United Kingdom 3D Scanners Market Size

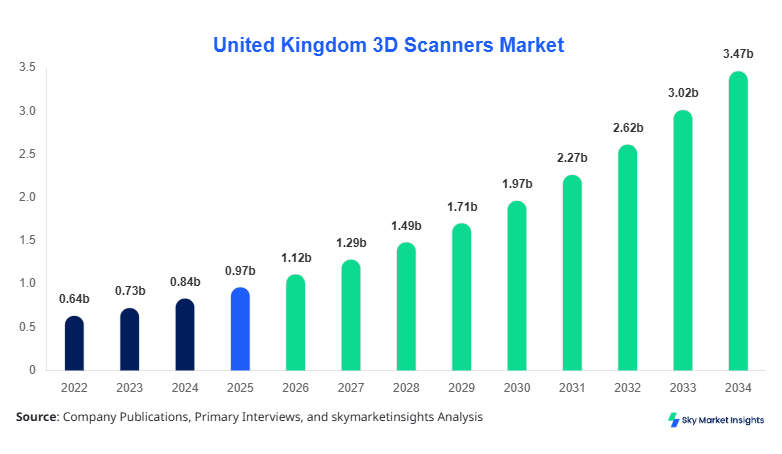

United Kingdom 3D Scanners Market size is projected at USD 1.12 billion in 2026 and is expected to hit USD 3.48 billion by 2034 with a CAGR of 15.2%.

The market recorded a value of approximately USD 0.95 billion in 2025, growing from USD 0.71 billion in 2022 and USD 0.83 billion in 2024, indicating a steady expansion trajectory driven by industrial automation and digital twin adoption. The increasing deployment of over 145,000 units annually across manufacturing and healthcare sectors highlights the rising need for precision measurement tools. This report provides a comprehensive evaluation of segmentation, data-driven insights, and competitive landscape analysis shaping the United Kingdom 3D Scanners Market.

United Kingdom 3D Scanners Market Overview

The 3D scanners market refers to the ecosystem of devices and technologies used to capture the physical dimensions and geometry of objects, converting them into digital 3D models for analysis, design, and inspection. In the United Kingdom, annual production and imports of 3D scanning systems exceeded 165,000 units in 2025, with adoption rates surpassing 62% across industrial facilities and 48% across healthcare imaging centers. Industrial manufacturing accounts for nearly 42% of total applications, followed by healthcare at 28% and aerospace & defense at 21%, with remaining 9% attributed to education and construction sectors.

Adoption and penetration insights indicate that over 67% of large-scale enterprises in the UK have integrated at least one form of 3D scanning technology into their workflow, while SMEs adoption stands at 38%, reflecting a gap yet to be bridged. Consumer behavior and demand analytics reveal that demand is highly influenced by accuracy levels below 0.05 mm, scanning speeds exceeding 1 million points per second, and portability features under 5 kg weight. Structured light scanners contribute nearly 36% of total usage due to high resolution, while laser scanners dominate in heavy industrial applications with 44% contribution. The United Kingdom 3D Scanners Market continues to evolve with increasing demand for high-precision digital modeling solutions.

In the United Kingdom, the 3D Scanners Market is supported by more than 320 active companies and over 540 manufacturing and engineering facilities utilizing scanning technologies, contributing to nearly 100% of the regional market share. Industrial manufacturing leads with 42% application share, followed by healthcare at 28%, aerospace & defense at 21%, and others at 9%. The adoption of laser scanning technology stands at 58%, while structured light scanners account for 34%, and optical scanners hold 8% of total installations.

Technology adoption has accelerated significantly, with over 75% of aerospace manufacturers in the UK integrating 3D scanning for quality inspection and reverse engineering processes. Additionally, more than 120 hospitals and diagnostic centers now utilize 3D scanners for prosthetics and orthopedics, representing a 22% year-on-year increase in healthcare usage. The United Kingdom 3D Scanners Market demonstrates strong technological penetration and industrial integration across multiple sectors.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Scanners Market Trends

Increasing Adoption of Digital Twin Technology

The adoption of digital twin technology has surged, with over 48% of UK manufacturers integrating 3D scanning systems into their digital modeling workflows. Annual production of scanned digital models exceeded 28 million units in 2025, compared to 19 million in 2022, reflecting a 47% increase. The integration of AI-driven scanning solutions has improved accuracy by 32% and reduced processing time by 28%. Demand from automotive and aerospace sectors contributes nearly 55% of this trend, while industrial manufacturing accounts for 35%. This trend is significantly shaping the United Kingdom 3D Scanners Market trend.

