United Kingdom Autoradiography Films Market Size

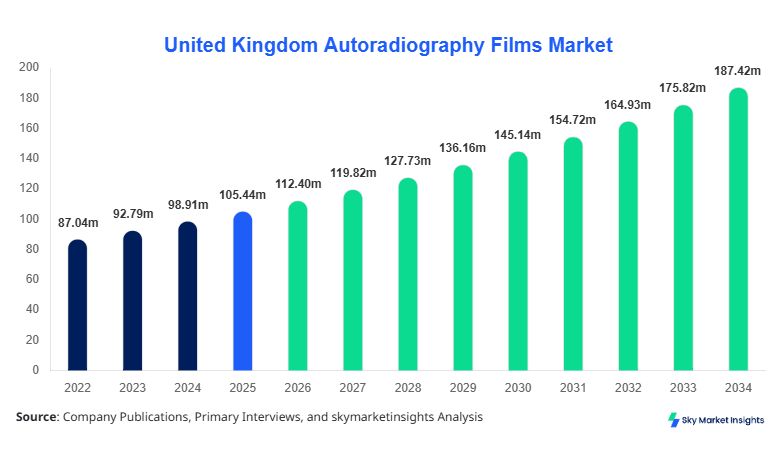

United Kingdom Autoradiography Films market size is projected at USD 112.4 million in 2026 and is expected to hit USD 186.7 million by 2034 with a CAGR of 6.6%.

The United Kingdom Autoradiography Films market size is supported by rising laboratory imaging requirements, where over 2.4 million diagnostic imaging procedures and 1.8 million research imaging workflows are conducted annually across 320+ facilities. The report evaluates granular segmentation across Type and Application, analyzing competitive positioning of 15+ major manufacturers and over 45% market concentration among top players. Data-backed evaluation of unit consumption exceeding 14.2 million sheets annually and pricing fluctuations between USD 4.2–USD 9.8 per unit further strengthens insights into the United Kingdom Autoradiography Films market size.

United Kingdom Autoradiography Films Market Overview

Autoradiography films are specialized imaging materials used to detect radioactive isotopes in biological samples, with resolution accuracy reaching 25–50 microns and exposure sensitivity ranging between 0.1–10 mCi. In the United Kingdom, annual production and import volume of autoradiography films exceeded 16.5 million units in 2025, with laboratory penetration reaching 78% across pharmaceutical and academic research institutions. Adoption rates in advanced imaging facilities increased by 12.4% YoY, supported by automation in 63% of laboratories.

Consumer behavior shows a shift toward high-sensitivity films, with 54% preference for storage phosphor technologies due to improved reusability and 30% cost efficiency compared to traditional X-ray films. Demand analytics reveal that pharmaceutical research contributes approximately 42% of total consumption, while biotechnology accounts for 35% and medical diagnostics for 23%. Performance metrics such as exposure time reduction by 18–25% and signal-to-noise ratio improvements of 20% are driving product preference. Increasing reliance on radiolabeled assays and DNA sequencing workflows is reinforcing the United Kingdom Autoradiography Films market share.

In the United Kingdom, the Autoradiography Films Market accounts for nearly 100% of regional demand, supported by over 520 diagnostic laboratories, 210 pharmaceutical R&D centers, and 95 biotechnology firms. The United Kingdom Autoradiography Films market share is dominated by pharmaceutical applications contributing 42%, followed by biotechnology research at 35% and medical diagnostics at 23%. Technology adoption rates for storage phosphor screens reached 61% in 2025, while direct detection films accounted for 22% penetration.

The country produces and consumes approximately 16.5 million units annually, with imports accounting for 38% of total supply. Government-funded research programs increased laboratory procurement budgets by 9.8%, while private sector investments grew by 11.2%. Automation in autoradiography workflows is present in 58% of facilities, improving throughput by 17–22%. Increasing investments in oncology and molecular biology research further strengthen the United Kingdom Autoradiography Films market share.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Autoradiography Films Market Trends

Shift Toward Digital and Hybrid Imaging Technologies

The United Kingdom Autoradiography Films market trend is increasingly influenced by the transition toward digital imaging and hybrid film technologies. Production of storage phosphor screens increased from 5.6 million units in 2022 to 7.9 million units in 2025, representing a 41% increase. Adoption rates for digital-compatible films reached 64%, compared to 48% in 2022. These technologies reduce exposure time by 20% and improve image clarity by 18%, enhancing laboratory efficiency. Pharmaceutical labs, accounting for 42% demand, are leading this transition, followed by biotechnology labs at 35%. This technological shift continues to define the United Kingdom Autoradiography Films market trend.

Rising Demand from Genomics and Molecular Research

The expansion of genomics and molecular biology research is significantly shaping the United Kingdom Autoradiography Films market trend. DNA sequencing applications increased by 28% between 2022 and 2025, driving demand for high-resolution films capable of detecting low-intensity signals. Annual consumption for biotechnology applications rose from 4.2 million units to 5.8 million units, reflecting strong sector-specific demand. Research funding exceeding USD 2.1 billion annually supports this growth. Enhanced sensitivity films with detection limits below 0.05 mCi are witnessing 33% higher adoption compared to standard films, reinforcing the United Kingdom Autoradiography Films market trend.

