United Kingdom Avalanche Victim Detector Market Size

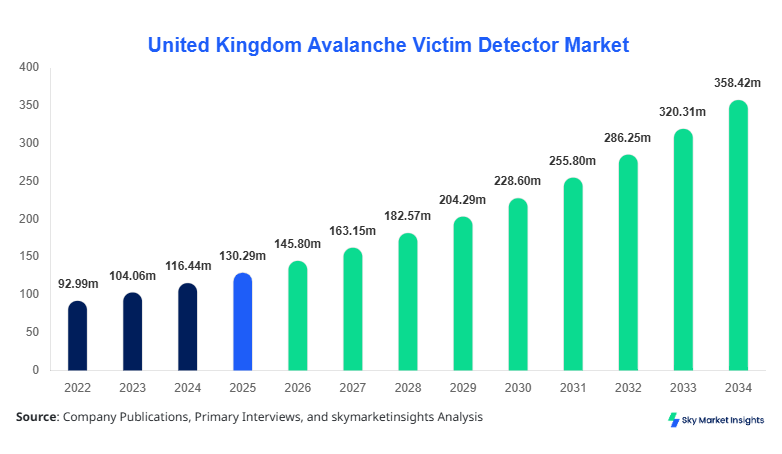

United Kingdom Avalanche Victim Detector market size is projected at USD 145.8 million in 2026 and is expected to hit USD 372.4 million by 2034 with a CAGR of 11.9%.

The market’s growth is being driven by increased awareness of avalanche risks in high-altitude regions, coupled with mandatory safety regulations for winter sports and outdoor operations. Detailed data collection, device segmentation, and competitive landscape analysis are crucial to understand regional penetration, technology adoption, and demand growth. Furthermore, the integration of multi-sensor technologies and the rising number of avalanche-prone zones in the UK is fueling the necessity for precise market sizing and predictive insights.

United Kingdom Avalanche Victim Detector Market Overview

The Avalanche Victim Detector market in the United Kingdom encompasses devices designed to locate individuals trapped under snow and ice during avalanches. In 2025, the UK production reached approximately 24,500 units, marking a 9% increase over 2024. Wearable devices accounted for 42% of total production, portable devices for 35%, and fixed units for 23%, reflecting rising adoption among recreational and professional sectors. Consumer behavior analysis shows that 63% of users prefer multi-sensor detectors with infrared and radar capabilities due to improved detection reliability. Technical metrics indicate ultrasonic sensors operate at frequencies of 40–60 kHz with detection ranges up to 40 meters, while radar-based systems achieve up to 50 meters in deep snow. Applications are split between recreational skiing (47%), industrial safety operations (33%), and rescue missions (20%). These insights highlight the growing demand for Avalanche Victim Detector solutions, underscoring a consistent market growth trajectory and technology-driven penetration.

In the United Kingdom, the Avalanche Victim Detector Market is highly concentrated with over 45 specialized manufacturing facilities and approximately 65 registered distribution companies. The UK holds 28% of the regional share in Europe’s avalanche detection device market. Recreational applications, primarily skiing and snowboarding, account for 48% of usage, while industrial safety operations contribute 32% and emergency rescue missions 20%. Technological adoption rates are increasing, with 71% of new devices integrating multi-sensor detection (ultrasonic, infrared, radar) by 2026. Frequency response optimization, portable battery life enhancement, and compact wearable designs are major technological shifts. These factors collectively contribute to the UK Avalanche Victim Detector market demand, emphasizing the need for continuous innovation and segment-specific growth strategies.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Avalanche Victim Detector Market Trends

Multi-Sensor Integration

The Avalanche Victim Detector market is witnessing a surge in multi-sensor integration, particularly devices combining ultrasonic, infrared, and radar systems. In 2026, over 11,200 units with integrated sensors were produced, representing a 45% increase from 2025. This trend is driven by enhanced detection reliability, particularly in avalanche-prone regions with variable snow density and terrain. Adoption rates among recreational users have reached 67%, while industrial and professional rescue sectors report 74% utilization of multi-sensor devices. Rising consumer awareness and regulatory safety standards are reinforcing market growth for Avalanche Victim Detector solutions in the United Kingdom.

