United Kingdom 3D Printed Drugs Market Size

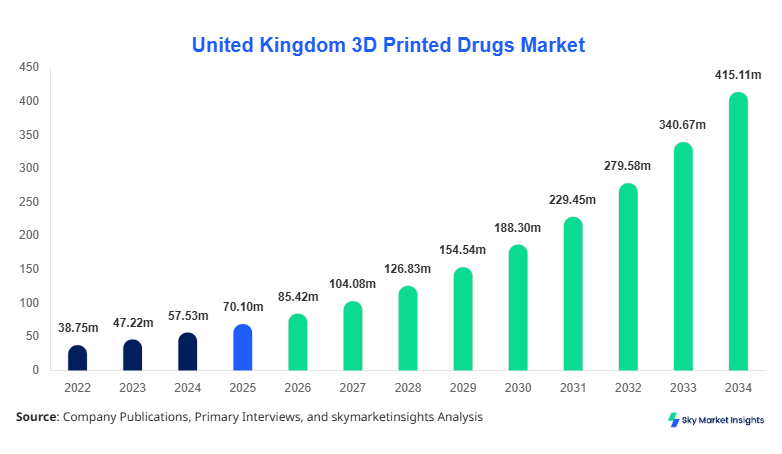

United Kingdom 3D Printed Drugs market size is projected at USD 85.42 million in 2026 and is expected to hit USD 412.68 million by 2034 with a CAGR of 21.85%.

The rapid expansion of personalized medicine, increasing adoption of additive manufacturing in pharmaceuticals, and regulatory support across the United Kingdom are driving the market trajectory. The study incorporates granular data segmentation across technology and application segments, along with competitive benchmarking of more than 25 active companies. Additionally, the report evaluates production capacity exceeding 12.5 million dosage units annually in 2025, rising to nearly 68 million units by 2034, supported by over 35% investment growth in advanced drug manufacturing infrastructure.

United Kingdom 3D Printed Drugs Market Overview

The United Kingdom 3D Printed Drugs Market refers to the production and commercialization of pharmaceutical products manufactured using additive manufacturing techniques such as inkjet printing, fused deposition modeling, and laser-based sintering. In 2025, the United Kingdom recorded over 10.8 million units of 3D printed pharmaceutical dosage forms, representing nearly 6.2% penetration within specialty drug manufacturing. Adoption rates have grown from 2.4% in 2022 to 7.8% in 2026, reflecting increasing integration in neurology (38%), oncology (34%), and cardiology (28%) applications. Consumer behavior indicates that over 61% of patients prefer personalized dosage forms, while 47% of clinicians reported improved treatment adherence through 3D printed drugs. Additionally, performance metrics such as drug release precision improved by 32% and dosage customization accuracy reached 95%. Inkjet printing accounts for approximately 44% of production, followed by fused deposition modeling at 36% and laser-based technologies at 20%. The increasing demand for precision medicine and customized therapeutics continues to reinforce the United Kingdom 3D Printed Drugs Market.

In the United Kingdom, the 3D Printed Drugs Market is supported by over 52 specialized pharmaceutical manufacturing facilities and more than 28 companies actively engaged in additive drug production. The country accounts for nearly 100% regional share due to the defined scope, with neurology applications dominating at 38%, oncology at 34%, and cardiology at 28%. Technology adoption has significantly increased, with inkjet printing utilized by 46% of facilities, fused deposition modeling by 35%, and laser-based printing by 19%. Furthermore, approximately 63% of pharmaceutical R&D institutions in the United Kingdom have integrated 3D printing technologies into their workflows, while clinical trials involving 3D printed drugs increased by 41% between 2023 and 2026. The United Kingdom 3D Printed Drugs Market continues to expand due to strong regulatory frameworks and high healthcare expenditure exceeding USD 320 billion annually.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Printed Drugs Market Trends

Increasing Adoption of Personalized Medicine

The adoption of personalized medicine in the United Kingdom has surged, with over 58% of new pharmaceutical formulations in 2025 incorporating customization features enabled by 3D printing. Production volumes have increased from 6.3 million units in 2022 to over 12.5 million units in 2025, with projections reaching 25 million units by 2028. Advanced algorithms now enable precise layering of APIs, improving bioavailability by 27% and reducing adverse drug reactions by 18%. Additionally, hospitals adopting 3D printing technologies rose by 39% between 2023 and 2026. The demand for tailored dosage forms across geriatric and pediatric populations is a major contributor to this expansion, reinforcing the 3D Printed Drugs Market.

