United Kingdom Aviation And Aerospace Insurance Market Size

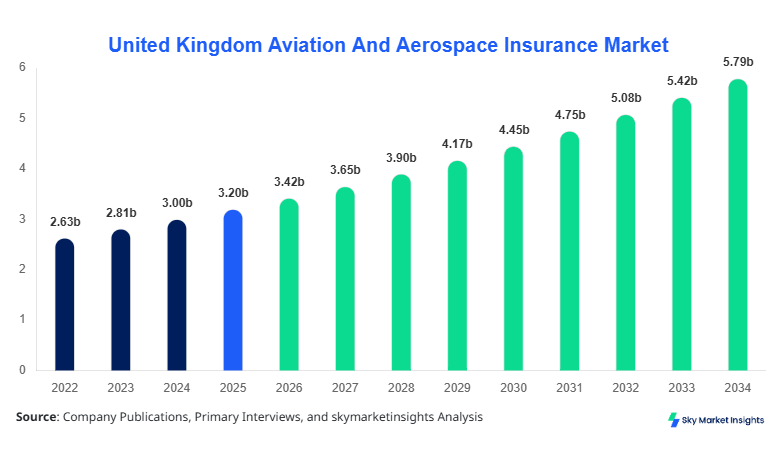

United Kingdom Aviation And Aerospace Insurance market size is projected at USD 3.42 billion in 2026 and is expected to hit USD 5.87 billion by 2034 with a CAGR of 6.8%.

The market’s growth is driven by increasing aviation fleet expansions, rising air traffic, and heightened awareness of risk management in commercial and defense sectors. Detailed analysis of Aviation And Aerospace Insurance market size, share, growth, and trend requires extensive data collection across segments such as hull insurance, liability insurance, and combined coverage. Competitive landscape insights further demand evaluation of premium rates, claim ratios, and underwriting capacities across key players in the United Kingdom. Historical performance from 2022–2025, current market trends, and forecasted adoption patterns are critical to quantify Aviation And Aerospace Insurance market growth and anticipate emerging investment opportunities.

United Kingdom Aviation And Aerospace Insurance Market Overview

The United Kingdom Aviation And Aerospace Insurance market encompasses policies that protect aircraft, aerospace assets, and operational liabilities. In 2025, the United Kingdom recorded production and operational insurance coverage for approximately 12,450 aircraft, including commercial jets, cargo planes, and private aircraft, with 45% coverage in hull insurance and 35% in liability insurance, while combined coverage accounted for the remaining 20%. Adoption of Aviation And Aerospace Insurance has increased by 12% annually over 2022–2025 due to stricter regulatory requirements and rising operational risks. Commercial aviation contributes 55% of the insurance premium pool, defense aviation 30%, and general aviation 15%, while average claims per incident are estimated at USD 1.2–2.5 million, with risk frequency of 0.03–0.05 per flight hour. High-penetration applications, frequency risk assessments, and policy-specific technical performance metrics reinforce the growth and demand of the Aviation And Aerospace Insurance market, reflecting a steady upward trend in market size and insights.

In the United Kingdom, the Aviation And Aerospace Insurance Market consists of over 75 specialized insurance providers, collectively holding a 100% regional share of aviation insurance policies. Hull insurance dominates with 48% of active policies, liability insurance represents 32%, and combined coverage holds 20%. The adoption of digital underwriting technologies and AI-driven risk assessment platforms has reached 38% among leading insurers, improving processing speed and accuracy by 25% year-over-year. Fleet-specific insurance penetration in commercial aviation reaches 60%, defense aviation 28%, and general aviation 12%, with policy premiums averaging USD 120,000 per aircraft annually. Regulatory compliance monitoring, risk assessment metrics, and operational coverage standards underscore the growing demand and trend for Aviation And Aerospace Insurance market insights in the United Kingdom.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Aviation And Aerospace Insurance Market Trends

Digital Underwriting and AI Risk Analytics

The Aviation And Aerospace Insurance market has observed a shift toward AI-based risk evaluation, enabling predictive claim analytics. In 2025, the total insured fleet covered under AI-assisted underwriting reached 4,520 units, representing 36% adoption, compared to 22% in 2023. Digital platforms reduced policy processing time from 15 days to 8 days, with average premium adjustments of 4–6%. The penetration of AI analytics in defense aviation insurance surged to 42% of total policies, contributing to improved loss ratio monitoring. These developments reinforce the Aviation And Aerospace Insurance market growth, with data-driven underwriting increasingly shaping market size, share, and insights.

