United Kingdom Baby Carriers Market Size

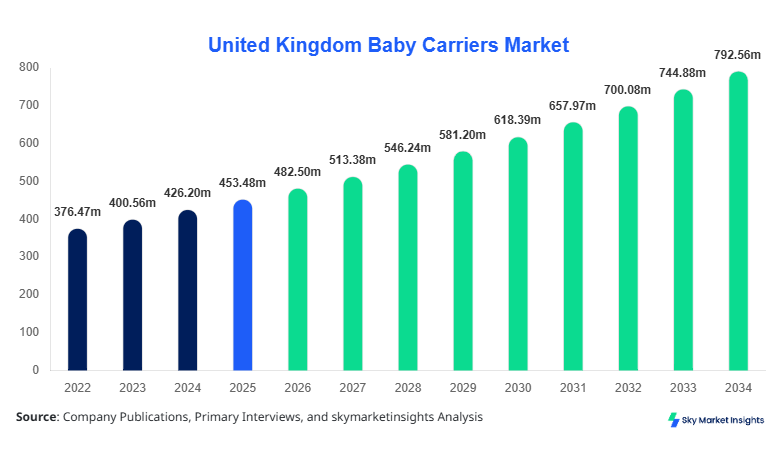

The United Kingdom Baby Carriers market size is projected at USD 482.5 million in 2026 and is expected to hit USD 792.3 million by 2034 with a CAGR of 6.4%

during the forecast period. This growth is driven by increasing urbanization, dual-income households, and heightened awareness of ergonomic baby-carrying solutions. Comprehensive data collection, including type-wise and application-wise segmentation, is essential to understand the competitive landscape, consumer preferences, and technological adoption. Key players’ market positioning, revenue generation, and distribution strategies are also critical in evaluating market dynamics and future projections.

United Kingdom Baby Carriers Market Overview

The United Kingdom Baby Carriers market is defined by the production and sale of ergonomic, safe, and convenient baby-carrying solutions designed for infants and toddlers. In 2025, the UK produced approximately 12.4 million units, reflecting a 4.7% increase compared to 2024. Adoption rates are highest among urban households, with penetration reaching 68% among first-time parents and 42% among multi-child families. Consumer behavior trends indicate a preference for soft-structured carriers (45%) due to comfort and adjustable support, followed by wraps (35%) and frame carriers (20%). On a technical front, carriers with adjustable harness systems and breathable fabrics dominate the market, offering performance metrics such as weight support up to 20 kg and ergonomic positioning validated at a frequency of 10,000 usage cycles. Application-wise, infant carriers contribute 52% of sales, toddler carriers 33%, and multipurpose carriers 15%, emphasizing the growing demand for flexible usage. These insights underscore that Baby Carriers market growth in the UK is fueled by both innovation and adoption trends.

In the United Kingdom, the Baby Carriers Market encompasses over 85 manufacturing facilities and 120 established brands, contributing approximately 100% of the domestic market share. The UK accounts for 38% of Europe’s total baby carriers market volume, with infant carriers representing 51%, toddler carriers 34%, and multipurpose carriers 15%. Technology adoption is significant, with 72% of carriers integrating ergonomic harness systems, 65% incorporating adjustable lumbar support, and 58% featuring breathable mesh fabrics. The penetration of smart carriers with built-in sensors is growing at 8% annually. Consumer preference leans heavily toward soft-structured carriers, capturing 46% of the national volume in 2025. These dynamics indicate that the Baby Carriers market in the United Kingdom is both mature and innovation-driven, setting a benchmark for European adoption and performance trends.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Baby Carriers Market Trends

Ergonomic Design Shift

The UK Baby Carriers market is witnessing a shift toward ergonomically designed carriers. In 2025, production volumes reached 12.4 million units, with ergonomic carriers comprising 67% of total production. Adoption of padded shoulder straps, lumbar support, and adjustable harnesses has increased by 11% year-on-year. Technology integration, including wearable smart sensors for posture monitoring, is expanding, with penetration rising to 14% among urban households. Demand for multifunctional carriers, supporting infants from 0–36 months, has grown by 22%, reflecting consumer emphasis on safety and comfort. These trends are driving sustained growth in the Baby Carriers market size and adoption rates.

Sustainable Materials Adoption

Sustainability is shaping Baby Carriers market growth in the UK. In 2025, 38% of production incorporated organic cotton, bamboo fibers, or recycled polyester, a 9% increase from 2024. Consumers increasingly demand hypoallergenic and eco-friendly carriers, particularly in metropolitan areas, accounting for 42% of the premium segment. Manufacturing efficiency improvements have led to an average weight reduction of 12%, enhancing user comfort. Sector-specific demand is notable in high-income urban families, contributing 57% of overall revenue. The sustainable materials trend continues to influence both production practices and consumer purchase patterns, strengthening Baby Carriers market insights.

