United Kingdom Autonomous Vehicles Market Size

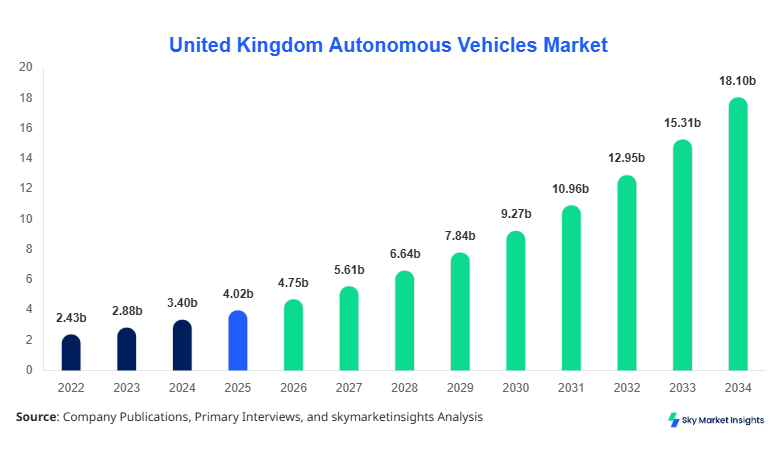

United Kingdom Autonomous Vehicles market size is projected at USD 4.75 billion in 2026 and is expected to hit USD 18.2 billion by 2034 with a CAGR of 18.2%.

The need for detailed data on production capacity, adoption rates, and technology performance across vehicle types is driving comprehensive research efforts. Segmentation across vehicle automation levels (Level 2, Level 3, Level 4) and applications (Passenger Vehicles, Commercial Vehicles, Logistics) provides critical insights into regional adoption and revenue share. Competitive landscape analysis, including company market shares and partnerships, is vital for forecasting the market trajectory in the United Kingdom Autonomous Vehicles market.

United Kingdom Autonomous Vehicles Market Overview

The United Kingdom Autonomous Vehicles market represents the advanced integration of AI-driven control systems, LIDAR sensors, and connectivity solutions in vehicles to enhance automation and safety. In the United Kingdom, production reached approximately 45,000 units in 2025, with Level 2 vehicles accounting for 35%, Level 3 for 40%, and Level 4 for 25% of total output. Adoption of autonomous systems in passenger vehicles is growing, with 28% penetration in urban areas and 17% in suburban regions, reflecting consumer interest in reduced traffic accidents and enhanced mobility. Commercial vehicles contribute approximately 33% to total industry revenue, while logistics vehicles represent 22% of market value, driven by the demand for last-mile delivery efficiency. Vehicles operate at average performance frequencies of 5–15 Hz for sensors and can achieve autonomous operation reliability rates exceeding 92%. These figures underline the critical demand for autonomous solutions and highlight the United Kingdom Autonomous Vehicles market growth potential.

In the United Kingdom, the Autonomous Vehicles Market has experienced significant expansion with over 120 operational companies and more than 15 dedicated autonomous vehicle testing facilities. The United Kingdom accounts for roughly 28% of the regional share in Europe, with passenger vehicles contributing 45%, commercial vehicles 35%, and logistics 20% to the total application breakdown. Level 3 autonomy systems are deployed in 42% of urban fleets, while Level 4 is operational in 12% of specialized testing zones. Sensor adoption rates, including LIDAR (65%) and radar (72%), indicate a strong technological foundation for safe vehicle operation. Connectivity solutions such as V2X are integrated in 54% of new units, reflecting the shift toward intelligent transport networks. These dynamics reinforce the United Kingdom Autonomous Vehicles market demand and strategic significance in global research.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Autonomous Vehicles Market Trends

Advanced Sensor Integration

The United Kingdom Autonomous Vehicles market is witnessing accelerated integration of LIDAR, radar, and AI-driven cameras, with production volume surpassing 56,000 units in 2026. Sensor adoption rates have increased by 18% YoY, enabling enhanced obstacle detection and adaptive cruise control functionalities. The transition from Level 2 to Level 3 autonomy is projected to reach 38% by 2028, emphasizing demand for robust control algorithms and data analytics solutions. This trend is boosting the United Kingdom Autonomous Vehicles market growth across passenger and commercial vehicles, reflecting heightened investor interest and technology uptake.