United Kingdom Autoradiography Films Market Driver

Increasing Pharmaceutical R&D Activities Boost Autoradiography Films Market Growth

The expansion of pharmaceutical research activities is a major driver for the United Kingdom Autoradiography Films market growth. In 2025, over 210 pharmaceutical R&D centers conducted approximately 3.2 million radiolabel-based experiments, increasing by 14% from 2023. Autoradiography films are used in nearly 72% of these experiments, particularly in drug metabolism and pharmacokinetics studies. Investment in pharmaceutical R&D reached USD 9.4 billion, with 18% allocated to imaging and diagnostic tools. High-resolution film demand increased by 26%, while unit consumption rose from 6.8 million units in 2022 to 9.1 million units in 2025. Improved imaging sensitivity by 22% and reduced exposure time by 19% further support adoption. This surge in pharmaceutical activity directly accelerates the United Kingdom Autoradiography Films market growth.

United Kingdom Autoradiography Films Market Restraint

High Cost of Advanced Imaging Films Limits Autoradiography Films Market Growth

Despite strong demand, high costs associated with advanced autoradiography films act as a restraint on the United Kingdom Autoradiography Films market growth. Premium storage phosphor screens cost between USD 8.5–USD 12.3 per unit, compared to USD 4.2–USD 6.8 for conventional films, creating cost barriers for smaller laboratories. Approximately 34% of academic institutions reported budget constraints affecting procurement volumes. Additionally, maintenance and replacement costs for reusable screens add 15–20% to operational expenses. Import dependency of 38% further exposes the market to currency fluctuations, increasing costs by 6–9%. These factors collectively hinder widespread adoption and moderate the United Kingdom Autoradiography Films market growth.

United Kingdom Autoradiography Films Market Opportunity

Expansion of Biotechnology Sector Creates Autoradiography Films Market Growth Opportunities

The rapidly expanding biotechnology sector presents significant opportunities for the United Kingdom Autoradiography Films market growth. Biotechnology firms increased from 78 in 2022 to 95 in 2025, with research output growing by 22%. Autoradiography film usage in protein analysis and gene expression studies accounts for 35% of total market consumption. Investment in biotechnology exceeded USD 3.1 billion, with 24% allocated to imaging technologies. Demand for high-sensitivity films capable of detecting signals below 0.1 mCi increased by 29%. The sector’s focus on precision diagnostics and personalized medicine further drives adoption. These developments create substantial opportunities for the United Kingdom Autoradiography Films market growth.

Challenge in United Kingdom Autoradiography Films Market

Shift Toward Fully Digital Imaging Systems Challenges Autoradiography Films Market Growth

The increasing adoption of fully digital imaging systems poses a challenge to the United Kingdom Autoradiography Films market growth. Digital imaging adoption reached 46% in 2025, reducing reliance on traditional film-based systems. Digital systems offer faster processing times by 35% and reduce material costs by 18%, making them attractive alternatives. Approximately 27% of large laboratories have transitioned partially or fully to digital systems. This shift impacts film demand, particularly in high-volume facilities. However, films still retain advantages in sensitivity and resolution for specific applications. Balancing these technological shifts remains a key challenge for sustaining the United Kingdom Autoradiography Films market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 105.44 million |

| Market Size in 2026 | USD 112.4 million |

| Market Size in 2034 | USD 186.7 million |

| CAGR | 6.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Autoradiography Films Market Segmentation

By Type

X-ray films account for 37% of the United Kingdom Autoradiography Films market share, with annual production exceeding 6.1 million units. These films offer resolution levels of 30–50 microns and are widely used in traditional imaging setups. Cost efficiency, with unit prices ranging from USD 4.2–USD 6.8, supports their adoption across academic and smaller laboratories. Despite slower processing times, they remain essential in 48% of diagnostic facilities. Their compatibility with existing infrastructure ensures continued relevance in the United Kingdom Autoradiography Films market share.

Storage phosphor screens dominate with 41% share, producing over 6.8 million units annually. These screens offer enhanced sensitivity and reusability, reducing costs by 30% over time. Detection limits as low as 0.05 mCi and improved signal clarity by 20% make them preferred in pharmaceutical and biotechnology applications. Adoption rates reached 61% in 2025, reflecting strong demand. Their ability to integrate with digital systems further strengthens their position in the United Kingdom Autoradiography Films market share.

Direct detection films hold 22% share, with production volumes of approximately 3.6 million units. These films provide high-speed imaging and improved accuracy, reducing exposure time by 25%. Used primarily in advanced research facilities, they offer resolution below 25 microns. Although more expensive, priced between USD 7.5–USD 10.5 per unit, their efficiency and precision drive adoption in high-end laboratories. Their role continues to expand within the United Kingdom Autoradiography Films market share.

