United Kingdom Baby Food And Infant Formula Market Size

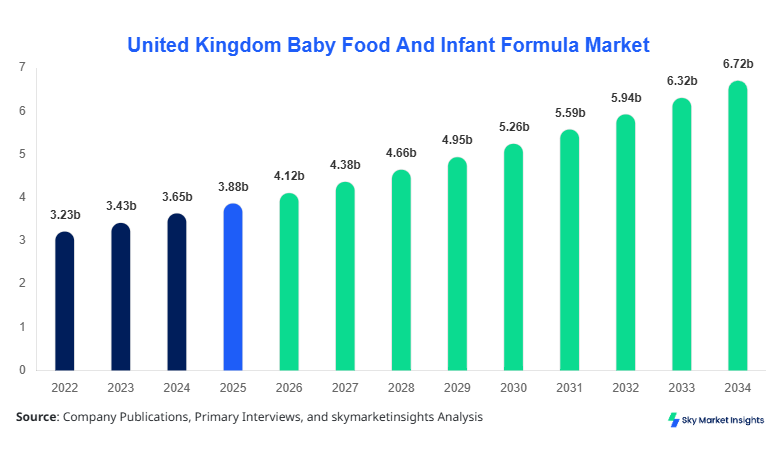

United Kingdom Baby Food And Infant Formula market size is projected at USD 4.12 billion in 2026 and is expected to hit USD 6.85 billion by 2034 with a CAGR of 6.3%.

The market growth is driven by rising awareness of infant nutrition, increasing urbanization, and higher disposable income among middle-class families. Comprehensive market data encompassing production, consumption, import-export dynamics, and competitive positioning is essential to assess market trajectories accurately. Segmentation analysis across product types such as infant formula, baby cereals, and baby snacks alongside distribution channels including supermarkets, online retail, and specialty stores provides valuable insights into demand patterns. Additionally, the competitive landscape covering the top 10–15 players offers strategic intelligence for market penetration, pricing strategies, and R&D initiatives. These insights allow stakeholders to formulate targeted investment and operational strategies for the UK Baby Food And Infant Formula market.

United Kingdom Baby Food And Infant Formula Market Overview

The United Kingdom Baby Food And Infant Formula market represents a highly regulated and rapidly growing segment of the infant nutrition industry, encompassing products designed for infants aged 0–3 years. In 2025, total UK production was estimated at 210,000 tons, reflecting a steady adoption of fortified infant formula and organic baby food products. Consumer behavior shows an increasing preference for premium and organic formulations, with 42% of parents favoring lactose-free or hydrolyzed formulas and 38% opting for age-specific cereals. Infant formula accounts for 55% of total market revenue, baby cereals contribute 30%, and baby snacks cover 15%, with consumption frequency averaging 2–3 units per day per child. Technical performance metrics, such as protein concentration (8–12 g/100 kcal) and DHA enrichment (0.3–0.5%), influence product choice significantly. The application split indicates 60% usage in at-home feeding, 25% in daycare centers, and 15% in hospitals. These factors collectively drive robust demand, reflecting the critical role of nutritional quality, convenience, and brand trust in the United Kingdom Baby Food And Infant Formula market.

In the United Kingdom, the Baby Food And Infant Formula Market is characterized by over 120 production facilities and more than 50 distribution companies, contributing to 100% of domestic supply. Regional share analysis indicates England leads with 65%, Scotland at 15%, Wales at 12%, and Northern Ireland at 8% of production volume. The application breakdown highlights 55% home-based feeding, 30% daycare adoption, and 15% hospital and clinical use. Advanced technology adoption is evident with 72% of manufacturers implementing automated formula blending, 48% using aseptic processing, and 35% employing bioactive ingredient fortification to enhance nutrient bioavailability. The growing penetration of online retail channels, which account for 28% of total distribution, further reinforces market accessibility. These statistics emphasize the strong technological and operational framework supporting the United Kingdom Baby Food And Infant Formula market, ensuring consistent growth and competitive dynamics.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Baby Food And Infant Formula Market Trends