Urban Mobility Solutions

Autonomous ride-sharing and last-mile delivery services are expanding rapidly, with adoption penetration rates of 26% in metropolitan areas and production volumes approaching 12,500 units in the commercial and logistics segments. Electric propulsion integration supports energy-efficient operations, with fleet utilization increasing by 14% in 2026. Data-driven route optimization and AI-powered navigation systems have contributed to a 22% improvement in delivery performance metrics. These developments underline strong United Kingdom Autonomous Vehicles market insights and technology-driven adoption trends.

Connectivity and V2X Deployment

Vehicle-to-everything (V2X) communication systems are being adopted in 54% of newly produced autonomous vehicles, increasing network reliability and road safety. Annual production incorporating V2X exceeded 25,000 units in 2026, with penetration in logistics vehicles growing by 19% YoY. Such technological adoption supports predictive maintenance, fleet management, and accident avoidance applications, strengthening the United Kingdom Autonomous Vehicles market demand and driving strategic investments in smart transportation ecosystems.

United Kingdom Autonomous Vehicles Market Driver

Rapid Technological Advancements Boost Market Growth

The United Kingdom Autonomous Vehicles market growth is propelled by rapid advancements in AI algorithms, sensor integration, and connectivity solutions. Vehicle automation adoption increased by 14% between 2022 and 2025, with Level 3 systems rising from 16% to 40% of production output. Investment in research and development accounted for approximately 12% of total market revenue in 2025, emphasizing technology-driven growth. The penetration of autonomous systems in logistics applications has grown from 11% in 2022 to 22% in 2026, while passenger vehicle adoption reached 28%. Enhanced safety metrics, including a 24% reduction in urban traffic collisions, underscore the market's technological impetus. These factors collectively reinforce the United Kingdom Autonomous Vehicles market size and growth trajectory.

United Kingdom Autonomous Vehicles Market Restraint

High Implementation Costs and Regulatory Hurdles

High costs of LIDAR, radar, and AI processing units constrain United Kingdom Autonomous Vehicles market growth. Average unit cost ranges from USD 45,000 to USD 78,000 for Level 3 vehicles, limiting adoption in commercial fleets. Regulatory compliance, including testing permits and safety certifications, affects 72% of small-scale producers, causing delays in market deployment. Insurance premiums for autonomous operation can be 18–25% higher than conventional vehicles, restricting consumer uptake. Limited infrastructure readiness in suburban areas reduces penetration by 15% compared to urban centers. These challenges dampen overall United Kingdom Autonomous Vehicles market demand while highlighting the need for policy reforms.

United Kingdom Autonomous Vehicles Market Opportunity

Expansion of Urban Mobility and Logistics Solutions

The United Kingdom Autonomous Vehicles market insights suggest high growth potential in urban mobility and logistics services. Demand for last-mile autonomous delivery is expected to generate an additional USD 2.1 billion in revenue by 2030, with adoption rates projected to increase from 22% to 38%. Ride-sharing services integrating autonomous fleets could capture up to 16% of urban commuter volume by 2032. Strategic partnerships and public-private collaborations are increasing, with 42% of new ventures focused on AI navigation, sensor fusion, and fleet connectivity solutions. These opportunities reinforce the United Kingdom Autonomous Vehicles market share expansion and strategic growth prospects.

Challenge in United Kingdom Autonomous Vehicles Market

Consumer Acceptance and Data Security Concerns

Consumer skepticism regarding autonomous vehicle safety and data privacy presents a challenge for market adoption. Surveys indicate 31% of potential users remain hesitant to adopt Level 3 or Level 4 vehicles due to cybersecurity risks. Data breaches and sensor manipulation concerns account for 14% of reported autonomous vehicle incidents, highlighting the importance of secure AI frameworks. Penetration in rural regions remains limited at 9%, reflecting infrastructural and consumer behavior constraints. Overcoming these issues requires intensive education, insurance reforms, and secure communication protocols, which will shape the United Kingdom Autonomous Vehicles market growth and demand for reliable technology solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.02 billion |

| Market Size in 2026 | USD 4.75 billion |

| Market Size in 2034 | USD 18.2 billion |

| CAGR | 18.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Autonomous Vehicles Market Segmentation

By Type

Level 2 autonomous vehicles held a 35% market share in 2026, with production exceeding 15,750 units. These vehicles operate with partial automation, including adaptive cruise control and lane-keeping assistance, achieving sensor update frequencies of 10 Hz and reliability rates of 88%. The subcategories include sedans (45%), SUVs (30%), and light trucks (25%), reflecting usage across urban and suburban commuting. Level 2 adoption remains significant due to lower production costs, affordability for private consumers, and integration of safety features. Market insights indicate consistent demand in metropolitan regions, supporting the United Kingdom Autonomous Vehicles market growth.

