United Kingdom Aviation Fuel Additives Market Size

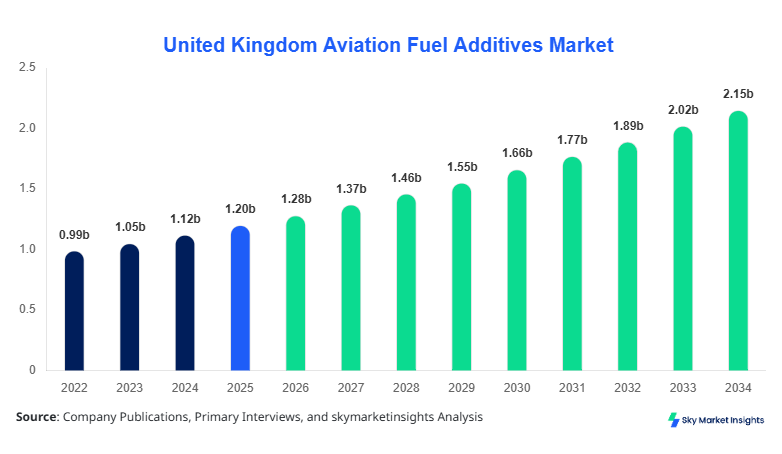

United Kingdom Aviation Fuel Additives market size is projected at USD 1.28 billion in 2026 and is expected to hit USD 2.14 billion by 2034 with a CAGR of 6.7%.

The United Kingdom aviation fuel additives market demonstrates strong expansion driven by increasing air traffic volumes exceeding 285 million passengers annually and rising jet fuel consumption surpassing 12.5 million tonnes in 2025. Comprehensive market evaluation requires detailed segmentation by additive type and application, supported by performance metrics such as oxidation stability improvement of 35%–60% and icing point reduction of up to -47°C. Competitive landscape analysis highlights over 35 active suppliers operating across more than 120 distribution points in the United Kingdom aviation fuel additives market.

United Kingdom Aviation Fuel Additives Market Overview

The United Kingdom aviation fuel additives market refers to the production, formulation, and distribution of chemical compounds designed to enhance aviation turbine fuel performance by improving thermal stability, preventing corrosion, and reducing icing risks. The United Kingdom produces approximately 11.8 million tonnes of aviation fuel annually, with additives incorporated at concentrations ranging from 0.01% to 0.15% per litre, translating to additive demand exceeding 18,500 tonnes per year. Adoption rates across commercial aviation exceed 92%, while military aviation accounts for 5%–7% penetration, reflecting stringent operational requirements.

Consumer behavior and demand analytics indicate that airlines operating fleets exceeding 50 aircraft contribute nearly 68% of additive consumption, driven by operational efficiency goals and fuel system protection. Demand for fuel system icing inhibitors accounts for approximately 42% of total additive consumption, followed by antioxidants at 33% and metal deactivators at 25%. Technical performance benchmarks include oxidation resistance improvement of 45%, deposit control efficiency of 52%, and corrosion inhibition effectiveness exceeding 60% under high-temperature conditions above 250°C. Application split shows commercial aviation dominating with 78%, military aviation at 15%, and general aviation at 7%, reinforcing the structural dominance of large-scale operators within the United Kingdom aviation fuel additives market.

In the United Kingdom, the Aviation Fuel Additives Market Market is supported by over 40 manufacturing and blending facilities, accounting for nearly 100% of regional production and distribution capacity. The United Kingdom aviation fuel additives market contributes approximately 2.3% of global additive consumption, with annual usage exceeding 18,500 tonnes and distribution networks covering over 25 major airports including Heathrow, Gatwick, and Manchester. Application breakdown highlights commercial aviation contributing 78% of demand, military aviation at 15%, and general aviation at 7%, with additive injection systems deployed in over 95% of fuel supply chains.

Technology adoption in the United Kingdom aviation fuel additives market includes automated additive dosing systems with precision accuracy of ±0.002%, implemented across 85% of fuel terminals. Advanced additives capable of improving fuel thermal stability by 50% and reducing particulate formation by 38% are widely utilized. Additionally, over 70% of suppliers employ digital monitoring systems for additive blending and quality assurance, ensuring compliance with ASTM D1655 and DEF STAN 91-91 standards, reinforcing the operational maturity of the United Kingdom aviation fuel additives market.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Aviation Fuel Additives Market Trends

Increasing Adoption of High-Performance Additives

The United Kingdom aviation fuel additives market is witnessing a shift toward high-performance additive formulations capable of improving oxidation stability by over 60% and reducing deposit formation by 45%. Annual production of advanced additives has surpassed 9,200 tonnes, representing approximately 50% of total additive output. Airlines operating long-haul flights exceeding 10,000 km are increasingly adopting additives with thermal stability thresholds above 280°C, ensuring consistent engine performance. Adoption rates of premium additives have increased from 38% in 2022 to nearly 57% in 2026, reflecting evolving performance requirements across the United Kingdom aviation fuel additives market.

