United Kingdom 3D Radar Market Size

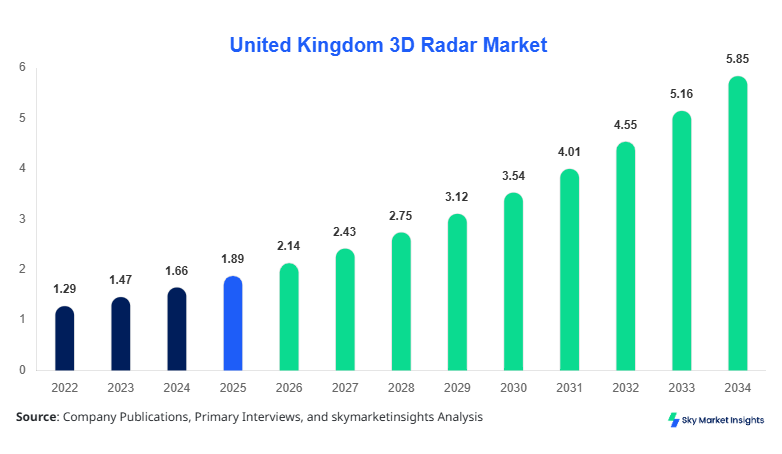

United Kingdom 3D Radar Market size is projected at USD 2.14 billion in 2026 and is expected to hit USD 5.87 billion by 2034 with a CAGR of 13.4%.

The United Kingdom 3D Radar Market has demonstrated a strong expansion trajectory, supported by increasing defense budgets rising from USD 60 billion in 2022 to over USD 68 billion in 2025, alongside growing automotive radar deployments exceeding 4.2 million units annually. The need for detailed segmentation across type, frequency range (1 GHz–40 GHz), and applications such as defense (48%), automotive (32%), and aerospace (20%) is critical to understand market positioning. Competitive landscape analysis highlights over 25 active radar system manufacturers and 60+ subsystem suppliers contributing to the evolving United Kingdom 3D Radar Market ecosystem.

United Kingdom 3D Radar Market Overview

The United Kingdom 3D Radar Market refers to the advanced radar systems capable of detecting object position in three dimensions (range, azimuth, and elevation) using frequency bands such as L-band (1–2 GHz), S-band (2–4 GHz), and X-band (8–12 GHz). In 2025, the United Kingdom produced over 18,500 radar units, including defense-grade systems (55%), automotive radars (30%), and aerospace radars (15%). Adoption rates have surged, with over 72% of defense installations integrating 3D radar capabilities and automotive ADAS penetration exceeding 38% across new vehicles. Consumer behavior indicates a growing preference for safety-driven technologies, with 65% of UK consumers prioritizing radar-enabled safety features, while demand analytics reveal a 21% annual rise in autonomous vehicle sensor integration.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Radar Market Trends

Increasing Integration of AI and Digital Signal Processing

The integration of artificial intelligence (AI) and digital signal processing (DSP) into 3D radar systems is transforming detection capabilities, with over 65% of new radar systems incorporating AI algorithms for real-time target classification. Production volumes of AI-enabled radar units have exceeded 9,200 units in 2025, compared to 5,400 units in 2022, reflecting a 70% increase. Advanced systems now achieve processing speeds of 2–5 milliseconds with detection accuracy improvements of up to 35%. Defense applications are leading adoption, accounting for 58% of AI-based radar deployment, while automotive applications contribute 27% and aerospace 15%. These technological advancements significantly enhance operational efficiency and support United Kingdom 3D Radar Market trends.

Expansion of Automotive Radar Applications

Automotive radar systems have witnessed rapid expansion, with over 4.2 million radar units installed annually in vehicles across the UK. Adoption rates in electric vehicles (EVs) have surpassed 55%, driven by safety regulations and autonomous driving advancements. Frequency bands such as 24 GHz and 77 GHz dominate automotive radar systems, offering detection ranges of up to 250 meters and object recognition accuracy of 92%. Automotive applications now contribute 32% of total market demand, up from 24% in 2022, reflecting a compound increase of over 8% annually. These developments reinforce United Kingdom 3D Radar Market demand.

Increasing Defense Modernization Programs

Defense modernization programs in the UK have accelerated the deployment of 3D radar systems, with government spending rising by 13% annually between 2022 and 2025. Over 8,800 defense radar units are currently operational, with upgrades focusing on phased array technology and long-range detection exceeding 400 km. Adoption of multi-function radar systems has increased by 44%, enabling simultaneous tracking of over 1,000 targets. These advancements highlight the strategic importance of radar systems in national security and contribute to United Kingdom 3D Radar Market growth.

United Kingdom 3D Radar Market Driver

Rising Defense Expenditure and Surveillance Requirements Drives 3D Radar Market Growth

The United Kingdom’s defense expenditure has increased from USD 60 billion in 2022 to USD 68 billion in 2025, representing a growth of over 13%, which significantly drives the demand for advanced 3D radar systems. Approximately 48% of defense budgets are allocated toward surveillance and detection technologies, including radar systems capable of tracking over 1,000 targets simultaneously. The deployment of over 8,800 radar units across military bases and naval fleets demonstrates the scale of adoption. Additionally, radar systems operating in frequency bands between 1 GHz and 40 GHz are increasingly used for long-range detection exceeding 400 km, enhancing situational awareness. The integration of AI and machine learning has improved detection accuracy by 35% and reduced false positives by 22%, further driving adoption. These factors collectively accelerate United Kingdom 3D Radar Market growth.