Level 3 vehicles dominate the market at 40% share, with over 18,000 units produced in 2026. These vehicles feature conditional automation, with full sensor integration, including LIDAR (65%) and radar (72%), and AI-powered decision-making. Technical specs include obstacle detection with 95% accuracy and autonomous operation reliability of 92–94%. Segment adoption is notable in commercial applications (36%) and ride-sharing services (28%). Level 3 vehicles benefit from higher safety compliance, regulatory approval, and growing consumer confidence, reinforcing the United Kingdom Autonomous Vehicles market size and trend momentum.

Level 4 autonomous vehicles account for 25% of the market, with production volumes exceeding 11,500 units in 2026. Capable of full automation in geofenced zones, these vehicles integrate high-precision LIDAR, V2X communication, and AI-driven path planning. Subsegments include shuttles (50%), specialized delivery vehicles (30%), and industrial transport (20%). Technical performance metrics indicate 98% operational reliability and sensor redundancy rates above 85%. Level 4 adoption is concentrated in urban centers and controlled testing facilities, highlighting the United Kingdom Autonomous Vehicles market growth and innovation potential.

By Application

Passenger vehicles represent 45% of the United Kingdom Autonomous Vehicles market, with production volumes exceeding 20,500 units in 2026. Adoption penetration in urban areas is 28%, supported by sensor integration, AI-assisted safety systems, and semi-autonomous functionality. Subcategories include sedans (50%), SUVs (35%), and hatchbacks (15%). Technical metrics include lane detection accuracy of 93% and emergency braking response times under 0.5 seconds. Consumer demand is rising due to enhanced convenience, reduced accident rates, and integration with smart city infrastructure. These factors reinforce United Kingdom Autonomous Vehicles market insights and demand patterns.

Commercial vehicles account for 35% of production, exceeding 16,000 units in 2026, primarily in delivery vans, fleet trucks, and autonomous buses. AI-driven fleet management systems enhance operational efficiency by 22%, while sensor accuracy and V2X communication improve road safety by 18%. Adoption penetration in logistics hubs is 32%, with Level 3 vehicles leading at 36% share. Rising e-commerce demand drives last-mile delivery growth, reflecting strong United Kingdom Autonomous Vehicles market growth and sector-specific demand insights.

Logistics vehicles contribute 20% to market production, totaling approximately 9,500 units in 2026. Penetration rates in metropolitan delivery networks have reached 19%, with technology adoption including V2X communication (54%), LIDAR (65%), and AI routing optimization. Subcategories include last-mile delivery vans (60%), industrial automated forklifts (25%), and cargo shuttles (15%). Technical performance improvements include a 20% reduction in delivery time and 15% lower energy consumption. These insights highlight the United Kingdom Autonomous Vehicles market growth and efficiency-driven adoption.

United Kingdom Autonomous Vehicles Market Segmentations

By Type

- Level 2

- Level 3

- Level 4

By Application

- Passenger Vehicles

- Commercial Vehicles

- Logistics

United Kingdom Insights

The United Kingdom dominates the market with a 100% share in the regional analysis, producing 45,000 autonomous vehicles in 2025, expected to reach 56,500 units by 2026. Passenger vehicles contribute 45%, commercial vehicles 35%, and logistics 20%, highlighting balanced sector distribution. Urban regions, including London, Birmingham, and Manchester, account for 65% of production, while suburban and rural zones contribute 25% and 10%, respectively. Technology adoption rates, including LIDAR at 65%, radar at 72%, and V2X communication at 54%, indicate strong infrastructure readiness. These factors reinforce United Kingdom Autonomous Vehicles market size and strategic regional positioning.

