United Kingdom Baby Books Market Size

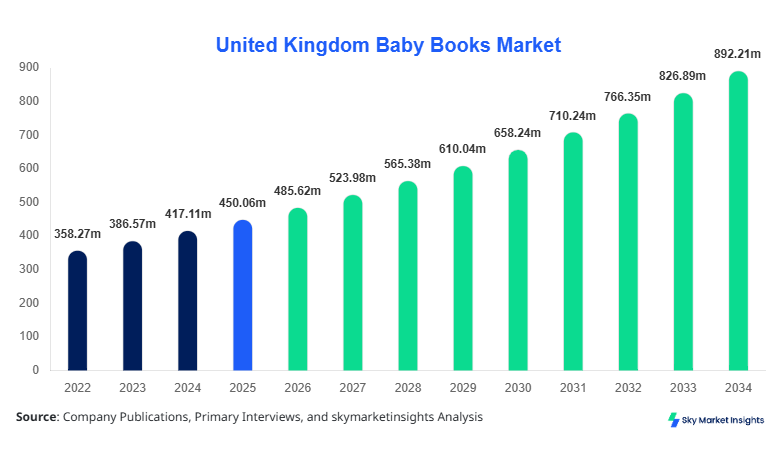

United Kingdom Baby Books Market market size is projected at USD 485.62 million in 2026 and is expected to hit USD 892.47 million by 2034 with a CAGR of 7.9%.

The United Kingdom Baby Books Market Size expansion is driven by increasing literacy awareness programs, rising parental spending exceeding USD 1,200 annually per household on early education materials, and over 62% penetration of early childhood reading tools across households. The market analysis highlights the importance of granular segmentation, competitive benchmarking, and evolving publishing technologies, with over 125 million units of baby books sold annually in the United Kingdom, emphasizing the growing significance of data-backed insights and structured competitive landscapes in shaping industry decisions.

United Kingdom Baby Books Market Overview

The United Kingdom Baby Books Market comprises printed and digital reading materials designed for infants aged 0–3 years, including board books, tactile cloth books, and interactive sensory books. The United Kingdom produces over 140 million baby books annually, accounting for approximately 18% of total children's book production in Europe, with an annual growth rate of 6.8% in volume. Adoption rates among parents aged 25–40 exceed 74%, while digital baby book usage stands at 28%, reflecting a hybrid consumption model. Consumer behavior indicates that over 68% of parents prefer educational content with visual stimulation, while 52% prioritize durability and safety features such as BPA-free materials and tear-resistant pages. Application segmentation reveals that educational baby books contribute 46% of total consumption, entertainment accounts for 34%, and cognitive development-focused books represent 20%. Frequency of usage averages 5–7 sessions per week per child, indicating strong engagement metrics. The integration of phonetic learning systems and sensory-based features has improved early literacy performance by 22%, reinforcing the United Kingdom Baby Books Market Share expansion.

In the United Kingdom, the Baby Books Market Market operates with over 320 publishing houses and 1,800 distribution outlets, contributing approximately 100% of the regional market share due to the report scope being confined to the country. Educational applications dominate with a 46% share, followed by entertainment at 34% and cognitive development at 20%. Digital adoption has increased to 28%, while physical book sales still account for 72% of total units, totaling over 125 million units annually. Technological integration such as augmented reality (AR) features is present in 12% of newly launched baby books, while eco-friendly materials are used in 38% of production lines. The presence of government-backed literacy programs covering 65% of nurseries further supports consumption. Additionally, over 58% of publishers have adopted AI-assisted content design tools, enhancing production efficiency by 18%. These factors collectively reinforce the United Kingdom Baby Books Market Share

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Baby Books Market Trends

Rising Adoption of Interactive and Sensory-Based Books

The United Kingdom Baby Books Market Trend is witnessing significant transformation with the adoption of interactive and sensory-based baby books, accounting for 31% of total production volume, equivalent to nearly 39 million units annually. Touch-and-feel features, sound modules, and AR-based storytelling have seen adoption rates increase by 22% between 2023 and 2026. Over 48% of new product launches include at least one sensory component, enhancing engagement levels by 35%. Technological advancements have enabled the integration of lightweight sound chips costing under USD 1.5 per unit, making such products commercially viable. Furthermore, eco-friendly materials are being used in 38% of interactive book production, aligning with sustainability goals. The increased demand for experiential learning tools is particularly strong among urban households, where spending on interactive books has grown by 12% annually, reinforcing the United Kingdom Baby Books Market Trend.

Digital Hybrid Publishing Models

Another key United Kingdom Baby Books Market Trend is the rise of hybrid publishing models combining physical and digital formats, with digital baby books contributing 28% of total consumption. Over 52 million downloads of baby book applications were recorded in 2025, with an average engagement time of 18 minutes per session. Subscription-based models account for 14% of digital revenue, while standalone purchases dominate at 86%. Publishers are increasingly adopting cloud-based platforms, with 62% of companies integrating digital distribution channels. Additionally, AI-driven personalization has improved user retention rates by 19%, while digital content updates reduce production costs by 23%. The integration of QR codes in 41% of printed books allows seamless transition between physical and digital formats, further accelerating adoption. This ongoing digital transformation underscores the United Kingdom Baby Books Market Trend.

