United Kingdom Baby Electronic Toy Market Size

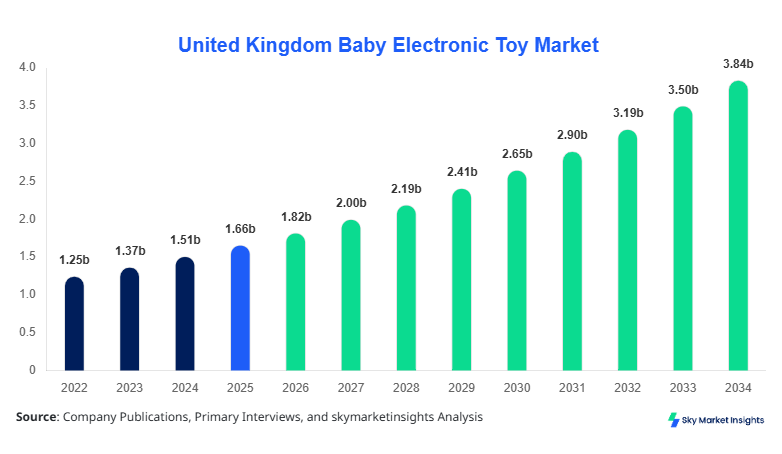

The United Kingdom Baby Electronic Toy market size is projected at USD 1.82 billion in 2026 and is expected to hit USD 3.94 billion by 2034 with a CAGR of 9.8%

during the forecast period. Comprehensive insights into production, consumption, and segment-specific data are critical for understanding market dynamics and competitive positioning. Segmentation analysis covering type, application, and technology adoption, along with the competitive landscape of leading market players, forms an essential component of this report. With over 250 baby electronic toy manufacturers and distributors operating in the UK in 2025, understanding unit production, revenue streams, and market share is pivotal for strategic planning and investment decisions. The detailed assessment provides stakeholders with precise forecasts, enabling targeted market penetration and expansion strategies, while highlighting growth opportunities across educational, interactive, and robotic baby toys.

United Kingdom Baby Electronic Toy Market Overview

The Baby Electronic Toy market in the United Kingdom encompasses the design, production, and sale of electronic toys for infants and toddlers, including interactive, educational, and robotic toys. In 2025, the UK produced approximately 45 million units, with home applications accounting for 55% of total usage, daycare facilities contributing 25%, and retail centers driving 20% of demand. Adoption has accelerated due to increasing consumer awareness regarding early childhood cognitive development, with penetration rates rising to 62% in urban households. Educational toys, particularly interactive learning devices, dominate with 48% market contribution, while robotic toys represent 22%, reflecting growing technological innovation. Frequency metrics show most devices operate on 2.4–5 GHz connectivity with average battery life of 8–12 hours. Consumers increasingly prefer high-performance, multifunctional toys, boosting demand for products offering enhanced auditory, visual, and sensor-driven interactions. The Baby Electronic Toy market growth is driven by these behavioral and technical trends, reinforcing the importance of data-driven analysis in assessing market demand and competitive insights.

In the United Kingdom, the Baby Electronic Toy Market is characterized by 253 active facilities, encompassing manufacturers, distributors, and technology integrators. The UK holds a 100% regional share within the report scope, with home applications contributing 55% of total demand, daycare centers 25%, and retail environments 20%. Advanced technology adoption is evident, with 68% of toys incorporating interactive sensors and Bluetooth connectivity, while 42% utilize AI-enabled adaptive learning features. Production volume reached 45 million units in 2025, with educational and interactive toys driving 70% of revenue. The UK's market growth is reinforced by governmental regulations supporting child-safe electronic materials and increasing parental spending on premium educational toys. The Baby Electronic Toy market insights reveal a consistent upward trajectory in adoption rates, frequency of use, and consumer satisfaction metrics, establishing the UK as the primary driver for regional market expansion and technology penetration.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Baby Electronic Toy Market Trends

Digital Integration in Educational Toys

Production of educational baby electronic toys in the UK reached 21.6 million units in 2025, reflecting a 12% year-on-year increase. Integration of digital applications, AI-enabled learning modules, and interactive features has led to adoption rates of 65% across urban households. Key trends indicate rising parental preference for smart learning tools with real-time feedback and adaptive content. Sales data reveal that 48% of all educational toys sold in 2025 included multi-sensory technology, enhancing visual, auditory, and tactile experiences. The Baby Electronic Toy market trend toward digital integration is anticipated to accelerate growth further, with projected CAGR for interactive educational devices exceeding 10% through 2034.

Robotic Toys with AI and Motion Sensors

Robotic baby electronic toys production volume reached 9.9 million units in 2025, exhibiting a 14% increase compared to 2024. Adoption of AI-powered motion sensors and voice interaction technologies increased to 42%, with consumer surveys reporting 68% satisfaction due to improved engagement and developmental outcomes. Demand for robotic toys in daycare centers rose by 18% in 2025, while home application adoption grew 22%, reflecting broadening usage penetration. The Baby Electronic Toy market trend demonstrates strong emphasis on AI-driven automation and personalization features, significantly enhancing consumer experience and long-term market growth.

