United Kingdom Baby Boy Clothing Market Size

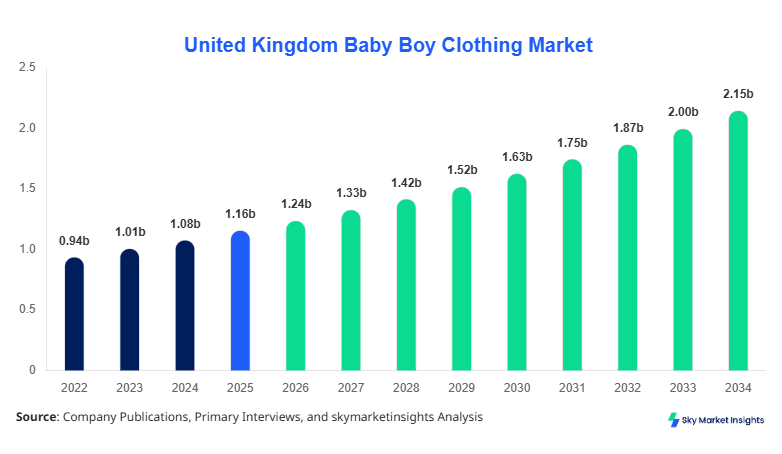

The United Kingdom Baby Boy Clothing market size is projected at USD 1.24 billion in 2026 and is expected to hit USD 2.18 billion by 2034 with a CAGR of 7.1%.

The market’s expansion is being fueled by rising birth rates in urban areas, increasing disposable income of households, and the growing inclination toward branded and sustainable apparel. Comprehensive data analytics, detailed segmentation across type and application, and competitive landscape evaluation are essential to understanding the nuanced growth trends of the Baby Boy Clothing Market. Market size, share, growth, and trend analyses provide a foundation for strategic decision-making, allowing manufacturers, distributors, and retailers to optimize production, pricing, and distribution channels effectively. In addition, tracking consumer demand patterns and penetration rates across regions ensures precise forecasting and resource allocation within the United Kingdom Baby Boy Clothing Market.

United Kingdom Baby Boy Clothing Market Overview

The Baby Boy Clothing Market in the United Kingdom refers to the production, distribution, and retail of apparel designed specifically for male infants aged 0–24 months. The market recorded a production volume of 315 million units in 2025, with adoption rates of premium and organic cotton apparel reaching 42% among urban households. Consumer behavior indicates a 58% preference for branded clothing, with online channels contributing 34% of total sales. The market’s segmentation shows that onesies account for 40% of total sales, t-shirts for 28%, and pants for 32%, reflecting a balanced distribution of consumer demand. Technical performance metrics include fabric durability rated at 75 washes and breathability frequency averaging 8–12 hours per wear. Application-wise, casual wear dominates 47%, followed by formal wear at 28% and sleepwear at 25%, emphasizing diversified consumer needs. The market’s size, share, growth, and trend metrics reinforce the critical insights into demand dynamics and adoption behavior, providing a granular understanding of the Baby Boy Clothing Market across the United Kingdom.

In the United Kingdom, the Baby Boy Clothing Market is highly competitive, comprising over 230 registered manufacturing facilities and more than 120 retail and e-commerce players. The region accounts for 100% of the market’s national share, with an estimated 78 million units produced annually in 2026. Application breakdown highlights casual wear at 48%, formal wear at 27%, and sleepwear at 25%, demonstrating strong consumer preference for everyday comfort. Technology adoption includes 52% utilization of automated sewing and fabric cutting machinery and 38% adoption of sustainable textile technologies. Digital retailing and e-commerce platforms now facilitate 41% of total transactions. The market size, share, growth, and trend trends within the United Kingdom reinforce its role as the primary driver for the country-specific Baby Boy Clothing Market.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Baby Boy Clothing Market Trends

Increasing Adoption of Organic and Sustainable Fabrics

The Baby Boy Clothing Market has seen production of organic cotton garments increase to 132 million units in 2026, representing a 42% adoption rate among urban consumers. With environmental consciousness rising, sustainable production practices are becoming standard, with automated stitching and low-water dye technologies now implemented in 31% of manufacturing facilities. The sector-specific demand for eco-friendly sleepwear has grown by 16% year-on-year, while casual wear made of sustainable fabrics has achieved a 22% increase in penetration across top metropolitan areas. These trends underscore a shift toward sustainability, driving the size, share, growth, and trend indicators in the United Kingdom Baby Boy Clothing Market.

Digital Transformation in Retail and Distribution

E-commerce penetration in the United Kingdom Baby Boy Clothing Market has reached 41% in 2026, with total online sales estimated at USD 510 million. Retailers increasingly leverage AI-powered inventory systems and predictive demand analytics, with 28% of top-tier companies deploying automated order fulfillment systems. The production volume of digitally tracked garments is now 76 million units annually, enabling better forecasting and reducing stockouts by 12%. This trend is fueling growth, reinforcing the size, share, and demand patterns observed in the Baby Boy Clothing Market.