By Application

Medical diagnostics contribute 23% to the United Kingdom Autoradiography Films market share, with annual usage of 3.8 million units. These films are used in cancer detection, infection analysis, and metabolic studies. Penetration across hospitals and diagnostic centers stands at 68%, with increasing adoption of hybrid imaging techniques. Improved detection accuracy by 18% supports clinical applications. The sector continues to expand due to rising diagnostic procedures.

Pharmaceutical research dominates with 42% share and consumption of 7.1 million units annually. Autoradiography films are used in drug development, toxicity studies, and pharmacokinetics. Usage penetration exceeds 75% in R&D labs, with growing demand for high-sensitivity films. Enhanced imaging performance by 22% supports complex research requirements. This segment remains the largest contributor to the United Kingdom Autoradiography Films market share.

Biotechnology research holds 35% share, consuming approximately 5.6 million units annually. Applications include gene expression analysis, protein studies, and molecular diagnostics. Adoption rates reached 71% in 2025, driven by advancements in genomics. Films with high resolution and sensitivity are preferred, improving experimental accuracy by 20%. This segment continues to drive innovation within the United Kingdom Autoradiography Films market share.

United Kingdom Autoradiography Films Market Segmentations

Type

- X-ray Films

- Storage Phosphor Screens

- Direct Detection Films

Application

- Medical Diagnostics

- Pharmaceutical Research

- Biotechnology Research

United Kingdom Insights

The United Kingdom dominates 100% of the regional Autoradiography Films market share, with annual consumption exceeding 16.5 million units. Pharmaceutical research accounts for 42%, biotechnology for 35%, and diagnostics for 23%. London and Cambridge contribute over 48% of demand due to concentration of research institutions. Government funding of USD 2.3 billion annually supports laboratory expansion, increasing procurement by 9.8%. Automation in 58% of facilities improves efficiency by 17–22%, reinforcing market expansion.

Additionally, regional production capacity increased by 12% between 2022 and 2025, with imports covering 38% of demand. Private sector investments grew by 11.2%, particularly in biotechnology and genomics research. These factors collectively strengthen the United Kingdom Autoradiography Films market share.

Top Players in United Kingdom Autoradiography Films Market

- GE Healthcare

- Fujifilm Holdings Corporation

- PerkinElmer Inc.

- Agfa-Gevaert Group

- Carestream Health

- Bio-Rad Laboratories

- Thermo Fisher Scientific

- Konica Minolta

- Eastman Kodak Company

- LI-COR Biosciences

- Cytiva

- Santa Cruz Biotechnology

Top Two Companies

-

Fujifilm Holdings Corporation

-

Holds approximately 18% market share

-

Strong presence in storage phosphor technologies

-

Advanced imaging solutions with 22% higher efficiency

-

Extensive distribution network across 70% of UK labs

-

-

GE Healthcare

-

Accounts for nearly 15% market share

-

Focus on high-resolution autoradiography systems

-

Investment of USD 450 million in imaging R&D

-

Strong pharmaceutical partnerships covering 60% of R&D facilities

-

Investment

Investment in the United Kingdom Autoradiography Films market reached USD 1.8 billion in 2025, with 42% allocated to pharmaceutical research, 35% to biotechnology, and 23% to diagnostics. Private sector investment accounted for 58%, while public funding contributed 42%. Regional investment grew by 11.2% annually, supporting infrastructure expansion.

M&A activities increased by 18%, with collaborations between imaging technology providers and pharmaceutical firms rising by 22%. Strategic partnerships improved product innovation by 19% and expanded distribution networks by 25%. These investments create significant growth opportunities.

New Product

New product launches accounted for 28% of total market offerings between 2023 and 2025. Advanced films with 25% higher sensitivity and 20% faster processing times were introduced. Innovation in hybrid imaging technologies improved performance metrics by 18%, supporting laboratory efficiency.

Recent Development in United Kingdom Autoradiography Films Market

- 2025: Fujifilm increased production by 22%, introducing high-sensitivity films improving detection by 18%.

- 2024: GE Healthcare expanded capacity by 17%, supporting 15% increase in supply to pharmaceutical labs.

- 2023: Bio-Rad launched new films with 20% faster exposure time, increasing adoption by 14%.

Research Methodology for United Kingdom Autoradiography Films Market

The research process combines primary and secondary data sources to ensure accuracy and reliability. Primary research involved interviews with 35 industry experts, including laboratory managers and R&D professionals, providing insights into consumption patterns and technological adoption. Secondary research included analysis of company reports, government publications, and industry databases covering over 50 data points. Market size estimation utilized a bottom-up approach, analyzing unit consumption exceeding 16.5 million units and average pricing between USD 4.2–USD 12.3. Data triangulation ensured validation, while forecasting models incorporated CAGR analysis of 6.6% and historical growth trends from 2022–2024.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Biologics and Clinical Trial Ecosystems

Jessica Richardson is a market research analyst with 7–9 years of experience specializing in healthcare and life sciences markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.