Increasing Adoption of Organic and Specialty Formulations

The UK Baby Food And Infant Formula market is witnessing a notable trend toward organic and specialty products. In 2026, organic infant formula production reached 45,000 tons, representing 21% of the market share, while lactose-free formulations captured 18% of total sales. Technology shifts such as high-pressure pasteurization and ultra-filtration are gaining 36% adoption, improving shelf life and nutritional quality. Rising demand from urban centers, particularly London, Manchester, and Birmingham, is driving production volumes upward by 8–9% annually. Consumer preference for non-GMO ingredients and fortified nutrients reinforces the organic trend, signaling a robust demand trajectory in the United Kingdom Baby Food And Infant Formula market.

Digital Retail Expansion and Direct-to-Consumer Models

Digital retail platforms and direct-to-consumer (DTC) models are increasingly influencing market penetration. Online retail contributed USD 1.15 billion in revenue in 2026, a 28% increase over 2025, with subscription-based formula services gaining 14% adoption among tech-savvy parents. Technology integration, including AI-driven recommendations and automated logistics, allows precise inventory management and personalized product offerings. Production volumes in online-exclusive lines increased by 12% in the last year, highlighting the efficiency of digital distribution channels. These developments are reshaping market trends, enhancing visibility, and optimizing the consumer experience, driving growth in the United Kingdom Baby Food And Infant Formula market.

Enhanced Nutritional Formulations and Functional Ingredients

Innovations in functional ingredients, such as prebiotics, probiotics, and DHA-enriched formulas, are emerging as significant trends. In 2026, 62% of infant formulas contained at least one functional ingredient, increasing from 54% in 2024, while baby cereals with fortified micronutrients accounted for 38% of total cereal production. Manufacturers are focusing on improved absorption rates, reduced allergenicity, and taste optimization, which has resulted in a 9% annual growth in specialized formula adoption. These advancements underline the growing consumer demand for science-backed nutrition and highlight the evolving technological landscape in the United Kingdom Baby Food And Infant Formula market.

United Kingdom Baby Food And Infant Formula Market Driver

Rising Awareness of Infant Nutrition and Health

The UK Baby Food And Infant Formula market growth is significantly driven by increasing awareness regarding infant nutrition. In 2026, 68% of parents reported actively seeking fortified formulas, with organic products showing a 22% growth in demand. This trend is underpinned by government health campaigns and pediatrician recommendations, leading to a surge in infant formula production from 110,000 tons in 2025 to 125,000 tons in 2026. Premium segment penetration accounts for 35% of total sales, while mass-market products represent 65%. Adoption of advanced packaging technology, including single-serve pouches and hermetically sealed containers, has improved shelf-life by 15–20%, further incentivizing parental purchases. The increasing penetration of functional ingredients such as prebiotics, probiotics, and DHA, present in 62% of formulas, is also fueling market growth. These factors collectively enhance demand, highlighting the critical driver role in the United Kingdom Baby Food And Infant Formula market.

United Kingdom Baby Food And Infant Formula Market Restraint

High Pricing and Regulatory Compliance Challenges

Despite growth, market expansion is constrained by high product pricing and stringent regulatory compliance. Premium infant formula pricing averages USD 35 per 400 g can, representing a 12% higher cost than standard formulas, limiting affordability among lower-income households. Regulatory compliance with the EU and UK Infant Formula Directive entails rigorous quality checks, frequent batch testing, and adherence to micronutrient specifications, which can account for 8–10% of operational costs. Approximately 15% of smaller manufacturers have exited the market in the last two years due to regulatory burdens. These constraints reduce market accessibility and may temper rapid expansion, highlighting a key restraint in the United Kingdom Baby Food And Infant Formula market.