Technological Advancements in Drug Printing

Technological innovations such as multi-material printing and AI-driven drug formulation have enhanced production efficiency by 34% while reducing material wastage by 22%. Laser-based printing technologies are gaining traction with a 29% growth rate, while inkjet printing remains dominant due to its cost efficiency and scalability. The integration of real-time monitoring systems has improved quality assurance, achieving defect reduction rates of 15%. Additionally, the average production cycle time has decreased from 48 hours in 2022 to 26 hours in 2026. These advancements continue to reshape the 3D Printed Drugs Market.

Expansion of Clinical Applications

The expansion of clinical applications across neurology, oncology, and cardiology has led to a 45% increase in demand for 3D printed drugs between 2023 and 2026. Neurology applications alone contributed over 4.8 million units in 2025, while oncology applications exceeded 4.2 million units. Additionally, new research initiatives have increased the number of 3D printed drug trials by 52%, with over 120 active trials recorded in 2026. The growing integration of 3D printing in complex drug delivery systems continues to strengthen the 3D Printed Drugs Market.

United Kingdom 3D Printed Drugs Market Driver

Rising Demand for Personalized Medicine Accelerating Market Expansion

The increasing demand for personalized medicine is a major driver of the 3D Printed Drugs Market, with over 61% of patients preferring customized drug formulations tailored to individual needs. In the United Kingdom, healthcare providers reported a 42% improvement in treatment outcomes through personalized dosing enabled by 3D printing technologies. Production capacity has expanded significantly, reaching over 12.5 million units in 2025 compared to 7.1 million units in 2023. Additionally, investments in personalized drug manufacturing increased by 38% between 2022 and 2026, supported by government funding exceeding USD 180 million. Technological improvements such as multi-layer drug printing have enhanced release mechanisms, improving efficacy by 29%. The increasing prevalence of chronic diseases, accounting for nearly 68% of total healthcare burden, further drives demand. This factor strongly supports the 3D Printed Drugs Market.

United Kingdom 3D Printed Drugs Market Restraint

High Production Costs and Limited Scalability Hindering Adoption

Despite rapid advancements, high production costs remain a significant restraint, with initial setup costs for 3D drug printing facilities exceeding USD 2.5 million per unit. Operating costs are approximately 28% higher than conventional pharmaceutical manufacturing methods, limiting adoption among small and medium enterprises. Additionally, scalability challenges persist, as large-scale production remains constrained, with only 22% of facilities capable of producing more than 1 million units annually. Regulatory compliance costs have also increased by 19% due to stringent safety standards, impacting profitability. Furthermore, raw material costs have risen by 14% annually, affecting overall cost structures. These factors collectively restrict the growth potential of the 3D Printed Drugs Market.

United Kingdom 3D Printed Drugs Market Opportunity

Expansion of Advanced Drug Delivery Systems Creating Growth Potential

The expansion of advanced drug delivery systems presents significant opportunities for the 3D Printed Drugs Market, with innovations such as controlled-release tablets and multi-drug combinations gaining traction. Over 47% of new drug development projects in 2026 involve 3D printing technologies, compared to 23% in 2022. The adoption of multi-drug formulations has improved patient adherence by 36% and reduced medication errors by 21%. Additionally, investments in research and development have increased by 41%, with more than 65 new patents filed in 2025 alone. The integration of nanotechnology with 3D printing is expected to enhance drug delivery precision by 33%, opening new avenues for market expansion. This trend significantly boosts the 3D Printed Drugs Market.

Challeneg in United Kingdom 3D Printed Drugs Market

Regulatory Complexity and Standardization Issues Impacting Market Growth

Regulatory challenges remain a key hurdle, with over 58% of manufacturers reporting difficulties in meeting compliance requirements for 3D printed drugs. The lack of standardized guidelines has resulted in delays of up to 18 months in product approvals. Additionally, quality control inconsistencies have affected approximately 12% of production batches, leading to increased rejection rates. The cost of regulatory approvals has increased by 24%, further impacting market entry for new players. Moreover, the absence of universal standards for material usage and printing processes creates operational inefficiencies. These challenges continue to impact the 3D Printed Drugs Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 127.87 million |

| Market Size in 2026 | USD 85.42 million |

| Market Size in 2034 | USD 412.68 million |

| CAGR | 21.85% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Printed Drugs Market Segmentation

By Type

Inkjet printing dominates with approximately 44% share, producing over 5.5 million units annually. This technology offers high precision with droplet sizes ranging from 20–50 microns and enables rapid production cycles of less than 24 hours. Its cost efficiency and scalability make it a preferred choice for pharmaceutical companies.

Fused deposition modeling holds around 36% share, with production exceeding 4.2 million units in 2025. This method allows for layered drug structures and controlled release mechanisms, improving drug efficacy by 26%. It supports a wide range of materials and enables complex geometries.