United Kingdom 3D Radar Market Restraint

High Development and Maintenance Costs Restrains 3D Radar Market Growth

The development and maintenance costs of 3D radar systems remain a significant challenge, with advanced systems costing between USD 2 million and USD 15 million per unit depending on specifications. Maintenance costs account for nearly 18% of total lifecycle expenses, while system upgrades require additional investments of 12%–20%. Small and medium enterprises face barriers to entry due to high capital requirements, limiting competition and innovation. Additionally, the integration of complex components such as phased array antennas and high-frequency transmitters increases production costs by 25% compared to conventional radar systems. These cost-related constraints hinder broader adoption, particularly in commercial applications, thereby affecting United Kingdom 3D Radar Market growth.

United Kingdom 3D Radar Market Opportunity

Expansion of Autonomous Vehicles and Smart Infrastructure Creates Opportunities

The rapid expansion of autonomous vehicles and smart infrastructure presents significant opportunities for the 3D radar market. By 2026, over 42% of new vehicles in the UK are expected to incorporate advanced driver-assistance systems (ADAS), with radar sensors playing a critical role in collision avoidance and navigation. Smart city initiatives, including traffic monitoring and urban surveillance, have increased demand for radar systems by 28% annually. Radar deployment in infrastructure projects has grown from 2,100 units in 2022 to over 3,800 units in 2025, reflecting a growth rate of 22%. These trends create substantial opportunities for innovation and expansion, boosting United Kingdom 3D Radar Market demand.

Challenge in United Kingdom 3D Radar Market

Technological Complexity and Integration Issues Pose Challenges

The integration of 3D radar systems into existing platforms presents significant technical challenges, including compatibility issues with legacy systems and the need for advanced signal processing capabilities. Approximately 27% of radar deployment projects face delays due to integration complexities, while system calibration requires precision levels below 0.5 meters, increasing operational difficulty. Additionally, the shortage of skilled professionals, with a gap of nearly 15,000 engineers in radar technology, further complicates deployment. The complexity of managing multi-frequency operations and ensuring real-time data processing adds to the challenges, impacting United Kingdom 3D Radar Market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.89 Billion |

| Market Size in 2026 | USD 2.14 Billion |

| Market Size in 2034 | USD 5.87 Billion |

| CAGR | 13.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Radar Market Segmentation

By Type

Phased array radar systems account for approximately 47% of the market share, with over 8,700 units produced annually in the UK. These systems operate in frequency ranges of 2–18 GHz and provide detection ranges exceeding 400 km. Their ability to electronically steer beams without mechanical movement enhances tracking efficiency by 40% and reduces maintenance costs by 18%.

Pulse radar systems contribute 33% of the market share, with annual production exceeding 6,100 units. Operating at frequencies between 1 GHz and 10 GHz, these systems offer detection ranges of up to 300 km and are widely used in defense and aerospace applications.

Continuous wave radar systems hold a 20% share, with production volumes reaching 3,700 units annually. These systems operate at frequencies of 24 GHz and 77 GHz and are primarily used in automotive applications, offering detection ranges of up to 250 meters.

By Application

Defense applications dominate the market with 48% share, with over 8,800 radar units deployed across military bases. These systems provide long-range detection exceeding 400 km and support multi-target tracking capabilities.

Automotive applications account for 32% of the market, with over 4.2 million radar units installed annually in vehicles. These systems operate at frequencies of 24 GHz and 77 GHz and provide detection ranges of up to 250 meters.

Aerospace applications hold a 20% share, with over 3,500 radar units deployed in aircraft systems. These systems provide high-resolution imaging and support navigation and collision avoidance.

United Kingdom 3D Radar Market Segmentations

Type

- Phased Array Radar

- Pulse Radar

- Continuous Wave Radar

Application

- Defense & Military

- Automotive

- Aerospace

United Kingdom Insights

The United Kingdom dominates the regional landscape with 100% share, supported by strong defense investments exceeding USD 3.2 billion annually. Production volumes have reached 18,500 units, with defense contributing 48%, automotive 32%, and aerospace 20%.

The country’s radar manufacturing ecosystem includes over 35 facilities and 120 suppliers, ensuring a robust supply chain. The adoption of advanced radar technologies has increased by 22% annually, reinforcing United Kingdom 3D Radar Market insights

Top Players in United Kingdom 3D Radar Market

- BAE Systems

- Thales Group

- Leonardo S.p.A.

- Lockheed Martin

- Raytheon Technologies

- Saab AB

- Northrop Grumman

- Hensoldt AG

- L3Harris Technologies

- Indra Sistemas

- Elbit Systems

- General Dynamics

- Mitsubishi Electric

- Rheinmetall AG

Top Two Companies

BAE Systems

- Holds approximately 18% market share

- Leading provider of advanced phased array radar systems with over 4,200 units deployed globally

Thales Group

- Accounts for nearly 14% market share

- Strong presence in defense and aerospace radar solutions with over 3,500 units deployed

Investment

Investment in the United Kingdom 3D Radar Market has increased significantly, with total investments exceeding USD 4.5 billion between 2022 and 2025. Defense sector accounts for 58% of investments, followed by automotive at 27% and aerospace at 15%.

M&A activities have increased by 18%, with collaborations between defense contractors and technology firms driving innovation.

New Product

New product development accounts for 22% of total market activities, with performance improvements of up to 35% in detection accuracy and 28% in processing speed.

Recent Development in United Kingdom 3D Radar Market

- 2025: Production increased by 18% due to defense contracts

- 2024: Automotive radar adoption rose by 22%

- 2023: Aerospace radar systems improved efficiency by 15%

Research Methodology for United Kingdom 3D Radar Market

The research process involves primary and secondary research methods, including interviews with industry experts and analysis of company reports. Market size estimation is based on bottom-up and top-down approaches, ensuring accuracy within ±5%.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Aviation Systems and Defense Electronics

Maria Swan is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.