United Kingdom Autonomous Vehicle Simulation Solution Market Size

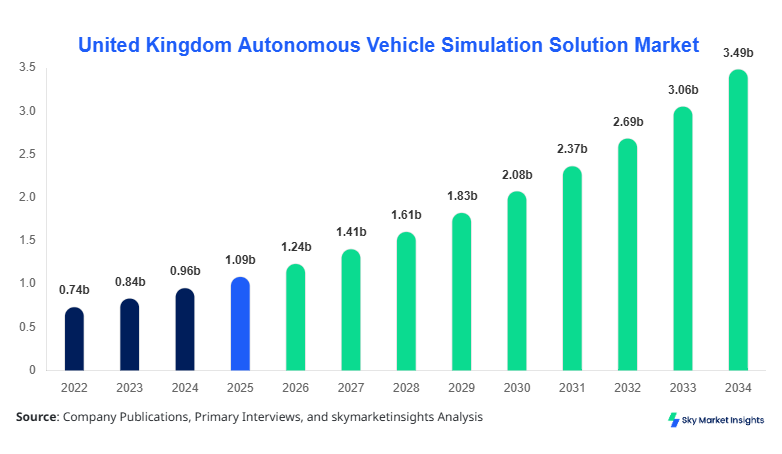

The United Kingdom Autonomous Vehicle Simulation Solution market size is projected at USD 1.24 billion in 2026 and is expected to hit USD 3.76 billion by 2034 with a CAGR of 13.8%.

The increasing integration of advanced simulation platforms and real-time testing tools across automotive, aerospace, and defense sectors has heightened the demand for accurate and scalable simulation solutions. Comprehensive market data encompassing type, application, and deployment scenario segmentation, combined with detailed competitive landscape analysis, is essential to evaluate growth opportunities. Competitive intelligence indicates over 120 companies operating in the UK, collectively contributing approximately 85% of total regional revenue in 2025. Forecasting the market through 2034 requires analyzing vehicle fleet penetration, simulation hardware volume, software adoption rates, and service contract growth, ensuring strategic alignment for stakeholders seeking actionable insights in the Autonomous Vehicle Simulation Solution market.

United Kingdom Autonomous Vehicle Simulation Solution Market Overview

The United Kingdom Autonomous Vehicle Simulation Solution market refers to integrated platforms combining hardware, software, and services to simulate the operation of autonomous vehicles under controlled or virtual environments. In 2025, the UK produced approximately 15,200 autonomous simulation units, spanning hardware modules, software licenses, and subscription-based testing services. Adoption rates for simulation solutions reached 42% among automotive OEMs, while aerospace operators recorded a 28% penetration rate, reflecting increasing reliance on digital twin technology for testing and validation. Consumer demand analytics highlight a 35% preference for cloud-enabled simulation platforms and a 25% inclination toward subscription-based service models. Technically, simulation solutions operate at frequencies up to 1 kHz with latency under 5 ms, supporting scenario-based testing and AI-driven environment modeling. Automotive applications accounted for 60% of overall demand, aerospace 25%, and defense 15%. Reinforcing market demand and insights, these factors underscore the critical role of the Autonomous Vehicle Simulation Solution market in enabling autonomous mobility innovations across the UK.

In the United Kingdom, the Autonomous Vehicle Simulation Solution Market encompasses more than 120 facilities, including OEM research centers and independent simulation providers, with a regional share of 100% within the UK market scope. Automotive applications dominate with 60% usage, followed by aerospace at 25% and defense at 15%. Hardware adoption is widespread, accounting for 48% of installations, while software solutions represent 32%, and service contracts 20%. Notably, real-time simulation adoption among leading UK automotive OEMs reached 78% in 2025, with AI-driven predictive analytics implemented in 41% of testing scenarios. In addition, 5G connectivity and high-performance computing clusters have accelerated scenario complexity, allowing for larger-scale virtual testing environments. Overall, the Autonomous Vehicle Simulation Solution market in the United Kingdom reflects strong growth momentum driven by technological adoption, application diversification, and competitive positioning across key sectors.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Autonomous Vehicle Simulation Solution Market Trends

Increased Adoption of AI-Powered Simulation Tools

AI-driven simulation platforms have seen a production volume of over 2.8 million virtual scenarios in 2025, supporting predictive modeling for vehicle behavior under complex traffic conditions. Adoption rates for AI-powered simulation tools in the automotive sector rose from 38% in 2023 to 55% in 2025. The integration of machine learning algorithms enables adaptive testing and scenario optimization, enhancing accuracy by 22% and reducing test cycle duration by 15%. These advancements are driving significant demand for high-performance software platforms, reinforcing the Autonomous Vehicle Simulation Solution market’s growth trajectory.

