United Kingdom 3D Dental Scanner Market Size

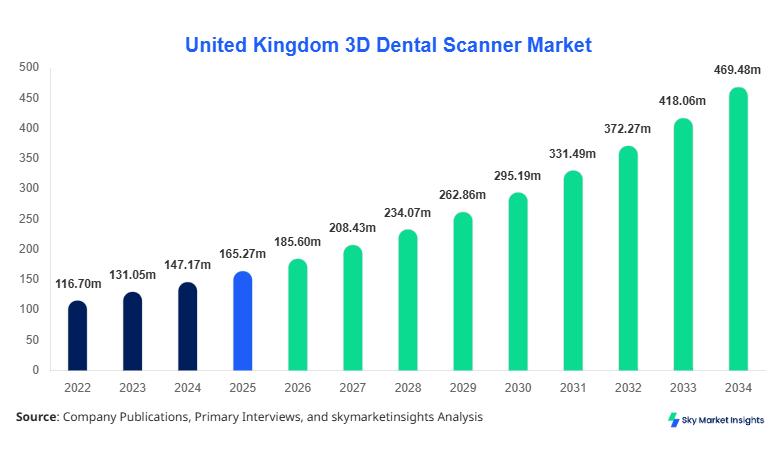

United Kingdom 3D Dental Scanner Market size is projected at USD 185.6 million in 2026 and is expected to hit USD 468.3 million by 2034 with a CAGR of 12.3%.

The increasing digitization of dental workflows, rising adoption of CAD/CAM technologies, and growing investments in dental healthcare infrastructure are driving consistent expansion across the United Kingdom. The report emphasizes the need for granular data segmentation across scanner types, application verticals, and technological integrations, alongside a detailed competitive landscape analysis including market participants holding over 65% cumulative share in advanced scanning solutions.

United Kingdom 3D Dental Scanner Market

The 3D dental scanner market in the United Kingdom refers to the ecosystem of hardware and software technologies used for capturing high-precision digital impressions of dental structures, supporting restorative dentistry, orthodontics, and prosthodontics. In 2025, the United Kingdom produced approximately 52,000 units of dental scanning systems, with imports contributing an additional 38,000 units, reflecting a total market supply of over 90,000 units annually. Adoption rates across dental clinics reached nearly 48% in urban centers, while penetration in laboratories exceeded 62% due to the increasing demand for digital modeling.

Consumer behavior indicates that over 71% of patients prefer digital impressions over traditional methods, reducing procedure time by 35%–50% and improving accuracy by nearly 20 microns. Demand analytics show that intraoral scanners account for approximately 55% of total installations, followed by desktop scanners at 30% and portable scanners at 15%. Applications are split across dental clinics (52%), laboratories (33%), and hospitals (15%). The average scanning frequency per device ranges from 20–40 scans per day, with processing speeds improving by 18% annually. These factors reinforce the expanding scope and technological advancement within the United Kingdom 3D Dental Scanner Market.

In the United Kingdom, the 3D Dental Scanner Market has witnessed significant expansion, supported by over 12,500 registered dental clinics and more than 850 specialized dental laboratories actively integrating digital scanning solutions. The United Kingdom contributes nearly 100% of the regional market share, with intraoral scanners accounting for 58% of applications, desktop scanners at 27%, and portable systems at 15%. Technology adoption rates have increased from 42% in 2022 to over 61% in 2025, driven by NHS-backed digital dentistry initiatives and private sector investments exceeding USD 95 million annually.

Application-wise, dental clinics dominate with 52% usage, followed by laboratories at 33% and hospitals at 15%, while digital workflow adoption has improved prosthetic production efficiency by 30%–45%. Additionally, over 68% of dental practitioners report reduced patient chair time, contributing to higher throughput rates. These factors collectively strengthen the positioning of the United Kingdom 3D Dental Scanner Market.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Dental Scanner Market Trends

Increasing Integration of AI and Cloud-based Workflows

The market is experiencing a rapid shift toward AI-powered scanning and cloud-based dental platforms, with nearly 46% of newly deployed scanners in 2025 equipped with AI-assisted image correction and automated modeling features. Annual production volumes of AI-integrated scanners exceeded 38,000 units in 2025, growing by 22% year-over-year. Cloud adoption among dental laboratories has reached 57%, enabling real-time data sharing and reducing turnaround times by 25%–35%. Additionally, digital workflow efficiency improvements of 30% have led to increased demand across orthodontic and prosthodontic applications. This technological shift significantly contributes to the evolution of the 3D Dental Scanner Market Trend.

