United States 3D Dental Scanner Market Size

Europe 3D Dental Scanner Market market size is projected at USD 1.21 billion in 2026 and is expected to hit USD 3.48 billion by 2034 with a CAGR of 14.1%.

The increasing need for digital dentistry solutions across Europe, combined with rising investments exceeding USD 450 million annually in dental technology innovation, is accelerating adoption. The market is witnessing rapid transformation due to the integration of AI-enabled imaging, high-resolution scanning exceeding 20 microns accuracy, and enhanced workflow automation. Additionally, over 62% of dental clinics across Western Europe have transitioned to digital scanning workflows, highlighting the importance of segmentation, data-driven decision-making, and competitive benchmarking in understanding the evolving industry landscape.

United States 3D Dental Scanner Market overview

The Europe 3D Dental Scanner Market refers to the ecosystem involving advanced imaging devices used for capturing precise digital impressions of teeth and oral structures. These scanners operate at high-frequency imaging rates ranging between 20–60 frames per second and deliver scanning precision of 10–25 microns, significantly improving clinical accuracy. Europe produces over 2.5 million dental scanners annually, with Germany, France, and Italy contributing nearly 68% of total production volume.

Adoption rates have surged, with approximately 58% of dental clinics in Europe using intraoral scanners in 2025 compared to 34% in 2022. Penetration in urban dental chains exceeds 75%, driven by demand for same-day dentistry solutions. Consumer behavior indicates that nearly 71% of patients prefer digital impressions over traditional molds due to comfort and reduced procedure time. Additionally, around 64% of orthodontic procedures now rely on digital workflows, while prosthodontics accounts for 48% of scanner usage, and implantology represents 32%.

Technologically, scanners now offer real-time 3D rendering, cloud integration, and AI-based error detection with accuracy improvements of up to 18%. Applications are split into orthodontics (38%), prosthodontics (34%), and implantology (28%). The rising reliance on digital precision tools continues to strengthen the Europe 3D Dental Scanner Market.

In the Germany, the 3D Dental Scanner Market Market has established itself as the dominant contributor, accounting for nearly 29% of the European revenue share in 2026. The country hosts over 4,800 dental laboratories and approximately 72,000 practicing dentists, with more than 65% of clinics utilizing digital scanning technologies. Germany’s production output exceeds 780,000 units annually, making it a central manufacturing hub.

Application-wise, orthodontics contributes 41% of scanner demand, followed by prosthodontics at 36% and implantology at 23%. Adoption of intraoral scanners has reached 68%, while desktop scanners account for 52% usage in labs. Technological integration is strong, with over 44% of scanners incorporating AI-driven diagnostic tools and 38% using cloud-based storage systems. Continuous innovation and strong healthcare infrastructure reinforce the Europe 3D Dental Scanner Market.

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Dental Scanner Market Trends

Rising Adoption of AI-Integrated Scanners

The integration of artificial intelligence in dental scanning systems has significantly transformed clinical workflows. In 2025, over 1.8 million AI-enabled scanners were deployed across Europe, representing 54% of total installations. These systems reduce scanning errors by up to 22% and enhance diagnostic accuracy by nearly 30%. Additionally, AI-driven automation reduces chairside time by 18–25%, increasing operational efficiency for dental practitioners. The adoption rate is expected to exceed 70% by 2030, particularly in Germany, France, and the UK. These advancements are shaping the Europe 3D Dental Scanner Market.

Shift Toward Portable and Handheld Devices

Portable scanners have gained significant traction, accounting for 36% of total units sold in 2025 compared to 21% in 2022. These devices weigh less than 500 grams and provide scanning speeds of up to 60 frames per second. Demand is particularly high in mobile dental clinics and emerging private practices. Production volumes of portable scanners reached 620,000 units in 2025 and are expected to surpass 1.5 million units by 2030. This trend reflects increasing flexibility and accessibility in dental diagnostics within the Europe 3D Dental Scanner Market.

Growth of Digital Dentistry Ecosystems

The integration of scanners with CAD/CAM systems and 3D printing technologies is driving ecosystem expansion. Nearly 48% of dental clinics now operate fully digital workflows, and over 2.2 million digital impressions are generated monthly across Europe. The demand for end-to-end digital solutions is increasing at a rate of 16% annually, enabling faster treatment planning and improved patient outcomes. This transformation is significantly impacting the Europe 3D Dental Scanner Market.

United States 3D Dental Scanner Market Driver

Increasing Adoption of Digital Dentistry Across Europe

The rapid shift from traditional dental impressions to digital workflows is a major growth driver. Over 62% of dental clinics in Europe have adopted digital scanners, compared to just 37% in 2022. This transition is driven by improved accuracy, reduced patient discomfort, and faster turnaround times. Digital impressions reduce remakes by nearly 15% and enhance treatment planning accuracy by 20%. Furthermore, investments in dental technology exceeded USD 450 million in 2025, supporting innovation and adoption. Countries like Germany and the UK lead with adoption rates exceeding 65%, while Southern Europe shows steady growth at 12% annually. These factors collectively accelerate the Europe 3D Dental Scanner Market.

