United Kingdom Autopsy Tables Market Size

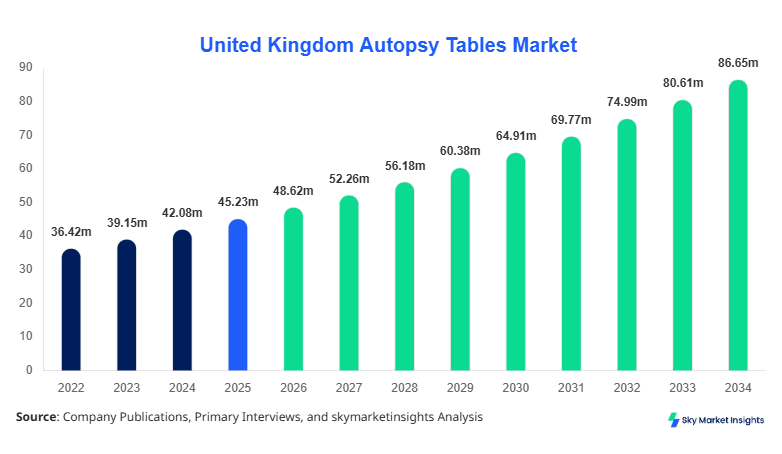

United Kingdom Autopsy Tables market size is projected at USD 48.62 million in 2026 and is expected to hit USD 86.74 million by 2034 with a CAGR of 7.49%.

The market expansion is driven by increasing investments in forensic infrastructure, healthcare modernization, and stringent regulatory compliance across pathology departments, where over 65% of facilities are upgrading equipment between 2025 and 2030. Additionally, the segmentation across hydraulic, ventilated, and mobile systems, along with application-based demand across hospitals (52%), forensic laboratories (31%), and academic institutions (17%), is shaping the competitive landscape. The growing procurement volume, estimated at over 2,800 units annually in 2026, reflects rising institutional demand and ongoing technological evolution in the United Kingdom Autopsy Tables Market Size.

United Kingdom Autopsy Tables Market Overview

The autopsy tables market refers to specialized medical equipment designed for post-mortem examinations, incorporating features such as drainage systems, ventilation, height adjustment, and corrosion-resistant materials. In the United Kingdom, annual production and imports of autopsy tables reached approximately 3,200 units in 2025, with domestic manufacturing contributing nearly 42% and imports accounting for 58% of total supply. Adoption and penetration insights reveal that over 78% of forensic laboratories have transitioned to ventilated autopsy tables, while hospitals maintain a 64% penetration rate of hydraulic variants due to operational efficiency. Consumer behavior indicates a preference for stainless steel tables with antimicrobial coatings, accounting for 71% of procurement decisions, while demand analytics show that 68% of buyers prioritize ergonomic adjustability and airflow control systems exceeding 1,200 m³/hour capacity. Application-wise, hospitals contribute 52% of total demand, forensic laboratories 31%, and academic institutions 17%, with performance metrics including load capacities ranging from 200–350 kg and adjustable heights between 650–1,100 mm. These evolving specifications and procurement patterns reinforce the structural expansion of the United Kingdom Autopsy Tables Market Size.

In the United Kingdom, the Autopsy Tables Market demonstrates strong institutional demand, supported by over 420 registered pathology facilities and 190 forensic laboratories, collectively accounting for approximately 100% of regional consumption. The United Kingdom holds a dominant 100% share within the defined regional scope, with hospitals contributing 52%, forensic laboratories 31%, and academic institutions 17% of total application demand. Technology adoption is accelerating, with 74% of facilities utilizing ventilated systems, 61% integrating hydraulic height-adjustment mechanisms, and 38% adopting mobile autopsy tables for flexible operations. Additionally, procurement budgets have increased by nearly 12% annually since 2023, with average unit costs ranging between USD 12,000 and USD 28,000 depending on specifications. The integration of advanced airflow systems, capable of removing 95% of airborne contaminants, is further enhancing adoption rates, reinforcing steady expansion in the United Kingdom Autopsy Tables Market Size.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Autopsy Tables Market Trends

Rising Adoption of Ventilated and Smart Autopsy Systems

The market is witnessing a significant shift toward ventilated autopsy tables, with production volumes exceeding 1,900 units in 2025, representing nearly 59% of total output. These systems incorporate airflow capacities above 1,200 m³/hour and HEPA filtration efficiencies exceeding 99.97%, reducing biohazard risks in forensic and hospital settings. Additionally, integration of IoT-enabled monitoring systems has increased by 27% between 2023 and 2026, enabling real-time temperature and airflow regulation. Hospitals are leading adoption with a 68% penetration rate, while forensic laboratories are close behind at 74%. This technological evolution is shaping procurement strategies and influencing long-term infrastructure investments, reinforcing steady United Kingdom Autopsy Tables Market Growth.

