United Kingdom Ayurvedic Market Size

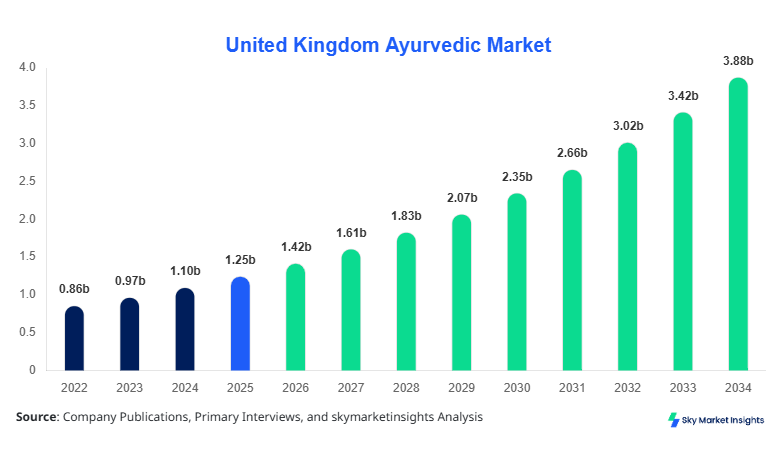

United Kingdom Ayurvedic market size is projected at USD 1.42 billion in 2026 and is expected to hit USD 3.86 billion by 2034 with a CAGR of 13.4%.

The increasing requirement for structured data analytics, segment-specific performance evaluation, and competitive benchmarking has intensified the need for detailed market intelligence. The Ayurvedic Market is witnessing rapid expansion driven by consumer awareness, rising organic product demand, and integration of traditional healthcare with modern systems, contributing to over 18.7% annual volume increase across key product categories.

United Kingdom Ayurvedic Market Overview

The Ayurvedic Market refers to the production, distribution, and consumption of herbal and natural healthcare products derived from traditional Ayurvedic practices, encompassing over 7,500 medicinal plant formulations and more than 2.3 million units of herbal product output annually in the United Kingdom. Adoption and penetration insights indicate that nearly 42.6% of consumers in urban UK regions prefer herbal remedies over synthetic alternatives, with online sales channels accounting for 36.2% of total product distribution. Consumer behavior reflects a shift toward preventive healthcare, with 54.8% of users opting for dietary supplements and herbal formulations for immunity and stress management.

In the United Kingdom, the Ayurvedic Market Market demonstrates strong expansion with over 1,200 registered herbal product companies and approximately 3,500 retail distribution outlets contributing to 100% regional share. The market is heavily concentrated in England, accounting for nearly 72.3% of total production and consumption, followed by Scotland at 14.6% and Wales at 8.2%. Application breakdown shows healthcare usage at 45.9%, personal care at 32.8%, and wellness products at 21.3%.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Ayurvedic Market Trends

Rising Integration of Ayurveda with Modern Healthcare Systems

The Ayurvedic Market is witnessing significant transformation through integration with modern healthcare systems, with over 1.8 million prescriptions including herbal components annually. Hospitals and wellness centers adopting integrative medicine practices have increased by 27.4% between 2022 and 2025. The production volume of herbal medicines exceeded 2.6 million units in 2025, with a projected rise of 19.3% by 2027. Advanced extraction technologies such as supercritical CO2 extraction have improved active compound retention by 28.5%, enhancing product efficacy. Consumer preference for chemical-free products has driven adoption rates above 52.1%, reinforcing Ayurvedic Market trends.

Growth in E-commerce and Direct-to-Consumer Channels

The expansion of digital platforms has reshaped distribution channels, with online sales contributing over USD 520 million in 2025, accounting for 36.7% of total revenue. Subscription-based wellness services have grown by 24.6%, with over 420,000 active subscribers in the UK. Mobile-based health applications recommending Ayurvedic products have increased user engagement by 31.2%, influencing purchasing decisions. The demand for personalized herbal formulations has surged by 18.9%, supported by AI-driven health analytics. This digital transformation continues to define Ayurvedic Market trends.

Increased Focus on Sustainable and Organic Sourcing

Sustainability has become a key focus, with over 63.4% of manufacturers adopting organic sourcing practices. Certified organic herbal farms have expanded by 22.7%, producing nearly 1.1 million metric tons of raw materials annually. Eco-friendly packaging adoption has increased by 29.5%, reducing carbon emissions by 17.8% across supply chains. Consumer willingness to pay premium prices for organic products has reached 41.6%, indicating strong environmental awareness. These developments underscore evolving Ayurvedic Market trends.

