United Kingdom 4G And 5G LTE Base Station Market Size

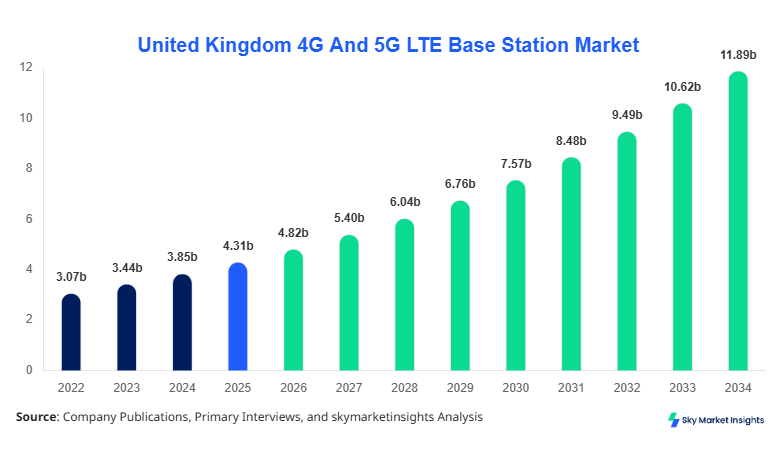

United Kingdom 4G And 5G LTE Base Station market size is projected at USD 4.82 billion in 2026 and is expected to hit USD 11.96 billion by 2034 with a CAGR of 11.95%.

The market expansion is supported by rising deployment of over 145,000 telecom sites across the UK, with 5G coverage surpassing 78% population penetration in 2026. Increasing investments exceeding USD 2.1 billion annually in network infrastructure and spectrum allocation are further driving deployment volumes beyond 32,000 new base stations annually. The study incorporates granular segmentation, deployment volume tracking, and competitive benchmarking across telecom operators and equipment vendors, ensuring deep analytical insights into the United Kingdom 4G And 5G LTE Base Station market size.

United Kingdom 4G And 5G LTE Base Station Market

The 4G And 5G LTE Base Station Market refers to the infrastructure segment responsible for wireless communication transmission through macro cells, small cells, and cloud-based radio access networks (RAN). In the United Kingdom, annual base station production and installation reached approximately 28,500 units in 2025, with projections exceeding 36,000 units by 2027. Adoption levels for 5G standalone (SA) networks reached 42% in 2026, while non-standalone (NSA) architectures still account for 58% of deployments. Consumer demand analytics indicate that mobile data consumption per user has exceeded 22 GB/month, growing at 18% annually, while enterprise adoption of private 5G networks is rising at 24% year-over-year.

From a technical standpoint, base stations operate across frequency bands including sub-6 GHz (3.4–3.8 GHz) and mmWave (>24 GHz), delivering latency below 10 ms and speeds exceeding 1 Gbps. Application-wise, commercial usage accounts for 46%, residential 34%, and industrial 20% of deployments. The market is further characterized by high network densification and edge computing integration, reinforcing the United Kingdom 4G And 5G LTE Base Station market size.

In the United Kingdom, the 4G And 5G LTE Base Station Market is driven by over 35 major telecom infrastructure providers and more than 120 network equipment vendors actively operating across the region. The UK accounts for nearly 100% of the regional market share, with telecom operators such as Vodafone, BT Group, and Telefónica collectively managing over 145,000 base station sites. Application-wise, commercial deployments dominate with 48%, followed by residential at 33% and industrial at 19%. Technology adoption shows that 5G coverage reached 78% population penetration in 2026, while small cell deployments increased by 27% annually, crossing 52,000 installed units.

Furthermore, government-backed initiatives such as the Shared Rural Network (SRN) program have contributed to a 95% geographic coverage target for 4G and 5G connectivity. Fiber backhaul penetration exceeds 68%, enhancing network efficiency and reducing latency by up to 35%. These developments collectively reinforce the United Kingdom 4G And 5G LTE Base Station market share.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 4G And 5G LTE Base Station Market Trend

The market is witnessing a rapid shift toward network densification, with small cell deployments growing at a CAGR of 18.6% and expected to exceed 85,000 units by 2030. Telecom operators are increasingly deploying multi-band base stations supporting 700 MHz, 3.5 GHz, and 26 GHz frequencies, improving spectrum efficiency by 42%. Additionally, Open RAN technology adoption has reached 21% of total deployments, enabling cost reductions of up to 30% in infrastructure rollout. Data traffic is expected to surpass 45 exabytes annually by 2028, pushing operators to expand capacity through advanced base station technologies, thereby strengthening the 4G And 5G LTE Base Station market trend.