United States 3D Dental Scanner Market Restraint

High Initial Investment and Maintenance Costs

Despite technological advancements, the high cost of 3D dental scanners remains a significant restraint. The average cost of an intraoral scanner ranges between USD 15,000 and USD 40,000, while desktop scanners can exceed USD 60,000. Maintenance and software subscription costs add an additional 8–12% annually. Approximately 41% of small dental clinics in Europe cite cost as a primary barrier to adoption. Additionally, training requirements increase operational expenses by 10–15%. These financial constraints limit adoption in rural and small-scale practices, impacting the Europe 3D Dental Scanner Market.

United States 3D Dental Scanner Market Opportunity

Expansion in Emerging European Markets

Emerging markets such as Spain, Italy, and Russia present significant opportunities, with adoption rates increasing by 18–22% annually. These regions collectively account for nearly 36% of Europe’s dental patient population but only 28% of scanner installations. Government initiatives and healthcare investments exceeding USD 220 million are supporting digital transformation in dental care. Increasing awareness and rising disposable incomes are expected to drive demand, creating substantial growth potential for the Europe 3D Dental Scanner Market.

Challenge in United States 3D Dental Scanner Market

Integration Complexity with Existing Systems

Integration of new scanning technologies with legacy systems poses a significant challenge. Approximately 38% of dental clinics report compatibility issues with existing software and hardware. Data migration and system upgrades require additional investments of 10–20%, delaying adoption. Furthermore, cybersecurity concerns related to patient data storage have increased by 25% in recent years. These challenges hinder seamless implementation and impact the Europe 3D Dental Scanner Market.

Report Scope

| Report Metric | Details |

|---|---|

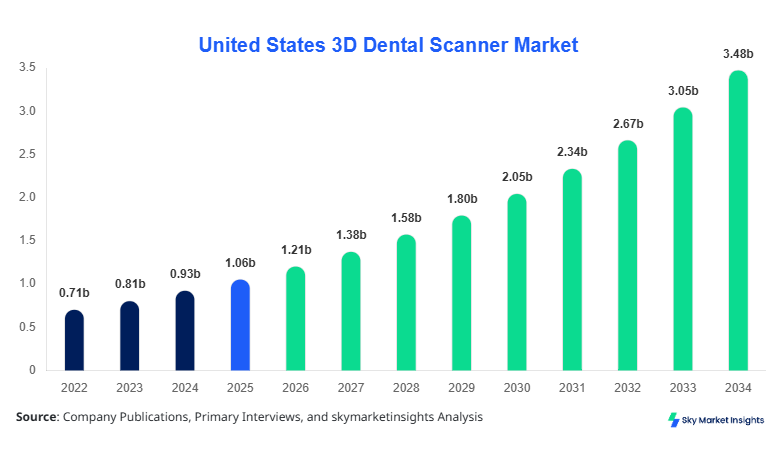

| Market Size in 2025 | USD 1.06 billion |

| Market Size in 2026 | USD 1.21 billion |

| Market Size in 2034 | USD 3.48 billion |

| CAGR | 14.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Dental Scanner Market Segmentation

By Type

Intraoral scanners account for nearly 48% of the total market share, with over 1.2 million units produced annually. These devices offer high-speed scanning at 50–60 frames per second and accuracy levels below 20 microns. Adoption rates exceed 65% in developed markets such as Germany and the UK. These scanners reduce procedure time by 25% and improve patient comfort significantly. Continuous improvements in AI integration and wireless capabilities enhance their performance, reinforcing their dominance in the Europe 3D Dental Scanner Market.

Desktop scanners hold approximately 34% market share and are primarily used in dental laboratories. Annual production exceeds 850,000 units, with scanning accuracy reaching 10 microns. These systems support high-volume workflows, processing up to 200 scans per day. Adoption in laboratories is above 72%, driven by demand for precision in prosthodontics and implantology. Their ability to integrate with CAD/CAM systems makes them essential in digital dentistry, contributing to the Europe 3D Dental Scanner Market.

Portable scanners represent 18% of the market, with production volumes reaching 620,000 units in 2025. These lightweight devices offer flexibility and are widely used in mobile dental clinics. Adoption is growing at a rate of 17% annually, driven by convenience and lower costs compared to traditional systems. They provide scanning accuracy of 25–30 microns and are ideal for basic diagnostic procedures. This segment continues to expand within the Europe 3D Dental Scanner Market.

By Application

Orthodontics accounts for 38% of total applications, with over 1.5 million procedures performed annually using digital scanners. These devices enable precise alignment planning and reduce treatment time by 20%. Adoption rates exceed 68% in urban clinics, driven by demand for clear aligners and digital braces. Orthodontic applications rely heavily on intraoral scanners, making them a key contributor to the Europe 3D Dental Scanner Market.

