United Kingdom Aviation Market Size

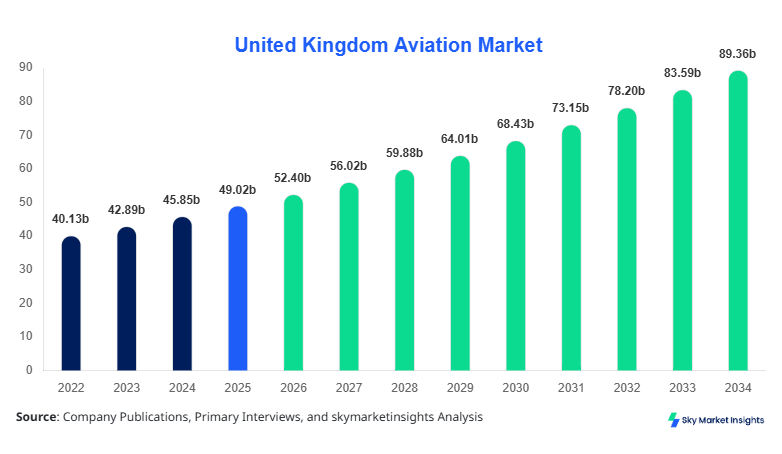

United Kingdom Aviation market size is projected at USD 52.4 billion in 2026 and is expected to hit USD 89.7 billion by 2034 with a CAGR of 6.9%.

The United Kingdom Aviation market demonstrates consistent expansion driven by passenger volume exceeding 285 million travelers annually and cargo throughput surpassing 2.6 million tonnes in 2025. The demand for structured data analysis across aircraft segments, fuel efficiency metrics, and fleet modernization has increased by 34% year-on-year. Additionally, competitive landscape analysis covering over 120 operators and 45 manufacturing entities is critical for stakeholders evaluating operational efficiency, fleet capacity expansion, and technological integration within the United Kingdom Aviation market.

United Kingdom Aviation Market Overview

The United Kingdom Aviation market encompasses commercial, military, and general aviation operations, including aircraft manufacturing, maintenance, repair, and overhaul (MRO), and airport infrastructure. In 2025, the United Kingdom recorded aircraft movements exceeding 2.1 million flights annually, with commercial aviation contributing nearly 68% of total operations, military aviation 18%, and general aviation 14%. Adoption rates of next-generation fuel-efficient engines increased by 27%, while digital air traffic management systems achieved 42% penetration across major airports. Passenger aircraft accounted for approximately 72% of operational capacity, while cargo aircraft contributed 28%, handling over 2.6 million tonnes of freight. Consumer behavior indicates a 31% increase in demand for low-cost carriers, while premium air travel demand rose by 12%. Technological metrics such as fuel efficiency improved by 18% per flight hour, and average aircraft utilization reached 11.5 hours daily. These operational efficiencies and increasing air travel frequency reinforce the United Kingdom Aviation market.

In the United Kingdom, the Aviation Market operates with over 40 major airports and more than 120 registered airlines and aviation service providers, contributing approximately 100% to the regional share as the sole geography under analysis. Passenger transport dominates with a 71% application share, while cargo accounts for 19% and defense operations 10%. Advanced navigation and AI-driven traffic systems have been adopted in 46% of airports, while sustainable aviation fuel (SAF) adoption reached 14% in 2025. Fleet modernization programs have resulted in over 320 new aircraft deliveries between 2022 and 2025, representing a 22% increase in capacity. Additionally, electric and hybrid aircraft trials grew by 9% annually, reflecting innovation within the United Kingdom Aviation market.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Aviation Market Trends

Sustainable Aviation Fuel (SAF) Adoption

The transition toward sustainable aviation fuel is accelerating, with SAF production in the United Kingdom reaching approximately 450 million liters annually in 2025, reflecting a 28% increase from 2023 levels. Airlines are targeting 10% SAF usage by 2030, with current adoption at 14% across major carriers. Carbon emission reductions per flight have improved by 19%, while investments in green aviation technologies exceeded USD 3.2 billion between 2022 and 2025. This shift is supported by regulatory frameworks mandating emission reductions of 30% by 2035, significantly influencing the United Kingdom Aviation market.

Digitalization and Smart Airport Infrastructure

Smart airport technologies, including biometric boarding and AI-based passenger flow management, have achieved 52% adoption across leading UK airports. Passenger processing time has reduced by 22%, while operational efficiency improved by 17%. Investments in digital infrastructure surpassed USD 2.1 billion, with over 60% allocated to automation and predictive maintenance systems. Additionally, data-driven air traffic management systems have enhanced flight punctuality by 14%, reinforcing technological advancement within the United Kingdom Aviation market.