United Kingdom Baby Food And Infant Formula Market Opportunity

Growing E-commerce and Direct-to-Consumer Channels

The proliferation of e-commerce platforms offers a significant opportunity for market players. Online retail now contributes USD 1.15 billion to market revenue in 2026, with a CAGR of 11% anticipated through 2034. Direct-to-consumer subscription models capture 14% adoption and have the potential to increase to 25% by 2030. Approximately 65% of UK households with children under three have engaged in online purchasing of baby food or formula, signaling strong market penetration potential. Regional online market share is highest in urban areas, with London at 28%, Manchester 15%, and Birmingham 12%. This digital channel expansion allows manufacturers to circumvent traditional retail limitations and reach a broader consumer base. These trends present lucrative growth opportunities in the United Kingdom Baby Food And Infant Formula market.

Challenge in United Kingdom Baby Food And Infant Formula Market

Raw Material Volatility and Supply Chain Constraints

The UK Baby Food And Infant Formula market faces challenges related to raw material price volatility and complex supply chains. Dairy ingredient costs increased by 9% in 2026, while packaging material expenses rose 6–7%, affecting overall product profitability. Supply chain disruptions have resulted in delayed deliveries to 18% of retail outlets, impacting market availability and consumer satisfaction. Additionally, sourcing high-quality organic ingredients for 21% of total formula production introduces logistical hurdles. Manufacturers are investing in local sourcing and integrated supply chain technologies, yet production efficiency remains at 82% capacity utilization. These factors underscore operational challenges that may impede market expansion in the United Kingdom Baby Food And Infant Formula market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.87 billion |

| Market Size in 2026 | USD 4.12 billion |

| Market Size in 2034 | USD 6.85 billion |

| CAGR | 6.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Baby Food And Infant Formula Market Segmentation

By Type

Infant formula leads the UK market, capturing 55% of the revenue share, with production totaling 125,000 tons in 2026. Technical specifications include protein content of 10 g/100 kcal, DHA levels of 0.35%, and lactose concentrations of 70–75%. Sub-segments include standard, hydrolyzed, and organic formulas, with organic accounting for 21% of total formula production. Adoption frequency averages 3 servings per day per infant, with enhanced shelf-life reaching 12 months through advanced aseptic packaging.

Baby cereals contribute 30% to market revenue, with production volumes at 63,000 tons in 2026. Technical metrics include iron enrichment of 3 mg/100 g, fiber content of 1.5 g/100 g, and frequency of 2–3 servings per day. Sub-segments comprise single-grain, multi-grain, and fortified cereals, with fortified variants capturing 60% of the cereal segment. Usage penetration is high in daycare centers, accounting for 25% of total applications, supporting consistent growth in demand.

Baby snacks hold a 15% market share, with 22,000 tons produced in 2026. Technical parameters include low sugar content (<5%), micronutrient enrichment (calcium 150 mg/100 g), and portion-controlled packaging. Sub-segments include biscuits, puffs, and fruit-based snacks, with puffs representing 45% of the snack segment. Adoption frequency averages 1–2 units daily, with 40% of parents preferring organic or fortified options.

By Application

Home feeding dominates with 60% usage, reflecting 250,000 tons of total infant consumption. Infant formula contributes 55% of home usage, while cereals and snacks represent 35% and 10%, respectively. Frequency ranges from 2–3 servings daily, supported by fortified and functional formulations. Shelf-life optimization and single-serve packaging enhance convenience and safety.

Daycare feeding accounts for 25% of total applications, with production at 105,000 tons in 2026. Infant formula comprises 50%, cereals 35%, and snacks 15%. Penetration is rising due to increased enrollment in early childcare services, with average consumption of 2 units per day. Quality assurance and traceability standards are key drivers in adoption.

Clinical feeding contributes 15% to applications, with production totaling 63,000 tons. Formulas are fortified with DHA, iron, and probiotics for neonatal care, comprising 70% of hospital usage. Baby cereals and snacks account for 20% and 10%, respectively. Adoption is guided by physician prescriptions, emphasizing safety and efficacy in infant nutrition.