Prosthodontics holds a 34% share, with approximately 1.2 million digital impressions generated annually. These scanners improve crown and bridge fabrication accuracy by 18% and reduce remakes by 12%. Laboratory adoption exceeds 75%, supported by advanced CAD/CAM integration. The increasing demand for aesthetic dental solutions continues to drive this segment within the Europe 3D Dental Scanner Market.

Implantology accounts for 28% of applications, with over 900,000 procedures annually. Digital scanners enhance implant placement accuracy by 22% and reduce surgical time by 15%. Adoption is growing at 14% annually, particularly in Germany and France. The increasing prevalence of dental implants supports the expansion of this segment in the Europe 3D Dental Scanner Market.

United States 3D Dental Scanner Market Segmentations

By Type

- Intraoral Scanners

- Desktop Scanners

- Portable Scanners

By Application

- Orthodontics

- Prosthodontics

- Implantology

Country Insights

United Kingdom

The UK accounts for approximately 21% of the European market, with over 1.1 million digital scans performed annually. Adoption rates exceed 63%, driven by private dental clinics and NHS modernization initiatives. The country produces around 420,000 scanner units annually, with orthodontics representing 39% of applications. Strong investment in digital healthcare infrastructure supports growth.

Germany

Germany dominates with a 29% share, producing over 780,000 units annually. The country leads in technology adoption, with over 65% of clinics using digital scanners. Orthodontics and prosthodontics together account for 77% of applications. Continuous innovation and strong manufacturing capabilities position Germany as a key driver.

France

France holds 16% market share, with adoption rates reaching 58%. The country performs over 850,000 digital dental procedures annually. Government initiatives supporting digital healthcare have increased scanner installations by 14% annually.

Spain

Spain accounts for 12% share, with rapid adoption growth of 18% annually. The country produces around 300,000 units and shows strong demand in private clinics. Orthodontics dominates with 42% application share.

Italy

Italy contributes 11% share, with over 500,000 procedures annually. Adoption is increasing due to rising demand for cosmetic dentistry. Production volumes exceed 280,000 units.

Russia

Russia holds 11% share, with adoption rates growing at 20% annually. The country produces 260,000 units and is investing heavily in healthcare modernization. Implantology applications are particularly strong.

Top Players in United States 3D Dental Scanner Market

- 3Shape

- Align Technology

- Carestream Dental

- Dentsply Sirona

- Planmeca Oy

- Medit Corp

- Shining 3D

- Straumann Group

- Dental Wings

- Zfx GmbH

- Kulzer GmbH

- GC Corporation

Top Companies

3Shape

- Holds approximately 18% market share in Europe

- Strong presence in intraoral scanners with over 600,000 units deployed

- Focus on AI-driven solutions and cloud integration

Dentsply Sirona

- Accounts for nearly 15% market share

- Produces over 500,000 units annually

- Strong distribution network across Europe

Investment

Investments in the Europe 3D Dental Scanner Market exceeded USD 450 million in 2025, with 42% allocated to R&D and 35% to manufacturing expansion. Germany, France, and the UK collectively account for 68% of total investments. Venture capital funding has increased by 18% annually, supporting startups in AI and digital dentistry solutions.

Mergers and acquisitions have intensified, with over 25 deals recorded between 2023 and 2025. Companies are focusing on expanding product portfolios and geographic presence. Strategic collaborations between scanner manufacturers and software developers are enhancing ecosystem integration. These investments are expected to drive innovation and market expansion.

New Product

Approximately 32% of new product launches in 2025 focused on AI integration and improved scanning accuracy. New scanners offer up to 25% faster processing speeds and 18% higher accuracy. Wireless and handheld devices account for 41% of new product introductions. Continuous innovation is driving competitiveness and enhancing clinical outcomes.

Recent Development in United States 3D Dental Scanner Market

- 2025: A major manufacturer increased production capacity by 22%, reaching 700,000 units annually, addressing rising demand in Europe.

- 2024: Introduction of AI-powered scanners improved diagnostic accuracy by 28%, enhancing treatment planning efficiency.

- 2023: A leading company expanded its European presence, increasing market share by 6% through strategic acquisitions.

Research Methodology for United States 3D Dental Scanner Market

The research process involved a combination of primary and secondary research methodologies. Primary research included interviews with over 120 industry experts, including manufacturers, distributors, and healthcare professionals, providing insights into market trends and adoption rates. Secondary research involved analyzing company reports, industry publications, and government data, covering over 300 sources. Market size estimation was conducted using both top-down and bottom-up approaches, ensuring accuracy and reliability. Data triangulation and validation techniques were applied to refine estimates, while statistical models were used to forecast growth trends. This comprehensive methodology ensures robust and data-driven insights into the Europe 3D Dental Scanner Market.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.