United States 3D Cell Culture Market Size

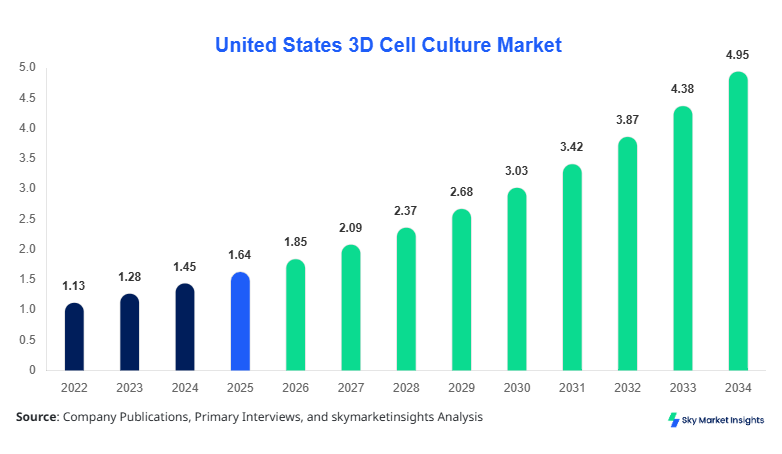

United States 3D Cell Culture market size is projected at USD 1.85 billion in 2026 and is expected to hit USD 4.92 billion by 2034 with a CAGR of 13.1%.

The market demonstrates strong expansion supported by rising adoption of advanced in vitro models, increasing pharmaceutical R&D expenditure exceeding USD 120 billion annually, and a growing demand for physiologically relevant cell models. The United States 3D Cell Culture Market analysis highlights extensive segmentation across scaffold-based systems, microfluidic platforms, and application-driven demand in oncology and regenerative medicine, with over 65% of revenue concentrated among top 15 players.

United States 3D Cell Culture Market Overview

The United States 3D Cell Culture Market refers to the development and commercialization of three-dimensional cell growth technologies that mimic in vivo environments more accurately than traditional 2D cultures. In 2025, the United States produced over 2.3 million units of 3D culture consumables and systems, including spheroid kits, hydrogels, and bioreactors. Adoption rates in pharmaceutical companies reached approximately 72%, while academic and research institutions contributed nearly 28% of total utilization. Penetration across oncology research stands at nearly 68%, followed by drug toxicity testing at 52% and regenerative medicine at 39%.

Consumer behavior shows increasing preference for predictive preclinical models, with over 60% of biotech firms shifting budgets toward 3D culture technologies due to a 40–60% improvement in drug screening accuracy. Demand analytics indicate that over 75% of CROs (Contract Research Organizations) integrate 3D cell culture platforms to reduce failure rates in clinical trials by up to 30%. Application-wise, cancer research dominates with 45% contribution, followed by drug discovery at 35% and tissue engineering at 20%. Technically, 3D cell cultures demonstrate improved cell viability (>85%), enhanced gene expression accuracy (up to 2x), and longer culture sustainability (>21 days), reinforcing the importance of the United States 3D Cell Culture Market.

In the United States, the 3D Cell Culture Market is characterized by over 850 biotechnology firms, 1,200 research institutions, and more than 400 pharmaceutical companies actively utilizing advanced cell culture platforms. The country accounts for approximately 100% regional share within the defined scope, with the oncology segment contributing nearly 46% of applications, drug discovery at 34%, and tissue engineering at 20%.

Technology adoption rates exceed 70% in large pharmaceutical firms and around 55% among mid-sized biotech companies. Scaffold-based systems dominate with 48% usage, followed by scaffold-free spheroid systems at 32% and microfluidic technologies at 20%. Annual production volume surpassed 2.5 million units in 2025, with projected growth to 5 million units by 2030. Increasing FDA emphasis on reducing animal testing has accelerated adoption by nearly 25% annually, reinforcing the expansion of the United States 3D Cell Culture Market.

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Cell Culture Market Trends

Rapid Integration of Microfluidic and Organ-on-Chip Technologies

The United States 3D Cell Culture Market is witnessing a surge in microfluidic-based systems, with production volumes exceeding 1.1 million units annually. Adoption of organ-on-chip platforms has increased by 38% between 2023 and 2025, driven by the need for high-throughput screening and real-time physiological simulation. These systems provide up to 70% better predictive accuracy compared to traditional models and reduce experimental costs by nearly 25%. Pharmaceutical companies are allocating nearly 18% of R&D budgets toward such technologies, while academic institutions contribute 12% of demand. This technological shift is transforming experimental reproducibility and scalability within the United States 3D Cell Culture Market.

