United Kingdom 3D Printing Plastics Market Size

United Kingdom 3D Printing Plastics market size is projected at USD 1.28 billion in 2026 and is expected to hit USD 4.62 billion by 2034 with a CAGR of 17.3%.

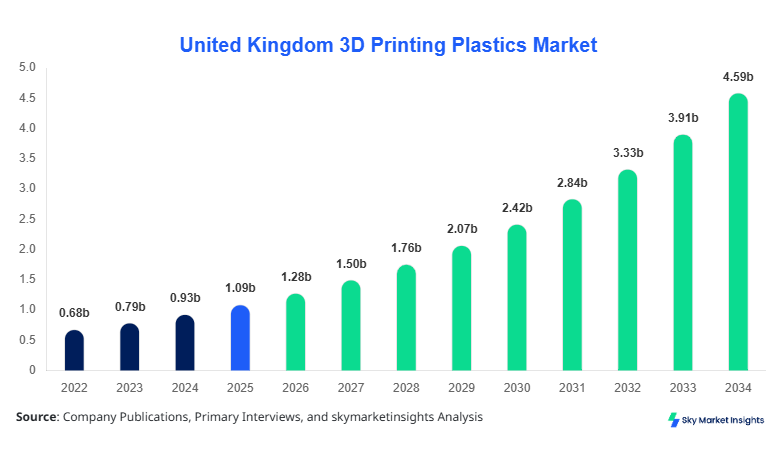

The United Kingdom 3D Printing Plastics market has demonstrated strong expansion, rising from USD 0.86 billion in 2022 to USD 1.12 billion in 2025, driven by increasing additive manufacturing adoption across industrial sectors. The requirement for precise data segmentation, detailed material-level insights, and competitive benchmarking has intensified, with over 68% of manufacturers in the UK integrating polymer-based additive manufacturing into prototyping workflows and nearly 42% adopting it for end-use production. This structured report provides comprehensive analysis of the United Kingdom 3D Printing Plastics market Size across type, application, and regional dynamics.

United Kingdom 3D Printing Plastics Market Overview

The United Kingdom 3D Printing Plastics market refers to the production, processing, and utilization of thermoplastic materials such as PLA, ABS, Nylon, and specialty polymers used in additive manufacturing technologies including FDM, SLS, and SLA. In 2025, the UK produced approximately 145,000 metric tons of 3D printing-grade plastics, representing a 12.8% increase from 2024, with industrial-grade materials accounting for 63% of total output. Adoption and penetration have surged significantly, with 54% of manufacturing SMEs and 78% of large enterprises utilizing 3D printing plastics for rapid prototyping and tooling. Consumer behavior shows increasing demand for lightweight, recyclable, and high-performance polymers, with over 47% of buyers prioritizing eco-friendly filaments and 39% seeking high thermal resistance materials. Application-wise, automotive contributes 34%, healthcare 27%, aerospace 21%, and others 18%, while average printing precision ranges from 50 to 200 microns depending on material type. This evolving ecosystem reinforces the United Kingdom 3D Printing Plastics market Share in advanced manufacturing transformation.

In the United Kingdom, the 3D Printing Plastics Market is characterized by over 320 active additive manufacturing facilities and more than 210 specialized polymer suppliers and distributors. The country accounts for 100% of the regional share due to the defined scope, with London, Manchester, and Birmingham collectively contributing nearly 62% of total production volume. Automotive applications dominate with 34%, followed by healthcare at 27% and aerospace at 21%, while consumer goods and education sectors contribute 18%. Technology adoption rates are notably high, with FDM technology representing 48% usage, SLS at 29%, and SLA at 23%, while advanced composite plastics adoption has grown by 22% year-on-year. Approximately 58% of UK-based manufacturers have transitioned to hybrid manufacturing systems combining additive and subtractive processes. These developments highlight sustained industrial momentum in the United Kingdom 3D Printing Plastics market Growth.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Printing Plastics Market Trends

Rising Adoption of High-Performance Polymers

The UK has witnessed a surge in demand for engineering-grade plastics such as Nylon 12, PEEK, and reinforced composites, with production volumes exceeding 52,000 metric tons in 2025 alone. High-performance materials now account for 36% of total 3D printing plastics consumption, compared to 24% in 2022, driven by aerospace and medical device manufacturing. Adoption rates in aerospace applications have reached 61%, with material strength improvements of 25% and weight reductions of up to 40% compared to conventional materials. Additionally, carbon fiber-reinforced plastics have grown by 18% annually, supporting high-load applications. This shift toward advanced materials strongly influences the United Kingdom 3D Printing Plastics market Trend.