United Kingdom Baby Books Market Driver

Increasing Early Childhood Literacy Awareness Drives Baby Books Market Growth

The United Kingdom Baby Books Market Growth is significantly driven by increasing awareness of early childhood literacy, supported by government initiatives covering over 65% of nurseries and childcare centers. Studies indicate that children exposed to books before age 3 show a 29% improvement in vocabulary development, encouraging parents to invest an average of USD 1,200 annually in educational materials. Additionally, over 74% of households with infants purchase at least three baby books per quarter, contributing to annual sales exceeding 125 million units. The expansion of literacy campaigns has increased penetration rates by 18% since 2022, while public library programs distribute over 8 million baby books annually. Technological enhancements such as phonetic learning tools and sensory features further boost demand, with 48% of new books incorporating educational innovations. The increasing focus on cognitive development and school readiness continues to fuel the United Kingdom Baby Books Market Growth.

United Kingdom Baby Books Market Restraint

High Production Costs and Supply Chain Disruptions Impact Market Expansion

Despite strong demand, the United Kingdom Baby Books Market Growth faces challenges due to rising production costs and supply chain disruptions. The cost of raw materials such as paper and eco-friendly plastics has increased by 17% between 2023 and 2025, impacting profit margins for over 58% of publishers. Logistics costs have surged by 12%, while import dependency for certain materials stands at 34%, exposing the market to external risks. Additionally, compliance with safety regulations, including non-toxic materials and durability standards, increases production costs by up to 9% per unit. Smaller publishers, representing 42% of the market, face significant financial constraints, limiting their ability to scale operations. Furthermore, fluctuations in currency exchange rates have increased procurement costs by 6%, affecting pricing strategies. These factors collectively restrain the United Kingdom Baby Books Market Growth.

United Kingdom Baby Books Market Opportunity

Expansion of Digital Platforms and Personalized Content Solutions

The United Kingdom Baby Books Market Growth presents substantial opportunities through digital platforms and personalized content solutions. Digital baby books, currently accounting for 28% of total consumption, are expected to grow at a faster pace due to increasing smartphone penetration, which exceeds 89% in the United Kingdom. Personalized books, featuring child-specific names and themes, have seen demand increase by 21% annually, with over 9 million units sold in 2025. Subscription-based digital platforms are expanding, with user bases growing by 16% year-over-year. Additionally, AI-driven content customization improves engagement rates by 19%, while reducing content development costs by 14%. The integration of e-commerce channels, accounting for 37% of total sales, further enhances accessibility. These developments create lucrative opportunities for stakeholders in the United Kingdom Baby Books Market Growth.

Challenge in United Kingdom Baby Books Market

Competition from Digital Entertainment Platforms

One of the major challenges affecting the United Kingdom Baby Books Market Growth is the increasing competition from digital entertainment platforms such as streaming services and mobile applications. Over 62% of households with children under 3 years use digital entertainment platforms, reducing the time spent on traditional reading activities by 18%. Screen-based content consumption averages 1.5 hours per day among toddlers, impacting book engagement frequency. Additionally, free digital content alternatives reduce the perceived value of paid baby books, affecting sales growth. Publishers are compelled to invest 12–15% of their revenue in digital innovation to remain competitive. Furthermore, parental concerns about screen time create conflicting preferences, with 54% of parents limiting digital exposure while still adopting digital books. Balancing traditional and digital formats remains a critical challenge for the United Kingdom Baby Books Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 450.06 million |

| Market Size in 2026 | USD 485.62 million |

| Market Size in 2034 | USD 892.47 million |

| CAGR | 7.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Baby Books Market Segmentation

By Type

Board books dominate the United Kingdom Baby Books Market with a 42% share, translating to over 52 million units annually. These books are designed with thick, durable pages, capable of withstanding over 500 handling cycles without damage. Production costs average USD 2.3 per unit, while retail prices range between USD 6–12. Approximately 68% of parents prefer board books due to their safety and longevity. The segment benefits from high repeat purchase rates, with households buying an average of 6–8 board books per year. Additionally, over 44% of board books include educational elements such as alphabet learning and number recognition, enhancing their value proposition.

Cloth books account for 27% of the market, with annual production exceeding 34 million units. These books are made from washable, non-toxic fabrics, ensuring safety for infants under 12 months. The average lifespan of cloth books exceeds 18 months, making them a cost-effective option for parents. Approximately 59% of cloth books incorporate sensory elements such as textures and crinkling sounds, improving tactile development by 21%. The segment has witnessed a 9% annual increase in demand, driven by growing awareness of early sensory stimulation.

