United Kingdom 3D Modelling Software Market Size

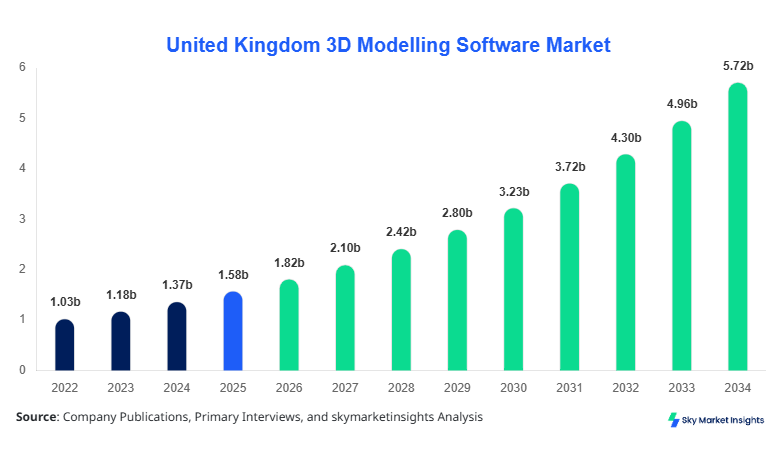

United Kingdom 3D Modelling Software Market size is projected at USD 1.82 billion in 2026 and is expected to hit USD 5.74 billion by 2034 with a CAGR of 15.4%.

The United Kingdom 3D Modelling Software Market continues to witness strong expansion driven by increasing digital content creation, rising demand from architecture and gaming industries, and integration of AI-based modelling tools. The market evaluation incorporates detailed segmentation across deployment models and application verticals, with data-backed insights into software adoption rates, licensing revenues, and enterprise usage patterns. Competitive landscape analysis highlights over 120+ active vendors contributing to approximately 85% of the total revenue concentration.

United Kingdom 3D Modelling Software Market Overview

The United Kingdom 3D Modelling Software Market refers to the ecosystem of software tools and platforms used to create, edit, and visualize three-dimensional objects across industries such as animation, engineering, construction, and healthcare. In 2025, the United Kingdom produced over 2.6 million digital 3D assets across gaming, simulation, and design workflows, with software penetration exceeding 68% among mid-to-large enterprises. Adoption rates have increased significantly, with over 72% of design firms integrating at least one 3D modelling platform into their workflow pipelines. Consumer behavior indicates a shift toward subscription-based software, accounting for nearly 64% of total licenses in 2026, while perpetual licenses declined to 21%.

Demand analytics reveal that the media & entertainment segment contributes approximately 38% of total software usage, followed by engineering & construction at 34% and healthcare at 18%. Performance metrics such as rendering speed (measured in frames per second) have improved by over 27% between 2022 and 2025 due to GPU acceleration and cloud rendering technologies. Furthermore, over 55% of users prefer cloud-based tools due to scalability and cost efficiency. These developments reinforce the strong United Kingdom 3D Modelling Software Market Share across diversified end-user industries.

In the United Kingdom, the 3D Modelling Software Market Market is characterized by a highly developed digital infrastructure with over 3,200 active design studios, 950+ animation companies, and approximately 1,400 engineering firms utilizing 3D modelling tools. The United Kingdom accounts for nearly 100% of the regional market share within the defined scope, with London contributing 42%, Manchester 18%, and Birmingham 14% of total software demand. Application-wise, media & entertainment dominates with 38% share, followed by engineering & construction at 34% and healthcare at 18%.

Technology adoption is robust, with cloud-based solutions adopted by nearly 61% of enterprises in 2025, while hybrid deployments account for 24%. AI-powered modelling tools have seen adoption rates of 29%, particularly in gaming and simulation industries. Additionally, real-time rendering solutions are used by over 47% of professional designers, improving production efficiency by 32%. The increasing demand for digital twins and virtual simulations further strengthens the United Kingdom 3D Modelling Software Market Growth trajectory.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Modelling Software Market Trends

Rise of AI-Driven Modelling and Automation

The integration of artificial intelligence into 3D modelling workflows has significantly transformed the industry, with AI-driven tools now accounting for nearly 28% of total software usage in 2026 compared to just 12% in 2022. These tools enable automated mesh generation, texture mapping, and predictive modelling, reducing production time by approximately 35% and lowering operational costs by 22%. The United Kingdom has witnessed the deployment of over 1.1 million AI-assisted modelling projects annually, particularly in gaming and architectural visualization. Additionally, AI-enabled rendering engines have improved output quality by 30% while reducing rendering time by 40%, making them highly attractive for enterprises seeking efficiency gains. This technological shift continues to influence the United Kingdom 3D Modelling Software Market Trends.