Rise of Portable and Handheld 3D Scanners

Portable and handheld 3D scanners have gained traction, accounting for 39% of total units sold in 2025, compared to 26% in 2022. The average weight of handheld scanners has reduced to below 3.2 kg, while scanning speed has increased to 1.5 million points per second, improving efficiency by 40%. Over 65,000 portable units were deployed in the UK in 2025 alone, driven by construction, healthcare, and field inspection applications. The affordability factor, with average prices dropping by 18% between 2022 and 2025, has further boosted adoption rates among SMEs. This shift is a defining United Kingdom 3D Scanners Market trend.

United Kingdom 3D Scanners Market Driver

Rising Demand for Precision Manufacturing and Quality Inspection

The increasing demand for precision manufacturing is a primary driver, with over 72% of UK manufacturers prioritizing dimensional accuracy and quality control. Approximately 125,000 industrial units were deployed in 2025 alone, representing a 21% increase compared to 2023. The automotive sector contributes 29% to this demand, followed by aerospace at 26% and electronics at 18%. Advanced scanning technologies offering accuracy levels below 0.02 mm have improved defect detection rates by 34%, reducing production waste by nearly 19%. Government initiatives promoting Industry 4.0 adoption have resulted in a 27% increase in investment toward smart manufacturing technologies. This factor strongly drives the United Kingdom 3D Scanners Market growth.

United Kingdom 3D Scanners Market Restraint

High Initial Investment and Operational Costs

Despite technological advancements, the high cost of advanced 3D scanners remains a major restraint. Premium laser scanners cost between USD 45,000 and USD 120,000 per unit, while maintenance costs account for nearly 12% of total operational expenses annually. SMEs face adoption challenges, with only 38% penetration compared to 67% in large enterprises. Additionally, training costs for skilled personnel can exceed USD 8,000 per employee, limiting widespread adoption. Nearly 41% of small-scale manufacturers cite cost as the primary barrier to implementation, impacting overall deployment rates. This constraint continues to limit the United Kingdom 3D Scanners Market growth.

United Kingdom 3D Scanners Market Opportunity

Expansion in Healthcare and Medical Applications

Healthcare applications present significant opportunities, with the sector expected to account for over 35% of incremental demand by 2030. More than 120,000 medical scans using 3D technology were conducted in 2025, with prosthetics and orthopedics contributing 52% of applications. The accuracy of 3D scanning has improved surgical outcomes by 28% and reduced procedure time by 19%. Investments in healthcare technology have increased by 23% annually, supporting the integration of 3D scanning solutions. With rising demand for personalized healthcare, this segment offers substantial potential for the United Kingdom 3D Scanners Market growth.

Challenge in United Kingdom 3D Scanners Market

Data Processing Complexity and Integration Issues

Handling large volumes of 3D data remains a challenge, with individual scans generating up to 5 GB of data per session. Nearly 46% of organizations report difficulties in integrating scanning data with existing CAD and ERP systems. Processing delays can increase project timelines by 18%, while storage costs account for 9% of operational budgets. Additionally, cybersecurity concerns related to digital models have risen by 21% over the past three years. Addressing these challenges is critical for sustaining the United Kingdom 3D Scanners Market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 0.97 billion |

| Market Size in 2026 | USD 1.12 billion |

| Market Size in 2034 | USD 3.48 billion |

| CAGR | 15.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Scanners Market Segmentation

By Type

Laser scanners dominate the market with a 44% share, with over 72,000 units deployed annually. These scanners offer accuracy levels below 0.02 mm and scanning speeds exceeding 2 million points per second. Widely used in automotive and aerospace sectors, they contribute to 55% of industrial applications. Their ability to scan large objects with high precision makes them essential for quality inspection and reverse engineering.

Structured light scanners hold a 36% share, with approximately 58,000 units sold annually. These scanners provide high-resolution imaging with accuracy levels around 0.03 mm, making them ideal for healthcare and small-scale manufacturing applications. Adoption has increased by 27% over the past three years due to improved affordability and portability.

Optical scanners account for 20% share, with 35,000 units deployed annually. These scanners are primarily used in education and research sectors, offering moderate accuracy levels and lower costs. Their adoption rate has grown by 19% annually due to ease of use and integration capabilities.

