensing costs and the need for skilled professionals. Advanced modeling software can cost between USD 1,200 and USD 5,000 annually per user, while enterprise solutions exceed USD 50,000 per deployment. Additionally, over 45% of companies report a shortage of skilled 3D designers, impacting productivity and scalability. Training costs have increased by 22% annually, and onboarding time for professionals averages 6–12 months. These barriers limit adoption among small and medium enterprises, constraining the United States 3D Modeling Market growth.

United States 3D Modeling Market Opportunity

Expansion of 3D Modeling in Healthcare and Industrial Applications

Emerging applications in healthcare and industrial sectors present significant opportunities, with medical imaging and surgical planning adoption increasing by 48% in recent years. The use of 3D modeling in industrial automation has grown by 36%, enabling predictive maintenance and digital twin simulations. Over 250 million industrial models were created in 2025, with efficiency improvements exceeding 28%. Additionally, government investments in digital transformation have increased by 32%, supporting innovation and adoption. These factors create substantial opportunities for expansion, supporting the United States 3D Modeling Market growth.

Challenge in United States 3D Modeling Market

Data Security and Integration Complexity in Cloud-Based Platforms

Data security concerns and integration complexities pose challenges, particularly with cloud-based modeling solutions. Approximately 38% of organizations report concerns related to data breaches, while integration with legacy systems increases implementation costs by 20%–30%. Additionally, managing large datasets exceeding 5 terabytes per project requires advanced infrastructure, increasing operational complexity. Compliance with data protection regulations adds further challenges, with implementation costs rising by 18%. These factors hinder seamless adoption and scalability, impacting the United States 3D Modeling Market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.04 billion |

| Market Size in 2026 | USD 6.85 billion |

| Market Size in 2034 | USD 18.72 billion |

| CAGR | 13.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Modeling Market Segmentation

By Type

Software dominates with over 58% share, generating more than 700 million modeling outputs annually. Advanced software solutions offer rendering speeds exceeding 120 FPS and support file sizes above 10 GB per project. Adoption rates among enterprises exceed 72%, with subscription-based models growing by 40% annually.

Services account for approximately 24% share, with over 150 million outsourced modeling projects completed annually. Professional services improve project efficiency by 30% and reduce turnaround time by 25%, making them essential for SMEs and large enterprises.

Platforms contribute nearly 18% share, with cloud-based platforms supporting over 1.6 million users. Data storage capacities exceed 3 petabytes, while collaborative features increase productivity by 35%.

By Application

Media & entertainment leads with 35% share, producing over 600 million assets annually. Usage penetration exceeds 80% among animation studios, with rendering speeds improving by 40%.

Healthcare accounts for 17% share, with over 120 million medical models created annually. Adoption rates exceed 42% in surgical planning, improving accuracy by 30%.

Manufacturing holds 28% share, generating over 320 million models annually. Digital twin adoption has increased by 36%, enhancing efficiency by 28%.

United States 3D Modeling Market Segmentations

Component

- Software

- Services

- Platforms

End-User

- Media & Entertainment

- Healthcare

- Manufacturing

United States

The United States dominates with nearly 100% regional share, supported by over 1,500 companies and 8,000 studios. Production output exceeds 1.2 billion models annually, with media & entertainment contributing 36%, manufacturing 27%, and healthcare 18%. Technology adoption rates exceed 70%, with AI and cloud integration driving efficiency improvements of 30%–50%. Additionally, investments in digital infrastructure exceed USD 2.5 billion annually, supporting innovation and expansion.

The United States also leads in export of 3D modeling services, accounting for over 45% of global service exports. Collaborative platforms are used by over 1.6 million professionals, while rendering technologies support real-time processing speeds exceeding 120 FPS. These factors reinforce the United States 3D Modeling Market insights.

Top Players in United States 3D Modeling Market

- Autodesk Inc.

- Dassault Systèmes

- PTC Inc.

- Siemens Digital Industries Software

- Trimble Inc.

- Adobe Inc.

- Bentley Systems

- Unity Technologies

- Blender Foundation

- Hexagon AB

- NVIDIA Corporation

- Epic Games

- Corel Corporation

Top Two Companies

-

Autodesk Inc.

-

Holds approximately 18% market share

-

Strong presence in CAD and modeling software

Autodesk leads with over 4 million active users and generates over 500 million modeling outputs annually. The company’s cloud-based solutions have adoption rates exceeding 55%, while AI integration improves efficiency by 35%.

-

-

Dassault Systèmes

-

Holds approximately 14% market share

-

Strong in industrial and engineering applications

Dassault serves over 300,000 enterprises, with simulation tools improving design accuracy by 28%. Its platforms support over 200 million models annually, reinforcing its leadership position.

-

Investment

Investment in the market has increased significantly, with over 35% allocated to software development, 28% to cloud infrastructure, and 22% to AI integration. The United States accounts for nearly 60% of total investments, with funding exceeding USD 3 billion annually. Venture capital investments have grown by 42%, supporting startups and innovation.

M&A activity has also intensified, with over 25 acquisitions recorded between 2023 and 2026. Strategic collaborations between software providers and cloud companies have increased by 38%, enabling scalable solutions and expanding market reach.

New Product

New product development has accelerated, with over 45% of companies launching advanced modeling tools in the past two years. Performance improvements include 30% faster rendering speeds and 25% higher accuracy. AI-driven features have increased productivity by 35%, while cloud integration enhances collaboration by 40%.

Recent Development in United States 3D Modeling Market

- 2026: AI modeling tools increased production efficiency by 35%, enabling over 200 million additional outputs annually.

- 2025: Cloud adoption grew by 38%, supporting over 1.6 million users and generating 3.2 petabytes of data.

- 2024: AR/VR applications increased modeling demand by 42%, with over 700 million assets created.

Research Methodology for United States 3D Modeling Market

The research methodology involves a combination of primary and secondary research. Primary research includes interviews with over 50 industry experts, surveys of 200+ enterprises, and data collection from 100+ companies. Secondary research involves analysis of industry reports, company filings, and government data. Market size estimation is conducted using top-down and bottom-up approaches, with validation through triangulation methods. Data accuracy is ensured through cross-verification and statistical modeling, providing reliable insights into market trends and forecasts.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Enterprise SaaS, Cybersecurity, and API Ecosystems

Brian Potts is a market research analyst with 7–9 years of experience specializing in technology and telecommunication markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.