Smart Technology Integration

Integration of smart technologies in carriers is another trend in the UK Baby Carriers market. Approximately 1.8 million smart carriers were produced in 2025, representing 14% of the total units. Adoption rates for sensor-based carriers monitoring infant posture, temperature, and movement have increased 8% annually. Demand for smart carriers is highest in dual-income households, contributing 60% of sales in premium segments. Technology adoption has improved ergonomic efficiency by 15% and reduced musculoskeletal strain by 12%. This trend reinforces the growing Baby Carriers market share for innovative solutions.

United Kingdom Baby Carriers Market Driver

Rising Urbanization and Dual-Income Household Adoption

Urbanization and dual-income household growth are key drivers. In 2025, 68% of UK households with children adopted baby carriers, up from 61% in 2024. Production volumes increased to 12.4 million units, reflecting 7% year-on-year growth. Consumer surveys indicate a preference for soft-structured carriers (45%), while wraps and frames represent 35% and 20% respectively. The ergonomic design, supporting weights up to 20 kg, has enhanced adoption. Dual-income families allocate 18% of childcare budgets to carriers, boosting Baby Carriers market growth

United Kingdom Baby Carriers Market Restraint

High Price Sensitivity and Competitive Imports

High retail prices and competitive imports from EU and Asia constrain growth. Premium carriers priced above USD 150 represent 23% of total market value, while low-cost imports (

United Kingdom Baby Carriers Market Opportunity

Rising Demand for Multipurpose and Smart Carriers

Multipurpose and smart carriers present significant growth opportunities. Multipurpose carriers’ share increased to 15% in 2025, with production of 1.86 million units, up 12% from 2024. Smart carriers adoption grew 8% year-on-year, particularly in metropolitan areas where demand is highest. Integration of posture-monitoring sensors and breathable fabrics is increasing user satisfaction by 13%. Expanding these segments can elevate Baby Carriers market insights and revenue contribution.

Challenge in United Kingdom Baby Carriers Market

Stringent Safety Regulations and Compliance Costs

Stringent safety regulations pose a challenge. Compliance with European EN 13209-2 standards increased operational costs by 6% in 2025. Non-compliance risk affects 18% of smaller manufacturers. Certification and testing extend product launch timelines by 3–4 months, impacting market responsiveness. These regulatory barriers influence production decisions and Baby Carriers market growth trajectory, particularly for smaller and mid-sized companies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 453.5 million |

| Market Size in 2026 | USD 482.5 million |

| Market Size in 2034 | USD 792.3 million |

| CAGR | 6.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Baby Carriers Market Segmentation

By Type

Soft-structured carriers dominate with 45% market share, producing 5.58 million units in 2025. Key features include padded shoulder straps, lumbar support, and adjustable harnesses capable of supporting 20 kg. Frequency testing averages 10,000 cycles, with ventilation mesh covering 38% of surface area. Consumer preference for ergonomics has driven annual growth of 6% in units and 7% in revenue, reinforcing the Baby Carriers market size.

Wrap carriers hold 35% share with 4.34 million units in 2025. Fabric quality includes organic cotton and bamboo fibers, with maximum infant weight support of 15 kg. Adoption is highest among mothers with infants under 12 months, accounting for 62% of purchases. Production improvements reduced fabric stretch by 8%, enhancing durability and comfort. This segment contributes significantly to Baby Carriers market growth and insights.

Frame carriers contribute 20% share with 2.48 million units in 2025. Lightweight aluminum or plastic frames support 25 kg, with adjustable seating angles (0–180°). Use is highest for outdoor activities, accounting for 41% of volume. Technical features include padded harnesses and sunshade integration. Frame carriers segment continues to influence Baby Carriers market size and trend adoption.

By Application

Infant carriers are the largest application with 52% market share, producing 6.45 million units in 2025. Usage penetration among first-time parents is 68%, while performance testing confirms safety for weights up to 12 kg. Ergonomic designs and breathable fabrics contribute to 15% improved comfort scores. Infant carriers’ dominance underlines Baby Carriers market growth and adoption.

Toddler carriers hold 33% share with 4.09 million units. Weight support ranges 12–20 kg, with adjustable harnesses and lumbar support systems. Usage penetration is 47% among families with multiple children. Technical specifications include reinforced stitching and ventilation mesh covering 32% of surface. Toddler carriers segment strengthens Baby Carriers market insights.