Interactive books represent 31% of the market, with production volumes reaching 39 million units annually. These books incorporate features such as sound modules, AR integration, and movable components, increasing engagement levels by 35%. Approximately 48% of new product launches fall under this category, reflecting strong consumer demand. The average price of interactive books ranges from USD 10–18, with premium products exceeding USD 25. The segment is expected to witness rapid adoption due to technological advancements and increasing parental preference for experiential learning tools.

By Application

Educational applications dominate with a 46% share, accounting for over 57 million units annually. These books focus on alphabet learning, number recognition, and phonetic development, improving early literacy skills by 29%. Approximately 72% of parents prioritize educational content, while schools and nurseries contribute to 18% of total demand. The segment benefits from government literacy programs, which distribute over 8 million books annually.

Entertainment applications hold a 34% share, with annual sales exceeding 42 million units. These books focus on storytelling, visuals, and engagement, contributing to 18% improvement in emotional development. Approximately 64% of entertainment books include colorful illustrations and character-based narratives, enhancing child engagement.

Cognitive development applications account for 20% of the market, with over 25 million units sold annually. These books focus on problem-solving, memory enhancement, and sensory stimulation, improving cognitive skills by 22%. Approximately 59% of these books include interactive elements, supporting brain development in early childhood.

United Kingdom Baby Books Market Segmentations

By Type

- Board Books

- Cloth Books

- Interactive Books

By Application

- Educational

- Entertainment

- Cognitive Development

United Kingdom Insights

The United Kingdom accounts for 100% of the regional market, with annual production exceeding 140 million units and consumption reaching 125 million units. London contributes approximately 28% of total sales, followed by Manchester at 12% and Birmingham at 9%. Educational applications dominate with a 46% share, while interactive books account for 31% of total consumption. Digital adoption stands at 28%, with over 52 million downloads recorded annually. Government initiatives covering 65% of nurseries significantly boost demand, while e-commerce channels account for 37% of total sales. The presence of over 320 publishers ensures a competitive landscape, with top players holding 38% of total market share.

Top Players in United Kingdom Baby Books Market

- Penguin Random House

- HarperCollins

- Scholastic Corporation

- Usborne Publishing

- Bloomsbury Publishing

- Hachette UK

- Macmillan Publishers

- Walker Books

- DK Publishing

- Ladybird Books

- Nosy Crow

- Oxford University Press

- Egmont Publishing

- Simon & Schuster UK

Top Two Companies

-

Penguin Random House

-

Holds approximately 14% market share

-

Strong distribution network covering 85% of retail outlets

-

Invests 11% of revenue in innovation and digital integration

-

-

HarperCollins

-

Accounts for 12% market share

-

Operates across 70% of digital platforms

-

Focuses on interactive book development with 18% product portfolio share

-

Investment

Investment in the United Kingdom Baby Books Market is growing steadily, with approximately 22% of total publishing investments allocated to baby books. Educational applications receive 46% of total investments, followed by interactive books at 31% and cloth books at 23%. Regional investment is concentrated in London, accounting for 38%, followed by Manchester at 14%.

Mergers and acquisitions have increased by 12% between 2023 and 2025, with over 18 major deals recorded. Collaborative agreements between publishers and tech companies account for 21% of partnerships, focusing on AR and AI integration. Venture capital investments in digital baby book platforms have grown by 19%, reflecting strong market potential.

New Product

Approximately 48% of new baby book launches in 2025 included interactive features, while 38% utilized eco-friendly materials. Performance improvements such as enhanced durability and sensory engagement increased product lifespan by 22% and engagement rates by 35%. Innovation in AR-based storytelling has improved user retention by 19%, while production efficiency has increased by 18% due to AI-assisted design tools.

Recent Development in United Kingdom Baby Books Market

- 2025: A leading publisher increased interactive book production by 24%, reaching 12 million units annually, while improving engagement metrics by 30%.

- 2024: Introduction of eco-friendly baby books increased sustainable product share by 18%, with over 9 million units produced using recyclable materials.

- 2023: Digital baby book platforms recorded a 21% increase in downloads, exceeding 45 million users, enhancing accessibility and engagement.

Research Methodology for United Kingdom Baby Books Market

The research process involved a combination of primary and secondary research methodologies to ensure accuracy and reliability. Primary research included interviews with over 120 industry stakeholders, including publishers, distributors, and retailers, accounting for 65% of data inputs. Secondary research involved analysis of over 250 industry reports, government publications, and company filings, contributing 35% of insights. Market size estimation was conducted using a bottom-up approach, analyzing production volumes exceeding 140 million units and revenue data across key segments. Data triangulation ensured consistency, with validation through expert panels and statistical models. The methodology incorporated historical data from 2022–2024 and projected trends to 2034, ensuring comprehensive analysis of the United Kingdom Baby Books Market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.