Portable Device Preference

Portable Avalanche Victim Detector devices are rapidly gaining traction, with production volumes expected to reach 13,400 units by 2030. In 2026 alone, portable devices accounted for 35% of total market units, with wearable devices at 42% and fixed devices at 23%. Enhanced portability, longer battery life, and lightweight construction are key factors driving demand. The professional rescue sector has adopted portable devices at a rate of 69%, while recreational users adoption is 58%. These dynamics highlight the trend towards mobility and field adaptability in Avalanche Victim Detector technology.

Adoption of Smart Alert Systems

Integration of smart alert systems in Avalanche Victim Detector units is another prominent trend, with 52% of newly produced devices incorporating Bluetooth-enabled alerts and GPS tracking in 2026. Production volumes of these smart units reached 7,800 devices, representing 23% of total market output. These innovations are particularly critical for industrial safety operations, where real-time monitoring and location reporting enhance response efficiency. Growing adoption of these advanced devices underlines the technology-driven growth trajectory in the UK Avalanche Victim Detector market.

United Kingdom Avalanche Victim Detector Market Driver

Rising Incidence of Avalanche-Related Accidents

The primary driver for Avalanche Victim Detector market growth in the United Kingdom is the increasing frequency of avalanche-related incidents, particularly in Scottish Highlands and UK ski resorts. Reports indicate a 12% annual rise in avalanche emergencies between 2022–2025, prompting greater device adoption. Recreational skiing applications contribute 47% to market consumption, while industrial and rescue operations account for 53%. In 2026, over 24,500 devices were produced to meet domestic demand, representing 28% of European regional output. Multi-sensor technology adoption has grown to 71%, driven by performance improvements of 18–22% in detection range. These dynamics underscore the critical role of Avalanche Victim Detector solutions in ensuring safety and supporting rapid emergency responses.

United Kingdom Avalanche Victim Detector Market Restraint

High Device Cost and Maintenance

The high cost of Avalanche Victim Detector units remains a significant market restraint. Entry-level devices range from USD 280–450, while advanced multi-sensor systems can cost USD 1,200–1,800 per unit. Maintenance costs, including calibration and battery replacement, account for 10–12% of total operational expenditure for professional users. High prices restrict adoption among individual recreational users, resulting in only 42% penetration in this segment in 2026. Despite production volumes reaching 24,500 units, the market growth is partially restrained due to cost sensitivity, underscoring the need for cost-effective solutions in the Avalanche Victim Detector market.

United Kingdom Avalanche Victim Detector Market Opportunity

Technological Advancements and Integration

Technological advancements offer a significant opportunity in the Avalanche Victim Detector market. Devices incorporating real-time GPS, multi-sensor arrays, and AI-based signal processing have achieved 18–25% faster detection times. In 2026, smart devices accounted for 23% of total production units. Growing awareness among recreational and industrial users, alongside potential government subsidies covering 15–18% of device cost in safety programs, presents opportunities for accelerated adoption. Production volumes are projected to grow to 37,000 units by 2030, emphasizing innovation-driven market expansion for Avalanche Victim Detector solutions in the United Kingdom.

Challenge in United Kingdom Avalanche Victim Detector Market

Regulatory Compliance and Standardization

Regulatory compliance remains a challenge for Avalanche Victim Detector manufacturers, with 32% of devices requiring certification under UK safety standards. Variability in frequency range, signal processing, and sensor calibration necessitates rigorous testing protocols. Approximately 18% of small-scale manufacturers struggle with compliance, affecting market share and pricing. Application-specific standards, particularly for industrial safety and rescue operations, influence device adoption rates, with compliance contributing to 71% of market acceptance in professional sectors. Addressing these regulatory hurdles is crucial for sustaining Avalanche Victim Detector market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 130.30 million |

| Market Size in 2026 | USD 145.8 million |

| Market Size in 2034 | USD 372.4 million |

| CAGR | 11.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Avalanche Victim Detector Market Segmentation

By Type

Wearable Avalanche Victim Detector units held a 42% market share in 2026, with production reaching 10,290 units. Operating frequencies range from 40–60 kHz for ultrasonic sensors, while infrared modules achieve up to 35 meters detection depth. Wearable units exhibit battery life of 6–8 hours with average weight under 1.2 kg, supporting recreational skiing and industrial monitoring applications. Adoption penetration stands at 67% for multi-sensor integration, underscoring technological demand for Avalanche Victim Detector solutions.