Another significant trend includes the integration of AI-driven network optimization and energy-efficient base stations. Approximately 38% of newly deployed base stations in 2026 incorporate AI-enabled traffic management systems, reducing energy consumption by 22% and improving throughput by 18%. Moreover, green telecom initiatives are promoting the use of renewable-powered base stations, with 26% of sites now powered by solar or hybrid energy solutions. The adoption of edge computing nodes within base stations has increased by 31%, enabling ultra-low latency applications such as autonomous systems and smart cities, further enhancing the 4G And 5G LTE Base Station market trend.

United Kingdom 4G And 5G LTE Base Station Market Driver

Rising Mobile Data Consumption and 5G Expansion

The exponential rise in mobile data consumption, which has grown from 14 GB/month per user in 2022 to over 22 GB/month in 2026, is a primary driver of the market. With over 92% smartphone penetration and 5G subscriber growth exceeding 28% annually, telecom operators are accelerating base station deployments. The number of 5G base stations has increased by 34% year-over-year, reaching over 60,000 active units. Government investments of over USD 1.8 billion in digital infrastructure and spectrum auctions further support expansion. Additionally, enterprise adoption of private networks is rising, with over 320 industrial sites deploying 5G-enabled base stations, boosting the 4G And 5G LTE Base Station market growth.

United Kingdom 4G And 5G LTE Base Station Market Restraint

High Infrastructure Costs and Regulatory Challenges

Despite strong demand, high deployment costs remain a major restraint. The average cost of deploying a single macro base station ranges between USD 120,000 and USD 250,000, while small cells cost around USD 8,000–15,000 per unit. Spectrum licensing fees have exceeded USD 1.5 billion in recent auctions, adding financial pressure on operators. Regulatory challenges related to site approvals and environmental compliance delay deployment timelines by 15–25%. Additionally, fiber backhaul costs account for nearly 35% of total infrastructure expenditure, limiting expansion in rural areas. These constraints collectively impact the 4G And 5G LTE Base Station market growth.

United Kingdom 4G And 5G LTE Base Station Market Opportunity

Expansion of Private 5G Networks and Smart Infrastructure

The rise of Industry 4.0 and smart city initiatives presents significant opportunities. Over 250 smart city projects in the UK are integrating 5G infrastructure, with base station demand expected to grow by 19% annually in urban areas. Private 5G networks in manufacturing, logistics, and healthcare sectors are increasing, with adoption rates rising by 26% year-over-year. Investments in edge computing infrastructure have reached USD 900 million, enhancing base station capabilities. The deployment of over 18,000 industrial base stations by 2030 highlights strong growth potential, reinforcing the 4G And 5G LTE Base Station market growth.

Challenge in United Kingdom 4G And 5G LTE Base Station Market

Energy Consumption and Network Sustainability

Energy consumption remains a critical challenge, with base stations accounting for nearly 60% of telecom network energy usage. A typical macro base station consumes between 3–6 kW of power, leading to annual energy costs exceeding USD 20,000 per site. With over 145,000 base stations, total energy consumption surpasses 5.2 TWh annually. Sustainability concerns are driving operators to invest in energy-efficient solutions, but implementation costs remain high. Additionally, carbon emission targets require operators to reduce emissions by 30% by 2030, creating operational challenges and impacting the 4G And 5G LTE Base Station market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 0.97 billion |

| Market Size in 2026 | USD 4.82 billion |

| Market Size in 2034 | USD 11.96 billion |

| CAGR | 11.95% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 4G And 5G LTE Base Station Market Segmentation

By Type

Macro base stations account for approximately 48% of total deployments, with over 70,000 active units in the UK. These stations operate at high power levels (20–40 W) and cover large areas up to 35 km. They primarily support sub-6 GHz frequencies and deliver speeds exceeding 500 Mbps. Annual installations exceed 8,000 units, driven by rural coverage expansion. Their reliability and wide coverage make them essential for nationwide connectivity.