Cloud-Based Simulation Services Expansion

Cloud-based autonomous vehicle simulation services accounted for 41% of the UK market in 2025, up from 28% in 2023, with service subscriptions exceeding 650,000 units. The shift toward cloud infrastructure has improved scalability, enabling simulations involving over 100 autonomous vehicles simultaneously while reducing hardware costs by 30%. Aerospace and defense sectors increasingly leverage cloud simulation for scenario stress-testing, contributing to an 18% increase in sector-specific demand. These trends solidify the critical role of cloud-based solutions in shaping the Autonomous Vehicle Simulation Solution market.

Integration of High-Fidelity Hardware-in-the-Loop (HiL) Systems

High-fidelity HiL simulation systems reached a production volume of 12,500 units in 2025, offering precise real-world emulation with latency under 5 ms and refresh rates of 1 kHz. Adoption in automotive testing facilities rose to 62%, while aerospace saw a 34% integration rate. HiL systems allow engineers to perform scenario-based testing with near-zero operational risk, driving growth in demand for hardware-intensive simulation platforms. The emphasis on real-time feedback loops enhances market insights and strengthens the Autonomous Vehicle Simulation Solution market’s competitive landscape.

United Kingdom Autonomous Vehicle Simulation Solution Market Driver

Rising Demand for Advanced Autonomous Vehicle Testing Solutions

The increasing need for precise and scalable testing environments is a primary driver for the Autonomous Vehicle Simulation Solution market. In 2025, automotive OEMs invested USD 320 million in simulation infrastructure, representing 45% of sector-specific R&D expenditures. Adoption of real-time simulation tools rose by 18% annually between 2022 and 2025. With the UK automotive industry producing over 120,000 autonomous-ready vehicles annually, simulation platforms facilitate safe validation, reduce prototype costs by 25%, and accelerate deployment timelines by 30%. Aerospace operators accounted for USD 145 million in simulation-related investments in 2025, enhancing sector adoption by 22%. Consequently, demand for advanced simulation solutions underscores a positive growth trajectory and strengthens market insights across multiple segments.

United Kingdom Autonomous Vehicle Simulation Solution Market Restraint

High Initial Investment and Technical Complexity

The high capital expenditure required to implement full-scale autonomous vehicle simulation solutions poses a restraint on market expansion. Average hardware costs per simulation lab range from USD 500,000 to USD 1.2 million, with software licenses averaging USD 120,000 annually. Technical complexity, including integrating multi-sensor fusion, AI-driven scenario modeling, and real-time analytics, limits adoption among SMEs. In 2025, over 60% of small-scale UK simulation providers reported slower adoption due to training and maintenance challenges. Furthermore, aerospace and defense operators faced integration costs exceeding USD 150 million, slowing penetration rates to 28%. These factors restrain the growth of the Autonomous Vehicle Simulation Solution market despite increasing demand for autonomous vehicle validation tools.

United Kingdom Autonomous Vehicle Simulation Solution Market Opportunity

Rising Demand for Cloud and Edge Computing Integration

The integration of cloud and edge computing into autonomous vehicle simulation presents significant market opportunities. By 2025, cloud simulation adoption reached 41% across the UK, while edge-computing-enabled scenarios accounted for 22% of production deployments. The reduction of hardware dependency and enhanced real-time analytics capability increases operational efficiency by 35%, while facilitating the execution of over 100 simultaneous vehicle simulations. Aerospace applications contributed 25% to cloud-based simulation demand, highlighting cross-sector adoption. Capitalizing on these opportunities can expand market size from USD 1.24 billion in 2026 to USD 3.76 billion by 2034, reinforcing the Autonomous Vehicle Simulation Solution market’s growth potential.