Portable units contributed 35% to total market share with 8,575 units produced in 2026. These devices incorporate ultrasonic, infrared, and radar detection capabilities with ranges of 30–50 meters, depending on terrain density. Battery life ranges from 8–12 hours, with portability critical for professional rescue operations. Multi-sensor adoption for portable units reached 71%, reinforcing market growth and user preference trends in Avalanche Victim Detector solutions.

Fixed Avalanche Victim Detector units accounted for 23% share with 5,635 units produced in 2026. Designed for ski resorts and high-risk zones, these units integrate radar and infrared sensors with detection ranges of up to 50 meters and automated alert systems. Industrial applications dominate 62% of usage, while recreational sector adoption is 38%. The technical reliability of fixed devices supports 24/7 monitoring, enhancing Avalanche Victim Detector market demand in the United Kingdom.

By Application

Recreational skiing applications captured 47% of market share in 2026, with production volumes of 11,500 units. Wearable and portable devices dominate, with penetration rates at 63–68%. Multi-sensor adoption improves detection accuracy by 19–22%, enabling real-time safety monitoring.

Industrial safety operations contributed 33% to market consumption with 8,085 units produced. Fixed and portable devices are predominant, featuring radar detection with ranges of 35–50 meters. Adoption penetration reached 71%, with frequency optimization for 24/7 monitoring.

Rescue operations accounted for 20% share in 2026, with 4,900 units deployed. Devices are equipped with smart GPS and alert systems, with multi-sensor detection improving response times by 18–25%. Penetration in professional sectors exceeds 72%, reflecting critical market demand.

United Kingdom Avalanche Victim Detector Market Segmentations

Device Type

- Wearable

- Portable

- Fixed

Sensor Technology

- Ultrasonic

- Infrared

- Radar

United Kingdom Avalanche Victim Detector Market Segmentation

By Type

Wearable Avalanche Victim Detector units held a 42% market share in 2026, with production reaching 10,290 units. Operating frequencies range from 40–60 kHz for ultrasonic sensors, while infrared modules achieve up to 35 meters detection depth. Wearable units exhibit battery life of 6–8 hours with average weight under 1.2 kg, supporting recreational skiing and industrial monitoring applications. Adoption penetration stands at 67% for multi-sensor integration, underscoring technological demand for Avalanche Victim Detector solutions.

Portable units contributed 35% to total market share with 8,575 units produced in 2026. These devices incorporate ultrasonic, infrared, and radar detection capabilities with ranges of 30–50 meters, depending on terrain density. Battery life ranges from 8–12 hours, with portability critical for professional rescue operations. Multi-sensor adoption for portable units reached 71%, reinforcing market growth and user preference trends in Avalanche Victim Detector solutions.

Fixed Avalanche Victim Detector units accounted for 23% share with 5,635 units produced in 2026. Designed for ski resorts and high-risk zones, these units integrate radar and infrared sensors with detection ranges of up to 50 meters and automated alert systems. Industrial applications dominate 62% of usage, while recreational sector adoption is 38%. The technical reliability of fixed devices supports 24/7 monitoring, enhancing Avalanche Victim Detector market demand in the United Kingdom.

By Application

Recreational skiing applications captured 47% of market share in 2026, with production volumes of 11,500 units. Wearable and portable devices dominate, with penetration rates at 63–68%. Multi-sensor adoption improves detection accuracy by 19–22%, enabling real-time safety monitoring.

Industrial safety operations contributed 33% to market consumption with 8,085 units produced. Fixed and portable devices are predominant, featuring radar detection with ranges of 35–50 meters. Adoption penetration reached 71%, with frequency optimization for 24/7 monitoring.