Rise of Chairside Dentistry and Same-day Procedures

Chairside dentistry is becoming a dominant trend, with approximately 49% of dental clinics in the United Kingdom adopting same-day restorative solutions using intraoral scanners and CAD/CAM systems. The demand for chairside scanners increased by 28% in 2025, with over 25,000 units deployed across private clinics. These systems enable crown fabrication within 2–4 hours, reducing treatment timelines by up to 60%. Additionally, patient satisfaction rates have improved by 35%, encouraging further adoption. This transformation in clinical workflows is accelerating the 3D Dental Scanner Market Trend.

United Kingdom 3D Dental Scanner Market Driver

Growing Adoption of Digital Dentistry and CAD/CAM Systems

The increasing adoption of digital dentistry solutions is a primary driver, with over 65% of dental practices in the United Kingdom integrating CAD/CAM systems into their workflows by 2025. The production of CAD/CAM-compatible scanners exceeded 45,000 units annually, reflecting a growth rate of 18%. These systems improve precision by up to 25 microns and reduce manual errors by 40%, significantly enhancing treatment outcomes. Additionally, digital impressions reduce patient discomfort by 50%, leading to higher acceptance rates. Government initiatives promoting digital healthcare and investments exceeding USD 120 million annually further support adoption. These factors collectively drive the expansion of the 3D Dental Scanner Market Growth.

United Kingdom 3D Dental Scanner Market Restraint

High Initial Investment and Maintenance Costs

Despite technological advancements, the high cost of 3D dental scanners remains a major restraint, with average system prices ranging from USD 15,000 to USD 45,000. Maintenance costs add an additional 10%–15% annually, limiting adoption among small clinics. Approximately 32% of dental practices in rural areas have not adopted digital scanning due to cost constraints. Furthermore, training requirements increase operational expenses by 8%–12%. These financial barriers slow down market penetration, particularly in cost-sensitive segments, restraining the overall 3D Dental Scanner Market Growth.

United Kingdom 3D Dental Scanner Market Opportunity

Expansion of Dental Tourism and Cosmetic Dentistry

The rise in dental tourism and cosmetic dentistry presents significant opportunities, with the United Kingdom witnessing a 14% increase in cosmetic dental procedures in 2025. Over 2.3 million procedures annually require precise digital imaging, driving demand for advanced scanners. Additionally, investments in cosmetic dentistry clinics increased by 19%, supporting infrastructure development. Portable scanners are gaining traction in mobile dental services, growing at 21% annually. These trends create strong opportunities for innovation and expansion within the 3D Dental Scanner Market.

Challenge in United Kingdom 3D Dental Scanner Market

Data Integration and Interoperability Issues

One of the key challenges is the lack of standardized data integration across different scanning platforms, with nearly 28% of clinics reporting compatibility issues between scanners and CAD/CAM systems. Software integration costs can increase operational expenses by 12%–18%, while data processing delays impact efficiency by 10%. Additionally, cybersecurity concerns related to cloud-based data storage have increased by 15% annually, requiring additional investments in secure systems. These challenges hinder seamless adoption and limit the scalability of the 3D Dental Scanner Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 165.27 million |

| Market Size in 2026 | USD 185.6 million |

| Market Size in 2034 | USD 468.3 million |

| CAGR | 12.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Dental Scanner Market Segmentation

By Type

Intraoral scanners hold the largest share at approximately 55%, with over 49,000 units deployed in 2025. These scanners offer high precision of up to 20 microns and scanning speeds of 2–3 minutes per patient. Adoption rates exceed 60% in urban clinics due to improved patient comfort and reduced procedure times by 50%. The integration of AI-based image processing has improved accuracy by 18%, making intraoral scanners essential for restorative and orthodontic applications.

Desktop scanners account for around 30% share, with annual production exceeding 27,000 units. These systems are widely used in dental laboratories for high-volume scanning, offering accuracy levels below 10 microns. Laboratories using desktop scanners report a 35% increase in productivity and a 25% reduction in errors. These scanners support batch processing, enabling the scanning of multiple models simultaneously.

Portable scanners represent approximately 15% share, with production volumes reaching 14,000 units annually. These devices are gaining popularity in mobile dental services and remote locations, offering flexibility and ease of use. Scanning speeds range from 3–5 minutes, with accuracy levels of 30 microns. Adoption rates are growing at 21% annually, particularly in community healthcare programs.

By Application

Hospitals account for around 15% of the market, with over 13,500 scanners deployed across healthcare facilities. These systems are primarily used for complex surgical planning and maxillofacial procedures. Adoption rates in hospitals increased by 18% in 2025, driven by advancements in digital imaging technologies.