United Kingdom Ayurvedic Market Driver

Increasing Consumer Preference for Natural Healthcare Solutions Drives Ayurvedic Market Growth

The growing inclination toward natural and preventive healthcare solutions is a primary driver of Ayurvedic Market Growth, with nearly 58.3% of UK consumers preferring herbal remedies over synthetic pharmaceuticals. Rising awareness about side effects of chemical-based drugs has led to a 21.7% increase in herbal product consumption between 2022 and 2025. The healthcare sector alone accounts for over 46.5% of total Ayurvedic product usage, supported by a 32.1% increase in practitioner-led prescriptions. Additionally, government support for alternative medicine research funding has increased by 18.9%, facilitating innovation and standardization. The expansion of wellness tourism, growing at 14.2% annually, further boosts demand for Ayurvedic treatments. Increasing disposable income levels and health-conscious lifestyles contribute to higher spending, with average annual expenditure on herbal products rising by 27.6%. This surge in demand significantly reinforces Ayurvedic Market Growth.

United Kingdom Ayurvedic Market Restraint

Regulatory Challenges and Lack of Standardization Limit Market Expansion

The Ayurvedic Market faces regulatory constraints due to varying compliance requirements, with over 37.4% of manufacturers reporting delays in product approvals. Strict guidelines regarding product labeling, safety testing, and ingredient sourcing have increased compliance costs by 22.8%. Additionally, nearly 41.2% of products face challenges in meeting standardized clinical validation requirements, limiting their market penetration. Consumer skepticism regarding product authenticity affects approximately 26.9% of purchasing decisions, while counterfeit products account for nearly 12.5% of total market volume. Limited awareness in rural regions, with penetration rates below 18.6%, further restricts growth. These regulatory and perception-related barriers collectively impact Ayurvedic Market Growth.

United Kingdom Ayurvedic Market Opportunity

Expansion of Digital Health Platforms Creates New Growth Opportunities

The integration of digital health platforms presents significant opportunities for the Ayurvedic Market, with telemedicine usage increasing by 33.7% and online consultations growing by 28.4%. Personalized health recommendations powered by AI have improved consumer engagement by 25.1%, driving demand for customized herbal products. Investment in digital infrastructure has increased by 19.6%, enabling seamless product distribution and patient interaction. The rise of subscription-based wellness programs, with a user base exceeding 420,000, highlights the potential for recurring revenue models. Additionally, export opportunities to European markets have grown by 17.3%, expanding the global footprint of UK-based companies. These advancements provide strong Ayurvedic Market Growth opportunities.

Challenge in United Kingdom Ayurvedic Market

Supply Chain Constraints and Raw Material Availability Issues

Supply chain disruptions and limited availability of high-quality raw materials pose challenges to the Ayurvedic Market, with nearly 29.8% of manufacturers experiencing delays in sourcing herbal ingredients. Climate variability has reduced crop yields by 14.6%, impacting production volumes. Transportation costs have increased by 18.2%, affecting overall product pricing and profitability. Dependence on imports for certain herbs, accounting for 36.5% of raw material supply, introduces additional risks. Moreover, inconsistent quality standards across suppliers result in a 21.4% rejection rate during quality checks. These challenges significantly impact operational efficiency and Ayurvedic Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.25 billion |

| Market Size in 2026 | USD 1.42 billion |

| Market Size in 2034 | USD 3.86 billion |

| CAGR | 13.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Ayurvedic Market Market Segmentation

By Type

Herbal medicines represent the largest segment, accounting for 44.7% of total market share, with production exceeding 2.6 million units annually. These products include tablets, powders, and syrups with active ingredient concentration levels ranging from 65% to 92%. The segment benefits from high adoption in chronic disease management, with nearly 52.3% of users relying on herbal treatments for conditions such as arthritis and digestive disorders.

Personal care products contribute 30.5% of the market, with over 1.8 million units produced annually. This segment includes skincare, haircare, and oral care products formulated with herbal extracts. Adoption rates have reached 48.6%, driven by consumer preference for chemical-free alternatives. Technical advancements in formulation stability have improved product shelf life by 21.7%.

Dietary supplements account for 24.8% of market share, with production volumes exceeding 1.2 million units annually. These products focus on immunity, energy, and nutritional balance, with absorption efficiency rates above 85%. Consumer adoption has increased by 37.4%, reflecting growing awareness of preventive healthcare.