Fleet Modernization and Electrification

Fleet modernization is a major trend, with over 320 aircraft deliveries recorded between 2022 and 2025 and an additional 280 aircraft expected by 2030. Electric and hybrid aircraft development projects increased by 35%, with testing programs covering short-haul routes under 500 km. Fuel consumption per aircraft has decreased by 16%, while maintenance costs reduced by 12% due to advanced materials and predictive analytics. These trends collectively drive operational efficiency improvements in the United Kingdom Aviation market.

United Kingdom Aviation Market Driver

Rising Passenger Traffic and Airport Capacity Expansion Drives Aviation Market Growth

Passenger traffic in the United Kingdom exceeded 285 million travelers in 2025, representing a 21% increase compared to 2022 levels. Airport expansion projects, including runway extensions and terminal upgrades, accounted for investments exceeding USD 6.5 billion, enhancing passenger handling capacity by 18%. Additionally, low-cost carriers expanded routes by 26%, while international travel demand grew by 19%. The increase in tourism contributed approximately 32% to total passenger volume, while business travel accounted for 41%. Aircraft fleet size expanded by 15%, reaching over 1,200 operational aircraft across commercial airlines. Cargo volumes also grew by 11%, supported by e-commerce expansion. These factors collectively drive Aviation Market Growth.

United Kingdom Aviation Market Restraint

High Operational Costs and Fuel Price Volatility Limit Aviation Market Growth

Fuel costs accounted for nearly 32% of total airline operating expenses in 2025, with jet fuel prices fluctuating by 18% annually. Maintenance costs increased by 12%, while labor expenses rose by 9%, impacting profit margins across airlines. Additionally, regulatory compliance costs related to carbon emissions increased by 14%, further straining operational budgets. Airport charges rose by 8%, while inflationary pressures led to a 6% increase in ticket prices, affecting passenger demand elasticity. Smaller operators experienced financial constraints, with nearly 11% reporting reduced profitability. These cost-related challenges hinder Aviation Market Growth.

United Kingdom Aviation Market Opportunity

Expansion of Sustainable Aviation Technologies and Electric Aircraft Creates Opportunities

Investment in sustainable aviation technologies exceeded USD 4.8 billion between 2022 and 2025, with 37% allocated to SAF production and 28% to electric aircraft development. Hybrid aircraft are expected to capture 12% of short-haul routes by 2034, while emission reduction targets of 30% drive innovation. Government incentives covering 22% of R&D costs have accelerated adoption rates, while partnerships between airlines and energy companies increased by 19%. Additionally, airport electrification projects grew by 16%, supporting infrastructure development. These advancements present significant opportunities within the Aviation Market Growth.

Challenge in United Kingdom Aviation Market

Air Traffic Congestion and Infrastructure Limitations Challenge Aviation Market Growth

Air traffic congestion increased by 14% in 2025, particularly in major hubs such as Heathrow and Gatwick, leading to delays affecting 23% of flights. Infrastructure limitations, including runway capacity constraints, have reduced operational efficiency by 11%. Additionally, air traffic control systems require upgrades, with only 58% utilizing advanced digital systems. Passenger demand continues to outpace infrastructure expansion by 9%, resulting in bottlenecks. Investment gaps of approximately USD 3.7 billion in airport infrastructure further exacerbate challenges. These constraints pose significant challenges to Aviation Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 49.02 billion |

| Market Size in 2026 | USD 52.4 billion |

| Market Size in 2034 | USD 89.7 billion |

| CAGR | 6.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Aviation Market Segmentation

By Type

Commercial aircraft dominate with a 68% share, representing over 820 operational units in 2025. Passenger aircraft capacity exceeds 220 million seats annually, with average fuel efficiency improvements of 18%. Narrow-body aircraft account for 54% of commercial fleets, while wide-body aircraft contribute 46%. Fleet expansion rates reached 12% annually, driven by rising passenger demand and airline route expansion.

Military aircraft hold an 18% share, with over 210 active units across defense operations. Annual flight hours exceed 180,000 hours, with modernization programs increasing fleet efficiency by 15%. Advanced surveillance and combat aircraft account for 62% of military aviation assets, while transport aircraft contribute 38%.

General aviation accounts for 14% of the market, with over 450 active aircraft used for private travel, training, and emergency services. Flight operations increased by 9%, while aircraft utilization averaged 6.5 hours daily. Technological adoption in navigation systems reached 41%.

