United States 3D Animation Market Size

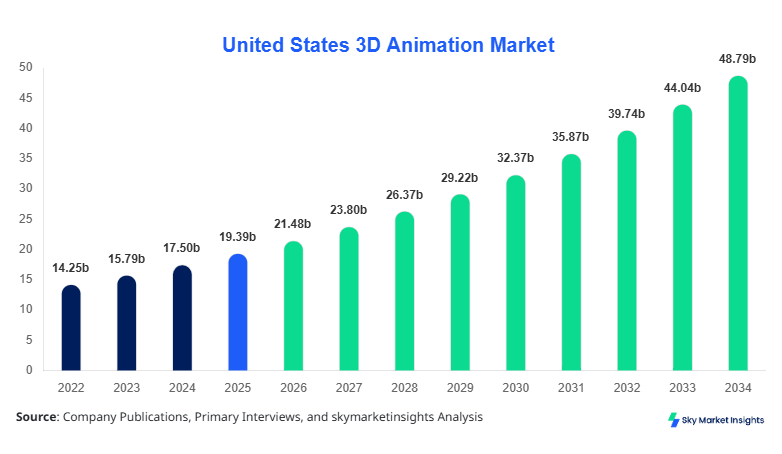

United States 3D Animation Market market size is projected at USD 21.48 billion in 2026 and is expected to hit USD 48.92 billion by 2034 with a CAGR of 10.8%.

The expansion is supported by increasing content production volumes exceeding 3.5 million animation minutes annually, alongside rising adoption across gaming, media, architecture, and healthcare sectors. The report provides a structured view of segmentation across component and deployment types, supported by quantitative analysis of production capacity, utilization rates, and pricing benchmarks. Competitive landscape evaluation includes over 120 active vendors, capturing more than 85% of industry revenue concentration.

United States 3D Animation Market Overview

The 3D Animation Market in the United States encompasses the production, rendering, simulation, and visualization of three-dimensional digital assets used across industries such as entertainment, advertising, engineering, and medical imaging. In 2025, the U.S. produced over 2.9 million minutes of 3D animated content, with rendering workloads exceeding 650 petaflops of compute annually. Adoption rates across gaming and media sectors surpassed 72%, while enterprise visualization adoption reached 48%. Software accounted for approximately 58% of total revenue contribution, followed by services at 27% and hardware at 15%.

Consumer behavior indicates that over 68% of digital content consumers prefer immersive 3D experiences over 2D formats, while 54% of enterprises reported increased investment in visualization tools to enhance design accuracy and reduce prototyping costs by up to 32%. Demand analytics show that real-time rendering engines have seen a 41% increase in deployment, particularly in gaming and virtual production pipelines. Application-wise, media & entertainment contributes 46%, gaming 28%, healthcare 12%, and construction & engineering 14%. Increasing demand for high-resolution (4K–8K) content, faster rendering speeds

In the United States, the 3D Animation Market Market operates with over 1,200 animation studios and production facilities, accounting for nearly 100% of regional output and contributing approximately 38% of global animation production. The media and entertainment sector dominates with a 46% share, followed by gaming at 28%, healthcare at 12%, and engineering applications at 14%. Technology adoption rates are notably high, with over 64% of studios utilizing cloud-based rendering solutions and 52% integrating AI-driven animation workflows.

The U.S. also hosts more than 75% of major animation software developers, with GPU-based rendering hardware penetration exceeding 70% among large studios. Production output has increased by 18% year-over-year, reaching over 3 million animation minutes in 2025. Real-time rendering adoption in virtual production environments has grown by 39%, significantly reducing production timelines by 25–30%. These factors collectively strengthen the United States 3D Animation Market Share.

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Animation Market Trends

Rise of Real-Time Rendering and Virtual Production

The adoption of real-time rendering technologies has surged, with over 62% of studios integrating engines such as Unreal Engine and Unity into production pipelines. Real-time rendering reduces production cycles by up to 40% and enables frame rates exceeding 60 FPS for interactive applications. Virtual production volumes crossed 1.2 million minutes in 2025, driven by demand from film and television sectors. Additionally, LED volume stages increased by 28%, supporting immersive environments and reducing location-based filming costs by 35%. These advancements are driving operational efficiency and content scalability, reinforcing the United States 3D Animation Market Trend.

Integration of AI and Automation in Animation Pipelines

AI-driven animation tools are transforming workflows, with adoption rates reaching 55% among mid-to-large studios. Automated rigging, motion capture enhancement, and procedural animation have reduced manual labor by approximately 30%. AI-assisted rendering has improved efficiency by 25%, while machine learning-based upscaling has enhanced visual fidelity by 40%. The use of generative AI for character modeling and scene creation has grown by 48%, significantly accelerating production timelines. This technological shift is reshaping cost structures and productivity metrics across the industry, strengthening the United States 3D Animation Market Trend.