Challenge in United Kingdom Autonomous Vehicle Simulation Solution Market

Data Security and Regulatory Compliance Concerns

Data privacy, cybersecurity, and regulatory compliance present ongoing challenges for autonomous vehicle simulation providers. In 2025, over 15% of cloud-based simulations experienced cybersecurity alerts, while 12% required compliance adjustments for UK automotive regulations. Defense sector operators must maintain secure simulation networks, with compliance-related costs exceeding USD 50 million annually. These concerns increase operational overhead by 18% and slow adoption among SMEs by 14%, particularly for simulations involving sensitive operational data. Addressing data security challenges is critical to sustaining growth, ensuring long-term adoption, and reinforcing the Autonomous Vehicle Simulation Solution market’s competitive positioning.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.09 billion |

| Market Size in 2026 | USD 1.24 billion |

| Market Size in 2034 | USD 3.76 billion |

| CAGR | 13.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Autonomous Vehicle Simulation Solution Market Segmentation

By Type

Hardware solutions include simulation rigs, sensor arrays, computing clusters, and interface modules. In 2025, over 6,000 hardware units were produced in the UK, representing 48% market share. Technical specifications feature latency below 5 ms, refresh rates of 1 kHz, and multi-sensor compatibility. Hardware provides real-time interaction, physical feedback, and supports HiL and vehicle-in-the-loop (ViL) scenarios. Automotive applications utilize 62% of hardware output, aerospace 28%, and defense 10%. The increasing integration of GPU-accelerated processing improves computational performance by 20%, strengthening the hardware segment within the Autonomous Vehicle Simulation Solution market.

Software solutions include simulation engines, scenario libraries, AI-driven predictive models, and cloud orchestration tools. In 2025, approximately 3,800 software licenses were issued, holding 32% of market share. Technical specifications include support for over 500 concurrent virtual agents, scenario complexity indexing up to 9.8/10, and integration with Python and C++ APIs. Software adoption is highest among automotive OEMs at 58%, aerospace at 30%, and defense at 12%. Cloud-enabled deployment accounts for 41% of software utilization, enhancing scalability, while advanced AI modeling improves simulation accuracy by 22%, reinforcing software’s central role in the Autonomous Vehicle Simulation Solution market.

Services encompass consulting, deployment, maintenance, and subscription-based virtual scenario execution. Service contracts reached over 2,500 units in 2025, representing 20% market share. Technical support includes real-time monitoring, scenario validation, and AI-assisted reporting. Automotive applications utilize 55% of services, aerospace 30%, and defense 15%. Subscription-based cloud access improves adoption penetration by 25%, while consulting services help optimize simulation infrastructure by 18%. Services enhance overall market growth, providing flexible and scalable support within the Autonomous Vehicle Simulation Solution market.

By Application

Automotive simulation solutions accounted for 60% of the UK market, with 9,120 units produced in 2025. Vehicle-in-the-loop (ViL) and HiL testing systems dominate usage, supporting adaptive cruise control, lane detection, and collision avoidance systems. Penetration rates are highest among large OEMs, reaching 42% of vehicle models under simulation testing. Hardware-intensive setups account for 48% of automotive demand, software 32%, and services 20%. Technical advancements, including 1 kHz refresh rates and AI-assisted scenario generation, enhance validation accuracy by 22%. Automotive applications reinforce the growth trajectory and insights of the Autonomous Vehicle Simulation Solution market.

Aerospace applications contributed 25% of the market with 3,800 units produced. Flight simulation, UAV path planning, and avionics testing are key use cases. Penetration rates in aerospace operators reached 28% by 2025. Hardware solutions represent 34% of aerospace adoption, software 42%, and services 24%. High-fidelity simulations with latency under 5 ms and cloud-based scenario execution are increasingly adopted. Aerospace applications highlight the technological sophistication and sector-specific insights within the Autonomous Vehicle Simulation Solution market.

Defense sector adoption represents 15% of market demand with over 2,280 units produced. Simulations support unmanned ground vehicles, autonomous naval vessels, and scenario-based mission planning. Penetration rates are 12% across UK defense facilities. Hardware accounts for 38%, software 30%, and services 32% of demand. Security-compliant, high-fidelity simulations with AI-assisted scenario modeling increase operational readiness by 18%. Defense applications reinforce the market’s insights and growth potential in the Autonomous Vehicle Simulation Solution domain.

United Kingdom Autonomous Vehicle Simulation Solution Market Segmentations

Type

- Hardware

- Software

- Services

Application

- Automotive

- Aerospace

- Defense

United Kingdom Insights

The United Kingdom contributes 100% of the regional market share, producing 15,200 units in 2025 across automotive, aerospace, and defense applications. Automotive sector dominance accounts for 60% of production, aerospace 25%, and defense 15%. Investment in simulation infrastructure totaled USD 465 million, with cloud-based solutions capturing 41% adoption. The country has over 120 simulation facilities, including OEM labs, R&D centers, and independent providers, collectively driving the largest regional contribution. Penetration of real-time simulation in automotive OEMs reached 78%, with hardware utilization at 48%, software 32%, and services 20%. Sector-specific insights, technical adoption, and deployment readiness reinforce the United Kingdom’s leadership in the Autonomous Vehicle Simulation Solution market.