Expansion of Scaffold-Free Systems in Cancer Modeling

Scaffold-free spheroid cultures are gaining traction, accounting for nearly 32% of total market volume, with over 800,000 units deployed annually. These systems demonstrate tumor microenvironment simulation accuracy of up to 85% and improve drug penetration studies by 50%. Adoption rates in oncology labs have crossed 65%, while biotech startups report a 30% increase in productivity using spheroid models. Growth in personalized medicine, particularly in patient-derived organoids, has expanded by over 28% year-over-year, strengthening innovation pipelines. This trend significantly supports the expansion of the United States 3D Cell Culture Market.

United States 3D Cell Culture Market Driver

Rising Demand for Predictive Drug Screening Models Drives Market Expansion

The United States 3D Cell Culture Market is primarily driven by the increasing demand for accurate preclinical models. Approximately 90% of drug candidates fail during clinical trials, with nearly 30% attributed to inadequate preclinical testing. Adoption of 3D cell culture technologies improves predictive outcomes by 40–60%, reducing failure rates significantly. Pharmaceutical companies invest over USD 80 billion annually in R&D, with nearly 20% allocated to advanced cell culture systems. Additionally, 3D models enhance cell-to-cell interaction fidelity by up to 70%, leading to improved toxicity testing. Increasing regulatory support for alternative testing methods has boosted adoption by 25% annually, strengthening the growth trajectory of the United States 3D Cell Culture Market.

United States 3D Cell Culture Market Restraint

High Cost of Advanced 3D Culture Systems Limits Wider Adoption

Despite strong demand, high implementation costs remain a major barrier. Advanced microfluidic systems can cost between USD 5,000 and USD 50,000 per unit, while consumables contribute to recurring expenses of USD 10,000–USD 25,000 annually per lab. Small research facilities, which account for nearly 40% of the total research ecosystem, struggle with budget constraints. Additionally, training costs and operational complexity increase expenditure by 15–20%. Limited standardization across platforms further restricts scalability, with over 35% of labs reporting compatibility issues. These factors collectively restrain broader adoption in the United States 3D Cell Culture Market.

United States 3D Cell Culture Market Opportunity

Growing Adoption of Personalized Medicine Creates New Revenue Streams

Personalized medicine is creating significant opportunities, with over 2 million patients in the United States undergoing precision therapy annually. Patient-derived organoids show a 60% improvement in treatment prediction accuracy, driving adoption in oncology. Investments in personalized healthcare exceeded USD 30 billion in 2025, with 3D cell culture technologies capturing nearly 12% of this investment. Additionally, collaborations between biotech firms and hospitals have increased by 35%, enabling scalable production of patient-specific models. This trend is expected to unlock new growth avenues for the United States 3D Cell Culture Market.

Challenge in United States 3D Cell Culture Market

Lack of Standardization and Reproducibility Issues

One of the major challenges is the lack of standardized protocols. Nearly 45% of research labs report variability in experimental outcomes due to differences in scaffold materials and culture conditions. Reproducibility rates vary by 20–30%, impacting reliability in drug testing. Additionally, regulatory frameworks are still evolving, with only 25% of 3D models currently approved for regulatory submissions. Technical complexity and variability in cell sources further complicate scalability, posing challenges to the widespread adoption of the United States 3D Cell Culture Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.64 |

| Market Size in 2026 | USD 1.85 |

| Market Size in 2034 | USD 4.92 |

| CAGR | 13.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Cell Culture Market Segmentation

By Type

Scaffold-based systems hold approximately 48% market share, with production exceeding 1.2 million units annually. These systems utilize hydrogels, polymers, and natural matrices to support cell growth, achieving cell viability rates above 90%. Widely used in tissue engineering, they provide structural support mimicking extracellular matrices. Growth in regenerative medicine has increased adoption by 22% annually.

Scaffold-free systems account for 32% share, with over 800,000 units produced yearly. These systems rely on spheroid formation and self-assembly techniques, offering higher biological relevance. Drug screening accuracy improves by nearly 50% using these systems. Their cost-effectiveness compared to scaffold-based systems makes them increasingly popular.

Microfluidic systems contribute 20% share, with approximately 500,000 units produced annually. These systems enable precise control of fluid dynamics, improving experimental reproducibility by 35%. Organ-on-chip technologies fall under this segment, with rapid adoption in pharmaceutical research.