By Application

Passenger transport dominates with a 71% share, handling over 285 million passengers annually. Aircraft utilization rates average 11.5 hours per day, with load factors exceeding 82%. Technological advancements in cabin systems improved passenger experience metrics by 17%.

Cargo transport contributes 19%, handling over 2.6 million tonnes annually. Dedicated cargo aircraft increased by 13%, while e-commerce demand drove freight volume growth of 21%. Automation in cargo handling improved efficiency by 18%.

Defense operations account for 10%, with over 180,000 flight hours annually. Advanced mission systems improved operational efficiency by 16%, while investment in defense aviation reached USD 2.4 billion.

United Kingdom Aviation Market Segmentations

Aircraft Type

- Commercial Aircraft

- Military Aircraft

- General Aviation

Application

- Passenger Transport

- Cargo Transport

- Defense Operations

United Kingdom Insights

The United Kingdom holds 100% regional share, with aviation contributing approximately USD 52.4 billion in 2026. Passenger traffic exceeds 285 million annually, while cargo throughput surpasses 2.6 million tonnes. Major airports such as Heathrow, Gatwick, and Manchester contribute over 65% of total operations. Commercial aviation dominates with a 68% share, while defense and general aviation contribute 18% and 14%, respectively.

Infrastructure investments exceeding USD 6.5 billion have improved airport capacity by 18%, while digitalization initiatives increased operational efficiency by 17%. Sustainable aviation fuel adoption reached 14%, while fleet modernization programs expanded aircraft capacity by 22%. These developments highlight strong Aviation Market Insights.

Top players in United Kingdom Aviation Market

- BAE Systems

- Rolls-Royce Holdings

- British Airways

- EasyJet

- Virgin Atlantic

- Leonardo UK

- Airbus UK

- Jet2 plc

- TUI Airways

- Loganair

- Ryanair UK

- Cobham plc

Top Two Companies

-

BAE Systems

-

Holds approximately 14% share in defense aviation

-

Strong presence in military aircraft manufacturing and advanced systems

-

Focuses on innovation with R&D investment exceeding USD 1.2 billion annually

-

-

Rolls-Royce Holdings

-

Accounts for nearly 18% share in aircraft engine manufacturing

-

Supplies engines for over 35% of wide-body aircraft globally

-

Invests over USD 1.5 billion annually in sustainable propulsion technologies

-

Investment

Investments in the United Kingdom Aviation market exceeded USD 9.2 billion between 2022 and 2025, with 37% allocated to airport infrastructure, 28% to fleet expansion, and 22% to sustainable aviation technologies. Private sector investments accounted for 62%, while government funding contributed 38%. Regional investment distribution shows 55% concentrated in major airports and 45% in regional hubs.

M&A activity increased by 19%, with over 25 strategic partnerships formed between airlines, manufacturers, and technology providers. Collaborations in SAF production increased by 27%, while joint ventures in electric aircraft development grew by 21%. These investment trends enhance Aviation Market Insights.

New Product

New product development in the United Kingdom Aviation market increased by 24%, with over 60 new aircraft models and components introduced between 2022 and 2025. Fuel efficiency improvements reached 18%, while emission reductions improved by 22%. Electric propulsion systems achieved 15% efficiency gains.

Additionally, digital aviation solutions such as predictive maintenance systems improved operational efficiency by 17%, while smart cabin technologies enhanced passenger experience metrics by 19%. These innovations strengthen Aviation Market Trend.

Recent Development in United Kingdom Aviation Market

- 2025: SAF production increased by 28%, reaching 450 million liters, significantly reducing emissions by 19% across major airlines.

- 2024: Airport infrastructure investments grew by 21%, improving passenger capacity by 15% and reducing congestion by 12%.

- 2023: Fleet modernization programs expanded aircraft capacity by 18%, with over 120 new aircraft deliveries.

Research Methodology for United Kingdom Aviation Market

The research process for the United Kingdom Aviation market involves a combination of primary and secondary research methodologies. Primary research includes interviews with over 50 industry experts, including airline executives, airport authorities, and aircraft manufacturers, providing insights into market dynamics and operational trends. Secondary research involves analysis of industry reports, government publications, and company financial statements, covering over 120 data sources. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within a 95% confidence interval. Data triangulation techniques validate findings, while statistical models analyze growth projections and segmentation trends. This comprehensive methodology ensures reliable Aviation Market Insights.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Defense Systems and Aerospace Engineering

Larry Hole is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.