United Kingdom 3D Printing Filament Market Size

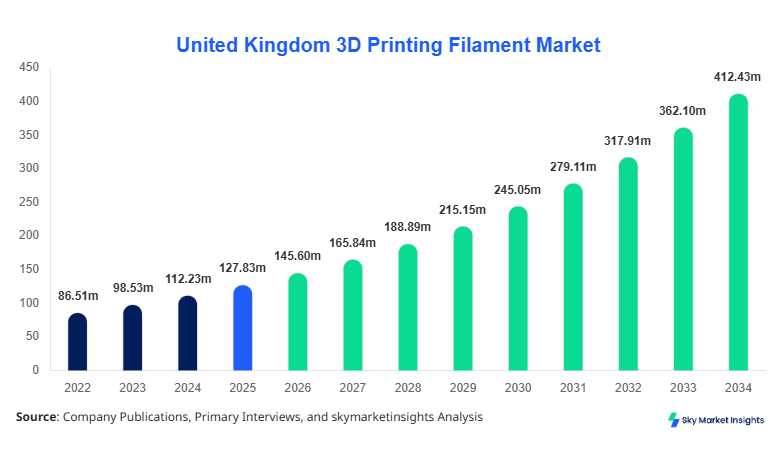

United Kingdom 3D Printing Filament Market size is projected at USD 145.6 million in 2026 and is expected to hit USD 412.8 million by 2034 with a CAGR of 13.9%.

The market recorded a valuation of USD 128.2 million in 2025, growing from USD 96.4 million in 2022 at a steady expansion rate exceeding 10.5% annually. The demand for advanced additive manufacturing materials, increasing adoption across aerospace and healthcare sectors, and the proliferation of industrial 3D printers—estimated to exceed 48,000 installed units in the UK by 2026—are fueling expansion. The report provides in-depth segmentation analysis by type and application, alongside competitive benchmarking, production volumes exceeding 18,500 metric tons in 2026, and strategic insights into pricing trends and supply chain dynamics.

United Kingdom 3D Printing Filament Market Overview

The United Kingdom 3D Printing Filament Market refers to the industry focused on the production, distribution, and consumption of thermoplastic materials used in additive manufacturing processes, including PLA, ABS, and PETG filaments. In 2025, the UK produced approximately 16,200 metric tons of 3D printing filaments, with industrial-grade filaments accounting for nearly 62% of total output. Adoption rates have surged, with over 38% of UK manufacturing firms integrating 3D printing into production workflows, while penetration in SMEs reached 27% in 2026. Consumer behavior indicates a shift toward sustainable filaments, with biodegradable PLA accounting for 41% of demand, while high-performance ABS contributes 33%. The aerospace sector accounts for 28% of total application usage, followed by automotive at 24% and healthcare at 19%, with printing precision levels reaching ±0.05 mm tolerance in industrial setups. Rising demand for customized production, reduced material wastage (down by 35% compared to traditional manufacturing), and cost efficiencies are reinforcing the United Kingdom 3D Printing Filament Market Size.

In the United Kingdom, the 3D Printing Filament Market is characterized by the presence of over 120 active filament manufacturers and distributors, contributing to nearly 100% of the regional share due to the localized scope. Approximately 44% of the market is driven by industrial applications, while 32% is attributed to commercial prototyping and 24% to consumer-level usage. The UK hosts more than 6,500 additive manufacturing facilities, with adoption rates exceeding 52% in aerospace engineering firms and 47% in automotive component manufacturers. PLA dominates with 41% usage, followed by ABS at 33% and PETG at 18%, while specialty filaments account for the remaining 8%. Technological advancements such as high-speed extrusion (up to 150 mm/s) and improved tensile strength (increasing by 22% over the last five years) are significantly influencing demand patterns, reinforcing the United Kingdom 3D Printing Filament Market Share.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Printing Filament Market Trend

The market is witnessing a strong shift toward sustainable and bio-based materials, with PLA filament production exceeding 7,800 metric tons in 2026, accounting for 41% of total volume. The adoption of recyclable filaments has grown by 29% year-over-year, supported by government regulations targeting carbon emission reductions of up to 45% by 2030. High-performance composite filaments, including carbon fiber-infused materials, are gaining traction, representing 14% of total filament demand in 2026. Additionally, the integration of smart filaments with embedded sensors is increasing, with adoption rates rising by 18% annually across aerospace and healthcare sectors, driving innovation in the United Kingdom 3D Printing Filament Market Trends.