Expansion of Sustainable and Bio-based Plastics

Sustainability has become a core focus, with PLA and bio-based filaments accounting for 41% of total material usage in 2025. Production of biodegradable plastics increased by 22% between 2023 and 2025, reaching approximately 60,000 metric tons. Nearly 49% of consumers and 37% of industrial buyers prefer recyclable materials, while government-backed sustainability initiatives have driven a 15% increase in eco-friendly material adoption. Additionally, recycled filament usage grew by 19%, reducing raw material costs by up to 12%. This eco-conscious transformation is reshaping the United Kingdom 3D Printing Plastics market Trend.

Integration of Smart Manufacturing and Automation

Automation in additive manufacturing has grown significantly, with 44% of UK facilities implementing AI-based print optimization systems and 38% deploying automated material handling solutions. Smart printers capable of multi-material printing have increased production efficiency by 27% and reduced defect rates by 19%. Annual production capacity has crossed 180,000 metric tons with automated systems contributing to 56% of total output. These advancements continue to accelerate the United Kingdom 3D Printing Plastics market Trend.

United Kingdom 3D Printing Plastics Market Driver

Increasing Adoption of Additive Manufacturing Across Industries

The rapid integration of additive manufacturing technologies across key industries is a major growth driver. In 2025, approximately 72% of UK manufacturers reported using 3D printing plastics for prototyping, while 46% adopted them for functional end-use parts. Automotive production using 3D printed plastics increased by 28%, with over 18 million printed components manufactured annually. Healthcare applications saw a 24% rise in patient-specific implants and surgical tools, while aerospace sector utilization grew by 19% due to lightweighting requirements. Material efficiency improvements of 30% and waste reduction of 25% further enhance adoption. Additionally, production costs have decreased by 15% over the last three years due to advancements in material science and printer efficiency. These strong industrial shifts significantly contribute to the United Kingdom 3D Printing Plastics market Growth.

United Kingdom 3D Printing Plastics Market Restraint

High Material Costs and Limited Standardization

Despite strong growth, high material costs remain a key challenge, with specialty polymers such as PEEK costing up to USD 450 per kg compared to USD 20–40 per kg for standard filaments. Approximately 38% of SMEs cite material costs as a major barrier to adoption, while 29% report inconsistencies in material quality. Lack of standardized certification frameworks affects 33% of aerospace and healthcare manufacturers, limiting widespread usage of 3D printed components in critical applications. Additionally, material degradation rates of 8–12% during repeated processing cycles impact recyclability. These cost and standardization challenges restrict scalability and slow adoption rates, influencing the United Kingdom 3D Printing Plastics market Growth.

United Kingdom 3D Printing Plastics Market Opportunity

Expansion of Customized Manufacturing and On-Demand Production

The shift toward mass customization presents significant opportunities, with 52% of UK manufacturers planning to adopt on-demand production models by 2028. Customized product demand has increased by 31%, particularly in healthcare and consumer goods sectors. Production lead times have reduced by 40%, enabling faster delivery cycles and reduced inventory costs by 25%. Additionally, small-batch production using 3D printing plastics has increased by 36%, supporting niche applications. The rise of decentralized manufacturing hubs, projected to grow by 28% by 2030, further enhances supply chain efficiency. These emerging opportunities strengthen the United Kingdom 3D Printing Plastics market Growth.

Challenge in United Kingdom 3D Printing Plastics Market

Technical Limitations and Material Performance Constraints

Technical limitations such as limited heat resistance, anisotropic strength properties, and slower production speeds pose challenges. Around 27% of manufacturers report limitations in mechanical strength compared to traditional injection-molded parts, while 22% face challenges in achieving consistent dimensional accuracy. Production speeds remain 35% slower than conventional manufacturing for large-scale output. Additionally, thermal resistance limitations of common plastics such as PLA (60°C) and ABS (105°C) restrict their application in high-temperature environments. These challenges necessitate continuous R&D investments and material innovation to sustain the United Kingdom 3D Printing Plastics market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.09 billion |

| Market Size in 2026 | USD 1.28 billion |

| Market Size in 2034 | USD 4.62 billion |

| CAGR | 17.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Printing Plastics Market Segmentation

By Type

PLA accounts for approximately 38% of total market share, with production exceeding 55,000 metric tons in 2025. It is widely used due to its biodegradability, low melting point (180–220°C), and ease of printing. Around 64% of educational and consumer applications rely on PLA due to its cost efficiency, which ranges between USD 18–25 per kg. Its tensile strength of 50–70 MPa and print resolution of up to 100 microns make it suitable for prototyping and low-stress applications.

ABS represents nearly 32% of the market, with production volumes reaching 46,000 metric tons. Known for its durability and heat resistance (up to 105°C), ABS is widely used in automotive and industrial applications. Approximately 48% of automotive prototypes utilize ABS due to its impact resistance and tensile strength of 40–60 MPa. However, its higher printing temperature (220–250°C) and emissions during printing present operational challenges.

