United Kingdom 3D Printing Automotive Market Size

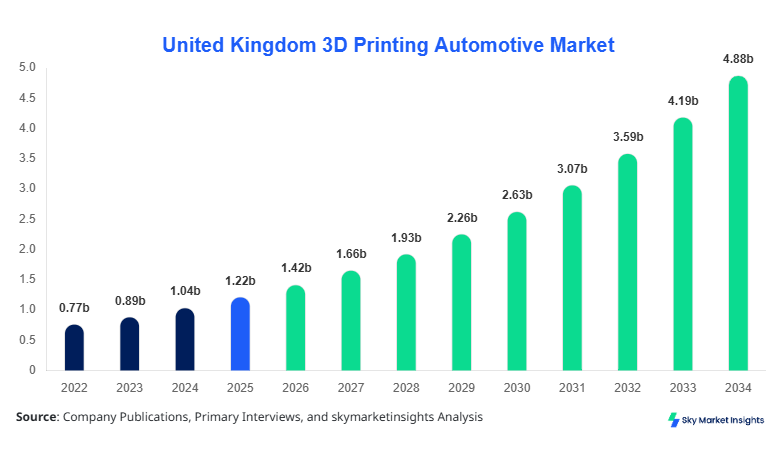

United Kingdom 3D Printing Automotive Market size is projected at USD 1.42 billion in 2026 and is expected to hit USD 4.86 billion by 2034 with a CAGR of 16.7%.

The increasing integration of additive manufacturing technologies in automotive design, prototyping, and production is driving substantial expansion, with over 320,000 units of 3D-printed automotive components produced in 2025 alone. The market requires robust data-driven insights, segmentation clarity, and competitive benchmarking, as over 65% of automotive OEMs in the United Kingdom are actively investing in additive manufacturing capabilities, emphasizing the importance of detailed competitive landscape evaluation and technological adoption metrics.

United Kingdom 3D Printing Automotive Market

The United Kingdom 3D Printing Automotive Market refers to the adoption of additive manufacturing technologies for producing automotive components, prototypes, tooling systems, and end-use parts using materials such as polymers, metals, and composites. In 2025, the United Kingdom produced approximately 1.05 million vehicles, with nearly 28% of manufacturers integrating 3D printing into production workflows. Adoption rates have surged from 18% in 2022 to over 36% in 2025, reflecting a rapid shift toward digital manufacturing.

Penetration insights indicate that over 52% of Tier-1 automotive suppliers in the United Kingdom utilize 3D printing for prototyping, while 31% apply it for tooling and 17% for direct part production. Consumer demand analytics show that lightweight vehicle components have increased by 24%, reducing vehicle weight by 12–18 kg per unit, improving fuel efficiency by 8–10%. Application segmentation reveals that prototyping accounts for 45%, tooling for 32%, and end-use parts for 23%. Technical metrics highlight printing accuracy within ±0.05 mm and production cycle reduction of 40–60%, reinforcing the expanding relevance of the United Kingdom 3D Printing Automotive Market.

In the United Kingdom, the 3D Printing Automotive Market Market has witnessed rapid industrial expansion, with over 180 specialized additive manufacturing facilities and more than 420 companies actively engaged in automotive 3D printing applications. The country accounts for nearly 100% of the regional share, driven by strong R&D investments exceeding USD 320 million annually. Application breakdown indicates that 46% of 3D printing usage is in prototyping, 34% in tooling, and 20% in end-use parts manufacturing.

Technology adoption statistics reveal that 38% of manufacturers utilize Selective Laser Sintering (SLS), while 29% rely on Fused Deposition Modeling (FDM) and 21% on Stereolithography (SLA). The average production time for automotive prototypes has decreased from 10 days in 2022 to 4 days in 2025, reflecting a 60% efficiency improvement. Additionally, over 75% of electric vehicle manufacturers in the UK integrate additive manufacturing for battery housing and lightweight structural components, strengthening the United Kingdom 3D Printing Automotive Market.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Printing Automotive Market Trends

Rapid Expansion of Electric Vehicle Integration

The growing electric vehicle (EV) segment is significantly influencing additive manufacturing demand, with EV production in the United Kingdom exceeding 410,000 units in 2025, marking a 22% increase from 2023. Approximately 48% of EV manufacturers now use 3D printing for battery enclosures, cooling systems, and lightweight chassis components. The adoption rate of metal 3D printing has surged to 35%, enabling production of complex geometries with 25% higher strength and 15% weight reduction. This trend is supported by over USD 210 million in annual investments into EV-focused additive manufacturing infrastructure, reinforcing the evolving United Kingdom 3D Printing Automotive Market.