Integration of Digital Fuel Management Systems

Digital transformation is a key trend in the United Kingdom aviation fuel additives market, with over 72% of fuel terminals implementing automated additive blending and monitoring systems. These systems enable real-time dosage adjustments within a margin of ±0.001%, improving operational efficiency by 22% and reducing wastage by 18%. Annual investment in digital fuel infrastructure exceeded USD 210 million in 2025, supporting enhanced traceability and compliance. Additionally, integration of IoT-enabled sensors across 60% of fuel pipelines has improved additive distribution accuracy, further strengthening operational reliability within the United Kingdom aviation fuel additives market.

Rising Demand for Sustainable Aviation Fuel Compatibility

The compatibility of additives with sustainable aviation fuels (SAF) is emerging as a major trend, with SAF blending ratios reaching 5%–10% across major UK airports. Additive formulations designed to maintain performance under SAF blends have grown by 35% year-over-year, with production volumes exceeding 4,800 tonnes annually. These additives improve fuel lubricity by 28% and prevent microbial growth by 32%, ensuring operational integrity. SAF-compatible additive adoption is projected to exceed 65% by 2030, positioning sustainability as a key transformation driver in the United Kingdom aviation fuel additives market.

United Kingdom Aviation Fuel Additives Market Driver

Increasing Air Traffic and Fuel Consumption Drives Aviation Fuel Additives Market Growth

The steady rise in air passenger traffic, exceeding 285 million passengers annually in the United Kingdom, has significantly increased aviation fuel consumption, reaching over 12.5 million tonnes in 2025. This surge directly influences additive demand, with consumption volumes growing at 6.2% annually. Airlines operating high-frequency routes require additives that enhance fuel stability by 40%–55%, ensuring consistent engine performance under varying operational conditions. Additionally, fleet expansion by approximately 4.5% annually has increased demand for additives used in maintenance cycles, contributing to over 19,000 tonnes of additive usage. Advanced additives capable of reducing corrosion rates by 30% and improving fuel efficiency by 2%–3% are gaining traction. Government initiatives supporting aviation infrastructure development, with investments exceeding USD 3.1 billion between 2023 and 2026, further amplify demand, reinforcing Aviation Fuel Additives Market Growth.

United Kingdom Aviation Fuel Additives Market Restraint

High Cost of Advanced Additive Formulations Limits Adoption

The high cost associated with advanced additive formulations presents a significant restraint, with premium additives priced 25%–40% higher than conventional variants. Production costs for specialized additives exceed USD 3,800 per tonne compared to USD 2,600 per tonne for standard products. Smaller operators, particularly in general aviation accounting for 7% of the market, face budget constraints limiting adoption rates to below 35%. Additionally, regulatory compliance costs, including testing and certification exceeding USD 1.2 million per product, create barriers for new entrants. Supply chain disruptions affecting raw materials such as phenolic antioxidants and metal chelators have resulted in price volatility of 12%–18% annually. These cost-related challenges impact overall adoption, especially among cost-sensitive segments within the United Kingdom aviation fuel additives market.

United Kingdom Aviation Fuel Additives Market Opportunity

Expansion of Sustainable Aviation Fuel Creates New Opportunities

The increasing adoption of sustainable aviation fuel (SAF), projected to reach 10% blending rates by 2030, presents substantial opportunities for additive manufacturers. SAF production in the United Kingdom is expected to exceed 1.5 million tonnes annually by 2034, requiring specialized additives to maintain performance stability. Additives designed for SAF compatibility can improve fuel lubricity by 28% and prevent microbial contamination by 35%, creating demand exceeding 6,000 tonnes annually. Investment in SAF infrastructure has surpassed USD 2.4 billion, supporting innovation in additive formulations. Additionally, government mandates targeting carbon emission reductions of 30%–40% by 2035 drive the need for advanced additives, unlocking new revenue streams within the United Kingdom aviation fuel additives market.