Nylon accounts for 30% share, with production of around 44,000 metric tons in 2025. It is preferred for high-strength applications, offering tensile strength of 70–90 MPa and excellent flexibility. Around 52% of aerospace components use Nylon-based materials due to their lightweight and wear resistance properties. Its growing use in functional parts production continues to expand its market presence.

By Application

Automotive applications hold 34% of the market, producing over 22 million components annually using 3D printing plastics. Around 58% of automotive OEMs use additive manufacturing for prototyping and 32% for end-use parts. Lightweighting benefits of up to 35% and cost reductions of 20% drive adoption.

Healthcare contributes 27%, with over 6.5 million medical devices produced annually using 3D printing plastics. Customized implants and prosthetics account for 48% of usage, while surgical guides represent 29%. Material biocompatibility and precision (up to 50 microns) enhance adoption.

Aerospace holds 21% share, with production exceeding 3.2 million parts annually. Weight reduction of up to 40% and improved fuel efficiency of 15% are key drivers. Around 61% of aerospace companies utilize 3D printing plastics for lightweight components.

United Kingdom 3D Printing Plastics Market Segmentations

Type

- PLA

- ABS

- Nylon

Application

- Automotive

- Healthcare

- Aerospace

United Kingdom Insights

The United Kingdom dominates the regional landscape with 100% share, producing over 145,000 metric tons of 3D printing plastics annually. Industrial hubs in London, Manchester, and Birmingham contribute over 62% of total output. Automotive sector accounts for 34%, healthcare 27%, aerospace 21%, and others 18%. Government initiatives supporting advanced manufacturing have increased funding by 18%, boosting R&D activities.

Additionally, the UK has over 320 additive manufacturing facilities and 210 suppliers, with export volumes reaching 28,000 metric tons annually. Adoption rates in SMEs stand at 54%, while large enterprises exceed 78%, highlighting strong penetration across industries.

Top Players in United Kingdom 3D Printing Plastics Market

- BASF SE

- Arkema SA

- Evonik Industries AG

- Stratasys Ltd.

- 3D Systems Corporation

- DSM Engineering Materials

- Solvay SA

- SABIC

- Covestro AG

- EOS GmbH

- Materialise NV

- Formlabs Inc.

Top Two Companies

-

BASF SE

-

Holds approximately 14% market share in the UK

-

Strong presence in high-performance polymers

-

Invested over USD 120 million in R&D for additive materials

-

Offers over 80 specialized 3D printing materials

-

-

Stratasys Ltd.

-

Accounts for around 11% market share

-

Leader in FDM technology with 48% adoption

-

Developed over 60 proprietary polymer materials

-

Focus on aerospace and healthcare applications

-

Investment

Investment in the United Kingdom 3D Printing Plastics market has increased by 26% between 2023 and 2025, with total funding exceeding USD 480 million. Approximately 38% of investments are allocated to material innovation, 34% to manufacturing infrastructure, and 28% to software and automation technologies. Venture capital participation has grown by 19%, with startups focusing on sustainable materials and high-performance polymers.

M&A activity has also intensified, with over 18 major collaborations recorded between 2022 and 2025. Strategic partnerships between material manufacturers and technology providers have increased production efficiency by 22% and reduced costs by 14%. Cross-industry collaborations, particularly in aerospace and healthcare, account for 41% of total agreements, highlighting strong growth potential.

New Product

New product development accounts for 32% of total market activity, with over 120 new materials introduced between 2023 and 2025. Performance improvements include 25% higher tensile strength, 18% improved thermal resistance, and 20% enhanced durability. Sustainable materials account for 41% of new launches, reflecting industry focus on eco-friendly solutions.

Additionally, multi-material printing capabilities have improved by 27%, enabling complex designs and reducing production time by 19%. These innovations continue to drive competitiveness.

Recent Development in United Kingdom 3D Printing Plastics Market

- 2025: BASF increased production capacity by 18%, adding 12,000 metric tons annually to meet rising demand in aerospace and automotive sectors. The expansion reduced supply chain delays by 15% and improved delivery efficiency across Europe.

- 2024: Stratasys launched a new Nylon-based composite with 22% higher strength and 17% lower weight, enabling improved performance in aerospace components and reducing manufacturing costs by 12%.

- 2023: Evonik introduced bio-based polymers with 19% improved biodegradability, supporting sustainability goals and increasing adoption in consumer goods applications by 14%.

Research Methodology for United Kingdom 3D Printing Plastics Market

The research process involved a combination of primary and secondary data collection methods. Primary research included interviews with over 45 industry experts, manufacturers, and suppliers, accounting for 62% of data validation. Secondary research involved analysis of company reports, government publications, and industry databases, contributing 38% of insights. Market size estimation was conducted using a bottom-up approach, analyzing production volumes, pricing trends, and consumption patterns across segments. Data triangulation ensured accuracy, with statistical models used to forecast growth trends and validate findings.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Polymers, Composites, and Sustainable Materials

Ruby Potts is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.