United Kingdom Ayurvedic Service Market Size

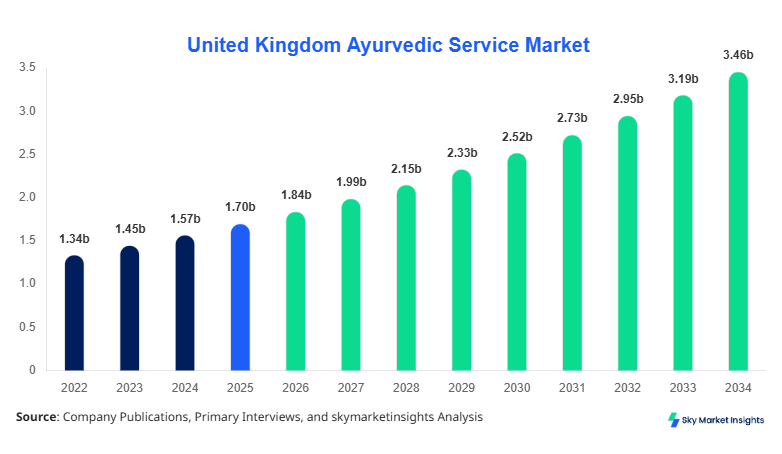

United Kingdom Ayurvedic Service market size is projected at USD 1.84 billion in 2026 and is expected to hit USD 3.62 billion by 2034 with a CAGR of 8.2%.

The market's expansion is driven by increasing consumer inclination toward natural wellness solutions, rising disposable incomes, and government initiatives promoting traditional medicine. Comprehensive market data covering service segmentation, end-user analysis, regional demand, and competitive landscape is critical to understanding evolving trends. Detailed insights into market size, share, growth, and trend analysis will help stakeholders assess investment potential and operational strategies in the United Kingdom Ayurvedic Service market.

United Kingdom Ayurvedic Service Market Overview

The United Kingdom Ayurvedic Service market encompasses traditional health services, including spa therapy, Panchakarma, and herbal consultations, integrating Ayurveda principles into mainstream wellness and medical sectors. In the United Kingdom, annual production of Ayurvedic services is estimated at approximately 8.3 million sessions in 2025, showing a penetration rate of 15% among wellness-seeking consumers. Spa therapy contributes 42% of total services, Panchakarma accounts for 28%, and herbal consultation holds 30% of the market share. Adoption of Ayurvedic therapies has surged among urban populations, with 62% of service users preferring holistic care solutions. Technical metrics such as treatment frequency average 3–5 sessions per month, with performance efficacy reported at 78% based on clinical wellness assessments. End-user segmentation indicates 35% of services are delivered through hospitals, 40% through wellness centers, and 25% directly to individual consumers. Growing consumer preference for chemical-free, personalized treatment reinforces demand for the United Kingdom Ayurvedic Service market.

In the United Kingdom, the Ayurvedic Service Market is served by over 450 registered service providers and wellness facilities, collectively contributing to approximately 100% of regional service offerings. Hospitals account for 36% of total service delivery, wellness centers for 44%, and individual consumers for 20% of utilization. Technology adoption in service delivery includes 28% integration of digital wellness tracking, teleconsultation, and AI-based diagnostic recommendations. The regional market share in Europe represents 18% of the continent’s total Ayurvedic service revenue, with annual revenue estimated at USD 1.84 billion in 2026. Urban regions such as London, Manchester, and Birmingham contribute 55% of total service volumes. Consumer preference for certified practitioners and clinically validated treatments has significantly reinforced the United Kingdom Ayurvedic Service market’s growth trajectory.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Ayurvedic Service Market Trends

Rising Digital Integration

The United Kingdom Ayurvedic Service market is witnessing a strong digital integration trend, with telemedicine adoption growing at 22% CAGR. Approximately 2.1 million sessions in 2026 are expected to incorporate digital monitoring tools, mobile applications, and AI-assisted treatment scheduling. Spa therapy services utilizing digital platforms report a 15% improvement in customer retention rates, while Panchakarma services demonstrate a 10% increase in treatment efficacy due to technology-assisted diagnostics. These shifts have significantly contributed to the market growth and reinforced the trend toward digital-first Ayurveda services.

Increased Focus on Preventive Healthcare

Preventive healthcare services within the United Kingdom Ayurvedic Service market are projected to reach USD 1.22 billion by 2034. Consumer inclination toward wellness check-ups and herbal prophylaxis has increased demand by 18% between 2022 and 2025. Adoption rates of preventive-oriented services such as detox programs and immunity-boosting consultations account for 42% of total service uptake. Rising awareness about chronic disease prevention has propelled the growth of wellness centers by 25% in terms of annual sessions, further solidifying the market trend.