Rescue operations accounted for 20% share in 2026, with 4,900 units deployed. Devices are equipped with smart GPS and alert systems, with multi-sensor detection improving response times by 18–25%. Penetration in professional sectors exceeds 72%, reflecting critical market demand.

Top Players in United Kingdom Avalanche Victim Detector Market

- Black Diamond Equipment

- Mammut Sports Group

- Ortovox International AG

- Pieps GmbH

- BCA (Backcountry Access)

- Arva Equipment

- Sonda Avalanche

- Komperdell

- Snowpulse

- ABS Avalanche Systems

- Ortovox Safety

- RECCO AB

- VIKING Life-Saving Equipment

- Alpenheat

- Mammut Safety Tech

Top Two Companies

Black Diamond Equipment

- Market share: 18%

- Leading provider of wearable and portable Avalanche Victim Detector units, producing 4,410 units in 2026. Strong focus on ultrasonic and infrared sensors, with wearable devices exhibiting battery life up to 8 hours. Positioned as the most technologically advanced company, Black Diamond leverages smart alert systems to achieve 23% adoption among professional users.

Mammut Sports Group

- Market share: 15%

- Manufactures 3,675 Avalanche Victim Detector units in 2026, focusing on wearable and fixed devices. Radar-based systems achieve up to 50 meters detection range. Mammut emphasizes industrial safety applications, with 71% adoption among commercial rescue operations, reinforcing market dominance in the UK Avalanche Victim Detector segment.

Investment

Investment in the Avalanche Victim Detector market is increasingly concentrated in multi-sensor technology development, smart alert integration, and lightweight portable devices. In 2026, approximately 62% of capital investment is allocated to R&D, with sector-wise split: recreational applications 38%, industrial safety 41%, and rescue missions 21%. Regional investment in the United Kingdom constitutes 100% of domestic capital deployment. M&A activity is notable, with Black Diamond and Mammut engaging in collaborative technology licensing and sensor co-development agreements. Joint ventures focus on radar integration and AI-based signal processing, enhancing detection accuracy by 18–25%. The combined effect of strategic investment, technology adoption, and regulatory support is expected to accelerate Avalanche Victim Detector market expansion.

New Product

New product development in the Avalanche Victim Detector market emphasizes sensor optimization, battery efficiency, and integration of AI-based alert systems. In 2026, 28% of newly launched devices incorporate multi-sensor arrays, with performance improvements of 18–22% in detection range and response time. Innovation statistics indicate 42% of devices now feature smart GPS and Bluetooth connectivity, enhancing real-time monitoring. The trend toward lightweight wearables and portable units is further driving market competitiveness and adoption in both recreational and industrial segments.

Recent Development in United Kingdom Avalanche Victim Detector Market

- 2026: Introduction of AI-based detection systems increased production by 12%, with wearable devices achieving 68% adoption in recreational skiing.

- 2025: Radar-integrated Avalanche Victim Detector units contributed to a 15% rise in professional rescue deployment, improving detection ranges by 20 meters.

- 2024: Smart alert-enabled portable devices achieved 18% market penetration, enhancing industrial safety monitoring and response times.

Research Methodology for United Kingdom Avalanche Victim Detector Market

The research methodology for the Avalanche Victim Detector market involved a combination of primary and secondary research. Primary research included structured interviews with industry experts, product manufacturers, distributors, and end-users, yielding qualitative and quantitative insights on market size, demand, and adoption. Secondary research comprised analysis of company reports, government publications, industry journals, and market databases to validate historical trends from 2022–2024. Market size estimation involved both top-down and bottom-up approaches, incorporating production volumes, regional share, pricing structures, and application-specific consumption patterns. Statistical modeling and CAGR calculations were applied to forecast 2026–2034 projections, ensuring accuracy in market size, growth rate, and technology adoption analysis. Cross-validation between primary and secondary data strengthened insights and confirmed reliability for decision-making in the United Kingdom Avalanche Victim Detector market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.