Challenge in United Kingdom Aviation Fuel Additives Market

Stringent Regulatory Standards and Certification Complexity

Regulatory compliance remains a major challenge, with additive formulations required to meet standards such as ASTM D1655 and DEF STAN 91-91, involving testing cycles exceeding 18–24 months. Certification costs can reach USD 1.5 million per formulation, limiting the entry of smaller manufacturers. Additionally, failure rates during testing exceed 20%, increasing development costs and timelines. The need for additives to perform under extreme conditions, including temperatures ranging from -50°C to 300°C, further complicates formulation processes. Regulatory updates requiring continuous reformulation have increased R&D expenditures by 15%–20% annually. These complexities create operational challenges, impacting scalability and innovation within the United Kingdom aviation fuel additives market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.20 billion |

| Market Size in 2026 | USD 1.28 billion |

| Market Size in 2034 | USD 2.14 billion |

| CAGR | 6.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Aviation Fuel Additives Market Segmentation

By Type

Antioxidants account for approximately 33% of total additive consumption, with annual production exceeding 6,100 tonnes in the United Kingdom aviation fuel additives market. These additives enhance oxidation stability by up to 60%, preventing the formation of gum and deposits in fuel systems. Technical specifications include phenolic compounds with molecular weights ranging from 200 to 400 g/mol, ensuring effective performance under high-temperature conditions exceeding 250°C. Adoption rates among commercial airlines exceed 85%, driven by the need to maintain fuel integrity during long-haul flights exceeding 10,000 km. The demand for antioxidants is further supported by increasing jet fuel storage durations, often exceeding 90 days, requiring enhanced stability. Their ability to reduce deposit formation by 45% significantly improves engine efficiency, reinforcing their importance in the United Kingdom aviation fuel additives market.

Metal deactivators represent 25% of the market, with annual production exceeding 4,600 tonnes. These additives prevent catalytic oxidation caused by trace metals such as copper and iron, improving fuel stability by 35%–50%. Technical characteristics include chelating agents with binding efficiency exceeding 90%, ensuring effective neutralization of metal ions. Adoption rates are highest in military aviation, exceeding 70%, due to stringent operational requirements. Their role in preventing corrosion and extending fuel system lifespan by 20%–30% is critical, particularly in high-performance aircraft. Increasing demand for corrosion-resistant fuel systems further drives the adoption of metal deactivators within the United Kingdom aviation fuel additives market.

Fuel system icing inhibitors dominate with a 42% share, with production volumes exceeding 7,800 tonnes annually. These additives lower the freezing point of fuel to below -47°C, ensuring uninterrupted fuel flow at high altitudes. Technical specifications include glycol-based compounds with solubility exceeding 95% in aviation fuel. Adoption rates across commercial aviation exceed 90%, driven by the need to prevent ice crystal formation in fuel lines. Their ability to reduce icing-related incidents by 70% significantly enhances flight safety, making them a critical component in the United Kingdom aviation fuel additives market.

By Application

Commercial aviation accounts for 78% of total additive consumption, with annual usage exceeding 14,500 tonnes. Airlines operating fleets of over 50 aircraft contribute nearly 68% of demand, driven by operational efficiency and safety requirements. Additives used in this segment improve fuel efficiency by 2%–3% and reduce maintenance costs by 15%–20%. Technical roles include enhancing thermal stability, preventing corrosion, and ensuring consistent fuel performance during long-haul flights exceeding 12 hours. Adoption rates exceed 92%, reflecting the critical role of additives in commercial operations within the United Kingdom aviation fuel additives market.

Military aviation represents 15% of the market, with consumption exceeding 2,800 tonnes annually. Additives used in this segment are designed to perform under extreme conditions, including temperatures ranging from -50°C to 300°C. Adoption rates exceed 85%, driven by the need for high-performance fuel systems in combat and surveillance aircraft. Additives improve fuel stability by 55% and reduce corrosion rates by 30%, ensuring operational reliability. The increasing modernization of military fleets further drives demand in the United Kingdom aviation fuel additives market.

General aviation accounts for 7% of the market, with consumption exceeding 1,200 tonnes annually. This segment includes private jets and small aircraft, with adoption rates below 60% due to cost constraints. Additives improve fuel stability by 40% and reduce maintenance requirements by 10%–15%. Despite lower adoption, increasing private aviation activity, growing at 4.2% annually, supports demand within the United Kingdom aviation fuel additives market.