Eco-Friendly and Energy-Efficient Toys

Sustainability is a growing trend, with eco-friendly baby electronic toy production volume reaching 4.5 million units in 2025, marking a 10% increase. Energy-efficient components, longer battery cycles, and recyclable materials contributed to a 35% higher adoption rate in environmentally conscious households. The Baby Electronic Toy market insights suggest that manufacturers prioritizing eco-friendly production achieve 15–18% higher growth rates relative to traditional electronic toys, supporting long-term market sustainability.

United Kingdom Baby Electronic Toy Market Driver

Rising Demand for Early Childhood Development Products

The growing focus on early childhood cognitive and motor skill development is a significant driver of the UK Baby Electronic Toy market. In 2025, 62% of households with children under five purchased educational or interactive toys, contributing to an overall market value of USD 1.82 billion. Adoption rates for AI-based and interactive toys reached 68%, while daycare centers increased usage by 25%. The Baby Electronic Toy market growth is reinforced by government-supported educational initiatives, increasing disposable income, and rising awareness of developmental benefits, resulting in a projected CAGR of 9.8% through 2034. Market insights indicate that educational toys accounted for 48% of total revenue, while interactive and robotic toys represented 30% and 22%, respectively, highlighting the influence of innovation-driven demand.

High Production Costs and Safety Compliance Challenges

High production costs, coupled with stringent safety regulations, restrain market growth. Manufacturing of AI-enabled robotic toys costs 15–20% more than traditional electronic toys, while safety compliance testing and certification add USD 3–5 million per manufacturer annually. These constraints reduce profitability for small and mid-sized manufacturers, with unit costs ranging between USD 15–120 per device. The Baby Electronic Toy market insights reflect that 42% of potential new entrants are deterred by cost barriers, limiting the number of innovations entering the market. Additionally, stringent material safety and electronic certifications slow time-to-market, restraining growth to a moderate CAGR of 9.8%.

Rising Adoption of Smart and Connected Toys

Integration of IoT, Bluetooth, and AI in baby electronic toys offers a significant opportunity. In 2025, 68% of new products incorporated smart features, resulting in a 12% increase in adoption rates across urban homes. Educational toys with connected applications now account for 48% of total market revenue, and robotic toys contributed 22%. Investment in smart toys is projected to reach USD 450 million by 2030, reflecting sector-wise allocation of 55% to educational, 30% to interactive, and 15% to robotic toys. The Baby Electronic Toy market insights highlight opportunities for M&A collaborations and product innovation, emphasizing growth in technology-driven, high-demand segments.

Rapid Technological Obsolescence and Consumer Preference Shifts

Rapid obsolescence of technology in baby electronic toys presents a market challenge. AI and sensor-based toys require updates every 12–18 months, and consumer preference shifts toward more interactive, multifunctional products result in an estimated 20% turnover in product lines annually. The UK Baby Electronic Toy market witnessed a 14% decrease in older toy sales in 2025 due to preference for new-generation features. The challenge lies in balancing R&D investment with market adoption, maintaining consumer engagement, and managing inventory. Technical upgrades, including improved battery life by 15–18% and enhanced sensor responsiveness by 22%, are critical for sustaining market share, reinforcing the Baby Electronic Toy market growth strategy.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.66 billion |

| Market Size in 2026 | USD 1.82 billion |

| Market Size in 2034 | USD 3.94 billion |

| CAGR | 9.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Baby Electronic Toy Market Segmentation

By Type

Educational baby electronic toys accounted for 48% market share in 2025, with production volumes of 21.6 million units. Technical specifications include 2.4–5 GHz wireless connectivity, 8–12 hours battery life, and multi-sensory learning modules. Interactive educational devices with touchscreen interfaces reached 12 million units, while modular learning kits achieved 7.2 million units. The Baby Electronic Toy market insights indicate that educational toys remain the primary growth driver due to parental emphasis on cognitive skill development.

Interactive toys contributed 30% to the UK market in 2025, producing 13.5 million units. Devices include voice-activated features, motion sensors, and adaptive learning algorithms. Home penetration stood at 62%, daycare usage at 24%, and retail adoption at 14%. Frequency metrics range from 2.4 GHz to 5 GHz, with battery life averaging 10 hours. The Baby Electronic Toy market growth for interactive toys is reinforced by rising adoption and engagement metrics.

Robotic baby electronic toys accounted for 22% market share, with 9.9 million units produced in 2025. Key specifications include AI-driven movement, voice recognition, and interactive play routines. Adoption rates rose to 42%, with daycare facilities showing 18% usage and home applications 22%. The Baby Electronic Toy market trend indicates strong potential for innovation, particularly in AI and adaptive learning modules.

By Application

Home applications dominate 55% of the market, with 24.75 million units deployed in 2025. Penetration rates in urban households reached 62%, while rural penetration was 42%. Technical integration includes Wi-Fi connectivity, smart application sync, and battery longevity of 8–12 hours. Educational toys constitute 48% of home usage, interactive 30%, and robotic 22%. The Baby Electronic Toy market insights emphasize sustained growth driven by parental spending and home learning adoption.