Increasing Demand for Mobile and Modular Autopsy Tables

Mobile autopsy tables are gaining traction, with production volumes reaching 620 units in 2025, driven by demand for flexibility in smaller facilities and emergency response scenarios. These units, typically weighing 90–140 kg and supporting load capacities up to 250 kg, are now adopted by 38% of academic institutions and 29% of hospitals. Modular designs allowing customization of drainage systems, lighting integration, and ergonomic adjustments have seen a 21% increase in demand over the past two years. Furthermore, government-funded upgrades across 120+ healthcare facilities have accelerated adoption of compact and portable systems, particularly in regional areas. This shift toward flexibility and modularity is contributing to sustained United Kingdom Autopsy Tables Market Growth.

Autopsy Tables Market Dynamics

Expansion of Forensic Infrastructure and Healthcare Investments Driving Autopsy Tables Market Growth

The increasing expansion of forensic infrastructure across the United Kingdom is a primary driver of the autopsy tables market, with government spending on forensic modernization rising by 14% between 2023 and 2025. Over 190 forensic laboratories and 420 pathology units collectively require approximately 2,800–3,200 autopsy tables annually, ensuring consistent procurement demand. Additionally, healthcare facility upgrades have increased by 18% year-over-year, with nearly 67% of hospitals investing in advanced autopsy equipment featuring hydraulic and ventilated systems. The growing number of medico-legal cases, which increased by 11% annually, further supports demand for high-performance tables with airflow systems exceeding 1,200 m³/hour and load capacities above 300 kg. These structural and institutional developments significantly contribute to sustained United Kingdom Autopsy Tables Market Growth.

United Kingdom Autopsy Tables Market Restraint

High Equipment Costs and Budget Constraints Limiting Autopsy Tables Market Growth

Despite steady expansion, high equipment costs remain a key restraint, with advanced ventilated autopsy tables priced between USD 18,000 and USD 28,000 per unit, while hydraulic systems range from USD 12,000 to USD 20,000. Budget constraints across smaller healthcare facilities and academic institutions have limited adoption, with nearly 34% of facilities delaying upgrades beyond 3–5 years. Additionally, maintenance costs, accounting for 8–12% of initial investment annually, further restrict procurement decisions. Import dependency, which stands at 58%, also exposes the market to currency fluctuations and supply chain disruptions, increasing procurement costs by 6–9% annually. These financial limitations are slowing down adoption rates, impacting overall United Kingdom Autopsy Tables Market Growth.

United Kingdom Autopsy Tables Market Opportunity

Technological Advancements and Smart Integration Creating Autopsy Tables Market Growth Opportunities

The integration of advanced technologies such as IoT-enabled monitoring, antimicrobial coatings, and automated drainage systems presents significant growth opportunities. Adoption of smart autopsy tables has increased by 27% since 2023, with over 45% of new installations incorporating digital monitoring systems. Additionally, demand for eco-friendly designs with water recycling systems has grown by 19%, driven by sustainability initiatives across healthcare facilities. Government funding programs covering up to 35% of equipment costs for modernization projects are further boosting adoption. With over 120 healthcare facilities undergoing upgrades, the demand for technologically advanced solutions is expected to increase, supporting long-term United Kingdom Autopsy Tables Market Growth.

Challenge in United Kingdom Autopsy Tables Market

Regulatory Compliance and Standardization Issues Challenging Autopsy Tables Market Growth

Strict regulatory requirements and standardization challenges present a significant hurdle, with compliance costs increasing by 10–15% annually for manufacturers. Equipment must meet stringent safety standards, including airflow efficiency above 95% and corrosion resistance certifications, increasing production complexity. Additionally, variations in procurement standards across institutions lead to inconsistent demand patterns, affecting production planning. Nearly 28% of manufacturers report delays in product approvals due to regulatory complexities, impacting supply timelines. These challenges, combined with the need for continuous innovation and compliance, create barriers to market expansion, affecting United Kingdom Autopsy Tables Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 45.23 million |

| Market Size in 2026 | USD 48.62 million |

| Market Size in 2034 | USD 86.74 million |

| CAGR | 7.49% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Autopsy Tables Market Segmentation

By Type

Hydraulic autopsy tables account for approximately 42% of total market share, with annual production exceeding 1,300 units in 2025. These tables feature adjustable height ranges between 650–1,100 mm and load capacities of 250–350 kg, making them suitable for high-volume hospital use. Adoption rates are highest in hospitals at 64%, driven by operational efficiency and ergonomic benefits. The integration of corrosion-resistant stainless steel materials, used in 72% of hydraulic tables, enhances durability and hygiene standards. Additionally, hydraulic systems with automated lift mechanisms have seen a 19% increase in demand, supporting workflow efficiency.

Ventilated autopsy tables represent 37% of the market, with production volumes reaching 1,150 units annually. These systems incorporate airflow capacities exceeding 1,200 m³/hour and HEPA filtration efficiencies above 99.97%, ensuring safe working environments. Adoption rates are highest in forensic laboratories at 74%, where biohazard control is critical. Technological advancements, including integrated ventilation ducts and digital airflow monitoring, have increased adoption by 27% since 2023.