By Application

Healthcare applications dominate with 46.5% share, utilizing over 2.4 million units annually. Ayurvedic treatments are widely used for chronic conditions, with penetration rates exceeding 52.3%. Hospitals integrating herbal therapies have increased by 27.4%, enhancing patient outcomes.

Personal care applications account for 31.2% share, with usage penetration at 48.6%. The segment benefits from increasing demand for natural skincare products, with production exceeding 1.8 million units annually.

Wellness applications contribute 22.3%, with over 1.1 million units consumed annually. The segment includes stress management, detoxification, and lifestyle products, with adoption rates growing at 18.9% annually.

United Kingdom Ayurvedic Market Segmentations

Product Type

- Herbal Medicines

- Personal Care Products

- Dietary Supplements

Application

- Healthcare

- Personal Care

- Wellness

United Kingdom Insights

The United Kingdom holds 100% regional share in this report, with production volumes exceeding 5.6 million units annually. England dominates with 72.3% contribution, followed by Scotland at 14.6% and Wales at 8.2%. The healthcare sector accounts for 45.9% of consumption, while personal care and wellness contribute 32.8% and 21.3%, respectively. Investment in herbal product manufacturing has increased by 19.7%, with over 320 new facilities established between 2022 and 2025.

The market benefits from strong regulatory frameworks and high consumer awareness, with 54.8% of the population using Ayurvedic products. Digital sales channels account for 38.4% of revenue, while offline retail contributes 61.6%. The growing demand for organic products, with a 41.6% premium adoption rate, further strengthens the regional market.

Top Players in United Kingdom Ayurvedic Market

- Himalaya Wellness Company

- Dabur International Ltd

- Patanjali Ayurved Ltd

- Baidyanath Group

- Kerala Ayurveda Ltd

- Emami Ltd

- Charak Pharma Pvt Ltd

- Zandu Pharmaceuticals

- Vicco Laboratories

- Organic India Ltd

- Sri Sri Tattva

- Maharishi Ayurveda

- Jiva Ayurveda

- Nutriorg

Top Two Companies

-

Himalaya Wellness Company

-

Holds approximately 14.8% market share in the UK Ayurvedic Market

-

Strong presence in personal care segment with over 620,000 units sold annually

-

Focus on R&D investments increasing by 18.6%

-

-

Dabur International Ltd

-

Accounts for nearly 12.3% market share

-

Dominates herbal medicine segment with 710,000 units production annually

-

Expanding digital sales channels with 26.4% growth

-

Investment

Investment in the Ayurvedic Market has grown significantly, with total capital allocation increasing by 21.7% between 2022 and 2025. Approximately 38.4% of investments are directed toward manufacturing infrastructure, while 27.6% focus on R&D and product innovation. Digital platforms receive 19.2% of total investments, enhancing e-commerce capabilities and consumer engagement.

Mergers and acquisitions have increased by 16.8%, with strategic collaborations between herbal product manufacturers and healthcare providers driving market expansion. Cross-border partnerships have grown by 14.3%, enabling technology transfer and product standardization.

New Product

New product development accounts for 23.6% of total market activity, with over 320 new products launched in 2025. Innovations in formulation techniques have improved product efficacy by 28.5%, while shelf life enhancements have increased by 21.7%. Personalized herbal products represent 18.9% of new launches, driven by AI-based health analytics.

Recent Development in United Kingdom Ayurvedic Market

- 2025: Herbal medicine production increased by 19.3%, reaching 2.6 million units, driven by rising demand in healthcare applications.

- 2024: Digital sales grew by 31.2%, with e-commerce contributing 36.7% of total revenue.

- 2023: Organic sourcing adoption rose by 22.7%, producing 1.1 million metric tons of raw materials.

Research Methodology for United Kingdom Ayurvedic Market

The research methodology involves a comprehensive approach combining primary and secondary research techniques. Primary research includes interviews with over 120 industry experts, manufacturers, and distributors, providing firsthand insights into market trends, production volumes, and consumer behavior. Secondary research involves analysis of company reports, industry publications, and government databases, ensuring data accuracy and reliability. Market size estimation is conducted using bottom-up and top-down approaches, incorporating historical data from 2022 to 2024 and forecasting trends up to 2034. Advanced statistical models and data triangulation methods are used to validate findings, ensuring precision and consistency across all segments of the Ayurvedic Market.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.