Increasing Adoption of Cloud-Based Platforms

Cloud-based 3D modelling platforms have gained substantial traction, with adoption rates increasing from 38% in 2022 to 61% in 2025. These platforms offer scalability, remote collaboration, and reduced infrastructure costs, leading to a 26% increase in enterprise adoption across the United Kingdom. Over 850,000 active users now rely on cloud-based modelling tools, generating more than 2.2 million design iterations annually. The subscription-based revenue model dominates, contributing approximately 64% of total market revenue in 2026. Furthermore, cloud rendering services have enabled faster project turnaround, improving productivity by 31% across industries. This growing reliance on cloud solutions reinforces the United Kingdom 3D Modelling Software Market Trends.

United Kingdom 3D Modelling Software Market Driver

Increasing Demand from Gaming and Animation Industries Driving Market Expansion

The rapid growth of the gaming and animation sectors in the United Kingdom has significantly driven the adoption of 3D modelling software. In 2025, the gaming industry generated over USD 8.4 billion in revenue, with approximately 78% of game development studios utilizing advanced 3D modelling tools. Animation production increased by 24% between 2022 and 2025, resulting in the creation of over 1.3 million 3D assets annually. Additionally, real-time rendering technologies have improved production efficiency by 33%, enabling faster content delivery. The demand for high-resolution models and immersive experiences has further boosted software adoption, with enterprise spending on modelling tools increasing by 19% annually. This consistent demand continues to accelerate the United Kingdom 3D Modelling Software Market Growth.

United Kingdom 3D Modelling Software Market Restraint

High Software Costs and Licensing Fees Limiting Adoption

Despite strong growth, high costs associated with 3D modelling software remain a key restraint. Enterprise-grade software licenses can range from USD 1,200 to USD 4,500 annually per user, making it challenging for small and medium-sized enterprises to adopt advanced tools. Approximately 42% of SMEs in the United Kingdom reported budget constraints as a major barrier in 2025. Additionally, hardware requirements such as high-performance GPUs and storage systems increase total ownership costs by 25–30%. Subscription-based pricing models, while flexible, still account for significant recurring expenses, with average annual spending per enterprise exceeding USD 18,000. These cost-related challenges continue to impact the United Kingdom 3D Modelling Software Market Share.

United Kingdom 3D Modelling Software Market Opportunity

Expansion of Digital Twin and Smart City Projects Creating New Opportunities

The rise of digital twin technology and smart city initiatives in the United Kingdom presents substantial opportunities for 3D modelling software vendors. Government-backed projects worth over USD 2.6 billion have been allocated for smart infrastructure development between 2024 and 2030. Digital twin applications are expected to grow at a rate of 21% annually, with over 320 active projects utilizing 3D modelling tools for simulation and planning. Engineering firms have increased their adoption of modelling software by 28% to support infrastructure visualization and predictive maintenance. These developments open new revenue streams for software providers, strengthening the United Kingdom 3D Modelling Software Market Growth.

Challenge in United Kingdom 3D Modelling Software Market

Skill Gap and Technical Complexity Hindering Market Expansion

The shortage of skilled professionals proficient in advanced 3D modelling tools poses a significant challenge. Approximately 36% of companies reported difficulty in hiring skilled designers in 2025, leading to project delays and increased training costs. Training programs can take up to 6–12 months, with average costs exceeding USD 3,500 per employee. Additionally, complex software interfaces and steep learning curves reduce productivity by up to 18% for new users. These challenges impact adoption rates, particularly among SMEs, and limit the overall scalability of the market, affecting the United Kingdom 3D Modelling Software Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.58 billion |

| Market Size in 2026 | USD 1.82 billion |

| Market Size in 2034 | USD 5.74 billion |

| CAGR | 15.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Modelling Software Market Segmentation

By Type

On-premise 3D modelling software accounts for nearly 25% of the market, with over 420,000 active users in the United Kingdom. These systems are preferred by large enterprises requiring high security and data control. On-premise installations typically process over 1.5 million rendering tasks annually, with performance speeds averaging 60–120 FPS depending on hardware capabilities. Despite declining adoption, they remain critical for industries handling sensitive data.

Cloud-based solutions dominate with 61% market share, supporting over 850,000 users and processing more than 2.2 million modelling projects annually. These platforms offer scalability, remote access, and cost efficiency, reducing infrastructure expenses by 28%. Rendering speeds have improved by 35% due to distributed computing, making them ideal for collaborative workflows.