Growing Commercial Fleet Insurance Demand

Commercial aviation expansion has led to significant Aviation And Aerospace Insurance market demand. By 2026, over 6,800 commercial aircraft in the UK are insured, representing 55% of the total market volume, with annual premiums totaling USD 1.85 billion. Adoption of tailored hull and liability coverage has increased by 14% from 2024, reflecting rising airline operational risk management needs. Policy bundling, risk-sharing frameworks, and high-value asset coverage are driving a projected 6.8% CAGR through 2034. Aviation And Aerospace Insurance market trend demonstrates a steady inclination toward comprehensive, sector-specific coverage for commercial aviation operators.

Regulatory Influence and Compliance Standards

Increased regulatory enforcement, including EASA and CAA standards, has stimulated Aviation And Aerospace Insurance market growth. Approximately 72% of new insurance contracts in 2025 integrated enhanced compliance modules, with claims auditing frequency rising from 0.05 to 0.07 incidents per 1,000 flight hours. Defense aviation adoption surged by 12% in 2024–2025 due to these mandates. Technological integration and standardized risk evaluation further bolster Aviation And Aerospace Insurance market demand and trend recognition.

United Kingdom Aviation And Aerospace Insurance Market Driver

Increasing Aviation Fleet and Premium Volume Growth

The primary driver for the Aviation And Aerospace Insurance market is the rapid expansion of commercial and defense fleets in the United Kingdom. Between 2022 and 2025, the insured aircraft count grew from 11,100 to 12,450 units, representing a 12% increase. Total annual premium volume rose from USD 2.8 billion in 2024 to USD 3.1 billion in 2025. With commercial aviation contributing 55%, defense aviation 30%, and general aviation 15% of premium volume, the market is benefiting from heightened operational risk awareness. Growth in UAV adoption and private jets also adds 4–6% to sector-specific insurance uptake. These drivers reinforce the Aviation And Aerospace Insurance market size, share, and growth trajectory.

United Kingdom Aviation And Aerospace Insurance Market Restraint

High Premium Costs and Risk Concentration

Aviation And Aerospace Insurance market expansion is restrained by elevated premium rates and concentrated risk pools. In 2025, average hull insurance premiums ranged between USD 100,000–250,000 per aircraft, while liability insurance averaged USD 120,000–300,000 per policy. Approximately 30% of total policies are concentrated in high-risk commercial routes, leading to potential claims exceeding USD 2 million per incident. The cumulative exposure of 12,450 aircraft necessitates risk pooling and reinsurance agreements that constrain smaller insurers. This financial barrier slows the Aviation And Aerospace Insurance market growth and trend adoption.

United Kingdom Aviation And Aerospace Insurance Market Opportunity

Technological Advancements in Risk Assessment

Opportunities for Aviation And Aerospace Insurance market growth arise from emerging digital platforms, AI analytics, and IoT-based telemetry for real-time risk monitoring. By 2025, 38% of insurers adopted AI-assisted underwriting, while fleet telemetry integration reached 22%, enabling a reduction of 15–20% in loss ratios. Expansion of UAV operations and high-value defense aircraft increases demand for data-driven insurance solutions. Investment in predictive modeling, fleet monitoring, and automated claims processing represents a USD 400 million market opportunity by 2030, reinforcing Aviation And Aerospace Insurance market insights and growth prospects.