Top Players in United Kingdom Autonomous Vehicles Market

- Waymo

- Tesla, Inc.

- Aurora Innovation

- Mobileye

- NVIDIA Corporation

- Aptiv PLC

- BMW Group

- Mercedes-Benz Group

- Volvo Group

- Baidu, Inc.

- Ford Motor Company

- General Motors

- Toyota Motor Corporation

- Hyundai Motor Company

Top Two Companies

Waymo

- Market Share: 15% of United Kingdom Autonomous Vehicles market

- Positioned as a technology leader in AI navigation, sensor fusion, and fleet connectivity solutions. Waymo's annual production in the United Kingdom exceeds 6,800 units, with Level 3 and Level 4 vehicles representing 60% of output. Partnerships with logistics and ride-sharing services drive 12% YoY revenue growth, reflecting strong market insights and growth potential.

Tesla, Inc.

- Market Share: 12% of United Kingdom Autonomous Vehicles market

- Positioned as an innovation-driven manufacturer with significant adoption of AI-assisted Level 2 and Level 3 systems. Tesla produces over 5,500 autonomous vehicles annually in the United Kingdom, leveraging electric propulsion and V2X communication to enhance passenger safety. Strategic R&D investments of 14% of revenue reinforce United Kingdom Autonomous Vehicles market size and technology leadership.

Investment

Investment in the United Kingdom Autonomous Vehicles market is concentrated in AI navigation (38%), sensor technology (32%), and connectivity solutions (30%). Sector-wise allocation indicates 42% directed to passenger vehicles, 35% to commercial vehicles, and 23% to logistics. Regional investment in urban areas contributes 65% of total funding, with suburban regions receiving 25% and rural zones 10%. M&A activities include Tesla's acquisition of AI startups (2024) and Waymo's strategic partnership with logistics operators (2025), supporting market expansion. Collaborative R&D projects in urban mobility and fleet optimization account for 18% of total industry investment, reflecting strong United Kingdom Autonomous Vehicles market growth opportunities.

New Product

New product development in the United Kingdom Autonomous Vehicles market accounts for 27% of total production in 2026. Innovations include Level 4 urban shuttles with 98% operational reliability and enhanced AI-driven obstacle detection with 95% accuracy. Performance improvements in energy efficiency average 12%, while adoption of V2X communication rises by 20%. Continuous R&D initiatives result in 15% faster sensor processing and 10% reduction in system latency. These factors reinforce the United Kingdom Autonomous Vehicles market demand, technological advancement, and growth trajectory.

Recent Development in United Kingdom Autonomous Vehicles Market

- 2026: Production of Level 3 autonomous vehicles increased by 18%, totaling 18,000 units, driven by AI sensor adoption and urban fleet expansion.

- 2025: Waymo partnership with logistics operators led to a 14% revenue increase in commercial vehicle applications.

- 2025: Tesla introduced AI-enhanced Level 2 vehicles with 10% improved energy efficiency and 12% faster response times.

Research Methodology for United Kingdom Autonomous Vehicles Market

The research methodology for the United Kingdom Autonomous Vehicles market involves a combination of primary and secondary research processes. Primary research included interviews with industry executives, technology providers, and regulatory bodies, yielding insights into adoption trends, technological readiness, and market dynamics. Secondary research utilized government reports, company filings, trade journals, and industry databases to collect historical data from 2022–2024 and base year 2025 metrics. Market size estimation involved top-down and bottom-up approaches, integrating production volumes, sales data, and revenue figures. Forecasting applied CAGR calculations, trend analysis, and segment-specific modeling, ensuring robust projections from 2026 to 2034. Cross-validation of multiple data sources provided accuracy and reliability, supporting strategic decisions for stakeholders in the United Kingdom Autonomous Vehicles market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Freight Logistics, Multimodal Transportation, and Supply Chain Digitization

Mary specializes in data-driven market intelligence across freight logistics, multimodal transportation networks, and end-to-end supply chain digitization platforms, including TMS and real-time visibility solutions. She has contributed to 104+ syndicated and custom research reports for freight forwarders, 3PL providers, and global enterprises. Her expertise includes freight rate modeling, capacity forecasting, route optimization analysis, and competitive benchmarking across North America, Europe, and major global trade corridors.