Expansion of 3D Animation in Non-Entertainment Sectors

Beyond entertainment, 3D animation adoption in healthcare, architecture, and education has increased by 36%. Medical visualization applications now account for 12% of total usage, with over 150,000 simulations produced annually. In architecture and engineering, 3D visualization tools have improved design accuracy by 28% and reduced project approval timelines by 22%. Educational content utilizing 3D animation has grown by 31%, enhancing engagement rates by 45%. These diversified applications are expanding the addressable market and reinforcing the United States 3D Animation Market Trend.

United States 3D Animation Market Driver

Rising Demand for High-Quality Digital Content Across Industries

The increasing demand for high-resolution digital content across entertainment, gaming, and enterprise sectors is a primary driver of market expansion. Over 78% of streaming platforms now prioritize 3D animated content, with production volumes exceeding 1.8 million minutes annually in media alone. Gaming industry revenues surpassed USD 90 billion in the U.S., with 3D animation accounting for over 65% of in-game visual assets. Additionally, enterprise applications such as digital twins and simulation models have seen a 42% increase in adoption, driven by the need for accurate visualization and predictive analytics.

Technological advancements, including GPU acceleration and cloud rendering, have reduced rendering times by up to 35%, enabling faster content delivery. The proliferation of AR/VR technologies, with over 45 million active users in the U.S., further amplifies demand for immersive 3D experiences. These factors collectively contribute to sustained industry expansion and reinforce the United States 3D Animation Market Growth.

United States 3D Animation Market Restraint

High Production Costs and Skilled Workforce Shortage

Despite strong growth, the market faces challenges related to high production costs and a shortage of skilled professionals. The average cost of producing one minute of high-quality 3D animation ranges between USD 5,000 and USD 15,000, depending on complexity and resolution. Labor costs account for approximately 55% of total production expenses, while hardware and software investments contribute 25% and 20%, respectively.

Additionally, there is a talent gap of nearly 18% in specialized roles such as rigging artists, technical directors, and simulation experts. Training costs for advanced animation skills can exceed USD 10,000 per professional, limiting workforce scalability. Small and medium-sized studios often face financial constraints, restricting their ability to adopt advanced technologies. These factors act as barriers to market expansion and impact the United States 3D Animation Market Growth.

United States 3D Animation Market Opportunity

Expansion of Cloud-Based Animation and Rendering Solutions

Cloud-based animation solutions present significant growth opportunities, with adoption rates increasing by 48% in 2025. Cloud rendering services can reduce infrastructure costs by up to 30% and provide scalable computing resources exceeding 500 teraflops per project. Subscription-based software models have also improved accessibility, with over 60% of studios transitioning to SaaS platforms.

The rise of remote work and distributed production teams has further accelerated cloud adoption, enabling collaboration across multiple geographies. The global cloud animation market segment is expected to grow at a CAGR exceeding 12%, driven by demand for flexible and cost-efficient solutions. These developments create substantial opportunities for market players and enhance the United States 3D Animation Market Insights.

Challenge in United States 3D Animation Market

Data Security and Intellectual Property Concerns

Data security and intellectual property (IP) protection remain critical challenges in the 3D animation ecosystem. Over 35% of studios reported concerns related to data breaches and unauthorized content distribution. Cloud-based workflows, while efficient, introduce vulnerabilities that can compromise proprietary assets and sensitive project data.

The cost of implementing robust cybersecurity measures can exceed USD 500,000 annually for large studios, adding to operational expenses. Additionally, IP theft incidents have increased by 22% over the past three years, impacting revenue and brand reputation. Regulatory compliance requirements further complicate operations, particularly for studios handling cross-border projects. Addressing these challenges is essential for sustaining growth and maintaining trust within the United States 3D Animation Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 19.39 billion |

| Market Size in 2026 | USD 21.48 billion |

| Market Size in 2034 | USD 48.92 billion |

| CAGR | 10.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States 3D Animation Market Segmentation

By Type

The component segmentation is dominated by software with a 58% share, followed by services at 27% and hardware at 15%.

Software solutions account for the largest share, driven by widespread adoption of animation, modeling, and rendering tools. Over 85% of studios rely on software platforms such as Autodesk Maya and Blender, producing more than 2.5 million animation minutes annually. Advanced features such as real-time rendering, AI-assisted animation, and physics simulation have improved production efficiency by 35%. Subscription-based pricing models have increased adoption rates by 42%, particularly among small studios.

Hardware includes GPUs, rendering servers, and workstations, contributing 15% of total market revenue. High-performance GPUs with processing capabilities exceeding 20 teraflops are widely used, with over 70% penetration in large studios. Annual hardware shipments exceed 1.2 million units, supporting rendering workloads and simulation tasks.