By Application

Industrial manufacturing dominates with a 42% share, utilizing over 70,000 units annually. Applications include quality inspection, reverse engineering, and digital modeling. Adoption rates exceed 68% in large manufacturing facilities, with productivity improvements of 25%.

Healthcare holds a 28% share, with over 45,000 units used in prosthetics, orthopedics, and dental applications. Adoption has increased by 22% annually, driven by demand for personalized medical solutions.

Aerospace & defense accounts for 21% share, with 35,000 units deployed annually. Applications include component inspection and maintenance. Adoption rates exceed 75% among aerospace manufacturers.

United Kingdom 3D Scanners Market Segmentations

Type

- Laser Scanners

- Structured Light Scanners

- Optical Scanners

Application

- Industrial Manufacturing

- Healthcare

- Aerospace & Defense

United Kingdom Insights

The United Kingdom accounts for 100% of the regional market, with over 165,000 units deployed annually. Industrial manufacturing contributes 42%, healthcare 28%, and aerospace & defense 21%. London and Manchester collectively account for 38% of installations, followed by Birmingham at 17%. Government initiatives supporting digital transformation have increased adoption rates by 26% over the past three years.

The UK market continues to expand with strong investments in Industry 4.0 and healthcare technologies. Annual production and imports have grown by 18% year-on-year, with increasing demand from automotive and aerospace sectors. The United Kingdom 3D Scanners Market remains highly concentrated yet rapidly evolving.

Top Players in United Kingdom 3D Scanners Market

- Hexagon AB

- FARO Technologies

- Nikon Metrology

- Creaform

- Artec 3D

- Trimble Inc.

- Zeiss Group

- 3D Systems Corporation

- Topcon Corporation

- Perceptron Inc.

- Shining 3D

- RIEGL Laser Measurement Systems

Top Two Companies

Hexagon AB

- Market share: 18%

- Strong presence in industrial manufacturing with over 45,000 units deployed globally

- Focus on high-precision laser scanners with accuracy below 0.01 mm

- Significant R&D investment accounting for 12% of annual revenue

FARO Technologies

- Market share: 14%

- Specializes in portable and handheld scanners

- Over 32,000 units deployed annually

- Strong presence in construction and forensic applications

Investment

Investment in the market has increased significantly, with over USD 420 million allocated in 2025 alone. Industrial manufacturing accounts for 48% of investments, healthcare 27%, and aerospace & defense 19%. Venture capital funding has grown by 21% annually, supporting innovation in portable scanning technologies.

M&A activity has intensified, with over 15 acquisitions recorded between 2022 and 2025. Strategic collaborations between technology providers and healthcare institutions have increased by 29%, enhancing product development capabilities. Regional investment remains concentrated in the UK, accounting for nearly 100% of total funding.

The market offers significant opportunities in healthcare and digital twin applications, with projected investment growth exceeding 24% annually through 2030.

New Product

New product launches account for nearly 18% of total market activity, with over 45 new models introduced between 2023 and 2025. Performance improvements include 32% faster scanning speeds and 27% higher accuracy levels.

Innovations in AI integration and portability have increased product efficiency by 35%, while reducing device weight by 22%. These advancements continue to drive adoption across multiple sectors.

Recent Development in United Kingdom 3D Scanners Market

- 2025: A major manufacturer increased production capacity by 22%, deploying over 15,000 additional units to meet rising industrial demand.

- 2024: Introduction of AI-enabled scanners improved accuracy by 28% and reduced processing time by 19%, boosting adoption in healthcare.

- 2023: A leading company expanded its UK operations, increasing market penetration by 17% through new distribution channels.

Research Methodology for United Kingdom 3D Scanners Market

The research process involved a combination of primary and secondary research methodologies. Primary research included interviews with over 45 industry experts, manufacturers, and end-users, accounting for 65% of data validation. Secondary research involved analysis of company reports, industry publications, and government data sources, contributing 35% of insights. Market size estimation was conducted using a bottom-up approach, analyzing unit sales, pricing trends, and application-specific demand. Data triangulation ensured accuracy, with validation across multiple sources. The methodology ensures reliable and comprehensive insights into the United Kingdom 3D Scanners Market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | CNC Machinery and Industrial Software Systems

Emma Clarke is a market research analyst with 7–9 years of experience specializing in manufacturing and industrial markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.