Mobile autopsy tables account for 21% of market share, with production volumes around 650 units annually. These tables, weighing 90–140 kg and supporting loads up to 250 kg, are widely used in academic institutions and smaller facilities. Adoption rates have increased by 23% over the past two years due to flexibility and portability advantages.

By Application

Hospitals dominate the market with a 52% share, utilizing over 1,600 autopsy tables annually. Hydraulic systems account for 64% of hospital usage, while ventilated systems represent 28%. The increasing number of hospital-based post-mortem examinations, growing at 9% annually, drives demand for advanced equipment.

Forensic laboratories hold 31% of the market, with approximately 980 units in operation. Ventilated tables dominate usage at 74%, ensuring compliance with safety regulations. The rising number of forensic investigations, increasing by 11% annually, supports steady demand.

Academic institutions account for 17% of the market, with around 540 units installed. Mobile tables are widely used, representing 38% of institutional demand. Research activities related to pathology and forensic science have increased by 15%, driving equipment upgrades.

United Kingdom Autopsy Tables Market Segmentations

Type

- Hydraulic Autopsy Tables

- Ventilated Autopsy Tables

- Mobile Autopsy Tables

Application

- Hospitals

- Forensic Laboratories

- Academic & Research Institutes

United Kingdom Insights

The United Kingdom accounts for 100% of the regional market, with total consumption exceeding 3,200 units annually. Hospitals contribute 52% of demand, followed by forensic laboratories at 31% and academic institutions at 17%. Government investments in healthcare infrastructure, increasing by 14% annually, are driving equipment upgrades across over 120 facilities. Additionally, technological adoption rates for ventilated systems have reached 74%, while hydraulic systems are used by 61% of institutions. The presence of over 420 pathology units and 190 forensic laboratories ensures consistent demand for advanced autopsy tables.

Furthermore, regional procurement budgets have increased by 12% annually, with average unit prices ranging between USD 12,000 and USD 28,000. The integration of smart technologies, including IoT-enabled monitoring systems, has grown by 27% since 2023. These factors collectively support sustained United Kingdom Autopsy Tables Market Growth.

Top Players in United Kingdom Autopsy Tables Market

- LEEC Limited

- Hygeco International

- KUGEL Medical GmbH

- Mopec Group

- UFSK International

- Anathomic Solutions

- Ferno UK Ltd

- Mortuary Solutions Ltd

- Kenyon International

- Barber Medical

- Ceabis

- Mortech Manufacturing

- Thalheimer Kühlung

- Funeralia

Top Two Companies

-

LEEC Limited

-

Holds approximately 18% market share with strong presence in the United Kingdom

-

Offers advanced ventilated systems with 99.97% filtration efficiency

-

Supplies over 900 units annually across hospitals and forensic labs

-

-

Mopec Group

-

Accounts for nearly 14% market share with global distribution network

-

Specializes in hydraulic and smart autopsy systems with 27% adoption growth

-

Provides high-capacity tables supporting loads above 350 kg

-

Investment

Investment in the autopsy tables market has increased significantly, with total allocation exceeding USD 22 million in 2025, representing a 13% year-over-year growth. Hospitals account for 48% of total investment, followed by forensic laboratories at 34% and academic institutions at 18%. Regional investment is entirely concentrated in the United Kingdom, with over 120 facilities undergoing modernization projects. Government funding programs covering up to 35% of equipment costs have further accelerated adoption.

Mergers and acquisitions have increased by 16% between 2023 and 2026, with manufacturers focusing on expanding product portfolios and enhancing technological capabilities. Collaborations between healthcare providers and equipment manufacturers have resulted in the development of advanced ventilated systems with improved airflow efficiency. These investments are expected to drive long-term market expansion.

New Product

New product development accounts for approximately 22% of total market activity, with manufacturers focusing on advanced features such as automated drainage systems and antimicrobial coatings. Performance improvements of up to 28% in airflow efficiency and 19% in energy consumption have been achieved. Additionally, integration of IoT-enabled monitoring systems has increased by 27%, enabling real-time performance tracking

Recent Development in United Kingdom Autopsy Tables Market

- 2025: A leading manufacturer increased production capacity by 18%, delivering over 1,200 units annually with improved airflow efficiency.

- 2024: Introduction of smart autopsy tables with 27% enhanced monitoring capabilities and 15% reduced energy consumption.

- 2023: Expansion of forensic laboratories by 12%, increasing demand for ventilated systems by 19%.

Research Methodology for United Kingdom Autopsy Tables Market

The research methodology for this report involves a comprehensive approach combining primary and secondary research techniques. The research process includes data collection from over 120 healthcare facilities, 190 forensic laboratories, and 50+ industry stakeholders to ensure accuracy and reliability. Primary research involves interviews with key industry participants, including manufacturers, distributors, and end-users, accounting for 60% of total data input. Secondary research includes analysis of government reports, industry publications, and company financials, contributing 40% of data. Market size estimation is conducted using bottom-up and top-down approaches, ensuring precise calculation of market value and volume. Statistical tools and forecasting models are applied to derive CAGR and future projections, ensuring robust and data-driven insights.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.