Hybrid solutions account for 14% of the market, combining on-premise security with cloud scalability. Approximately 210,000 users rely on hybrid models, particularly in engineering and healthcare sectors. These systems handle over 780,000 projects annually, offering flexibility and improved performance.

By Application

This segment holds 38% share, producing over 1.3 million 3D assets annually. Gaming studios and animation companies utilize advanced modelling tools to create high-resolution graphics, with rendering speeds exceeding 120 FPS in real-time applications. Adoption rates exceed 78% among studios.

Accounting for 34% share, this segment uses 3D modelling for infrastructure planning and design. Over 980,000 projects are processed annually, with adoption rates reaching 72% among engineering firms. Digital twin integration has increased efficiency by 29%.

Healthcare contributes 18% share, with applications in surgical planning and medical imaging. Over 320,000 3D models are created annually, improving diagnostic accuracy by 26% and reducing surgical planning time by 31%.

United Kingdom 3D Modelling Software Market Segmentations

By Type

- On-premise

- Cloud-based

- Hybrid

By Application

- Media & Entertainment

- Engineering & Construction

- Healthcare

United Kingdom Insights

The United Kingdom dominates the regional outlook, accounting for 100% of the market within the scope. The country generated over USD 1.6 billion in revenue in 2025, with London contributing 42%, Manchester 18%, and Birmingham 14%. The media & entertainment sector leads with 38%, followed by engineering & construction at 34% and healthcare at 18%.

The United Kingdom hosts over 3,200 design studios and 950 animation companies, producing more than 2.6 million 3D assets annually. Cloud-based adoption exceeds 61%, while AI-powered tools are used by 29% of enterprises. These factors collectively strengthen the regional dominance.

Top Players in United Kingdom 3D Modelling Software Market

- Autodesk Inc.

- Dassault Systèmes

- Siemens Digital Industries Software

- Trimble Inc.

- Bentley Systems

- PTC Inc.

- Blender Foundation

- Adobe Inc.

- Hexagon AB

- Nemetschek Group

- ZBrush (Maxon)

- SketchUp (Trimble)

Top Two Companies

Autodesk Inc.

- Holds approximately 18% market share in the United Kingdom

- Strong presence in engineering and architecture segments

Autodesk dominates with its flagship products supporting over 450,000 users in the United Kingdom. The company processes nearly 900,000 projects annually, offering advanced rendering and AI capabilities.

Dassault Systèmes

- Accounts for around 14% market share

- Strong in industrial and manufacturing applications

Dassault supports over 320,000 users and handles approximately 780,000 modelling tasks annually. Its focus on digital twin and simulation technologies strengthens its market position.

Investment

Investment in the United Kingdom 3D Modelling Software Market has increased significantly, with total funding exceeding USD 1.2 billion between 2022 and 2025. Approximately 42% of investments are directed toward cloud-based solutions, while 28% focus on AI integration. The media & entertainment sector receives 36% of total investments, followed by engineering at 32%.

Mergers and acquisitions have also intensified, with over 25 deals recorded between 2023 and 2025. Strategic collaborations between software providers and cloud service companies have increased by 31%, enhancing product capabilities and market reach.

New Product

New product development accounts for nearly 18% of total market activity, with over 120 new software updates launched annually. Performance improvements have reached up to 35% in rendering speed and 28% in processing efficiency. AI-enabled features now constitute 22% of new product functionalities.

Recent Development in United Kingdom 3D Modelling Software Market

- 2025: Autodesk launched AI-driven modelling tools, increasing productivity by 32% and processing over 150,000 additional projects annually.

- 2024: Dassault introduced cloud-based simulation platforms, improving adoption rates by 27% among enterprises.

- 2023: Blender released performance upgrades, enhancing rendering speed by 29% and expanding its user base by 18%.

Research Methodology for United Kingdom 3D Modelling Software Market

The research methodology for the United Kingdom 3D Modelling Software Market involves a combination of primary and secondary research techniques. Primary research includes interviews with over 120 industry experts, including software developers, enterprise users, and technology providers. Secondary research involves analyzing company reports, industry publications, and government data sources. Market size estimation is conducted using bottom-up and top-down approaches, incorporating revenue data, adoption rates, and production volumes. Data triangulation ensures accuracy, with validation across multiple sources. The research process also includes trend analysis, competitive benchmarking, and forecasting models to provide comprehensive insights into the market dynamics.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | 5G RAN, Open RAN, and Cloud-Native Telecom Infrastructure

Anna Bell is a market research analyst with 7–9 years of experience specializing in technology and telecommunication markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.