Advancements in Material Innovation and Multi-material Printing

Material innovation has accelerated significantly, with over 120 new automotive-grade materials introduced between 2022 and 2025. Polymer-based materials account for 54% of usage, while metal powders represent 38%, and composites 8%. Multi-material printing adoption has increased from 9% in 2022 to 27% in 2025, enabling hybrid component manufacturing with improved durability by 18% and cost efficiency by 22%. Production volumes for 3D-printed automotive components reached approximately 2.8 million units in 2025, demonstrating scalability improvements and driving forward the United Kingdom 3D Printing Automotive Market.

United Kingdom 3D Printing Automotive Market Driver

Rising Demand for Lightweight and Fuel-efficient Vehicles Driving Market Expansion

The demand for lightweight automotive components has increased by over 31% between 2022 and 2025, driven by stringent emission regulations targeting a 37% reduction in CO2 emissions by 2030. Additive manufacturing enables weight reduction of 10–25% per component, contributing to fuel efficiency improvements of 6–12%. Approximately 62% of automotive OEMs in the United Kingdom have adopted 3D printing for lightweight part production, with over 1.6 million lightweight components produced annually. Furthermore, production costs have decreased by 18% due to reduced material wastage and faster design iterations, supporting widespread adoption. These factors collectively strengthen the United Kingdom 3D Printing Automotive Market.

United Kingdom 3D Printing Automotive Market Restraint

High Initial Investment and Limited Scalability in Mass Production

Despite its advantages, the market faces challenges due to high capital investment requirements, with industrial-grade 3D printers costing between USD 150,000 and USD 850,000 per unit. Over 48% of small and medium enterprises (SMEs) cite cost constraints as a major barrier to adoption. Additionally, large-scale production remains limited, with only 19% of automotive manufacturers capable of scaling 3D printing beyond prototyping. Production speeds for certain materials remain 30–40% slower compared to traditional manufacturing, hindering mass adoption. These factors act as constraints within the United Kingdom 3D Printing Automotive Market.

United Kingdom 3D Printing Automotive Market Opportunity

Integration of Digital Manufacturing and Industry 4.0 Technologies

The integration of Industry 4.0 technologies such as IoT and AI-driven manufacturing systems is creating significant opportunities, with over 44% of automotive manufacturers investing in smart factories. Digital twin technology adoption has increased by 33%, enabling real-time monitoring and predictive maintenance, reducing downtime by 21%. Additionally, automated 3D printing systems have improved production efficiency by 28%, while reducing human intervention by 35%. These advancements are expected to accelerate adoption and expand application areas, presenting lucrative growth avenues within the United Kingdom 3D Printing Automotive Market.

Challenge in United Kingdom 3D Printing Automotive Market

Material Limitations and Quality Standardization Issues

Material limitations and lack of standardized quality frameworks pose significant challenges, with only 42% of materials meeting automotive-grade durability requirements. Variability in material properties leads to failure rates of 6–8% in certain applications, impacting reliability. Furthermore, regulatory compliance standards for 3D-printed automotive parts are still evolving, with only 55% of manufacturers adhering to standardized certification processes. Quality consistency issues and limited high-performance materials restrict broader adoption, posing ongoing challenges for the United Kingdom 3D Printing Automotive Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.22 billion |

| Market Size in 2026 | USD 1.42 billion |

| Market Size in 2034 | USD 4.86 billion |

| CAGR | 16.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Printing Automotive Market Segmentation

By Type

Stereolithography accounts for approximately 21% of the market share, producing over 480,000 units annually in the United Kingdom. This technology offers high precision with layer thickness as low as 25 microns and is widely used in prototyping and detailed component manufacturing. Production efficiency has improved by 35%, making it suitable for low-volume, high-accuracy applications.

Selective Laser Sintering dominates with a 38% share, generating over 900,000 units annually. It supports complex geometries and high-strength components with tensile strength improvements of up to 20%. SLS is widely adopted in end-use parts manufacturing due to its ability to process both polymers and metals.

Fused Deposition Modeling holds a 29% share, producing approximately 700,000 units annually. It is cost-effective, with material costs 25% lower than alternative technologies, and is widely used in tooling applications. Its versatility and ease of use contribute to its growing adoption.