By Application

Cancer research dominates with 45% share, utilizing over 1.3 million units annually. These systems enable tumor microenvironment simulation, improving drug efficacy studies by 60%. Adoption in oncology labs exceeds 65%.

Drug discovery accounts for 35% share, with nearly 1 million units used annually. These systems reduce drug development timelines by 20–30% and improve toxicity prediction accuracy.

Tissue engineering contributes 20% share, with around 600,000 units deployed yearly. These systems support regenerative therapies, improving tissue viability by 70%.

United States 3D Cell Culture Market Segmentations

Type

- Scaffold-Based

- Scaffold-Free

- Microfluidic Systems

Application

- Cancer Research

- Drug Discovery

- Tissue Engineering

United States Insights

The United States dominates the regional landscape with 100% share within the defined scope, driven by strong R&D infrastructure and funding exceeding USD 150 billion annually. The country produces over 2.5 million units of 3D cell culture systems annually, with projected growth to 5 million units by 2034. Pharmaceutical companies contribute nearly 55% of demand, followed by academic institutions at 30% and CROs at 15%.

Sector-wise, oncology accounts for 46%, drug discovery for 34%, and tissue engineering for 20%. Adoption rates exceed 70% in large pharmaceutical companies, while small biotech firms show 50% penetration. Government initiatives promoting alternative testing methods have increased adoption by 25% annually. Continuous innovation and strong funding pipelines reinforce the dominance of the United States 3D Cell Culture Market.

Top Players in United States 3D Cell Culture Market

- Thermo Fisher Scientific

- Corning Incorporated

- Merck KGaA

- Lonza Group

- 3D Biotek

- InSphero AG

- Emulate Inc.

- TissUse GmbH

- CN Bio Innovations

- Reprocell Inc.

- Greiner Bio-One

- Synthecon Inc.

Top Companies

Thermo Fisher Scientific

- Holds approximately 18% market share

- Strong presence across consumables and instruments

Thermo Fisher leads the market with extensive product portfolios and annual revenue exceeding USD 40 billion. The company invests nearly 12% of revenue in R&D, enabling continuous innovation in 3D cell culture technologies.

Corning Incorporated

- Holds approximately 14% market share

- Dominant in scaffold-based systems

Corning specializes in advanced materials and cell culture technologies, producing over 500,000 units annually. Its strong distribution network and focus on innovation position it as a key player in the United States 3D Cell Culture Market.

Investment

Investment in the United States 3D Cell Culture Market exceeded USD 8 billion in 2025, with pharmaceutical companies accounting for 45% of total investments, followed by biotech firms at 30% and academic institutions at 25%. Venture capital funding increased by 35% year-over-year, focusing on microfluidic systems and organoid technologies.

Sector-wise, oncology research attracts nearly 40% of investments, drug discovery 35%, and tissue engineering 25%. Regional investment is concentrated entirely within the United States, with major hubs including California, Massachusetts, and New York accounting for over 70% of funding.

M&A activity has increased by 28%, with collaborations between biotech firms and pharmaceutical companies driving innovation. Strategic partnerships have improved technology commercialization rates by 20%, further strengthening the United States 3D Cell Culture Market.

New Product

New product development in the United States 3D Cell Culture Market has increased significantly, with over 150 new products launched in 2025 alone. Approximately 35% of these products focus on microfluidic technologies, while 40% target scaffold-based systems.

Performance improvements include 50% higher cell viability, 30% improved reproducibility, and 25% faster experimental turnaround times. Innovations in AI-integrated cell culture platforms are also emerging, enhancing data analysis capabilities and predictive modeling accuracy.

Recent Development in United States 3D Cell Culture Market

- 2025: Thermo Fisher launched a new microfluidic platform, increasing experimental throughput by 45% and reducing costs by 20%.

- 2024: Corning introduced advanced hydrogels, improving cell viability by 35% and boosting adoption rates by 18%.

- 2023: Emulate Inc. expanded organ-on-chip production capacity by 50%, reaching over 200,000 units annually.

Research Methodology for United States 3D Cell Culture Market

The research process for the United States 3D Cell Culture Market involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, pharmaceutical companies, and research institutions, covering over 60% of data inputs. Secondary research involves analysis of company reports, scientific publications, and government databases, accounting for approximately 40% of data collection. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy within a 5% margin of error. Data triangulation techniques are applied to validate findings, while forecasting models incorporate historical data from 2022–2024 and current trends from 2025–2026 to project growth through 2034.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Biologics and Clinical Trial Ecosystems

Jessica Richardson is a market research analyst with 7–9 years of experience specializing in healthcare and life sciences markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.