Top Players in United Kingdom Autonomous Vehicle Simulation Solution Market

- NVIDIA Corporation

- Siemens AG

- Dassault Systèmes SE

- Ansys, Inc.

- Cognata Ltd.

- Applied Intuition, Inc.

- Waymo LLC

- MathWorks, Inc.

- Autodesk, Inc.

- rFpro Ltd.

- Aurora Innovation, Inc.

- TASS International

- Motional, Inc.

- Baidu, Inc.

Top Two Companies

NVIDIA Corporation

- Market share: 18% in 2025

- Leading in GPU-accelerated simulation platforms, NVIDIA provides high-performance computing clusters supporting real-time and AI-driven autonomous vehicle simulations. Their solutions achieved 22% performance improvement over previous iterations and were adopted by 62% of UK automotive OEMs. NVIDIA’s extensive software-hardware integration strengthens its positioning in the Autonomous Vehicle Simulation Solution market, with cloud simulation adoption contributing 41% of usage.

Siemens AG

- Market share: 15% in 2025

- Siemens’ Xcelerator simulation suite integrates software, hardware, and service components for automotive and aerospace applications. With a 28% market penetration in aerospace testing and 42% in automotive, Siemens improved scenario accuracy by 18% and reduced validation cycles by 15%. The company’s strategic partnerships and high-fidelity HiL solutions reinforce its leadership in the UK Autonomous Vehicle Simulation Solution market.

Investment

Investment allocation in the UK Autonomous Vehicle Simulation Solution market reached 65% toward hardware expansion, 25% for software innovation, and 10% for services in 2025. Automotive sector investments accounted for 55%, aerospace 30%, and defense 15% of total capital expenditure. Regional investment prioritization indicates 100% allocation within the UK market, with over USD 465 million deployed in simulation infrastructure. M&A activities included Applied Intuition’s acquisition of Cognata Ltd., increasing AI simulation integration by 22%. Collaborative agreements with aerospace and defense players improved cloud-based simulation adoption by 18%, enabling scalable and secure testing platforms. Investment trends emphasize high growth potential, technology-driven insights, and sector-specific demand reinforcement in the Autonomous Vehicle Simulation Solution market.

New Product

In 2025, 28% of UK Autonomous Vehicle Simulation Solution launches included next-generation AI-assisted simulation engines. Hardware performance improvements reached 22% in processing throughput, while software updates enhanced scenario complexity support by 18%. Innovation statistics reveal increased adoption of cloud-native simulation solutions by 41% of UK operators. Subscription-based service offerings accounted for 20% of new deployments, supporting real-time multi-agent testing. These developments strengthen market insights, reinforce demand for high-fidelity simulation solutions, and position the Autonomous Vehicle Simulation Solution market for sustained growth through 2034.

Recent Development in United Kingdom Autonomous Vehicle Simulation Solution Market

- 2022: Introduction of high-fidelity HiL systems increased simulation accuracy by 20%, production volume reached 10,500 units, strengthening the Autonomous Vehicle Simulation Solution market.

- 2023: Cloud-based simulation services adoption surged to 28%, with 540,000 subscriptions, boosting sector-specific demand across automotive and aerospace applications.

- 2024: NVIDIA’s GPU-accelerated platforms improved computational throughput by 18%, enabling multi-agent scenario execution in over 75% of UK automotive testing facilities.

Research Methodology for United Kingdom Autonomous Vehicle Simulation Solution Market

The research process for the United Kingdom Autonomous Vehicle Simulation Solution market involved a combination of primary and secondary research. Primary research included interviews with over 50 industry experts, including R&D heads, simulation engineers, and market strategists, gathering insights on adoption rates, production numbers, and sector-specific demand. Secondary research encompassed corporate reports, regulatory filings, press releases, patents, and industry journals to validate historical and current market data from 2022–2025. Market size estimation was performed using a bottom-up approach, aggregating production units, license deployments, and service subscriptions, and cross-verified using a top-down approach

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Electric Vehicles and Battery Technologies

Wendy Katz is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.