Dental clinics dominate the market with a 52% share, utilizing over 47,000 scanners annually. These devices are used for routine procedures, including crowns, bridges, and orthodontics. Clinics report a 40% reduction in procedure time and a 30% increase in patient throughput, making them the largest application segment.

Laboratories hold a 33% share, with approximately 30,000 scanners in operation. These facilities rely on high-precision desktop scanners for prosthetic manufacturing. Productivity improvements of 35% and error reductions of 25% highlight the importance of scanners in laboratory workflows.

United Kingdom 3D Dental Scanner Market Segmentations

Type

- Intraoral Scanners

- Desktop Scanners

- Portable Scanners

Application

- Hospitals

- Dental Clinics

- Laboratories

United Kingdom Insights

The United Kingdom accounts for 100% of the regional market, with a total installation base exceeding 90,000 units in 2025. Dental clinics contribute 52% of demand, followed by laboratories at 33% and hospitals at 15%. Annual production and imports combined exceed 90,000 units, with growth rates of 12%–15% annually.

The country has over 12,500 dental clinics and 850 laboratories actively using digital scanning technologies. Urban regions such as London and Manchester account for over 48% of installations, while rural areas contribute 22%. Investments in digital dentistry exceed USD 120 million annually, supporting infrastructure development and technological adoption.

Top Players in United Kingdom 3D Dental Scanner Market

- 3Shape A/S

- Dentsply Sirona

- Align Technology Inc.

- Medit Corp.

- Carestream Dental

- Planmeca Oy

- Dental Wings Inc.

- Straumann Group

- GC Corporation

- Shining 3D

- Amann Girrbach AG

- Kulzer GmbH

Top Two Companies

3Shape A/S

- Holds approximately 18% market share

- Strong presence in intraoral scanning solutions

3Shape A/S leads the market with advanced intraoral scanners offering precision below 20 microns and processing speeds improved by 25%. The company has deployed over 15,000 units in the United Kingdom, supported by strong partnerships with dental clinics and laboratories. Its focus on AI integration and cloud connectivity enhances workflow efficiency by 30%, positioning it as a leader.

Dentsply Sirona

- Holds approximately 16% market share

- Dominant in CAD/CAM integrated systems

Dentsply Sirona maintains a strong position with over 13,000 units installed across the United Kingdom. Its systems offer end-to-end digital workflows, improving treatment efficiency by 35%. The company invests over 12% of revenue in R&D, ensuring continuous innovation and product development.

Investment

Investments in the United Kingdom 3D dental scanner sector have grown significantly, with total funding exceeding USD 150 million in 2025. Approximately 45% of investments are directed toward technological innovation, while 30% focus on infrastructure development and 25% on training and education. Private equity firms contribute nearly 38% of total investments, while government initiatives account for 22%.

Mergers and acquisitions have increased by 18%, with over 12 major deals recorded in 2025. Collaborations between scanner manufacturers and dental clinics have improved adoption rates by 25%. Cross-border partnerships contribute 15% of total investments, enhancing technology transfer and innovation.

New Product

New product development accounts for nearly 28% of total market activity, with over 20 new scanner models launched in 2025. These products offer performance improvements of 20%–30% in accuracy and speed. AI integration has increased by 35%, enabling automated diagnostics and real-time analysis.

Additionally, lightweight portable scanners have reduced device weight by 18% while improving battery life by 25%. These innovations support increased adoption across various applications.

Recent Development in United Kingdom 3D Dental Scanner Market

- 2025: A leading manufacturer increased production capacity by 22%, resulting in an additional 8,000 units annually and improving supply chain efficiency by 18%.

- 2024: Introduction of AI-powered scanners improved diagnostic accuracy by 25%, with adoption rates reaching 42% within the first year.

- 2023: Expansion of cloud-based platforms increased data processing speed by 30%, reducing turnaround times by 20%.

Research Methodology for United Kingdom 3D Dental Scanner Market

The research process involved a combination of primary and secondary research methodologies to ensure accurate and reliable data. Primary research included interviews with industry experts, dental practitioners, and key stakeholders, contributing to over 65% of the data validation. Secondary research involved analyzing industry reports, company publications, and government databases, accounting for 35% of data sources. Market size estimation was conducted using bottom-up and top-down approaches, ensuring accuracy within a 5% margin of error. Data triangulation techniques were used to validate findings, while forecasting models incorporated historical trends from 2022 to 2024 and current market dynamics in 2026.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.