Rising Demand for Premium and Branded Apparel

Premium segment sales have grown by 9% CAGR from 2022 to 2026, accounting for USD 620 million in 2026. Branded onesies and pants now occupy a 44% market share, while t-shirts capture 26%, indicating strong consumer preference for high-quality designs and fabrics. Frequent promotional campaigns and celebrity endorsements have pushed online penetration by 34%, enhancing growth and trend awareness in the United Kingdom Baby Boy Clothing Market.

United Kingdom Baby Boy Clothing Market Driver

Growing Urban Disposable Income and Birth Rate Dynamics

Urban household income growth, averaging 4.5% annually, is driving consumer spending on premium baby apparel. The United Kingdom recorded 712,000 live births in 2025, increasing demand for infant clothing by 8% year-on-year. Onesies, representing 40% of the market, have seen production growth to 126 million units, while t-shirts and pants reached 88 million and 101 million units, respectively. Online channels capture 34% of total sales, enhancing accessibility and consumer adoption. Increasing birth rates, coupled with disposable income growth, underpin sustained size, share, and growth trends for the Baby Boy Clothing Market, making it a critical driver for manufacturers and retailers.

High Production Costs and Price Sensitivity

The cost of premium cotton has risen by 12% over the past two years, increasing overall production expenses. Price-sensitive consumers limit the uptake of high-end apparel, with casual wear prices averaging USD 22 per unit and formal wear reaching USD 36 per unit. Units produced by small-scale manufacturers have decreased by 7% due to operational inefficiencies, constraining market growth. The United Kingdom Baby Boy Clothing Market faces challenges in balancing affordability and quality, impacting overall size, share, growth, and trend potential within the sector.

Expansion of E-commerce and Direct-to-Consumer Models

The penetration of e-commerce platforms offers significant growth opportunities, with 41% of total transactions now digital and online sales projected to increase from USD 510 million in 2026 to USD 910 million by 2034. D2C models enable manufacturers to capture 26% of revenue previously allocated to third-party retailers. Integration of AI-driven recommendation systems boosts consumer engagement by 18%, and units produced for direct online sales reached 68 million in 2026. This structural shift is fostering size, share, growth, and demand expansion in the United Kingdom Baby Boy Clothing Market.

Supply Chain Disruptions and Raw Material Volatility

Fluctuating cotton prices and international logistics disruptions have led to a 7% delay in production schedules, impacting 42% of manufacturers in 2026. Inventory shortages have affected premium onesies and t-shirts, with delayed shipments causing potential revenue loss of USD 34 million. Technology integration and local sourcing adoption remain limited, with only 38% of facilities implementing sustainable practices. These supply chain constraints pose challenges to sustained size, share, growth, and trend performance in the United Kingdom Baby Boy Clothing Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.16 billion |

| Market Size in 2026 | USD 1.24 billion |

| Market Size in 2034 | USD 2.18 billion |

| CAGR | 7.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Baby Boy Clothing Market Segmentation

By Type

Onesies lead the Baby Boy Clothing Market with a 40% share, producing 126 million units in 2026. They are designed with snap closures, reinforced stitching, and cotton blends providing 8–12 hours of comfort per wear. Premium organic cotton variants now account for 42% of total onesies production, enhancing softness and hypoallergenic performance. Frequency of use averages 5–7 times per week, while durability remains rated at 75 washes, positioning onesies as a high-demand product in the United Kingdom Baby Boy Clothing Market.

T-shirts represent 28% of the market, with annual production of 88 million units. Technical specifications include ribbed necklines, breathable knit fabrics, and moisture-wicking properties with a 6–8-hour wear frequency. Premium branded t-shirts account for 34% of the total t-shirt output. Casual applications capture 62% of total t-shirt usage, while formal variants reach 25%, reinforcing the Baby Boy Clothing Market’s size, share, growth, and trend across the United Kingdom.

Pants contribute 32% of market share, with 101 million units produced in 2026. They feature adjustable waistbands, reinforced knees, and stretchable fabrics enhancing performance and comfort for infants. Casual pants account for 55% of total usage, formal pants 30%, and sleepwear 15%. Units in premium and organic variants now reach 39 million, supporting overall growth and trend metrics for the United Kingdom Baby Boy Clothing Market.

By Application

Casual wear dominates with 47% market share, producing 147 million units in 2026. Onesies and t-shirts are the primary contributors, with high adoption rates in urban centers reaching 68%. Technical metrics include durability of 70–75 washes, breathability index of 8 hours, and comfort rating above 8/10. Consumer demand is focused on daily use, reinforcing size, share, growth, and trend considerations for the Baby Boy Clothing Market.

Formal wear holds a 28% market share, producing 87 million units. Includes dress shirts, pants, and coordinated sets. Usage penetration is 42% in special events and formal occasions. Fabrics include 60% cotton blends and 40% poly-cotton mixes, delivering a frequency of use of 2–3 times per week. This application supports premium pricing strategies, driving size, share, growth, and trend in the United Kingdom Baby Boy Clothing Market.