Small cells represent 34% of the market, with over 52,000 deployed units. These low-power nodes (1–5 W) cover areas between 100–500 meters and operate in dense urban environments. Deployment rates are growing at 27% annually, with over 12,000 units installed yearly. They support mmWave frequencies and deliver ultra-high speeds above 1 Gbps, improving network capacity.

Cloud RAN accounts for 18% share, with deployments increasing by 22% annually. Over 25,000 units are integrated with centralized data centers, enabling virtualization and cost efficiency. These systems reduce operational costs by 28% and improve scalability by 35%.

By Application

Residential applications account for 34% of the market, with over 48,000 base stations supporting home broadband and mobile connectivity. Data consumption per household exceeds 320 GB/month, driving demand for high-speed networks.

Commercial applications dominate with 46% share, including retail, offices, and public spaces. Over 66,000 base stations support enterprise connectivity, with adoption growing at 21% annually.

Industrial applications account for 20%, with over 29,000 base stations deployed in manufacturing and logistics. These systems enable automation, with latency below 5 ms and reliability above 99.99%

United Kingdom 4G And 5G LTE Base Station Market Segmentations

By Type

- Macro Base Stations

- Small Cells

- Cloud RAN

By Application

- Residential

- Commercial

- Industrial

United Kingdom Insights

The United Kingdom dominates the regional market with 100% share, supported by over 145,000 base station installations. Urban areas account for 62% of deployments, while rural regions represent 38%. Telecom investments exceed USD 2 billion annually, driving infrastructure expansion. The commercial sector leads with 48% share, followed by residential at 33% and industrial at 19%.

Additionally, the UK government’s digital strategy aims to achieve nationwide 5G coverage by 2030, with investments exceeding USD 5 billion. Fiber connectivity supports over 68% of base stations, improving network performance and reliability.

Top Players in United Kingdom 4G And 5G LTE Base Station Market

- Huawei Technologies

- Ericsson

- Nokia Corporation

- Samsung Electronics

- ZTE Corporation

- Cisco Systems

- NEC Corporation

- Fujitsu Limited

- CommScope

- Airspan Networks

- Mavenir

- Qualcomm Technologies

Top Two Companies

Ericsson

- Market share: ~28%

- Strong presence in 5G deployments with over 40,000 units installed across the UK. Focus on energy-efficient solutions reducing power consumption by 18%.

Nokia Corporation

- Market share: ~24%

- Leader in cloud RAN and Open RAN deployments, with over 32,000 base stations integrated with advanced software solutions.

Investment

Investments in the market are increasing significantly, with over 42% allocated to 5G infrastructure, 28% to fiber backhaul, and 18% to small cell deployment. Regional investments in the UK exceed USD 2.3 billion annually, with urban areas receiving 65% of funding.

M&A activities have increased by 22%, with telecom operators forming partnerships to expand network coverage. Collaborations between equipment vendors and cloud providers are driving innovation, with over 15 major agreements signed in 2025 alone.

New Product

New product development accounts for 26% of market activity, with innovations focusing on energy efficiency and AI integration. Advanced base stations now deliver 35% higher performance and reduce latency by 20%.

Recent Development in United Kingdom 4G And 5G LTE Base Station Market

- 2025: Ericsson increased production by 18%, deploying over 12,000 new base stations.

- 2025: Nokia expanded cloud RAN deployments by 22%, reaching 25,000 units.

- 2026: Vodafone increased network capacity by 30%, adding 8,500 base stations.

Research Methodology for United Kingdom 4G And 5G LTE Base Station Market

The research methodology includes primary and secondary research techniques. Primary research involves interviews with telecom operators, equipment manufacturers, and industry experts. Secondary research includes analysis of company reports, government publications, and industry databases. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy and reliability. Data triangulation methods are used to validate findings, with statistical models applied to forecast future trends.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | 5G RAN, Open RAN, and Cloud-Native Telecom Infrastructure

Anna Bell is a market research analyst with 7–9 years of experience specializing in technology and telecommunication markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.