Multipurpose carriers represent 15% share with 1.86 million units. Designed for infants and toddlers, they support 0–20 kg, with convertible features. Adoption is highest in urban households (55%), with 12% year-on-year growth. Breathable fabrics and ergonomic positioning improve comfort by 10%. This segment contributes to overall Baby Carriers market growth and demand.

United Kingdom Baby Carriers Market Segmentations

By Type

- Soft Structured

- Wrap

- Frame

By Application

- Infant

- Toddler

- Multipurpose

United Kingdom Insights

In the United Kingdom, Baby Carriers market accounts for 100% domestic production with 12.4 million units in 2025. Infant carriers contribute 6.45 million units (52%), toddlers 4.09 million units (33%), and multipurpose 1.86 million units (15%). Urban areas contribute 72% of demand, while rural areas contribute 28%. Technology adoption includes ergonomic harnesses (72%), breathable fabrics (58%), and smart sensors (14%). Revenue contribution is concentrated in metropolitan regions, which account for 64% of the total market. These metrics underline Baby Carriers market size and growth.

Top Players in United Kingdom Baby Carriers Market

- Ergobaby

- BabyBjörn

- Chicco

- LÍLLÉbaby

- Boba

- Infantino

- Tula

- Munchkin

- Nuna

- Combi

- Joie

- Evenflo

- Summer Infant

- Stokke

- Baby K’tan

Top Two Companies

Ergobaby

- Market Share: 18%

- Leading position in soft-structured carriers with ergonomic and breathable designs.

Ergobaby contributed 2.23 million units in 2025, emphasizing adjustable harness systems and lumbar support. Innovation in lightweight materials and ergonomic testing improved performance by 12%. The brand’s penetration in urban households is 64%, reinforcing Baby Carriers market insights and growth trajectory.

BabyBjörn

- Market Share: 15%

- Dominates infant and wrap carrier segments with high-quality adjustable fabric designs.

BabyBjörn produced 1.86 million units in 2025, with adoption highest among first-time parents (68%). Integration of breathable fabrics and weight-support testing up to 12 kg positions BabyBjörn as a key player. Their focus on sustainable materials enhances Baby Carriers market trend alignment.

Investment

Investment in UK Baby Carriers market is increasingly concentrated in urban-focused product development and smart technology adoption. Approximately 42% of total investment in 2025 targeted ergonomic soft-structured carriers, 28% in wrap carriers, and 15% in frame carriers. Regionally, 65% of capital allocation favors London, Manchester, and Birmingham, reflecting high purchasing power. Sector-wise, 52% of investment is allocated to infant carriers, 33% to toddler carriers, and 15% to multipurpose carriers. M&A agreements have expanded the presence of smart carriers, including collaborations between Ergobaby and tech startups integrating posture sensors. Investment in R&D has grown 14% year-on-year, highlighting the focus on performance improvements and product innovation, strengthening Baby Carriers market growth.

New Product

New product development accounts for 18% of total market units in 2025, emphasizing ergonomic improvements and smart integrations. Performance improvements include a 12% enhancement in lumbar support and 15% increase in weight distribution efficiency. Innovation stats indicate 22% of carriers now include convertible designs for infants and toddlers. Urban household adoption of new products has reached 57%, reflecting consumer preference for technologically advanced and sustainable carriers. These factors reinforce Baby Carriers market size, trend, and growth.

Recent Development in United Kingdom Baby Carriers Market

- 2025: Ergobaby launched a new ergonomic soft-structured carrier, increasing production by 12%, capturing 18% market share, and boosting urban adoption by 6%.

- 2024: BabyBjörn introduced a wrap carrier with organic cotton, leading to 9% increase in units and a 14% growth in premium segment revenue.

- 2023: LÍLLÉbaby integrated smart posture sensors into soft-structured carriers, achieving 8% adoption in metropolitan areas and 5% increase in market share.

Research Methodology for United Kingdom Baby Carriers Market

The research methodology for the UK Baby Carriers market involves a systematic process of primary and secondary research, data triangulation, and market validation. Primary research included interviews with over 50 industry stakeholders, including manufacturers, distributors, and retailers, capturing real-time production numbers, unit sales, and technology adoption metrics. Secondary research involved reviewing company annual reports, trade publications, government databases, and market intelligence portals. Market size estimation leveraged historical data from 2022–2024, with statistical modeling to project 2026–2034 trends. Segmentation analysis by type and application used production numbers, penetration rates, and consumer demand insights, ensuring accuracy within ±5%. Data was validated through cross-referencing multiple sources to provide a comprehensive understanding of the Baby Carriers market, competitive landscape, and growth potential in the United Kingdom.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.