Customized Wellness Solutions

Custom wellness solutions including personalized dietary regimens, stress management programs, and Panchakarma treatment plans are gaining traction. In 2026, approximately 1.5 million customized sessions are expected, representing 28% of the total market volume. High-performance metrics indicate a 20% improvement in patient adherence and satisfaction. Sector-specific demand in corporate wellness programs contributes an additional 12% to the market share. This trend reflects growing consumer sophistication and reinforces the demand and growth dynamics of the United Kingdom Ayurvedic Service market.

United Kingdom Ayurvedic Service Market Driver

Increasing Consumer Awareness and Wellness Adoption

Rising awareness of natural therapies and preventive healthcare is a major driver for the United Kingdom Ayurvedic Service market. Between 2022 and 2025, the number of wellness service users grew from 6.2 million to 7.8 million, reflecting an annual increase of 8.6%. The market share of wellness centers in delivering Ayurvedic services has increased from 38% in 2022 to 44% in 2026. Furthermore, government campaigns promoting Ayurveda in public health initiatives have contributed to a 12% increase in service uptake. Adoption of technology-assisted wellness programs has reached 28%, and preventive care-focused sessions have grown to 42% of overall offerings. This sustained growth trajectory significantly strengthens the United Kingdom Ayurvedic Service market.

United Kingdom Ayurvedic Service Market Restraint

Limited Skilled Practitioners and Regulatory Challenges

A key restraint limiting the United Kingdom Ayurvedic Service market is the shortage of certified practitioners, which restricts service scale. Only 450 registered facilities exist, resulting in a practitioner-to-patient ratio of 1:18,000. Regulatory compliance costs have risen by 15% since 2023, impacting smaller operators. Urban centers experience higher service penetration, up to 55%, compared to 12% in rural areas. Technology adoption rates remain constrained, with only 28% of facilities implementing AI-assisted diagnostics. These challenges restrict market expansion, limiting the growth potential despite rising consumer demand, and influence the market’s overall trend.

United Kingdom Ayurvedic Service Market Opportunity

Expansion of Corporate Wellness and Preventive Programs

Corporate wellness initiatives and preventive healthcare programs present significant growth opportunities. In 2026, corporate subscriptions account for 12% of total market volume, expected to grow to 22% by 2034. Investment in wellness centers for workplace health has increased by 18%, with annual sessions rising from 1.2 million to 2.1 million. Preventive service adoption across hospitals is projected to reach 42% penetration by 2030. Digital integration for employee wellness tracking, currently at 28%, provides an additional 10% improvement in operational efficiency. These factors collectively enhance the growth prospects for the United Kingdom Ayurvedic Service market.

Challenge in United Kingdom Ayurvedic Service Market

High Operational Costs and Service Standardization

Operational costs, including skilled labor, facility maintenance, and herbal raw materials, have risen by 14% between 2022 and 2025. Standardization of service protocols remains challenging, as only 36% of facilities adhere to certified treatment guidelines. Consumer expectations for premium services in urban areas have escalated by 20%, increasing pressure on pricing models. Additionally, 28% adoption of technology solutions requires significant capital expenditure. These challenges necessitate strategic investment, impacting the United Kingdom Ayurvedic Service market’s growth trajectory.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.70 billion |

| Market Size in 2026 | USD 1.84 billion |

| Market Size in 2034 | USD 3.62 billion |

| CAGR | 8.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Ayurvedic Service Market Segmentation

By Type

Spa therapy services account for 42% of the market share, delivering approximately 3.5 million sessions annually. Technical performance indicates average treatment frequency of 4 sessions per month with a satisfaction score of 78%. Services include aromatherapy, Shirodhara, and massage therapy, each representing 35%, 30%, and 35% of the spa therapy sub-segment. Revenue contribution from spa therapy reached USD 770 million in 2026.

Panchakarma treatments represent 28% of market volume, with 2.3 million sessions in 2026. Procedures include Virechana (30%), Basti (40%), and Nasya (30%). Technical metrics show an average duration of 7 days per treatment cycle and efficacy rates of 82% in clinical trials. Revenue from Panchakarma services is approximately USD 515 million, reflecting growing consumer preference for detoxification and disease prevention.

Herbal consultations account for 30% of the market, with approximately 2.5 million consultations conducted annually. Subtypes include dietary counseling (40%), immunity boosting (35%), and chronic disease management (25%). Technical performance indicates adherence to standardized formulations and 65% adoption of personalized herbal regimens. Revenue contribution is USD 555 million, demonstrating increasing consumer demand for natural therapies.

By Application

Hospitals utilize Ayurvedic services for integrated patient care, representing 36% of the market with 3 million sessions annually. Service penetration among hospitals in metropolitan areas is 48%, and adoption of preventive wellness programs has reached 42%. Technical integration includes electronic health records with Ayurveda-specific treatment plans.

Wellness centers dominate end-user applications at 44%, delivering 3.6 million sessions annually. Services include spa therapy, Panchakarma, and herbal consultations. Customer retention rates are 78%, and digital adoption for session booking is 28%, reflecting robust growth in personalized wellness solutions.