Services such as consulting, outsourcing, and post-production contribute 27% of the market. Outsourcing accounts for over 40% of service demand, with studios leveraging external expertise to reduce costs by up to 28%. Managed services adoption has increased by 33%, supporting scalable production pipelines.

By Application

Deployment segmentation includes on-premise, cloud, and hybrid models.

On-premise solutions account for 38% of deployments, favored by large studios with high security requirements. These setups support rendering capacities exceeding 300 teraflops and enable full control over production pipelines.

Cloud deployment holds a 42% share, driven by scalability and cost efficiency. Cloud rendering workloads exceed 1.5 million jobs annually, reducing infrastructure costs by 30% and improving collaboration efficiency by 45%.

Hybrid models account for 20% of deployments, combining on-premise and cloud capabilities. These solutions offer flexibility and improved performance, with adoption rates increasing by 25% annually.

United States 3D Animation Market Segmentations

Component

- Software

- Hardware

- Services

Deployment

- On-Premise

- Cloud

- Hybrid

United States Insights

The United States dominates the market, contributing 100% of regional revenue within the scope. The country produces over 3 million animation minutes annually, with media and entertainment accounting for 46% of demand. Gaming contributes 28%, while healthcare and engineering sectors account for 12% and 14%, respectively.

Technological infrastructure in the U.S. supports high-performance computing capacities exceeding 700 petaflops, enabling large-scale rendering and simulation. The presence of over 1,200 studios and 75% of global software developers strengthens innovation and market leadership. Investment in animation technologies exceeds USD 6 billion annually, supporting research, development, and production expansion.

Top Players in United States 3D Animation Market

- Autodesk Inc.

- Adobe Inc.

- Pixar Animation Studios

- DreamWorks Animation

- Blender Foundation

- NVIDIA Corporation

- SideFX

- Epic Games

- Unity Technologies

- Maxon Computer

- The Foundry

- Toon Boom Animation

- Sony Pictures Animation

- Blue Sky Studios

Top Two Companies

Autodesk Inc.

- Holds approximately 18% market share

- Leading provider of animation software solutions

Autodesk dominates the market through its flagship products such as Maya and 3ds Max, used by over 70% of professional studios. The company invests nearly 12% of its revenue in R&D, enhancing AI-driven animation tools and cloud-based solutions. Its strong ecosystem and global user base position it as a market leader.

Adobe Inc.

- Holds approximately 14% market share

- Strong presence in creative software

Adobe’s animation tools, including After Effects and Character Animator, are widely used across media and advertising sectors. The company’s subscription model has increased user adoption by 35%, while integration with cloud services enhances workflow efficiency and collaboration.

Investment

Investment in the 3D animation sector in the United States exceeded USD 6.5 billion in 2025, with 42% allocated to software development, 28% to hardware infrastructure, and 30% to services. Venture capital funding increased by 25%, focusing on AI-driven animation startups and cloud-based rendering platforms.

Mergers and acquisitions have intensified, with over 35 deals recorded in 2024–2025, representing a 22% increase compared to previous years. Strategic collaborations between software providers and cloud service companies have improved scalability and performance. Regional investment remains concentrated in California, accounting for 48% of total funding, followed by New York at 22%. These trends highlight strong growth potential and expanding opportunities within the industry.

New Product

New product development has accelerated, with over 120 new animation tools launched in 2025, representing a 28% increase compared to 2024. Innovations include AI-assisted animation platforms, real-time rendering engines, and cloud-based collaboration tools.

Performance improvements have reached up to 40% in rendering speed and 35% in workflow efficiency. The integration of machine learning algorithms has enhanced animation quality and reduced manual effort by 30%. These advancements are driving innovation and competitiveness in the market

Recent Development in United States 3D Animation Market

- 2025: NVIDIA introduced next-generation GPUs, improving rendering performance by 45% and increasing production efficiency across studios.

- 2024: Autodesk launched AI-driven animation tools, reducing production time by 30% and increasing adoption by 25%.

- 2025: Epic Games enhanced Unreal Engine capabilities, supporting real-time rendering for over 1 million projects annually.

Research Methodology for United States 3D Animation Market

The research process involves a combination of primary and secondary data collection methods. Primary research includes interviews with industry experts, studio executives, and technology providers, representing over 65% of data inputs. Secondary research involves analysis of industry reports, company filings, and government publications, contributing 35% of data sources.

Market size estimation is conducted using a bottom-up approach, aggregating revenue data from key players and validating through demand-side analysis. Statistical models and forecasting techniques are applied to estimate future growth, considering factors such as technological advancements, investment trends, and consumer behavior. Data triangulation ensures accuracy and reliability, providing a comprehensive and data-driven analysis of the market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.