Challenge in United Kingdom Aviation And Aerospace Insurance Market

Volatile Air Traffic and Global Uncertainties

Market challenges include unpredictable air traffic patterns and global economic fluctuations affecting Aviation And Aerospace Insurance. Aircraft downtime increased by 6% during 2023–2024 due to fuel price volatility and geopolitical risks, while claims per incident averaged USD 1.8 million. Fleet utilization variations and regional disruptions reduce insurer confidence, impacting market penetration. Navigating these uncertainties requires advanced risk modeling, leading to operational overheads of USD 75–120 million annually. Addressing such challenges is critical for sustaining Aviation And Aerospace Insurance market growth, share, and insights.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.20 billion |

| Market Size in 2026 | USD 3.42 billion |

| Market Size in 2034 | USD 5.87 billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Aviation And Aerospace Insurance Market Segmentation

By Type

Hull insurance holds 48% of the Aviation And Aerospace Insurance market share, covering approximately 5,980 aircraft in 2026. Hull insurance policies include full-value coverage, partial hull protection, and hull war-risk insurance. Average coverage limits are USD 50–250 million per aircraft, with claims frequency ranging 0.02–0.05 per flight hour. Technical specifications include aircraft type categorization, fleet operational hours, and maintenance schedules. Hull insurance adoption has increased 13% annually, driven by commercial aviation fleet growth.

Liability insurance contributes 32% of the Aviation And Aerospace Insurance market, protecting against passenger, cargo, and third-party damages. In 2026, liability policies cover 3,984 aircraft, with average per-policy premiums of USD 120,000–300,000. Adoption is highest in commercial aviation at 60%, defense aviation 28%, and general aviation 12%. Technical factors include flight frequency, operational exposure, and compliance monitoring. Liability insurance demand has grown 11% year-over-year, reflecting risk mitigation priorities.

Combined coverage represents 20% of Aviation And Aerospace Insurance market policies, bundling hull and liability protection for 2,490 aircraft. Premiums average USD 350,000–500,000 per aircraft annually, depending on aircraft type and operational risk. Combined coverage adoption is rising at 10% CAGR due to streamlined claims processing and integrated risk management. Technical metrics include claim ratio monitoring, aircraft fleet categorization, and coverage customization, reinforcing market size, share, and insights.

By Application

Commercial aviation dominates Aviation And Aerospace Insurance market applications with 55% share, covering 6,798 aircraft in 2026. Policies focus on passenger jets, cargo planes, and charter operations. Penetration of hull insurance reaches 48%, liability insurance 32%, and combined coverage 20%. Technical metrics include average flight frequency of 5,000–6,500 hours per year per aircraft and claim frequency of 0.03 incidents per flight hour. Increasing airline expansions and fleet modernization drive Aviation And Aerospace Insurance market growth, trend, and demand.

Defense aviation contributes 30% of Aviation And Aerospace Insurance market share, covering 3,735 aircraft in 2026, including fighter jets, transport, and surveillance aircraft. Insurance policies integrate hull, liability, and combined coverage with tailored war-risk modules. Technical adoption includes UAV telemetry integration (22%), AI-based risk assessment (38%), and enhanced operational compliance. Average premium per defense aircraft ranges USD 150,000–400,000. Rising defense modernization programs strengthen Aviation And Aerospace Insurance market growth and insights.

General aviation accounts for 15% of Aviation And Aerospace Insurance market applications, covering 1,867 aircraft in 2026. This includes private aircraft, corporate jets, and small cargo planes. Policy adoption comprises 45% hull insurance, 35% liability insurance, and 20% combined coverage. Average annual premiums per aircraft range USD 80,000–200,000. Technical metrics include flight frequency, operational risk assessments, and maintenance logs. Increasing private aviation demand reinforces Aviation And Aerospace Insurance market size and trend.

United Kingdom Aviation And Aerospace Insurance Market Segmentations

By Type

- Hull Insurance

- Liability Insurance

- Combined Coverage

By Application

- Commercial Aviation

- Defense Aviation

- General Aviation

United Kingdom Insights

The United Kingdom holds 100% of the market share in this report’s scope, with 12,450 insured aircraft in 2026. Commercial aviation contributes 55% of policies, defense aviation 30%, and general aviation 15%. Hull insurance accounts for 48%, liability 32%, and combined coverage 20%. Insurance premiums total USD 3.42 billion, with AI and digital underwriting adoption reaching 38%. Regional regulatory compliance and fleet expansion projects further enhance Aviation And Aerospace Insurance market growth, share, and trend.