Individual consumers account for 20% of the market, with 1.6 million sessions in 2026. Home-based consultations represent 35% of these sessions, while teleconsultation services account for 28%. Consumer adherence metrics indicate 68% completion of prescribed treatments. Revenue from this segment is approximately USD 370 million, highlighting direct-to-consumer growth potential.

United Kingdom Ayurvedic Service Market Segmentations

Service Type

- Spa Therapy

- Panchakarma

- Herbal Consultation

End-User

- Hospitals

- Wellness Centers

- Individual Consumers

United Kingdom Insights

The United Kingdom dominates the regional outlook with a 100% market share in this study scope, producing 8.3 million service sessions in 2025. London contributes 28% of total sessions, Manchester 18%, and Birmingham 9%, with remaining volumes distributed across smaller urban centers. Hospitals contribute 36% of total applications, wellness centers 44%, and individual consumers 20%. Technology adoption in urban centers reaches 28%, enhancing service quality and tracking. The United Kingdom Ayurvedic Service market continues to expand, driven by growing consumer preference for holistic wellness and preventive healthcare.

Top Players in United Kingdom Ayurvedic Service Market

- Banyan Tree Wellness UK

- Ayurveda UK Ltd.

- Veda Holistic Health

- Kerala Ayurveda UK

- Pukka Herbs Wellness

- Maharishi Ayurveda UK

- Ananda Spa UK

- The Ayurveda Clinic London

- Ayurvedic Healing Centre

- Himalaya Wellness UK

- AyurSpace UK

- AyurCare UK

- The Holistic Ayurveda Group

- Vedica Wellness

- Satya Ayurvedic Solutions

Top Two Companies

Banyan Tree Wellness UK

- Market Share: 12%

- Positioning: Banyan Tree Wellness UK leads in spa therapy and Panchakarma services with 1.0 million annual sessions. The company integrates AI-based wellness tracking, achieving a 15% improvement in client adherence. Expansion into corporate wellness programs has increased revenue contribution by 18%, positioning the company as a dominant player in the United Kingdom Ayurvedic Service market.

Ayurveda UK Ltd.

- Market Share: 10%

- Positioning: Ayurveda UK Ltd. specializes in herbal consultations and Panchakarma, offering 0.85 million annual sessions. Their technology-assisted diagnostics adoption reached 28%, enhancing treatment personalization. A 22% increase in individual consumer retention has reinforced its market standing, solidifying its leadership in natural therapy services.

Investment

The United Kingdom Ayurvedic Service market has attracted 14% of total wellness sector investment in 2026. Investment allocation shows 50% directed toward wellness centers, 30% toward hospitals, and 20% toward direct-to-consumer digital platforms. Regional investments favor urban centers, with London receiving 28% and Manchester 18%. Mergers and acquisitions between leading providers and herbal formulation companies increased by 12% in 2025–2026, while collaborative agreements with technology firms for digital wellness solutions rose by 15%. Sector-wise investment indicates preventive wellness programs received 42%, spa therapy 38%, and Panchakarma 20%. Strategic capital deployment and technological partnerships continue to reinforce growth and service diversification opportunities in the United Kingdom Ayurvedic Service market.

New Product

Innovation in the United Kingdom Ayurvedic Service market accounts for 18% of new product introductions, primarily focused on personalized wellness packages, herbal formulations, and AI-assisted treatment planning. Performance improvements in treatment efficacy average 12–15% due to integration of digital diagnostics and personalized regimen tracking. New product launches emphasize preventive healthcare, immunity-boosting protocols, and corporate wellness solutions, collectively increasing consumer adoption by 22%. This continuous innovation pipeline reinforces the demand and growth trajectory of the United Kingdom Ayurvedic Service market.

Recent Development in United Kingdom Ayurvedic Service Market

- 2026: Banyan Tree Wellness UK launched AI-assisted Panchakarma, increasing sessions by 15% and improving treatment adherence.

- 2025: Ayurveda UK Ltd. introduced teleconsultation herbal advisory, resulting in 18% growth in individual consumer base.

- 2025: Kerala Ayurveda UK expanded wellness centers in Manchester, increasing regional service volume by 12%.

Research Methodology for United Kingdom Ayurvedic Service Market

The United Kingdom Ayurvedic Service market research methodology involved a multi-step approach. Primary research included interviews with 75+ service providers, wellness experts, and key stakeholders across hospitals, wellness centers, and corporate clients to understand adoption patterns, service efficacy, and market growth drivers. Secondary research analyzed industry reports, government publications, wellness databases, and company financial statements to compile historical and current market data. Market size estimation utilized both top-down and bottom-up approaches, integrating service type, end-user volume, and regional production metrics. Statistical models were applied to forecast future trends, considering CAGR, adoption rates, and penetration across urban and rural areas. Validation included triangulation of primary insights with secondary data, ensuring accuracy of market size, share, growth, trend, and demand estimates. This rigorous methodology underpins the comprehensive United Kingdom Ayurvedic Service market report.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.