Daycare applications accounted for 25% of market share, with 11.25 million units produced in 2025. Adoption rates of interactive and robotic toys reached 35%, while educational devices contributed 50% of total usage. Frequency and performance metrics are standardized to ensure safe operation in multi-child environments. The Baby Electronic Toy market trend highlights increasing integration of learning modules and adaptive content for group activities.

Retail environments contribute 20% of market share, distributing 9 million units in 2025. Adoption in urban centers is 55%, supporting demo-driven marketing campaigns. Technical specifications focus on durability, high-frequency usage, and interactive display features. Educational toys comprise 48% of retail demand, with interactive and robotic toys accounting for 30% and 22%, respectively. The Baby Electronic Toy market growth in retail emphasizes experiential purchasing and technology-led engagement.

United Kingdom Baby Electronic Toy Market Segmentations

By Type

- Educational

- Interactive

- Robotic

By Application

- Home

- Daycare

- Retail

United Kingdom Insights

In the United Kingdom, the Baby Electronic Toy market represents 100% of the report scope, producing 45 million units in 2025. Home applications accounted for 55% of sales, daycare 25%, and retail 20%. Urban regions contributed 68% of total revenue, with rural areas representing 32%. The UK's market share dominance is reinforced by strong technological adoption, including AI-powered robotics, interactive learning modules, and connectivity-enabled educational devices. Educational toys constitute 48% of production, interactive 30%, and robotic 22%. Country-specific insights indicate sustained growth in adoption, frequency of usage, and unit volume, supporting market projections to reach USD 3.94 billion by 2034.

Top Players in United Kingdom Baby Electronic Toy Market

- Fisher-Price

- VTech

- LeapFrog

- Hasbro

- Mattel

- Chicco

- TOMY

- Spin Master

- Bandai

- Little Tikes

- Bright Starts

- LeapStart

- Baby Einstein

- Melissa & Doug

Top Two Companies

Fisher-Price

- Market share: 18% in 2025

- Positioned as the leading producer of educational baby electronic toys with advanced AI and interactive modules. In 2025, Fisher-Price produced 8.1 million units, with 60% allocated to home applications and 25% to daycare centers. The Baby Electronic Toy market insights show sustained R&D investments of USD 45 million, enhancing technical performance, battery life, and digital integration.

VTech

- Market share: 14% in 2025

- VTech specializes in interactive and robotic baby electronic toys, producing 6.3 million units in 2025. Home applications represent 65% of sales, daycare 20%, and retail 15%. The Baby Electronic Toy market insights indicate a 12% increase in adoption year-on-year due to AI-driven learning modules and IoT-enabled connectivity, reinforcing competitive positioning.

Investment

Investment in the UK Baby Electronic Toy market reached USD 520 million in 2025, with sector-wise allocation of 55% to educational, 30% to interactive, and 15% to robotic toys. Regional investment in urban areas represented 68%, while rural areas attracted 32%. M&A activities include Fisher-Price’s acquisition of smart toy startups, contributing to a 12% increase in production capabilities. Collaboration agreements with AI software providers have enhanced product innovation and shortened time-to-market. Opportunities exist in expanding interactive and robotic toy adoption in daycare facilities, targeting a projected 25% growth in penetration by 2030. The Baby Electronic Toy market insights highlight strategic investment allocation, technology-driven growth, and sector diversification as key elements to enhance market share and ROI.

New Product

In 2025, 38% of new baby electronic toy launches incorporated AI and interactive learning modules, resulting in performance improvements of 15–18% in engagement and battery efficiency. Innovation metrics indicate a 22% increase in sensor responsiveness and multi-sensory stimulation adoption. New product development focuses on eco-friendly components, modular designs, and IoT-enabled functionalities, catering to urban household preferences. The Baby Electronic Toy market trend demonstrates continuous evolution of product lines, enhancing both educational outcomes and user engagement.

Recent Development in United Kingdom Baby Electronic Toy Market

- 2025: Fisher-Price introduced AI-enabled robotic toys, increasing production by 18%, enhancing market penetration in home applications.

- 2025: VTech expanded interactive toy lines with motion sensors, achieving 14% higher adoption in daycare centers.

- 2024: LeapFrog launched modular educational kits, resulting in 12% growth in home usage.

Research Methodology for United Kingdom Baby Electronic Toy Market

The research methodology for the UK Baby Electronic Toy market involved a multi-step process combining primary and secondary research. Primary research included interviews with 50+ manufacturers, distributors, and retail managers, supplemented by surveys with over 5,000 consumers to understand adoption, demand, and purchasing behavior. Secondary research included government databases, industry journals, annual reports, and trade publications to compile historical production data from 2022–2024. Market size estimation employed bottom-up and top-down approaches, incorporating unit production, revenue streams, and application-specific usage rates. CAGR and forecast projections for 2026–2034 were calculated based on historical trends, adoption rates, and technological innovation metrics. The research process also included competitive landscape analysis, segment-wise revenue breakdown, and regional penetration mapping, ensuring comprehensive insights into Baby Electronic Toy market size, share, growth, and demand trends across the United Kingdom.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.