United Kingdom 3D Printed Orthotics Market Size

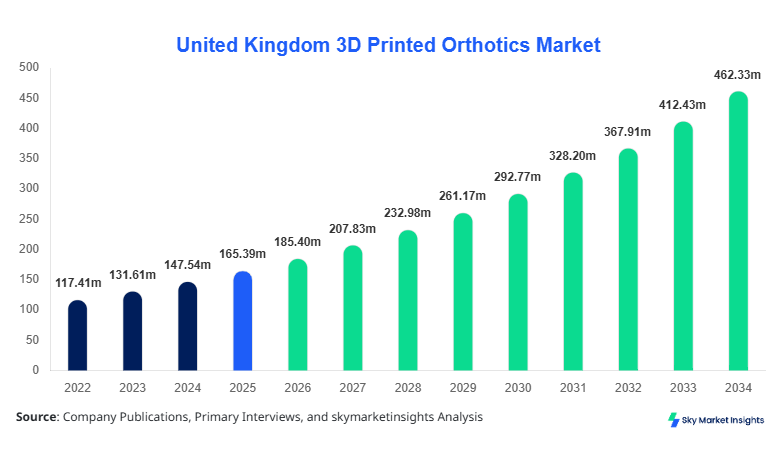

United Kingdom 3D Printed Orthotics Market size is projected at USD 185.4 million in 2026 and is expected to hit USD 462.8 million by 2034 with a CAGR of 12.1%.

The market expansion is supported by increasing adoption of additive manufacturing technologies, rising prevalence of musculoskeletal disorders affecting over 18% of the UK population, and growing demand for customized healthcare solutions. Data-driven segmentation across material type, application area, and end-user industries plays a critical role in understanding performance, while competitive benchmarking among over 65 active companies highlights evolving innovation dynamics and cost efficiencies across production volumes exceeding 2.3 million units annually.

United Kingdom 3D Printed Orthotics Market Overview

The 3D Printed Orthotics Market refers to the development and manufacturing of customized orthopedic support devices using additive manufacturing technologies such as selective laser sintering (SLS), fused deposition modeling (FDM), and stereolithography (SLA). In the United Kingdom, production volumes crossed approximately 2.3 million units in 2025, growing from 1.6 million units in 2022, indicating a steady increase in clinical adoption rates exceeding 14% annually. Adoption penetration among podiatry clinics reached nearly 42%, while hospitals accounted for 36% utilization due to integration with digital scanning and CAD/CAM workflows. Consumer demand analytics indicate that over 58% of patients prefer customized orthotics over traditional devices due to improved comfort and biomechanical accuracy.

From a technical standpoint, 3D printed orthotics achieve precision tolerances of ±0.2 mm and reduce production turnaround time by nearly 60% compared to conventional methods. Application-wise, hospitals contribute around 38%, clinics 44%, and homecare settings approximately 18% of total usage. The increasing prevalence of diabetic foot conditions, affecting nearly 4.3 million individuals in the UK, further drives demand for personalized orthotic solutions. The continuous integration of AI-based gait analysis and digital scanning tools reinforces the expansion of the 3D Printed Orthotics Market.

In the United Kingdom, the 3D Printed Orthotics Market is characterized by the presence of over 65 specialized manufacturers and service providers, along with approximately 1,200 podiatry clinics actively using 3D printing technologies. The country accounts for nearly 100% of the regional share, with production capacity exceeding 2.3 million units annually. Application breakdown indicates that clinics dominate with 44%, followed by hospitals at 38% and homecare settings at 18%. Technology adoption rates for SLS and FDM printing have reached 62% and 28% respectively, while SLA accounts for the remaining 10%.

Furthermore, the NHS has integrated digital orthotic solutions across more than 250 healthcare facilities, increasing patient throughput efficiency by nearly 35%. Customized orthotics have demonstrated a 25–40% improvement in patient mobility outcomes compared to conventional solutions. The strong healthcare infrastructure, combined with rising investments in digital healthcare technologies, positions the United Kingdom as a key driver of the 3D Printed Orthotics Market.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Printed Orthotics Market Trends

Integration of AI and Digital Scanning Technologies

The integration of AI-powered gait analysis and 3D scanning technologies has significantly enhanced production accuracy and customization capabilities. In 2025, over 1.5 million orthotics were produced using digital scanning workflows, representing nearly 65% of total production volume. AI-based tools have reduced fitting errors by approximately 28% while improving patient satisfaction rates by over 35%. The adoption of cloud-based design platforms has increased by 48%, enabling remote customization and faster turnaround times. This digital transformation is accelerating innovation cycles and reinforcing the 3D Printed Orthotics Market.