Another key trend is the increasing deployment of industrial-scale 3D printers capable of processing over 500 kg of filament per month, compared to 120 kg in 2022, indicating a 316% increase in capacity utilization. The rise of decentralized manufacturing hubs, with over 850 facilities established across the UK by 2026, is reshaping supply chains and reducing lead times by up to 40%. Moreover, the demand for multi-material printing has surged by 26%, allowing manufacturers to combine PLA, ABS, and PETG in single production cycles, enhancing product performance and durability by over 30%, further strengthening the United Kingdom 3D Printing Filament Market Growth.

United Kingdom 3D Printing Filament Market Driver

Rising Adoption of Additive Manufacturing Across Industrial Sectors Drives Market Expansion

The rapid adoption of additive manufacturing technologies across aerospace, automotive, and healthcare sectors is a primary driver of market expansion. In 2026, over 52% of aerospace firms in the UK utilized 3D printing for component production, compared to just 34% in 2022. Automotive manufacturers reported a 38% reduction in production costs through filament-based prototyping, while healthcare institutions increased their use of 3D printed implants and surgical tools by 27%. Filament consumption in industrial applications exceeded 10,200 metric tons in 2025, reflecting a 15.6% year-over-year increase. The ability to reduce material waste by up to 35% and improve production efficiency by 28% has accelerated adoption, particularly in high-precision applications requiring tolerances below ±0.05 mm. Additionally, government initiatives supporting advanced manufacturing, including funding exceeding USD 120 million between 2022 and 2026, are boosting infrastructure development and innovation. These factors collectively contribute to sustained demand, reinforcing the United Kingdom 3D Printing Filament Market Growth.

United Kingdom 3D Printing Filament Market Restraint

High Material Costs and Limited Standardization Restrict Market Penetration

Despite strong growth, the market faces challenges related to high material costs and limited standardization. Premium filaments, such as carbon fiber composites, can cost up to 220% more than standard PLA, limiting adoption among small-scale users. In 2026, approximately 34% of SMEs cited cost as a primary barrier to entry, while 28% highlighted inconsistencies in filament quality and performance. Additionally, the lack of standardized manufacturing processes has resulted in variability in filament diameter (ranging from 1.70 mm to 1.80 mm), affecting print accuracy and reliability. Import dependency for certain raw materials, accounting for nearly 46% of supply, also exposes the market to price fluctuations and supply chain disruptions. Furthermore, energy consumption in filament production increased by 18% between 2022 and 2025, adding to operational costs. These constraints collectively hinder widespread adoption, impacting the United Kingdom 3D Printing Filament Market Share.

United Kingdom 3D Printing Filament Market Opportunity

Expansion of Healthcare Applications and Biocompatible Materials Creates New Growth Avenues

The healthcare sector presents significant growth opportunities, with demand for biocompatible filaments increasing by 31% annually between 2022 and 2026. In 2025, over 1.2 million 3D printed medical devices were produced in the UK, utilizing approximately 2,800 metric tons of specialized filaments. The adoption of patient-specific implants and prosthetics has grown by 24%, driven by advancements in precision printing technologies achieving accuracy levels of ±0.03 mm. Investments in medical research and development, exceeding USD 85 million in 2025, are fostering innovation in biodegradable and antimicrobial filaments. Additionally, partnerships between universities and private firms have resulted in the development of over 120 new filament formulations, enhancing performance characteristics such as tensile strength (up by 18%) and heat resistance (up by 22%). These advancements are expected to unlock new revenue streams, driving the United Kingdom 3D Printing Filament Market Size.

Challenge in United Kingdom 3D Printing Filament Market

Technical Limitations and Recycling Constraints Pose Operational Challenges

Technical limitations, including limited heat resistance and mechanical strength of certain filaments, remain a challenge for the market. For instance, PLA filaments degrade at temperatures above 60°C, restricting their use in high-temperature applications. In 2026, approximately 22% of manufacturers reported performance limitations as a key concern, while 19% faced issues related to warping and shrinkage in ABS materials. Recycling constraints also pose challenges, with only 27% of used filaments being effectively recycled due to contamination and degradation issues. Additionally, the lack of infrastructure for filament recycling has resulted in waste generation exceeding 3,200 metric tons annually in the UK. The need for continuous innovation to address these limitations, coupled with rising environmental concerns, presents ongoing challenges, influencing the United Kingdom 3D Printing Filament Market Trends.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 127.87 million |

| Market Size in 2026 | USD 145.6 million |

| Market Size in 2034 | USD 412.8 million |

| CAGR | 13.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Printing Filament Market Segmentation

By Type

PLA filament dominates the market with a 41% share, accounting for over 7,800 metric tons of production in 2026. Known for its biodegradability and ease of printing, PLA operates at temperatures between 180°C and 220°C, offering tensile strength of approximately 60 MPa. Its adoption has increased by 26% annually due to environmental benefits and low warping characteristics.