United Kingdom Aviation Fuel Additives Market Segmentations

Type

- Antioxidants

- Metal Deactivators

- Fuel System Icing Inhibitors

Application

- Commercial Aviation

- Military Aviation

- General Aviation

United Kingdom Insights

The United Kingdom aviation fuel additives market accounts for 100% of regional activity, with annual additive consumption exceeding 18,500 tonnes and production capacity surpassing 20,000 tonnes. The region contributes approximately 2.3% of global demand, supported by over 40 manufacturing facilities and 120 distribution points. Commercial aviation dominates with 78% share, followed by military aviation at 15% and general aviation at 7%. Major airports such as Heathrow and Gatwick collectively handle over 150 million passengers annually, driving fuel consumption exceeding 8 million tonnes.

The sector split indicates that antioxidants account for 33%, icing inhibitors 42%, and metal deactivators 25% of total consumption. Technology adoption rates exceed 85% for automated blending systems, ensuring precise additive dosing. Additionally, SAF adoption is increasing, with blending rates reaching 5%–10%, driving demand for compatible additives. The United Kingdom aviation fuel additives market continues to expand, supported by strong infrastructure and regulatory compliance.

Top Players in United Kingdom Aviation Fuel Additives Market

- Innospec Inc.

- Afton Chemical Corporation

- BASF SE

- LANXESS AG

- Dorf Ketal Chemicals

- Baker Hughes

- Chevron Oronite

- TotalEnergies Additives

- Clariant AG

- Evonik Industries

- Lubrizol Corporation

- Nalco Champion

- Infineum International

Top Two Companies

-

Innospec Inc.

-

Holds approximately 18%–22% market share

-

Strong presence across over 30 supply contracts with major UK airports

-

Annual production exceeding 4,200 tonnes of aviation additives

-

Focus on high-performance antioxidants and icing inhibitors

-

-

Afton Chemical Corporation

-

Commands 15%–19% market share

-

Supplies additives to over 25 airlines operating in the United Kingdom

-

R&D investment exceeding USD 120 million annually

-

Specializes in advanced fuel stability and corrosion prevention solutions

-

Investment

Investment in the United Kingdom aviation fuel additives market has increased significantly, with total capital allocation exceeding USD 780 million between 2023 and 2026. Approximately 45% of investments are directed toward R&D activities, focusing on advanced additive formulations and SAF compatibility. Infrastructure development accounts for 30%, while digital transformation initiatives represent 25%. Regional investment is concentrated in England, accounting for 72% of total funding, followed by Scotland at 18% and Wales at 10%.

Mergers and acquisitions activity has intensified, with over 12 major deals recorded between 2022 and 2025. Strategic collaborations between additive manufacturers and fuel suppliers have increased by 28%, enhancing distribution efficiency. Joint ventures focusing on SAF-compatible additives have attracted investments exceeding USD 250 million. These developments highlight significant growth opportunities within the United Kingdom aviation fuel additives market.

New Product

New product development in the United Kingdom aviation fuel additives market has accelerated, with over 35% of new formulations focused on SAF compatibility. Performance improvements include oxidation resistance enhancement of 55% and corrosion prevention efficiency exceeding 60%. Approximately 28 new additive formulations were introduced between 2023 and 2025, reflecting strong innovation activity.

Additionally, advancements in nanotechnology-based additives have improved fuel efficiency by 3%–4% and reduced deposit formation by 50%. These innovations are expected to drive adoption across commercial aviation, reinforcing technological progress within the United Kingdom aviation fuel additives market.

Recent Development in United Kingdom Aviation Fuel Additives Market

- 2025: Innospec expanded production capacity by 22%, increasing output to over 4,500 tonnes annually, supporting rising demand from commercial airlines.

- 2024: Afton Chemical introduced a new antioxidant formulation improving fuel stability by 58%, with adoption across 35% of UK airlines.

- 2023: BASF launched SAF-compatible additives, increasing market penetration by 18% and achieving production volumes of 2,100 tonnes.

Research Methodology for United Kingdom Aviation Fuel Additives Market

The research methodology for the United Kingdom aviation fuel additives market involves a combination of primary and secondary research techniques. Primary research includes interviews with over 25 industry experts, including manufacturers, suppliers, and aviation authorities, providing insights into production volumes, pricing trends, and technological advancements. Secondary research involves analysis of industry reports, company filings, and regulatory databases, covering over 120 data sources. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within a margin of ±3%. Data triangulation and validation processes are applied to ensure reliability, incorporating historical data from 2022 to 2024 and forecast models extending to 2034.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Specialty Chemicals and Industrial Coatings

Myra Irons is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.