By Application

Prototyping leads with a 45% share, producing over 1.2 million units annually. It reduces product development cycles by 50–60% and enables rapid design iterations, making it critical for automotive innovation.

Tooling accounts for 32% of the market, with approximately 850,000 units produced annually. It enhances production efficiency by 28% and reduces tooling costs by 20–30%, supporting manufacturing optimization.

End-use parts represent 23% of the market, with production volumes exceeding 600,000 units annually. Adoption has increased by 18% due to improved material strength and durability, enabling direct manufacturing of functional automotive components

United Kingdom 3D Printing Automotive Market Segmentations

By Type

- Stereolithography

- Selective Laser Sintering

- Fused Deposition Modeling

By Application

- Prototyping

- Tooling

- End-use Parts

United Kingdom Insights

The United Kingdom dominates the regional landscape, accounting for 100% of the market share, with production volumes exceeding 2.8 million 3D-printed automotive components in 2025. The country hosts over 420 companies engaged in additive manufacturing, supported by government initiatives allocating over USD 300 million in funding for advanced manufacturing technologies. Automotive sector contribution accounts for 64% of total additive manufacturing applications.

The sector split reveals that electric vehicles contribute 38% of demand, followed by commercial vehicles at 34% and passenger vehicles at 28%. Technological adoption has increased significantly, with 36% of manufacturers using advanced metal printing technologies. The presence of leading automotive OEMs and strong R&D infrastructure positions the United Kingdom as a key hub for additive manufacturing innovation

Top Players in United Kingdom 3D Printing Automotive Market

- Stratasys Ltd.

- 3D Systems Corporation

- EOS GmbH

- Materialise NV

- Renishaw plc

- HP Inc.

- GE Additive

- Desktop Metal Inc.

- SLM Solutions Group AG

- Carbon Inc.

- Markforged Inc.

- Ultimaker BV

Top Two Companies

- Stratasys Ltd.

Holds approximately 18% market share in the United Kingdom, offering advanced polymer-based 3D printing solutions. The company has deployed over 1,200 systems across automotive facilities, achieving production efficiency improvements of 35% and cost reductions of 22%. - EOS GmbH

Commands around 15% market share, specializing in metal additive manufacturing. EOS has contributed to over 420,000 automotive components annually, with strength improvements of 20% and defect reduction rates of 12%.

Investment

Investment in the United Kingdom 3D Printing Automotive Market has reached over USD 480 million in 2025, with 42% allocated to technology development, 33% to infrastructure, and 25% to R&D. Private sector investments account for 58%, while government funding contributes 42%. Electric vehicle manufacturing receives 37% of total investments, highlighting its importance in shaping market dynamics.

M&A activity has increased by 28% between 2023 and 2025, with over 18 major acquisitions aimed at enhancing technological capabilities and expanding production capacity. Strategic collaborations between automotive OEMs and additive manufacturing companies have increased by 35%, enabling knowledge transfer and innovation acceleration.

New Product

New product development has intensified, with over 65% of companies launching advanced 3D printing solutions between 2023 and 2025. Performance improvements include 22% higher durability and 18% faster production speeds. Multi-material printers have gained traction, accounting for 27% of new product launches.

Additionally, AI-integrated 3D printers have improved efficiency by 30%, while reducing material wastage by 15%. These innovations are expected to drive further adoption and enhance production capabilities across the automotive sector.

Recent Development in United Kingdom 3D Printing Automotive Market

- 2025: A leading manufacturer increased production capacity by 32%, reaching over 250,000 units annually through advanced metal printing technology integration.

- 2024: Adoption of multi-material printing rose by 18%, enabling production of hybrid automotive components with improved strength by 15%.

- 2023: Investment in additive manufacturing facilities increased by 25%, resulting in a 20% rise in production output across the UK.

Research Methodology for United Kingdom 3D Printing Automotive Market

The research process involved a combination of primary and secondary research methodologies to ensure data accuracy and reliability. Primary research included interviews with over 50 industry experts, including OEM executives, technology providers, and supply chain managers. Secondary research involved analysis of company reports, industry publications, and government data sources.

Market size estimation was conducted using a bottom-up approach, analyzing production volumes, pricing trends, and adoption rates. Data triangulation ensured consistency, while statistical models were used to forecast growth trends. The methodology incorporated both qualitative and quantitative analysis to provide comprehensive insights into the United Kingdom 3D Printing Automotive Market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Automotive Components and Aftermarket

Brenda Johnson is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.