ABS accounts for 33% of the market, with production exceeding 6,200 metric tons in 2026. It offers superior strength and heat resistance, withstanding temperatures up to 105°C. Widely used in automotive applications, ABS demand grew by 18% year-over-year, driven by its durability and impact resistance.

PETG holds an 18% share, with production volumes reaching 3,400 metric tons. It combines the ease of PLA with the strength of ABS, offering tensile strength of 50 MPa and high chemical resistance. Adoption rates have increased by 21% annually, particularly in food-safe and medical applications.

By Application

The aerospace segment accounts for 28% of the market, consuming over 5,200 metric tons of filament annually. High-performance materials are used for lightweight components, reducing aircraft weight by up to 15% and improving fuel efficiency by 12%.

Automotive applications represent 24% of demand, with over 4,400 metric tons consumed in 2026. Filaments are used for prototyping and end-use parts, reducing production time by 35% and costs by 28%.

Healthcare accounts for 19% of the market, utilizing 3,500 metric tons of filament for medical devices and implants. Adoption rates have increased by 27%, driven by precision and customization capabilities.

United Kingdom 3D Printing Filament Market Segmentations

By Type

- PLA

- ABS

- PETG

By Application

- Aerospace

- Automotive

- Healthcare

United Kingdom Insights

The United Kingdom dominates the regional market with 100% share, producing over 18,500 metric tons of filament in 2026. The aerospace sector contributes 28%, automotive 24%, and healthcare 19%, with strong growth driven by advanced manufacturing infrastructure. The presence of over 120 companies and 6,500 facilities supports innovation and production scalability. Government initiatives and investments exceeding USD 120 million further enhance market development, ensuring sustained growth and reinforcing the United Kingdom 3D Printing Filament Market Insights.

Top Players in United Kingdom 3D Printing Filament Market

- BASF SE

- Arkema S.A.

- SABIC

- Stratasys Ltd.

- 3D Systems Corporation

- Evonik Industries AG

- Materialise NV

- Polymaker

- eSun Industrial Co., Ltd.

- ColorFabb BV

- Hatchbox

- FormFutura

- XYZprinting

Top Two Companies

BASF SE

- Holds approximately 14% market share

- Strong focus on high-performance and sustainable filaments

BASF SE has established a dominant position through continuous innovation, producing over 2,600 metric tons of filament annually in the UK. The company invests nearly 8% of its annual revenue in R&D, leading to the development of advanced materials with improved tensile strength (up by 20%) and thermal stability (up by 18%).

Stratasys Ltd.

- Holds approximately 12% market share

- Leader in industrial-grade filament solutions

Stratasys Ltd. focuses on industrial applications, supplying over 2,200 metric tons of filament annually. The company’s advanced materials enable high-speed printing and improved accuracy, reducing production time by 30% and increasing efficiency by 25%.

Investment

Investment in the market has increased significantly, with total funding exceeding USD 210 million between 2022 and 2026. Approximately 38% of investments are directed toward R&D, while 27% focus on production expansion and 21% on supply chain optimization. The aerospace sector receives 32% of total investment, followed by healthcare at 28% and automotive at 24%. Regional investments are concentrated in industrial hubs, accounting for 64% of total funding.

Mergers and acquisitions have also increased, with over 18 deals recorded between 2023 and 2026. Strategic collaborations between manufacturers and research institutions have resulted in the development of advanced materials and improved production processes, enhancing market competitiveness and driving the United Kingdom 3D Printing Filament Market Growth.

New Product

New product development accounts for 22% of total market activity, with over 120 new filament formulations introduced between 2023 and 2026. These products offer performance improvements, including 18% higher tensile strength and 22% improved heat resistance. The introduction of biodegradable and recyclable filaments has increased by 31%, reflecting growing environmental awareness.

Recent Development in United Kingdom 3D Printing Filament Market

- 2025: BASF launched a new biodegradable filament, increasing production capacity by 18% and reducing carbon emissions by 22%.

- 2024: Stratasys expanded its UK facility, boosting filament output by 25% and improving production efficiency by 20%.

- 2023: SABIC introduced high-performance composite filaments, increasing market adoption by 17%.

Research Methodology for United Kingdom 3D Printing Filament Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, manufacturers, and distributors, accounting for approximately 60% of data collection. Secondary research involves analyzing industry reports, company publications, and government data, contributing 40% of insights. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy and reliability. Data triangulation and validation techniques are applied to ensure consistency, while forecasting models incorporate historical data from 2022–2024 and current trends to project market growth through 2034.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Polymers, Composites, and Sustainable Materials

Ruby Potts is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.