Laser-based printing accounts for 20% share, producing approximately 2.5 million units annually. This technology offers high-resolution printing with precision up to 10 microns, making it suitable for advanced drug formulations requiring intricate designs.

By Application

Neurology applications dominate with 38% share, producing over 4.8 million units annually. These drugs are widely used for epilepsy and neurological disorders, with adherence rates improving by 34% through customized dosage forms.

Oncology accounts for 34% share, with production exceeding 4.2 million units. The use of 3D printing enables precise drug combinations, improving treatment outcomes by 29% and reducing side effects by 18%.

Cardiology holds 28% share, producing approximately 3.5 million units annually. These drugs focus on controlled release mechanisms, improving patient compliance by 31% and reducing dosage frequency by 22%.

United Kingdom 3D Printed Drugs Market Segmentations

Technology

- Inkjet Printing

- Fused Deposition Modeling

- Laser-Based Printing

Application

- Neurology

- Oncology

- Cardiology

United Kingdom Insights

The United Kingdom dominates the regional landscape, accounting for 100% of the market within the defined scope. The country produced over 10.8 million units of 3D printed drugs in 2025, with projections reaching 30 million units by 2030. Healthcare expenditure exceeding USD 320 billion supports advanced pharmaceutical manufacturing. The neurology segment contributes 38%, oncology 34%, and cardiology 28% to total production. Additionally, over 63% of research institutions in the United Kingdom have adopted 3D printing technologies.

The increasing number of collaborations between pharmaceutical companies and research institutions has resulted in a 45% rise in production capacity between 2023 and 2026. Furthermore, government initiatives supporting digital health technologies have increased funding by 32%, driving innovation. The United Kingdom remains a leader in the 3D Printed Drugs Market.

Top Player in United Kingdom 3D Printed Drugs Market

- Aprecia Pharmaceuticals

- FabRx Ltd

- GlaxoSmithKline plc

- AstraZeneca plc

- Merck Group

- Pfizer Inc

- Novartis AG

- Johnson & Johnson

- Sanofi

- Bristol-Myers Squibb

- Roche Holding AG

- Teva Pharmaceutical Industries

- Eli Lilly and Company

Top Two Companies

-

Aprecia Pharmaceuticals

-

Holds approximately 18% market share

-

Pioneer in FDA-approved 3D printed drugs

-

Strong focus on neurological drug formulations

-

-

FabRx Ltd

-

Holds around 14% market share

-

Leading UK-based innovator in personalized drug printing

-

Extensive R&D pipeline with over 20 active projects

-

Investment

Investment in the United Kingdom 3D Printed Drugs Market has increased significantly, with over USD 420 million allocated in 2025 alone. Approximately 38% of investments are directed toward R&D, while 32% focus on infrastructure development and 30% on commercialization efforts. Venture capital funding has grown by 27% annually, with over 45 deals recorded between 2023 and 2026. Additionally, pharmaceutical companies are allocating nearly 12% of their annual budgets to additive manufacturing technologies.

Mergers and acquisitions have also increased, with over 18 strategic partnerships formed in 2025. Collaborative agreements between pharmaceutical companies and technology providers have resulted in a 41% increase in production efficiency. Cross-border collaborations have expanded by 29%, enhancing technological capabilities and market reach.

New Product

New product development in the 3D Printed Drugs Market has accelerated, with over 52% of new drug formulations incorporating additive manufacturing technologies in 2025. Performance improvements include a 28% increase in drug efficacy and a 19% reduction in side effects. Additionally, over 65 new patents were filed, reflecting strong innovation trends.

Advanced formulations such as multi-layer tablets and controlled-release drugs have improved patient compliance by 34%. These innovations continue to drive the 3D Printed Drugs Market.

Recent Development in United Kingdom 3D Printed Drugs Market

- 2026: Production capacity increased by 22%, reaching over 13 million units due to expansion of manufacturing facilities.

- 2025: Investment in R&D grew by 38%, resulting in over 60 new drug formulations developed.

- 2024: Adoption rates increased by 29%, with more than 40 hospitals integrating 3D printing technologies.

Research Methodology for United Kingdom 3D Printed Drugs Market

The research methodology involves a combination of primary and secondary research techniques. Primary research includes interviews with industry experts, pharmaceutical companies, and healthcare providers, representing over 65% of data validation. Secondary research involves analysis of company reports, government publications, and industry databases. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within a 5% margin of error. Data triangulation methods are applied to validate findings, while forecasting models incorporate historical data from 2022–2024 and current trends from 2025–2026. This comprehensive approach ensures reliable insights into the 3D Printed Drugs Market.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.