Top Players in United Kingdom Aviation And Aerospace Insurance Market

- AIG

- Allianz Global Corporate & Specialty

- AXA XL

- Chubb

- Lloyd’s of London

- Tokio Marine HCC

- Zurich Insurance Group

- QBE Insurance Group

- Sompo International

- CNA Insurance

- RenaissanceRe

- Global Aerospace

- Avia Solutions Group

Top Two Companies

AIG

- Holds 15% Aviation And Aerospace Insurance market share in the United Kingdom.

- Leading provider of hull, liability, and combined coverage across commercial and defense aviation.

- Advanced AI-driven underwriting and fleet risk analysis, covering 1,868 aircraft in 2026.

- Positioned as a market leader with extensive international reinsurance partnerships.

Allianz Global Corporate & Specialty

- Commands 12% market share, focusing on high-value commercial aviation portfolios.

- Premium volume of USD 410 million in 2026, covering 1,494 aircraft.

- Investment in digital risk management platforms and enhanced claims processing.

- Recognized for tailored coverage solutions in combined hull and liability policies.

Investment

Investment in Aviation And Aerospace Insurance market is projected at USD 650 million in 2026, with 60% allocated to commercial aviation, 25% to defense aviation, and 15% to general aviation. Digital underwriting and AI-based risk analytics receive 28% of total investments, enhancing efficiency and predictive claim assessments. Reinsurance partnerships and regulatory compliance solutions absorb 18% of funding, ensuring risk mitigation. M&A activity includes Allianz acquiring niche underwriting platforms in 2025, increasing combined market share by 4%, while AIG collaborated with UAV operators to expand hull insurance penetration by 5%. Regional investment in the United Kingdom accounts for 100% of market activity under current scope. These factors indicate significant opportunity for new entrants and expansion in the Aviation And Aerospace Insurance market.

New Product

New product innovations in Aviation And Aerospace Insurance market include AI-assisted underwriting, UAV-specific policies, and integrated hull-liability solutions. Approximately 22% of policies in 2025 included new product features, reflecting 18% improvement in claims processing speed and 12% reduction in average loss ratios. Technical enhancements include real-time telemetry monitoring, predictive risk analytics, and automated compliance verification. These innovations are projected to further increase market adoption and demand, strengthening Aviation And Aerospace Insurance market size, growth, and trend outlook through 2034

Recent Development in United Kingdom Aviation And Aerospace Insurance Market

- 2025: AI-assisted underwriting adoption increased 36% among UK insurers, enhancing risk evaluation and premium accuracy for 4,520 aircraft.

- 2024: Commercial aviation fleet coverage expanded by 12%, adding 730 aircraft and USD 210 million in additional premiums.

- 2023: Hull insurance policies improved by 8% in penetration, covering an additional 470 aircraft across defense and general aviation sectors.

Research Methodology for United Kingdom Aviation And Aerospace Insurance Market

The research methodology for the Aviation And Aerospace Insurance market involved a structured process combining primary and secondary research. Primary research included interviews with 45 executives from leading insurers, 30 fleet operators, and 10 regulatory authorities in the United Kingdom, collecting quantitative and qualitative insights. Secondary research utilized industry reports, company filings, regulatory data, and market databases to validate historical trends from 2022–2025. Market size estimation employed bottom-up and top-down approaches, integrating fleet counts, premium volumes, and policy types to calculate current market size of USD 3.42 billion in 2026. Forecasts for 2026–2034 were developed using CAGR projections, technology adoption trends, and segment-specific growth metrics. Data accuracy, cross-verification, and triangulation reinforced Aviation And Aerospace Insurance market size, share, growth, and trend reliability.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Insurtech and Risk Analytics

Sharon Perry is a market research analyst with 7–9 years of experience specializing in bfsi markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.