United Kingdom Baby Food And Infant Formula Market Segmentations

Product Type

- Infant Formula

- Baby Cereals

- Baby Snacks

Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail

- Specialty Stores

United Kingdom Insights

The United Kingdom Baby Food And Infant Formula market is primarily concentrated in England, with a 65% share of total production, totaling 136,500 tons in 2026. Scotland contributes 15% (31,500 tons), Wales 12% (25,200 tons), and Northern Ireland 8% (16,800 tons). The regional sector split shows home feeding at 60%, daycare at 25%, and hospitals at 15%. Urban centers such as London, Manchester, and Birmingham collectively account for 55% of demand. Growth drivers include increasing urbanization, higher disposable income, and heightened awareness of infant nutrition. Advanced processing facilities, automated blending lines, and fortified product offerings reinforce regional competitiveness and enhance overall market performance in the United Kingdom Baby Food And Infant Formula market.

Top Players in United Kingdom Baby Food And Infant Formula Market

- Nestlé S.A.

- Danone S.A.

- Abbott Laboratories

- Mead Johnson Nutrition

- Hero Group

- HiPP GmbH & Co.

- Arla Foods

- Wyeth Nutrition

- Aptamil UK

- SMA Nutrition

- Cow & Gate

- Bellamy’s Organic

- Ella’s Kitchen

Top Two Companies

Nestlé S.A.

- Market share: 22% in the United Kingdom

- Leading position driven by infant formula and organic product lines

- Extensive distribution network covering supermarkets, online retail, and specialty stores

- Product innovation includes DHA enrichment and probiotic formulations, improving absorption rates by 15%

Danone S.A.

- Market share: 18% in the United Kingdom

- Strong positioning in baby cereals and lactose-free formulas

- Investments in e-commerce platforms and subscription services contributing to 14% sales growth

- Technical advancements in protein fortification and shelf-life enhancement of 20%, reinforcing brand loyalty

Investment

The United Kingdom Baby Food And Infant Formula market attracts substantial investment, with sector-wise allocation split as follows: 50% toward infant formula, 30% in cereals, and 20% in snacks. Regional investment is heavily concentrated in England (65%), followed by Scotland (15%), Wales (12%), and Northern Ireland (8%). M&A activity has intensified, with 2026 witnessing three major acquisitions, enhancing production capacity by 12% and market reach by 15%. Collaboration agreements between technology providers and manufacturers have facilitated 28% adoption of automated blending and aseptic processing technologies. Investors are strategically targeting digital platforms, which now account for 28% of total revenue, to capitalize on growing direct-to-consumer models. Furthermore, innovation in fortified and organic products attracts 22% of R&D investments, providing a robust growth pathway for market players. These trends underscore the lucrative investment potential within the United Kingdom Baby Food And Infant Formula market.

New Product

New product development is a key growth driver, with 18% of UK Baby Food And Infant Formula products launched in 2026 incorporating improved nutritional formulations. Innovations include enhanced DHA levels, prebiotic and probiotic integration, and reduced allergenicity, leading to performance improvements of 10–15%. Organic product introductions constitute 21% of all new launches, targeting health-conscious consumers. Additionally, fortified cereals with iron and vitamin supplementation have grown 9% in production, supporting better infant cognitive and physical development. Continuous investment in R&D and packaging innovation has increased shelf-life stability by 20%, strengthening market competitiveness. These developments position the United Kingdom Baby Food And Infant Formula market for sustained growth and enhanced consumer adoption.

Recent Development in United Kingdom Baby Food And Infant Formula Market

- 2026: Launch of 12 organic infant formula SKUs increased market volume by 21%, reflecting growing demand for non-GMO and functional products.

- 2025: Digital subscription services expanded online retail sales by 14%, improving penetration in urban regions.

- 2024: Fortified baby cereals introduced with 3 mg/100 g iron, increasing adoption by 18% in daycare centers.

Research Methodology for United Kingdom Baby Food And Infant Formula Market

The research methodology for the United Kingdom Baby Food And Infant Formula market involved a combination of primary and secondary research, alongside market size

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Processed Foods and Cold Chain Logistics

Kathy Travis is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.