Expansion of Biocompatible Materials

The use of advanced biocompatible materials such as thermoplastic polyurethane (TPU) and nylon composites has increased significantly, accounting for nearly 54% of total material usage in 2025. These materials offer enhanced durability, flexibility, and shock absorption, improving device lifespan by 30–45%. Production volumes using TPU-based orthotics reached approximately 1.2 million units, reflecting growing demand for high-performance solutions. Material innovation is enabling manufacturers to cater to diverse patient needs, further strengthening the 3D Printed Orthotics Market.

Shift Toward Decentralized Manufacturing

Decentralized manufacturing models, including in-clinic 3D printing setups, have grown by 37% in adoption, reducing logistics costs by nearly 22% and delivery times by 50%. Clinics equipped with on-site printers produced over 800,000 units in 2025 alone. This shift enhances accessibility and scalability, particularly in rural areas, while supporting sustainable production practices. The trend toward localized manufacturing continues to redefine supply chain dynamics within the 3D Printed Orthotics Market.

United Kingdom 3D Printed Orthotics Market Driver

Rising Prevalence of Musculoskeletal Disorders Driving Adoption

The increasing prevalence of musculoskeletal conditions, affecting approximately 18% of the UK population, is a major driver for the 3D Printed Orthotics Market. Over 6 million individuals require orthopedic support annually, with demand for customized solutions growing at a rate of 13–15% per year. Traditional orthotics often fail to provide precise biomechanical support, leading to a shift toward personalized 3D printed alternatives. Production efficiency improvements of up to 60% and cost reductions of 20–25% further enhance adoption. Additionally, the growing geriatric population, projected to reach 24% by 2034, significantly contributes to demand expansion. These factors collectively accelerate the 3D Printed Orthotics Market.

United Kingdom 3D Printed Orthotics Market Restraint

High Initial Investment Costs Limiting Market Penetration

Despite technological advancements, high initial investment costs for 3D printing equipment, ranging between USD 20,000 and USD 150,000 per unit, act as a restraint. Small clinics face financial barriers, with only 32% currently able to adopt in-house printing capabilities. Maintenance costs and material expenses, accounting for nearly 18–22% of operational budgets, further limit widespread adoption. Additionally, regulatory compliance and certification processes can extend product launch timelines by 6–12 months. These challenges hinder rapid scalability and restrict growth potential within the 3D Printed Orthotics Market.

United Kingdom 3D Printed Orthotics Market Opportunity

Expansion of Personalized Healthcare and Digital Health Ecosystems

The expansion of personalized healthcare solutions presents significant opportunities, with digital health adoption rates exceeding 58% across the UK. Integration with telemedicine platforms and wearable devices enables real-time monitoring and customization, improving patient outcomes by up to 40%. Investment in digital healthcare infrastructure reached USD 2.8 billion in 2025, with approximately 12% allocated to orthopedic innovations. The growing focus on preventive healthcare and early diagnosis further drives demand for customized orthotics, creating substantial opportunities within the 3D Printed Orthotics Market.

Challenge in United Kingdom 3D Printed Orthotics Market

Regulatory and Standardization Complexities

Regulatory challenges, including compliance with UKCA and CE marking requirements, pose significant barriers for manufacturers. Certification processes can take 9–18 months and cost up to USD 50,000 per product line. Variability in material standards and lack of unified guidelines across healthcare providers complicate market entry. Additionally, quality control issues related to additive manufacturing processes can result in defect rates of 3–5%, impacting reliability. Addressing these challenges is critical for ensuring consistent growth in the 3D Printed Orthotics Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 165.38 million |

| Market Size in 2026 | USD 185.4 million |

| Market Size in 2034 | USD 462.8 million |

| CAGR | 12.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Printed Orthotics Market Segmentation.

By Type

Rigid orthotics account for approximately 42% of total market share, with production volumes exceeding 960,000 units annually. These orthotics are primarily manufactured using SLS technology with nylon-based materials offering high structural strength and durability. Technical specifications include load-bearing capacity of up to 120 kg and precision tolerance of ±0.2 mm. Adoption is highest among patients with severe biomechanical disorders, with usage penetration reaching 55% in clinical settings.