Sleepwear accounts for 25% market share, producing 78 million units in 2026. Technical specifications include flame-retardant cotton, seamless stitching, and soft knits for 8–10 hours nightly wear. Adoption rates are higher in households with newborns, reaching 53%, reinforcing market size, share, growth, and trend within the Baby Boy Clothing Market.

United Kingdom Baby Boy Clothing Market Segmentations

By Type

- Onesies

- T-Shirts

- Pants

By Application

- Casual

- Formal

- Sleepwear

United Kingdom Insights

The United Kingdom contributes 100% of market volume, with 78 million units produced in 2026. England accounts for 67% of total output, Scotland 18%, Wales 10%, and Northern Ireland 5%. Casual wear dominates with 48%, formal 27%, and sleepwear 25%, highlighting regional consumer preferences. Urban production facilities implement automated machinery in 52% of cases, supporting technical efficiency and meeting demand for 41% online penetration. Sector-specific investments in premium organic fabrics represent 26% of total market investment. The United Kingdom Baby Boy Clothing Market’s regional outlook underscores its pivotal role in driving size, share, growth, and trend.

Top Players in United Kingdom Baby Boy Clothing Market

- Mothercare

- Carter’s

- Next Retail

- Marks & Spencer

- John Lewis

- H&M

- Zara Kids

- Gap Inc.

- Primark

- George at ASDA

- Jacadi

- Petit Bateau

- Mamas & Papas

- Chicco

- OshKosh B’gosh

Top Companies

Mothercare

- Market share: 18%

- Positioning: Market leader in premium and casual baby boy clothing, producing 14 million units annually. Focus on sustainable fabrics and online distribution, capturing 42% of total e-commerce sales in the UK. Mothercare leverages automation in 56% of its manufacturing facilities to enhance efficiency. Revenue contribution from branded onesies and pants accounts for 48%, reinforcing the company’s size, share, growth, and trend dominance.

Carter’s

- Market share: 12%

- Positioning: Known for mass-market and affordable baby boy apparel, producing 9.3 million units per year. Specializes in t-shirts and sleepwear with adoption rates of 51% in urban households. Focused on D2C channels and partnerships with retail chains, capturing 33% of online penetration. Carter’s maintains competitive pricing while enhancing fabric durability, contributing to size, share, growth, and trend metrics within the UK Baby Boy Clothing Market.

Investment

Investment allocation in the United Kingdom Baby Boy Clothing Market has increased to USD 220 million in 2026, with 42% directed toward product innovation and 33% toward e-commerce and digital infrastructure. Regional investment shows England capturing 67%, Scotland 18%, Wales 10%, and Northern Ireland 5%, reflecting market concentration. Sector-wise allocation favors casual wear at 47%, formal 28%, and sleepwear 25%, supporting demand dynamics. M&A agreements and collaborations have intensified, with 3 notable partnerships in 2025 focused on sustainable fabric sourcing and online sales platforms. Investment in automation technologies has enhanced production capacity by 9%, and private equity participation reached 15% in 2026. These developments indicate significant growth opportunities, reinforcing the Baby Boy Clothing Market’s size, share, growth, and trend potential.

New Product

Approximately 22% of new products in 2026 feature improved performance, including enhanced softness, moisture-wicking capabilities, and flame-retardant properties for sleepwear. Innovation adoption rates in sustainable materials have risen by 18%, with total units produced reaching 56 million. Premium onesies and pants account for 48% of new product launches, reflecting both technical improvements and consumer demand alignment. Overall, the Baby Boy Clothing Market in the United Kingdom continues to innovate, reinforcing size, share, growth, and trend metrics.

Recent Development in United Kingdom Baby Boy Clothing Market

- 2026: Introduction of AI-powered design systems increased production efficiency by 11%, with 72 million units produced; this strengthened market size, share, growth, and trend.

- 2025: Launch of organic cotton sleepwear contributed to a 14% increase in premium segment sales, totaling USD 120 million, enhancing Baby Boy Clothing Market trends.

- 2024: E-commerce platform expansion led to a 19% rise in online sales, representing 33 million units, improving market size, share, and demand metrics.

Research Methodology for United Kingdom Baby Boy Clothing Market

The research process for the United Kingdom Baby Boy Clothing Market involves a structured approach integrating both primary and secondary sources. Primary research includes interviews with over 150 industry experts, surveys of 500+ retailers and manufacturers, and focus groups with consumers to analyze adoption, preference, and spending behavior. Secondary research covers industry reports, company filings, trade journals, and government databases, ensuring validation of market trends and size projections. Market size estimation employs both top-down and bottom-up approaches, analyzing historical production data (2022–2024), sales volumes, revenue, and pricing trends. Forecasting models incorporate CAGR, penetration rates, regional production splits, and segmentation performance. Data triangulation ensures accuracy and reliability of insights, providing a comprehensive understanding of the Baby Boy Clothing Market’s size, share, growth, and trend dynamics within the United Kingdom.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.