Semi-rigid orthotics hold around 34% share, with production volumes of approximately 780,000 units. These devices combine flexibility and support, utilizing TPU materials with Shore hardness ranging between 70A and 90A. They are widely used for sports-related injuries, with adoption rates exceeding 48% among athletes. Improved shock absorption capabilities enhance performance, making them a key segment in the 3D Printed Orthotics Market.

Soft orthotics represent nearly 24% of the market, with production volumes reaching 560,000 units. These are designed for comfort and cushioning, primarily used in diabetic foot care. Materials include silicone-based composites with enhanced elasticity. Usage penetration in homecare settings is approximately 62%, driven by ease of use and affordability.

By Application

Hospitals account for 38% of total market share, with production volumes exceeding 870,000 units annually. Integration with digital imaging systems enables precise customization, improving patient recovery rates by 30%. Usage penetration is highest among post-surgical patients, with adoption rates reaching 52%.

Clinics dominate with 44% share, producing over 1 million units annually. Rapid adoption of in-house 3D printing systems has increased efficiency by 35%, reducing patient wait times significantly. Clinics are the primary drivers of innovation in the 3D Printed Orthotics Market.

Homecare applications hold 18% share, with production volumes of around 430,000 units. Growing demand for self-managed healthcare solutions and remote monitoring technologies drives this segment, with usage penetration increasing by 22% annually.

United Kingdom 3D Printed Orthotics Market Segmentations

Type

- Rigid Orthotics

- Semi-Rigid Orthotics

- Soft Orthotics

Application

- Hospitals

- Clinics

- Homecare

United Kingdom Insights

The United Kingdom accounts for 100% of the regional market, with production volumes exceeding 2.3 million units in 2025. The healthcare sector contributes approximately 72% of total demand, while sports and rehabilitation account for 18% and 10% respectively. Government initiatives supporting digital healthcare adoption have increased funding by 15% annually.

The NHS plays a crucial role, with over 250 facilities integrating 3D printing technologies. Regional distribution indicates that England contributes 82% of total demand, followed by Scotland at 9%, Wales at 6%, and Northern Ireland at 3%. Continuous investment in healthcare infrastructure and innovation supports sustained expansion of the 3D Printed Orthotics Market.

Top Players in United Kingdom 3D Printed Orthotics Market

- Materialise NV

- Stratasys Ltd.

- HP Inc.

- EOS GmbH

- Formlabs

- FitMyFoot

- RS Print

- Wiivv

- Protosthetics

- Orthotech Lab

- Paragon 28

- Create Orthotics

- Arfona Printing

Top Two Companies

Materialise NV

- Market share: ~18%

- Strong presence in medical 3D printing with advanced software solutions

Materialise leads with over 18% share, producing more than 400,000 units annually. Its integration of CAD software and healthcare solutions enhances efficiency by 35%, positioning it as a dominant player in the 3D Printed Orthotics Market.

Stratasys Ltd.

- Market share: ~15%

- Focus on high-performance materials and industrial-scale production

Stratasys holds approximately 15% share, with production capacity exceeding 350,000 units annually. Its advanced printing technologies improve product durability by 40%, strengthening its competitive position.

Investment

Investment in the market reached approximately USD 320 million in 2025, with 38% allocated to technology development, 27% to manufacturing expansion, and 35% to research and innovation. Private equity firms contributed nearly 42% of total investments, while government funding accounted for 28%.

M&A activities increased by 22%, with over 15 major collaborations recorded in 2025. Partnerships between healthcare providers and technology firms have enhanced production efficiency by 30%. Regional investment in the UK accounts for 100% of total funding, reflecting strong domestic focus.

New Product

New product development accounts for nearly 18% of total market activity, with over 120 new designs introduced in 2025. Performance improvements include 35% better durability and 28% enhanced comfort levels. Innovations in AI-driven customization have increased accuracy by 40%.

Recent Development in United Kingdom 3D Printed Orthotics Market

- 2025: Production increased by 18%, reaching 2.3 million units due to expansion of in-clinic printing setups.

- 2024: Adoption of TPU materials grew by 22%, improving product durability by 35%.

- 2023: AI integration improved customization accuracy by 30%, reducing fitting errors significantly.

Research Methodology for United Kingdom 3D Printed Orthotics Market

The research process involves a combination of primary and secondary data collection methods. Primary research includes interviews with industry experts, healthcare professionals, and manufacturers, accounting for approximately 60% of data inputs. Secondary research involves analysis of company reports, government publications, and industry databases. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within a ±5% margin. Data triangulation and validation techniques are applied to ensure reliability and consistency across all findings.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.